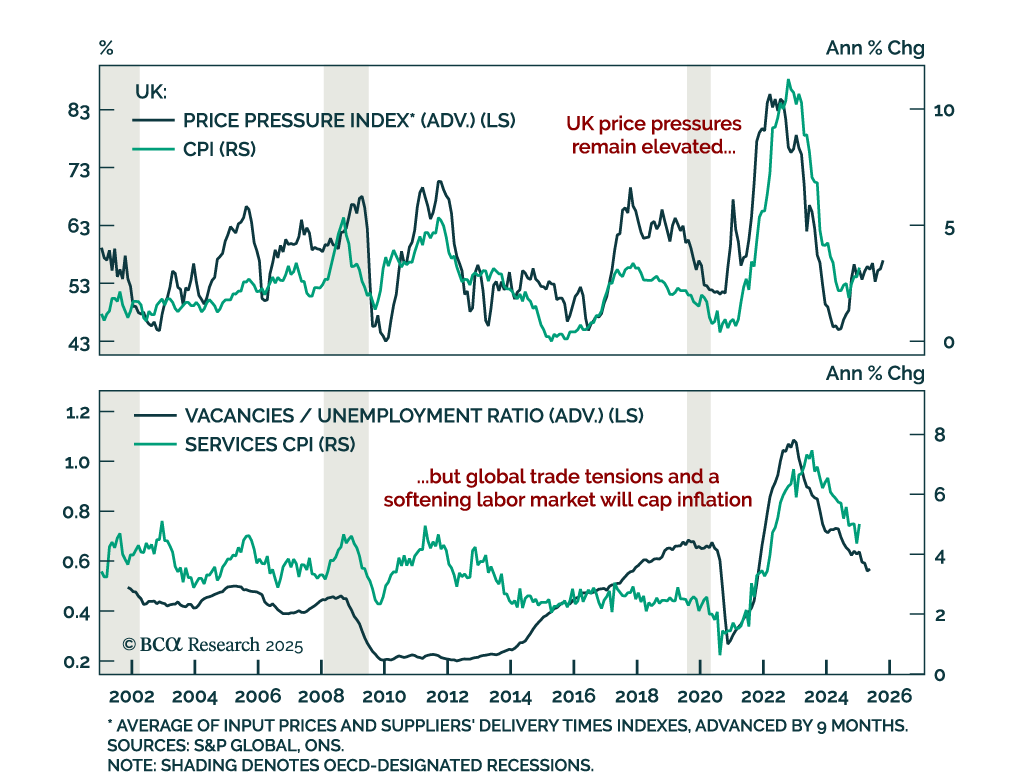

UK

With economic headwinds building and fiscal dynamics shifting, bond markets are at a turning point. Our latest note outlines why German bund yields are set to decline and why UK gilts are poised to outperform — and how to position accordingly.

This report is a quick take on our views on UK bonds and FX, given the recent budget.

Given the meetings between the Bank of Japan, the Bank of England, and the Swiss National Bank, our highest convictions views are:

Overweight UK Gilts. It is also time to sell sterling. We are short sterling, as of 1.30.

Underweight JGBs. Correspondingly, be long the yen.

A short CHF/JPY position remains a core holding. Selling GBP/JPY is also a great trade.

The US (and the UK) is staring down the barrel of a ‘mini-stagflation’ until a deflationary shock arrives to neutralise it. We describe a likely source for the deflationary shock and list three investment conclusions that are valid irrespective of how long it takes for the deflationary shock to arrive. Plus: RCI.B is deeply oversold and ripe for a rebound.

