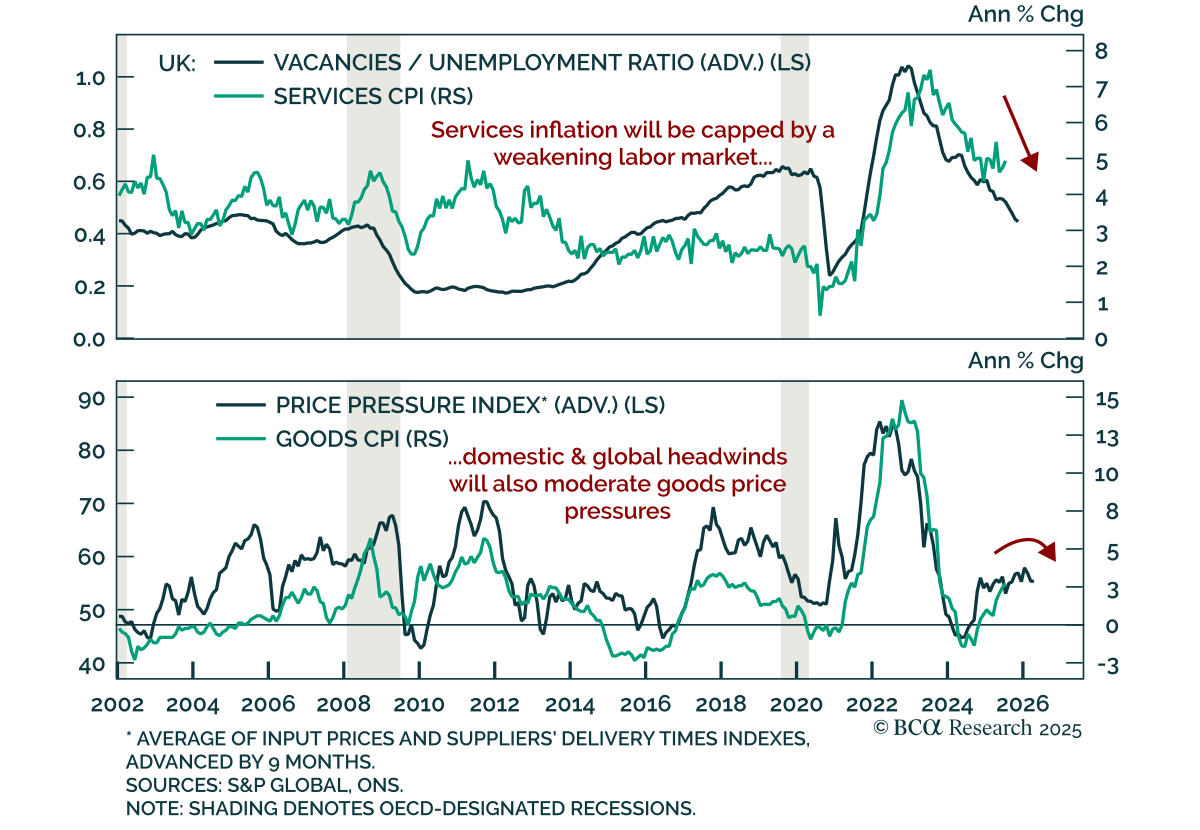

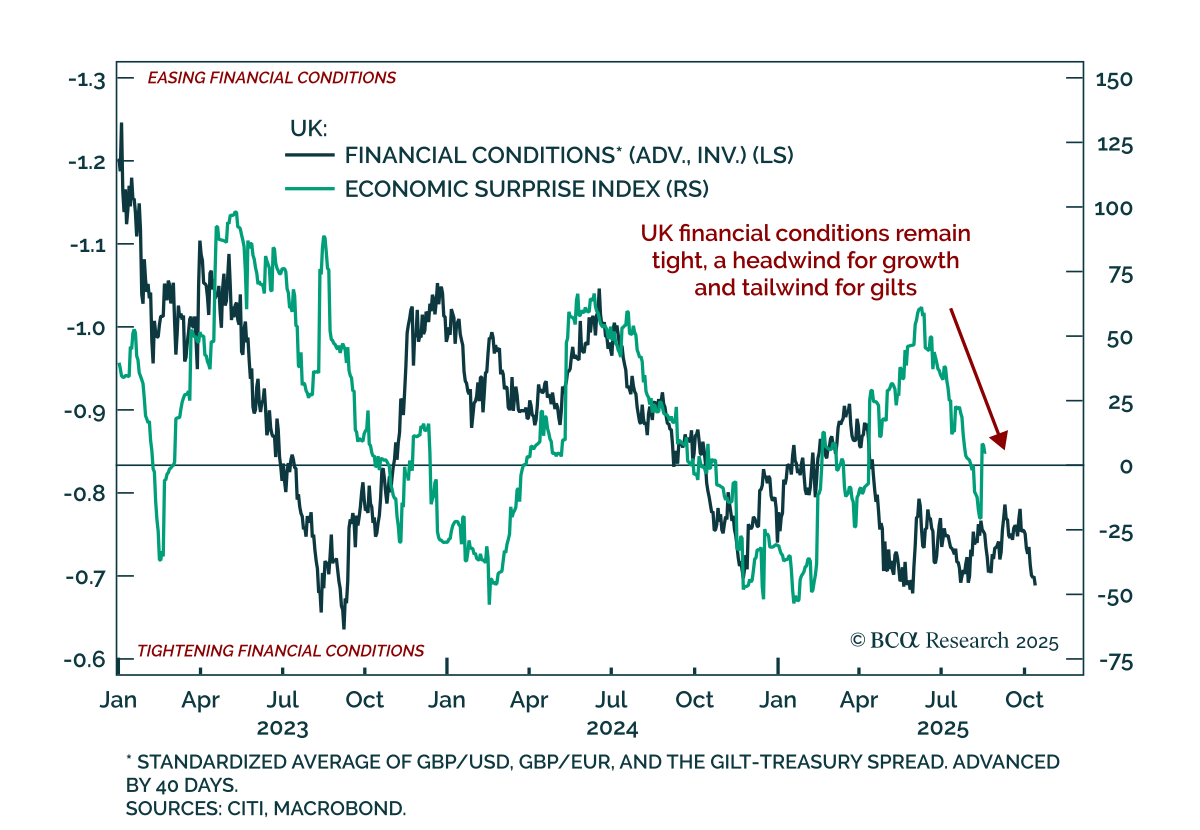

UK

Despite concerns about fiscal sustainability, a rise in term premia, and attacks on central bank independence, monetary policy remains the primary driver of bond markets. In our Q3 Review & Outlook, we update our views and identify opportunities in government bonds, short-term interest rate futures, global yield curves, inflation-linked bonds, and credit.

