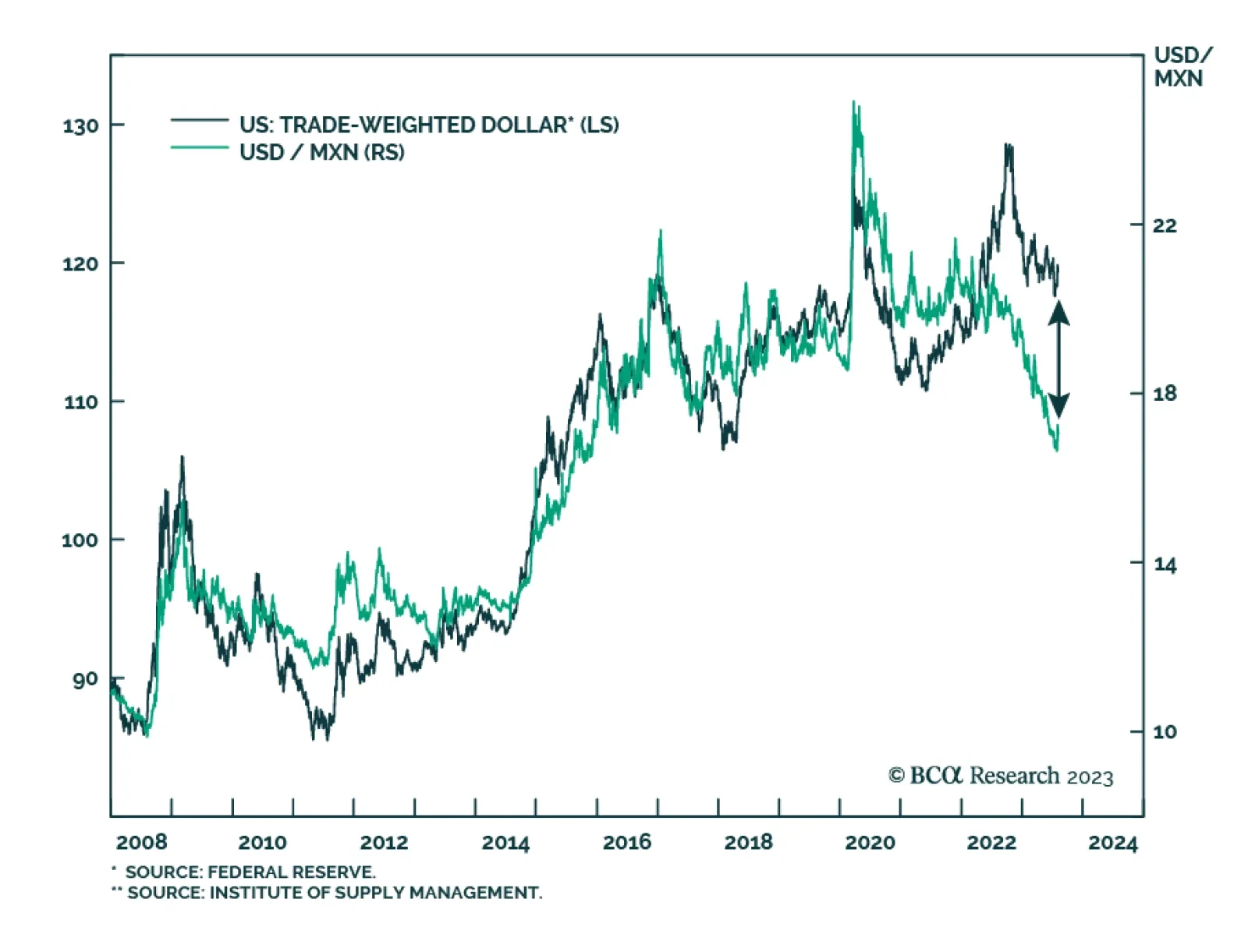

US Dollar

The stock market’s pre-eminent growth sector is not US tech, it is French luxuries. No other sector can compare with French luxuries’ massive and sustained pricing power. The risk for French luxuries is not a China slowdown, the risk is that the structural increase in super-wealth comes to an end. If anything though, the coming disruption from generative AI will boost super-wealth. Ironically therefore, the best investment play on generative AI might be French luxuries.

A global portfolio is likely to return only 5.3% a year over the next decade, compared to 6.7% in the past. Investors either need to lower their return expectations, or take more risk. Our total return methodology remains consistent with previous editions, with changes limited to the Alternatives section.

China has generated 41 percent of the world’s economic growth through the past ten years, al-most double the 22 percent contribution from the US. Now that the Chinese growth engine is failing, we explain why it is arithmetically impossible for world growth to maintain the altitude of the past few decades. And we discuss an important investment implication.

Although the RMB has cheapened, macro conditions are not yet favorable for the Chinese currency. We expect the RMB to decline by at least another 5% in the next six months. A weak currency and subdued economic growth lead us to maintain a cautious stance on Chinese equities.

The global economy will not enjoy an “immaculate disinflation” but will suffer a very maculate one due to China’s growth slowdown and restrictive monetary policy in the developed world. Investors should stay overweight low-beta assets.

China’s extremely high savings rate is the real culprit behind its current economic woes. The authorities have been slow to stimulate the economy, and the risks of “Japanification” have increased. For now, the fact that China is exporting deflation is not such a bad thing. However, if global recession risks were to flare up again, a lethargic Chinese economy would be a cause for concern. Chinese stocks are quite cheap but lack a clear catalyst to move higher. Favor EM markets where earnings and sales estimates have been moving up lately.