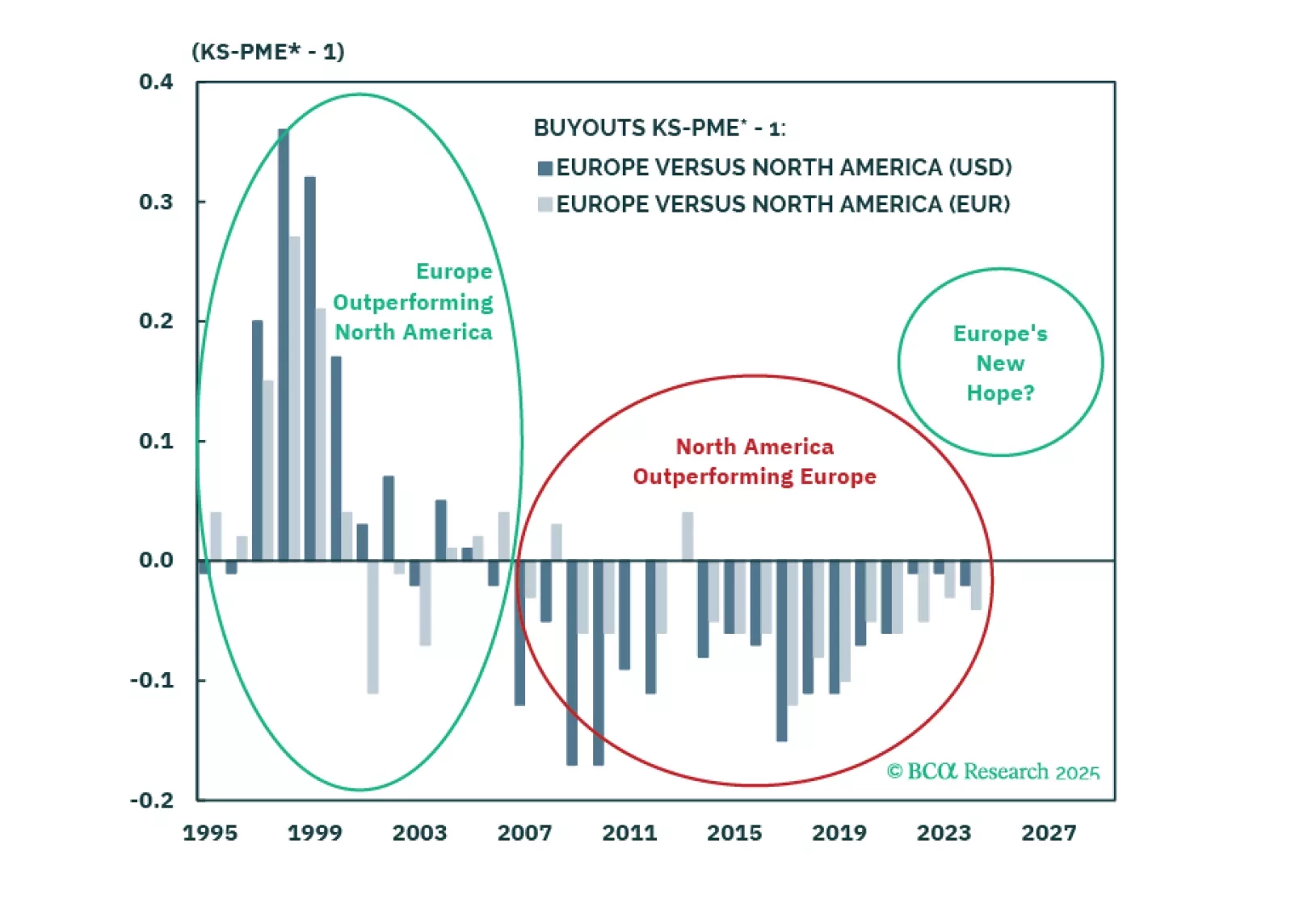

We are at a pivotal moment for Europe, supported by structural reforms and macro catalysts. While expanding credit markets and lower rates favor Private Equity over Private Credit, opportunities vary by segment. Large+ Buyouts are attractive as markets have priced in structural challenges. We downgrade Europe Private Credit, remain neutral on Europe Private Equity broadly but overweight Europe vs. North America in PE portfolios.