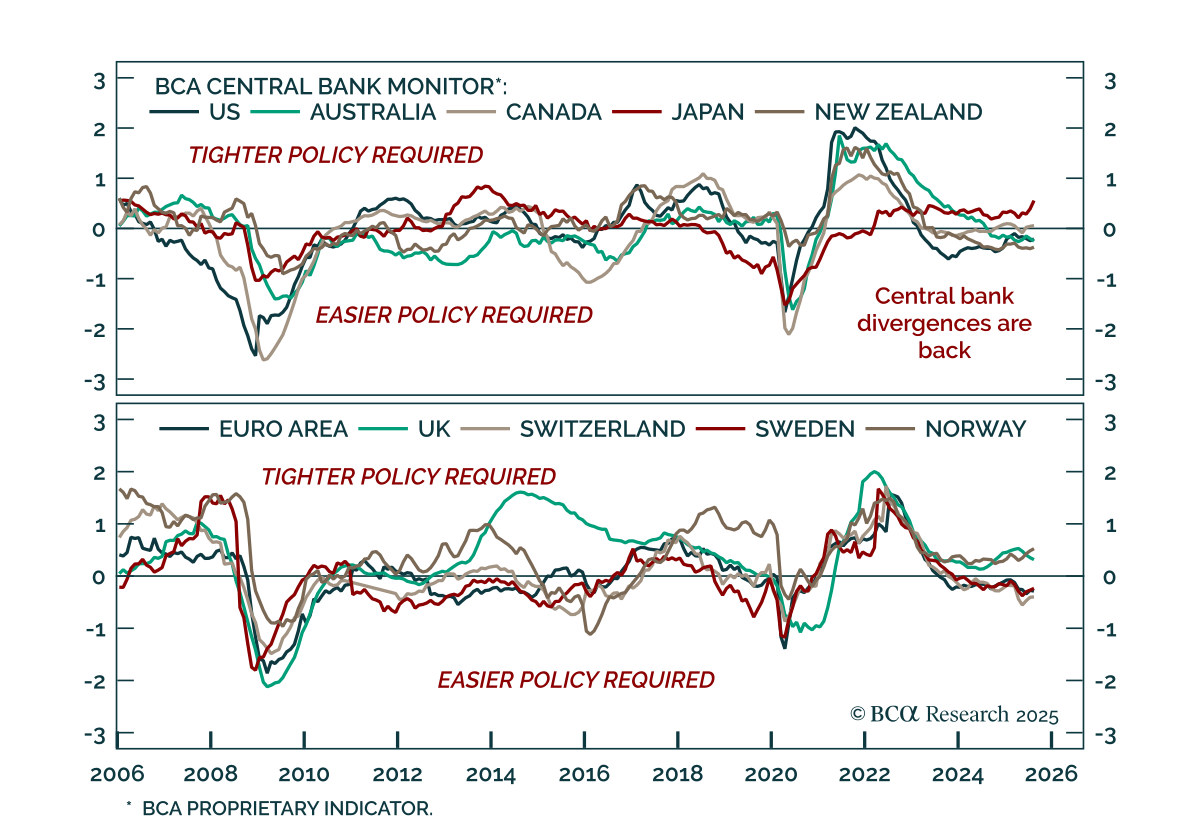

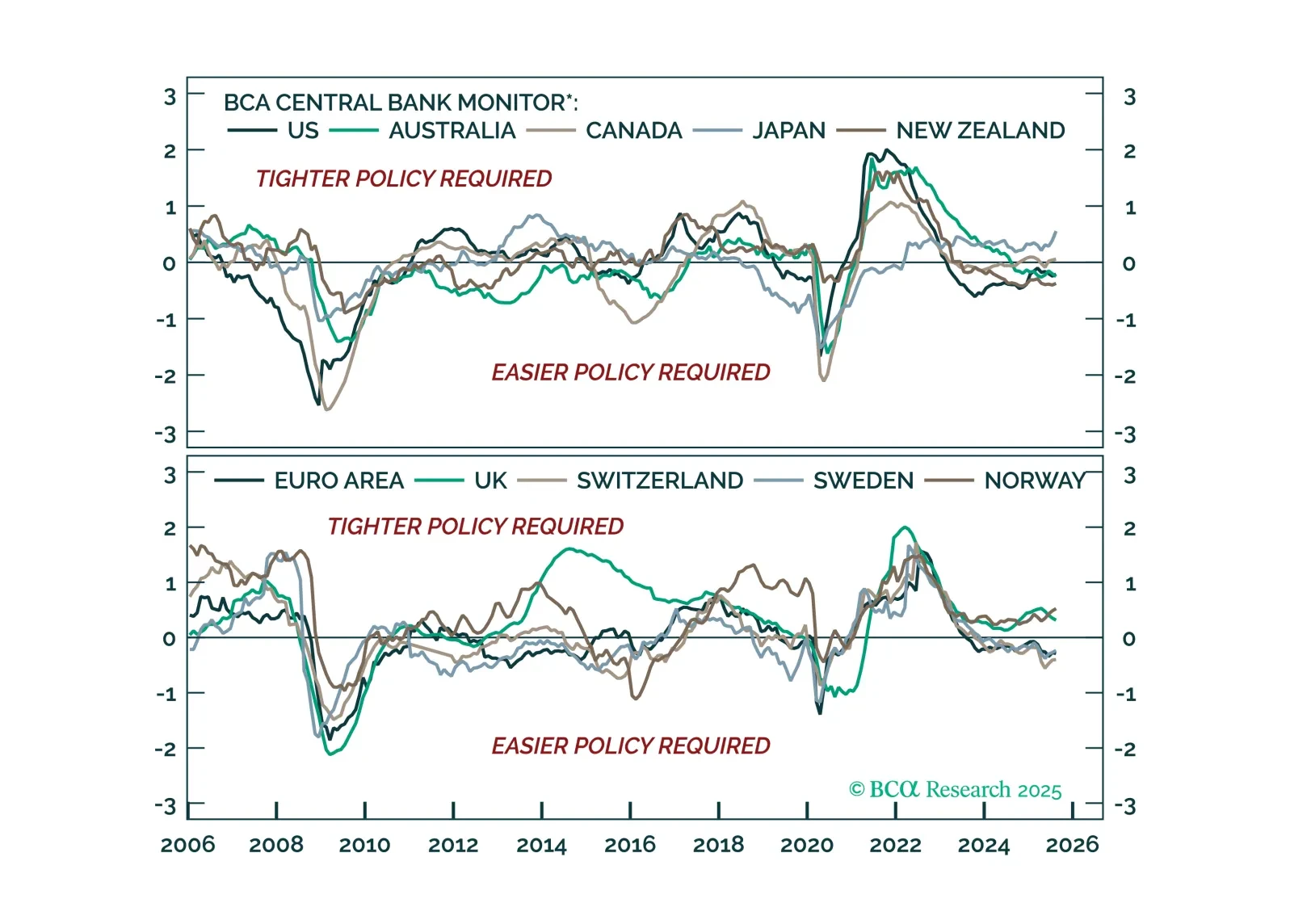

Monetary policy divergences are re-emerging. We rely on BCA’s Central Bank Monitor to assess the current policy stance of major central banks, and highlight the tactical opportunities across bond markets and currencies.

