US Dollar

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

The US dollar will become a pro-cyclical currency going forward. This regime shift would upend financial market correlations, and most investment portfolios are not positioned for it. A great deal of money is made or lost during regime changes - and one is coming soon. That is why our message remains loud and clear: Get Out of the Dollar (G.O.D.).

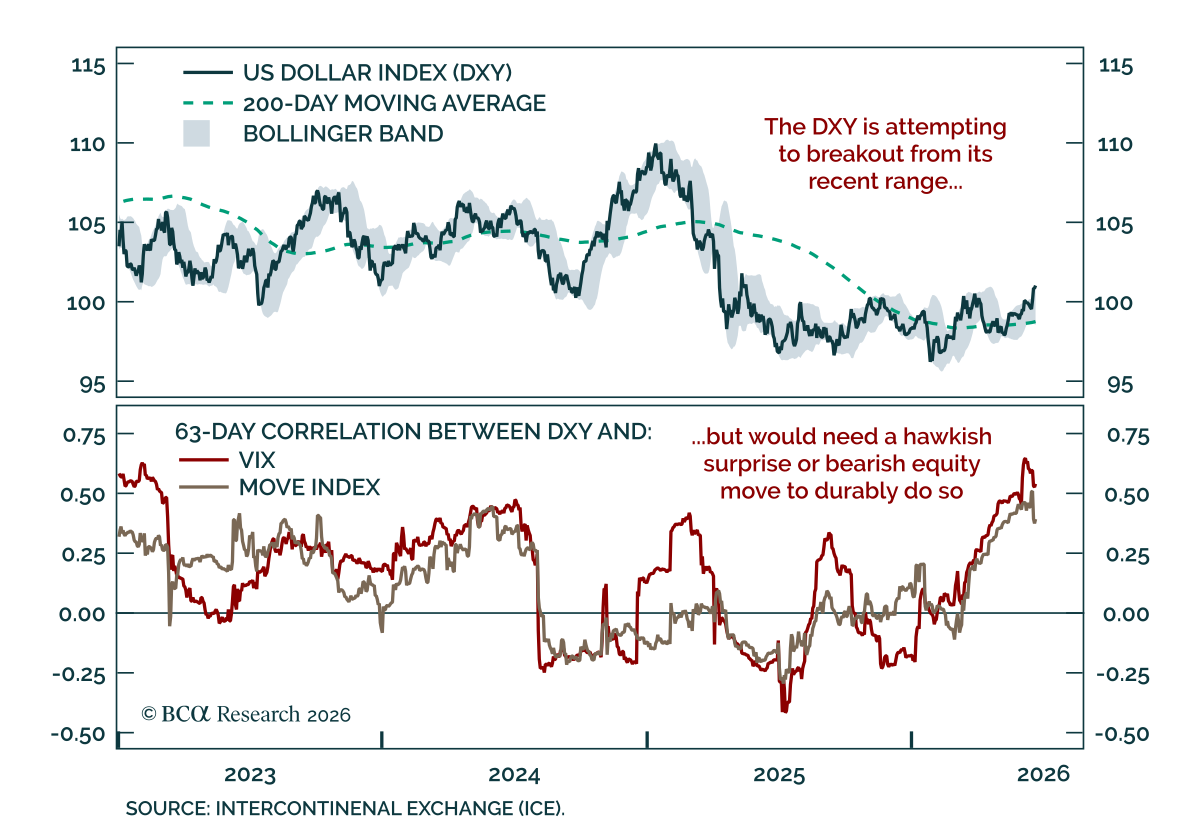

The dollar has had a strong run but its key supports from Fed repricing, positioning, and terms of trade are starting to fade. We close our tactical long USD positions and turn to short USD/JPY, where intervention risk makes yen shorts look increasingly dangerous.