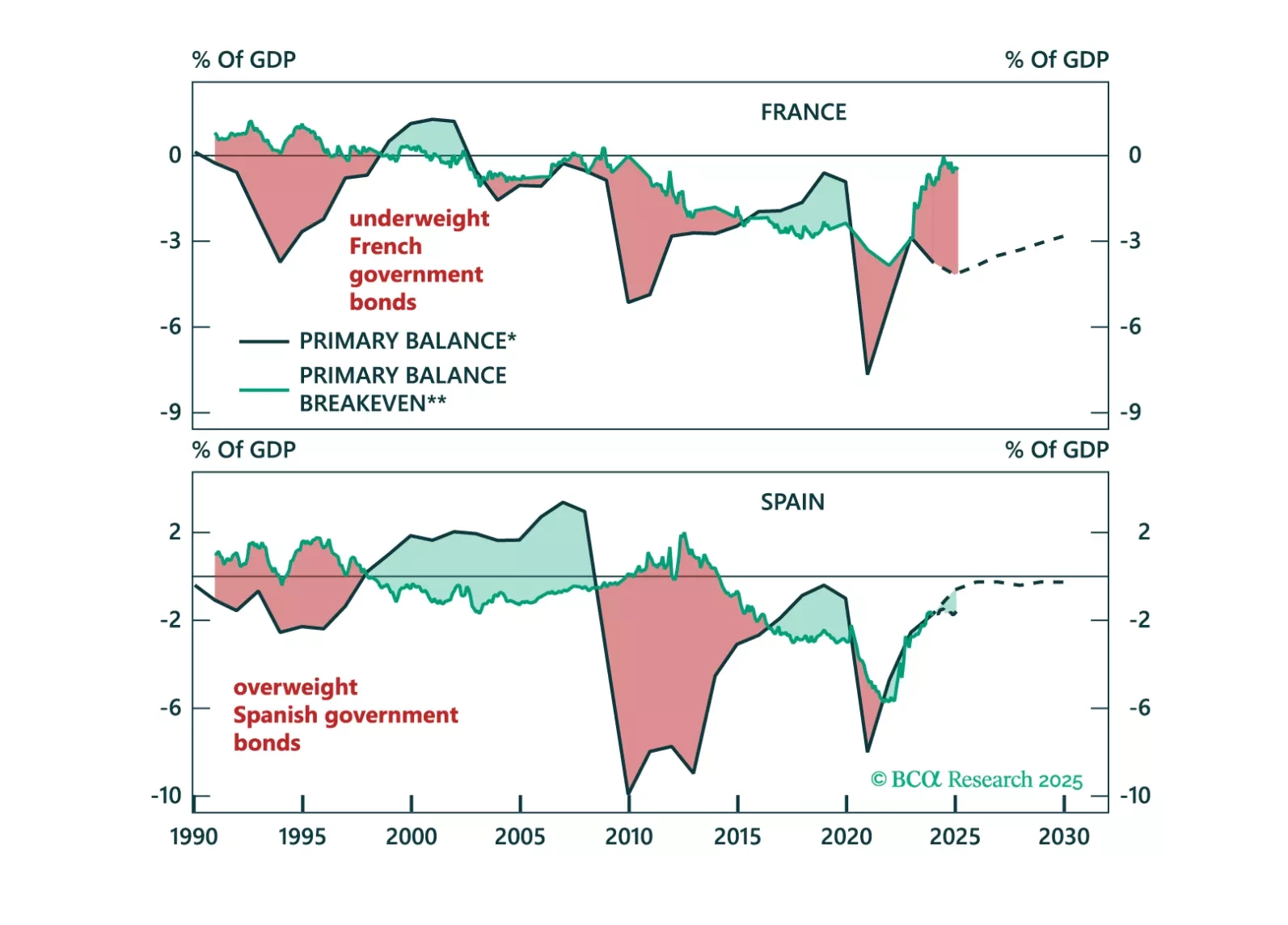

Questions about fiscal risks and their impact on bond markets have become more frequent in client conversations. This Special Report provides a framework to assess a country’s fiscal sustainability and how it affects its bond market outlook. On an individual country basis, Spain has shown a remarkable turnaround in its fiscal sustainability outlook while the fiscal outlook for France continues to deteriorate.