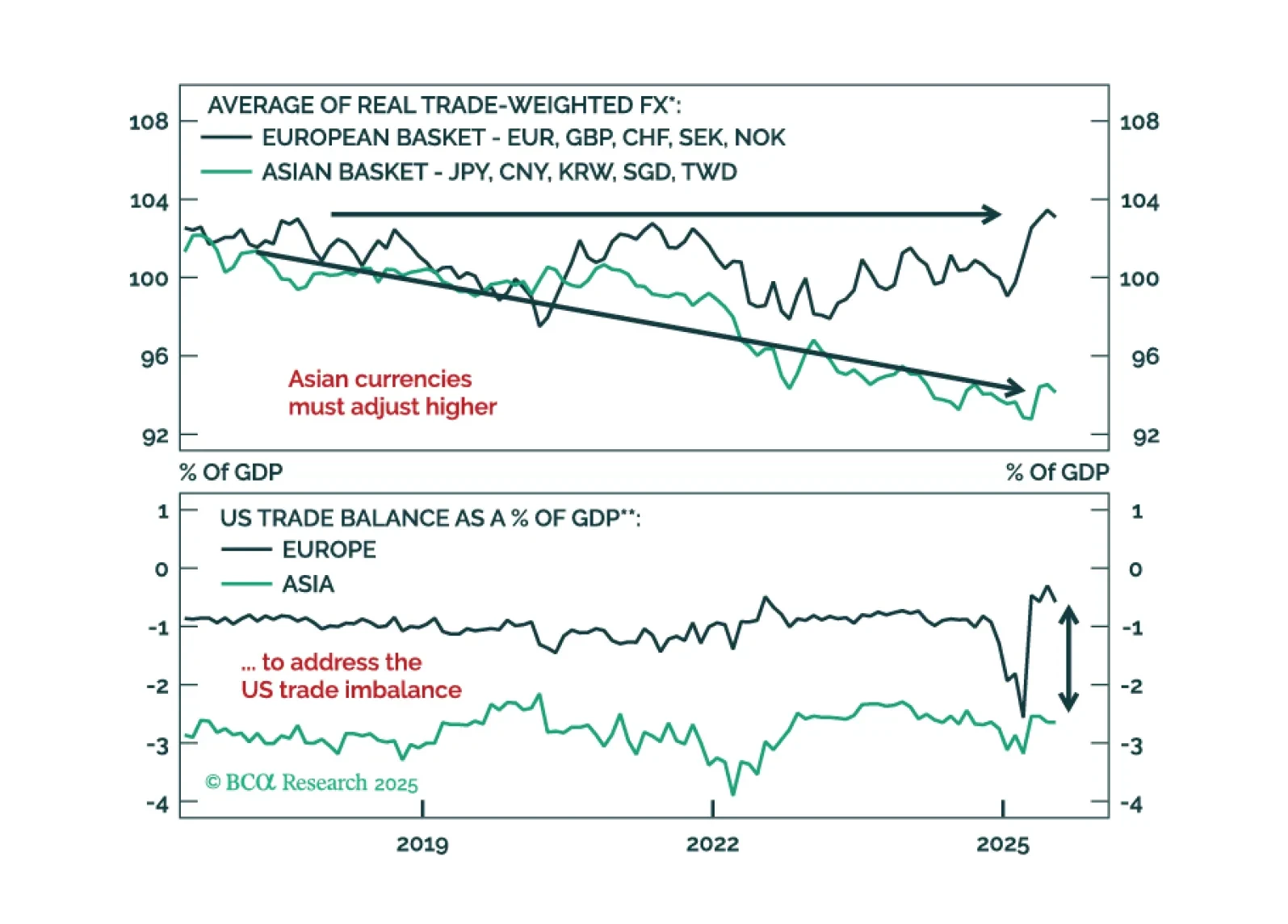

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.