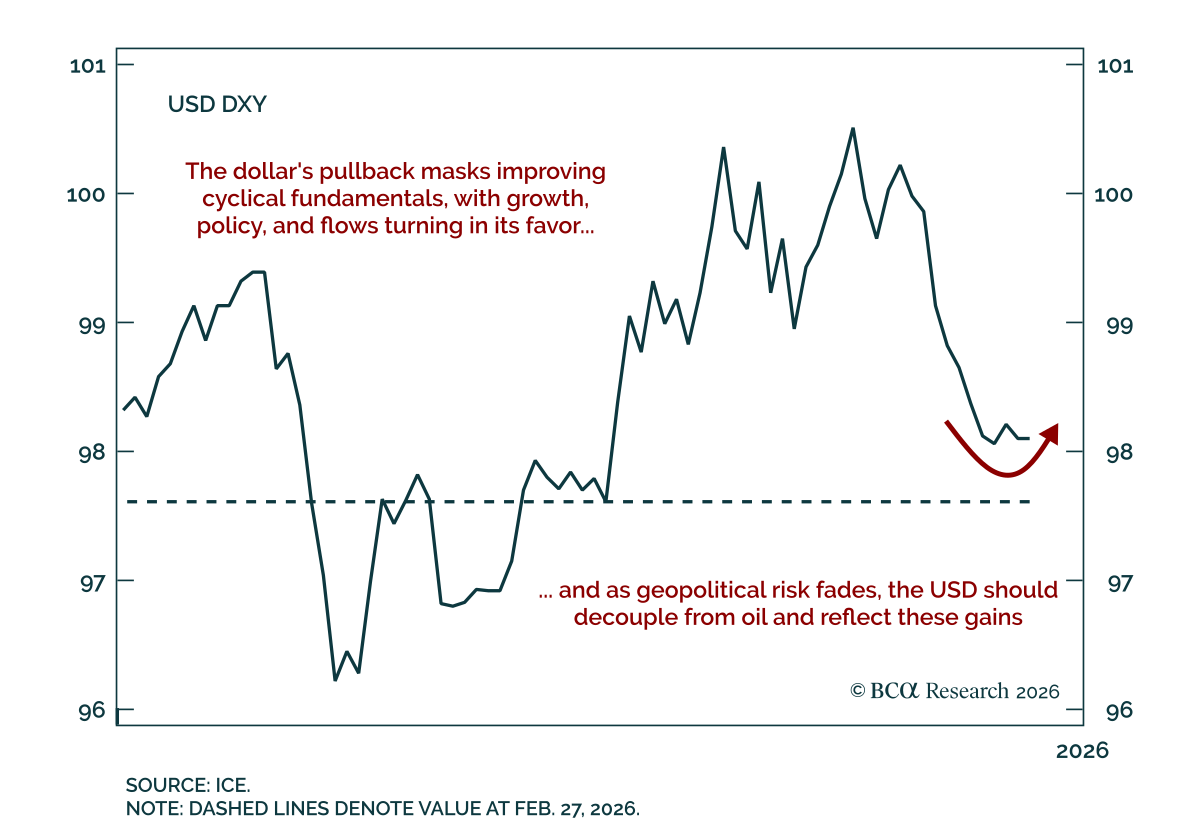

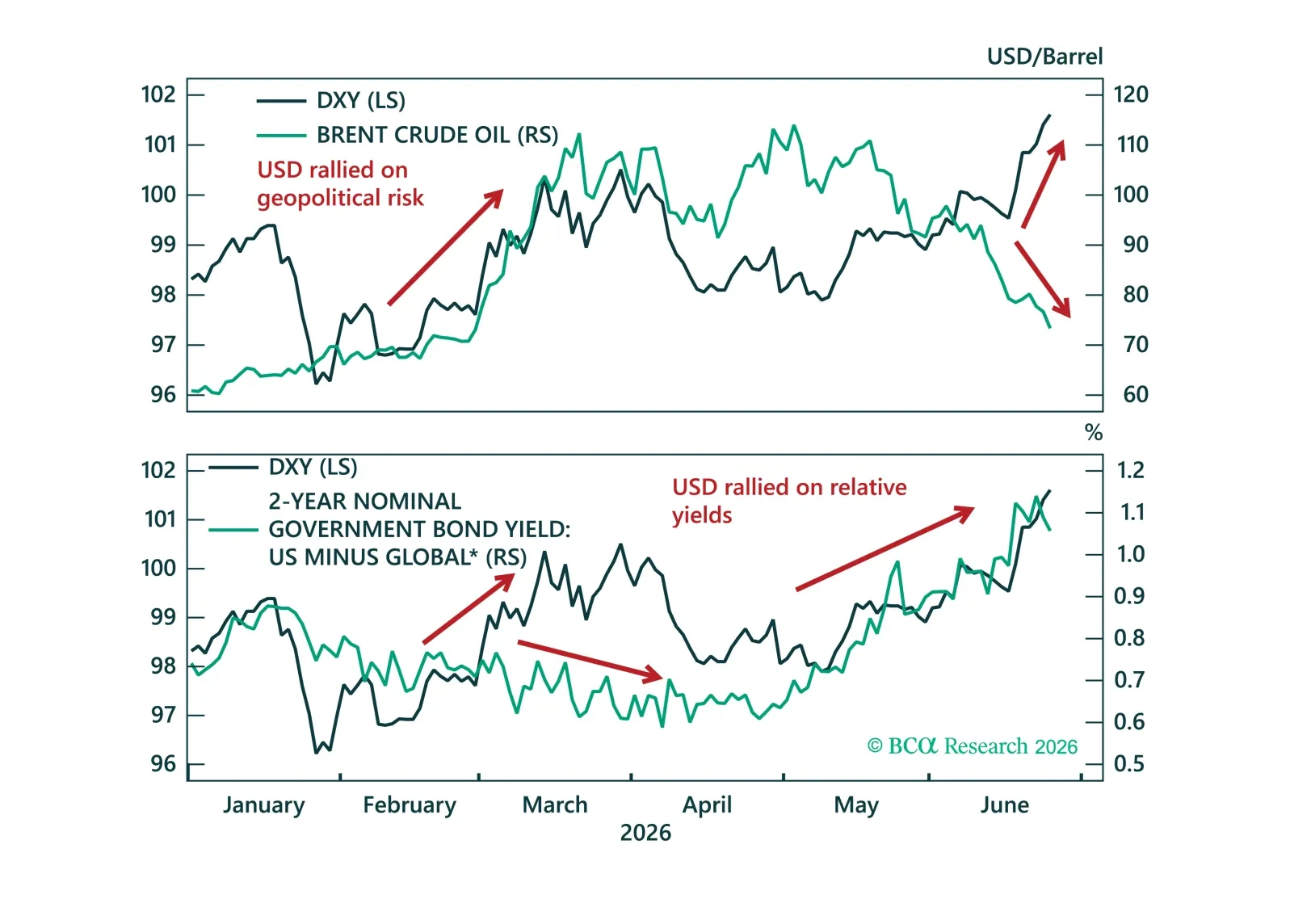

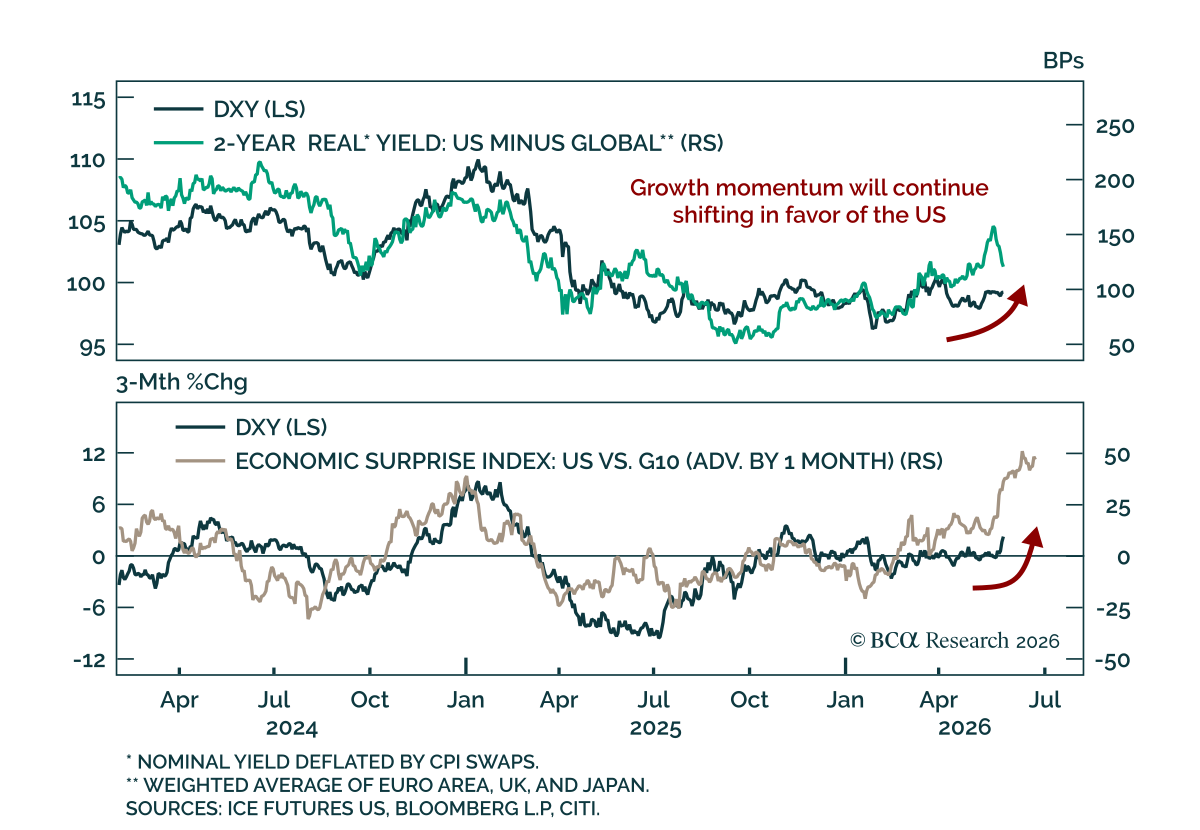