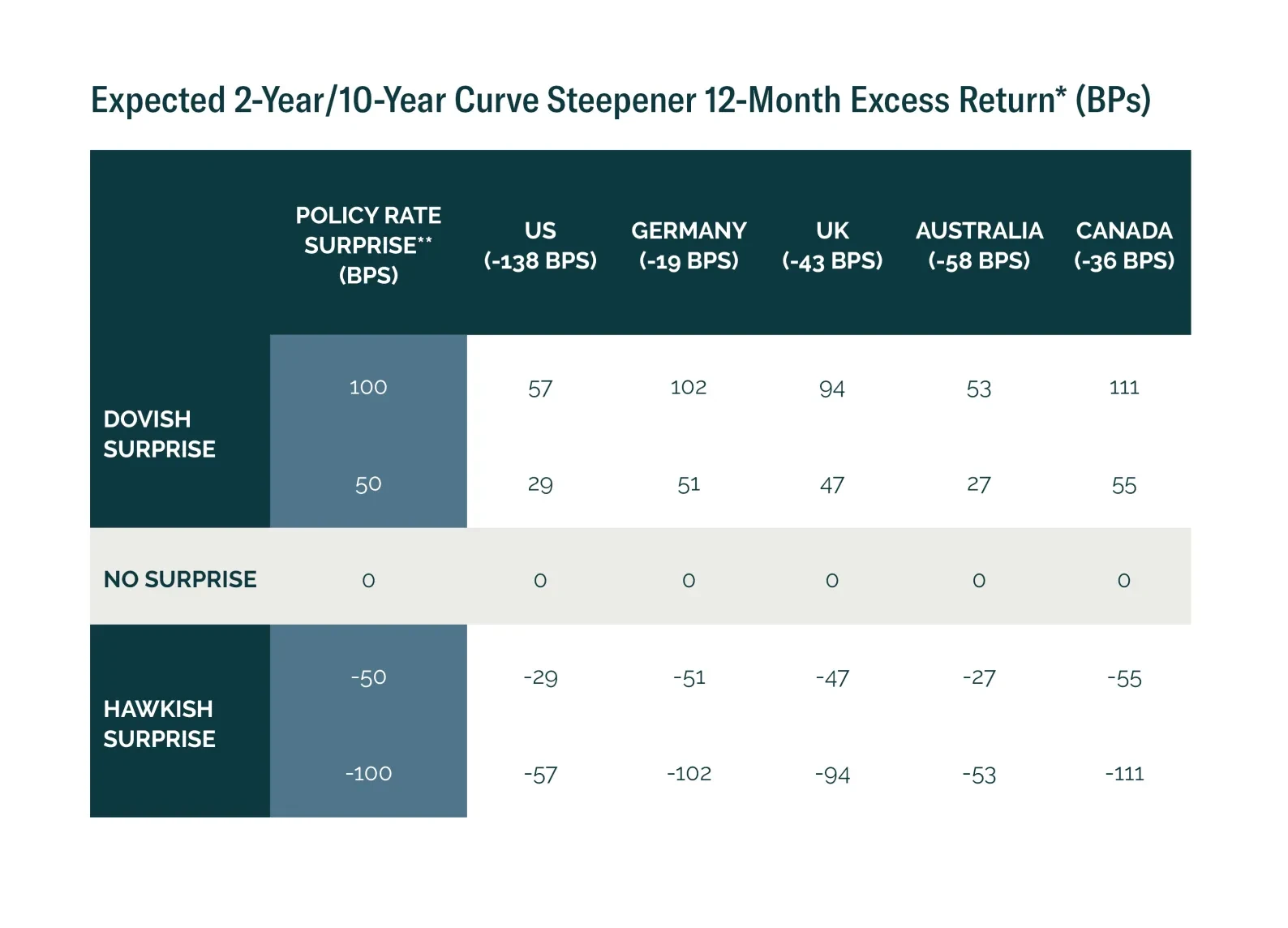

Monetary policy surprises shape curve trade returns. We show where steepeners and flatteners offer the best risk-reward in today’s market.

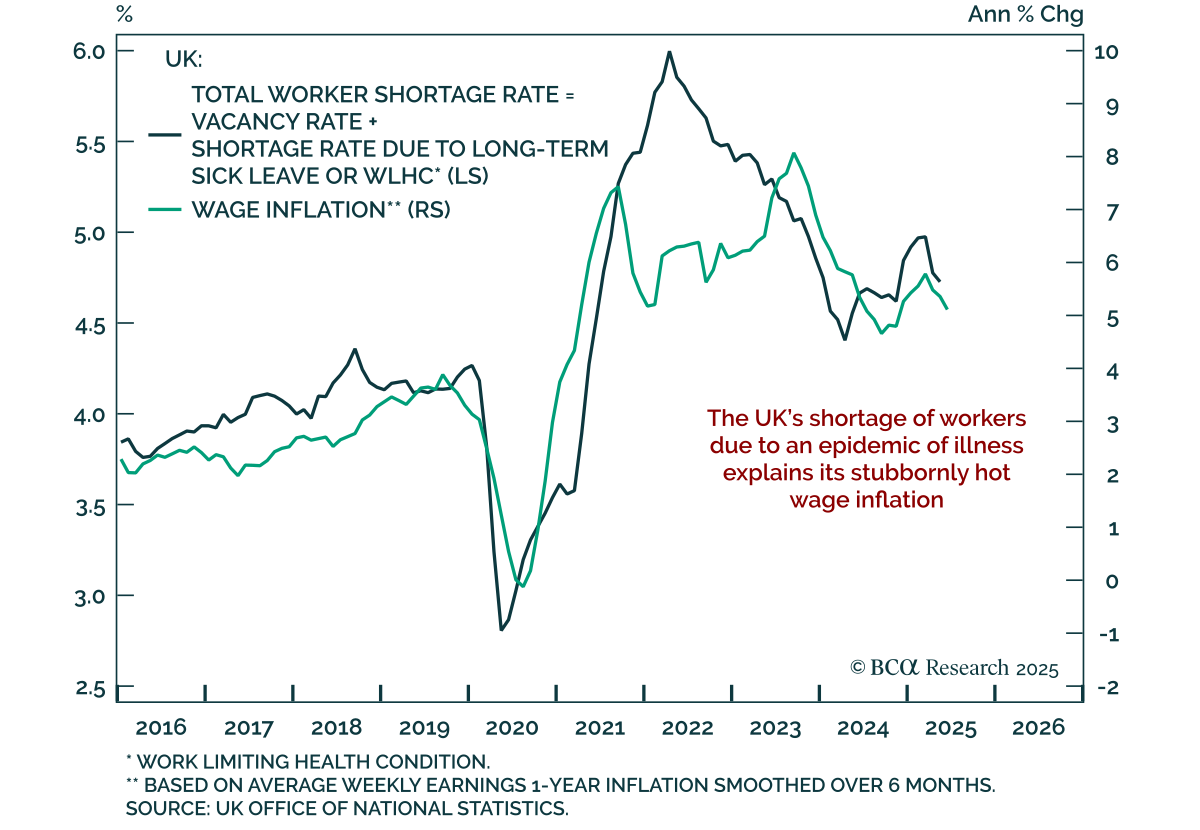

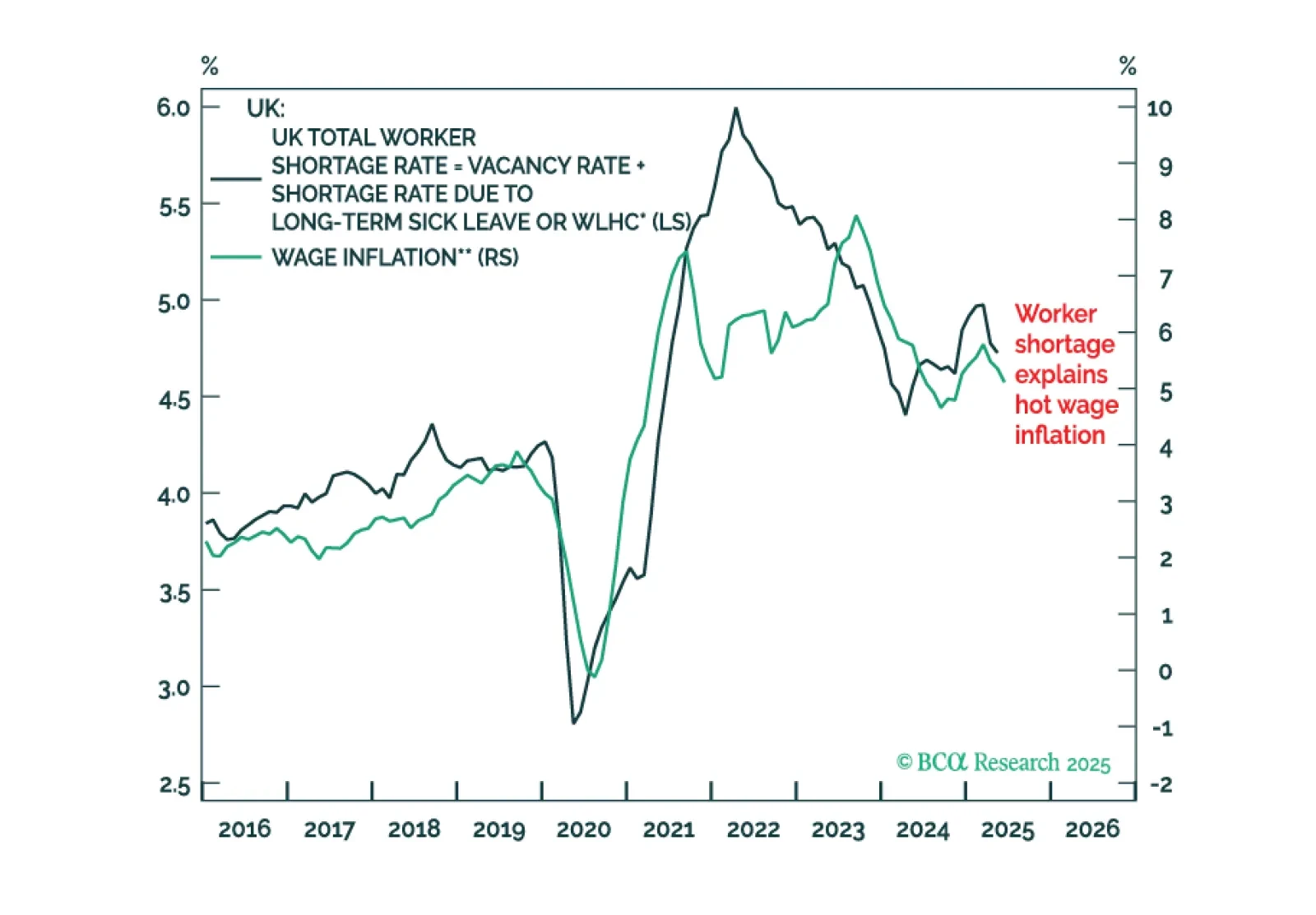

A surge in UK employees on long-term sick leave or with a work limiting health condition explains stubbornly high UK wage inflation. This leaves the Bank of England and the UK government with some tough choices to make in the months ahead. Plus, a new tactical trade is short CSI 300.