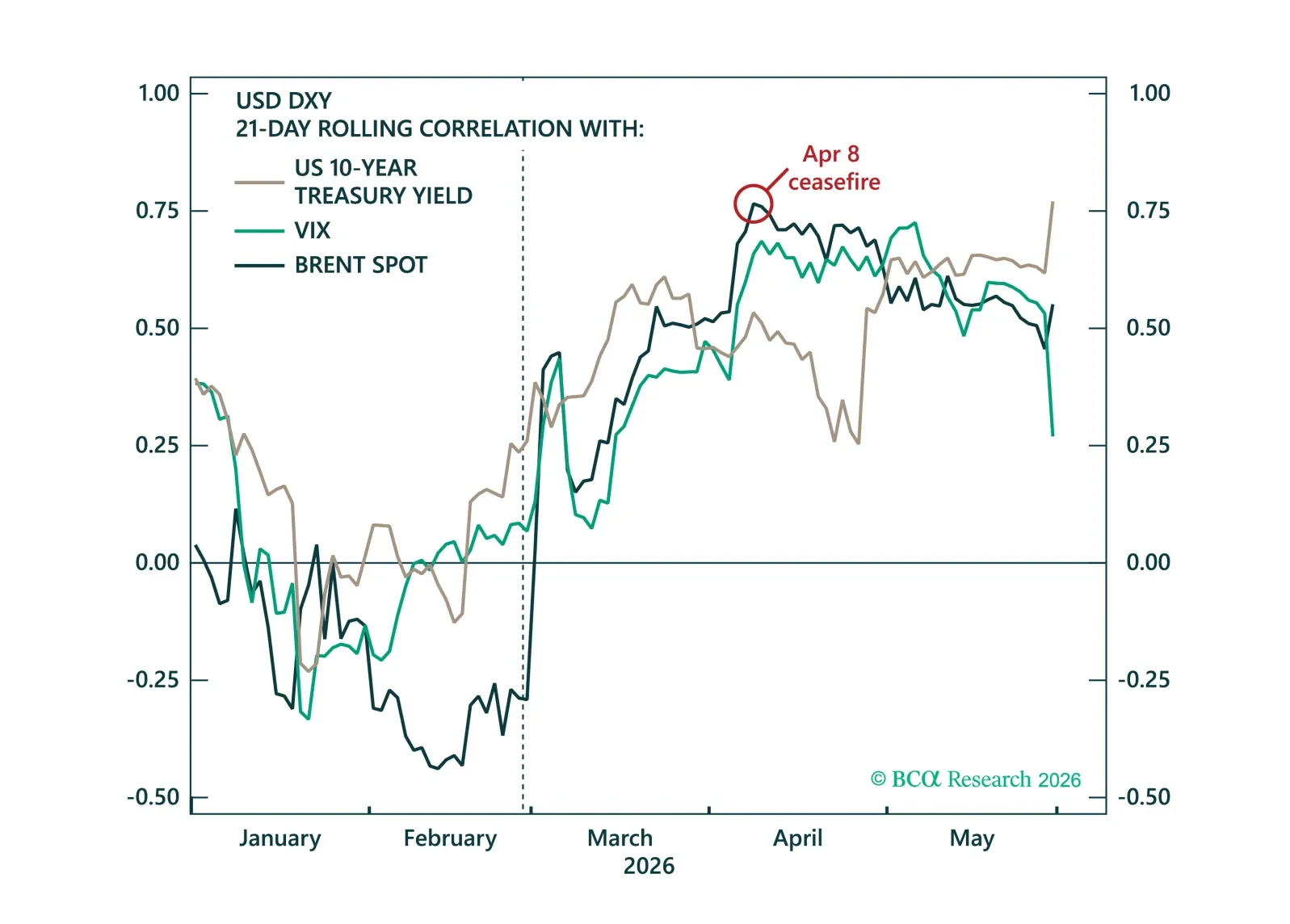

The dollar's muted response to the Iran conflict has led many to question its safe-haven appeal. We argue the opposite – the dollar's defensive properties have returned, while improving growth and rate dynamics should underpin further USD strength in the months ahead.