UK

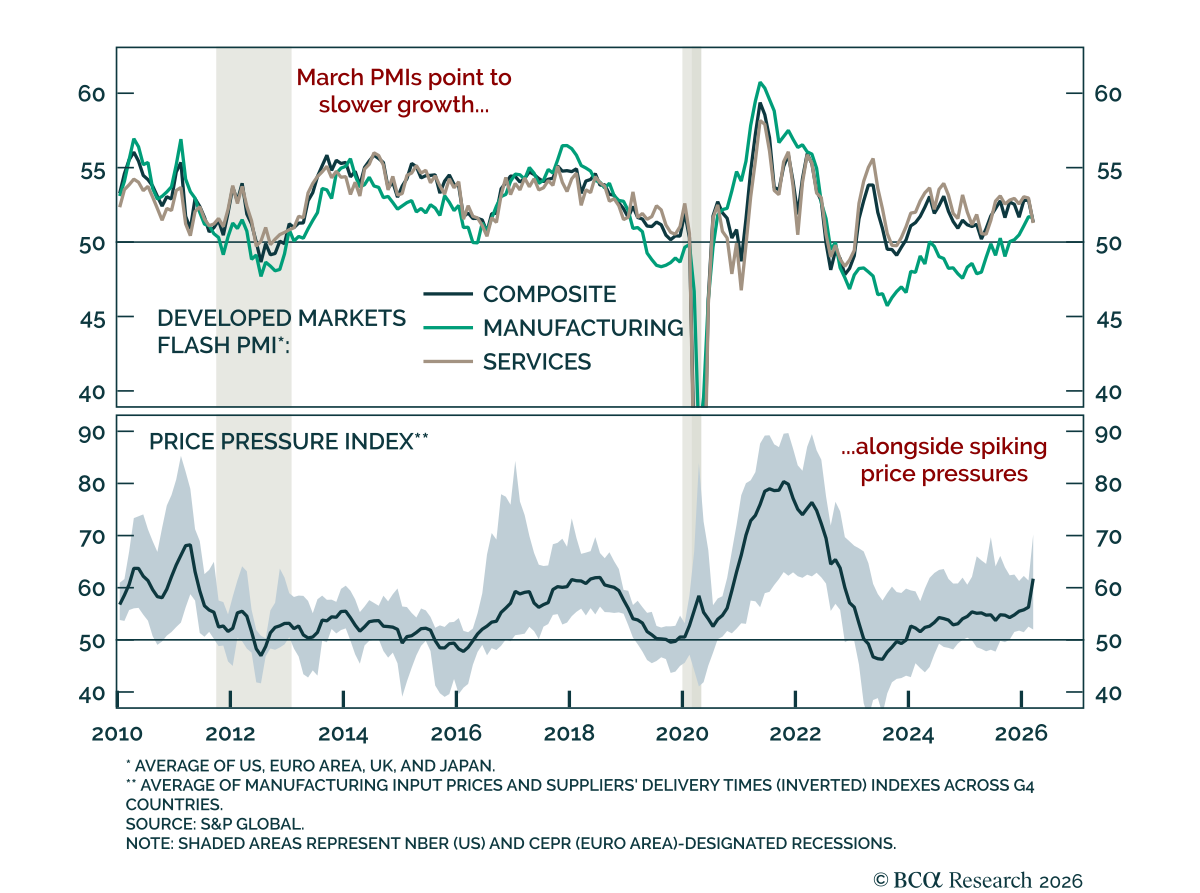

March flash PMIs point to rising inflation pressures, with the US more resilient than its DM peers. Input costs rose and delivery times lengthened across developed markets. Manufacturing was resilient, but services PMIs declined. The US PMIs pointed to…

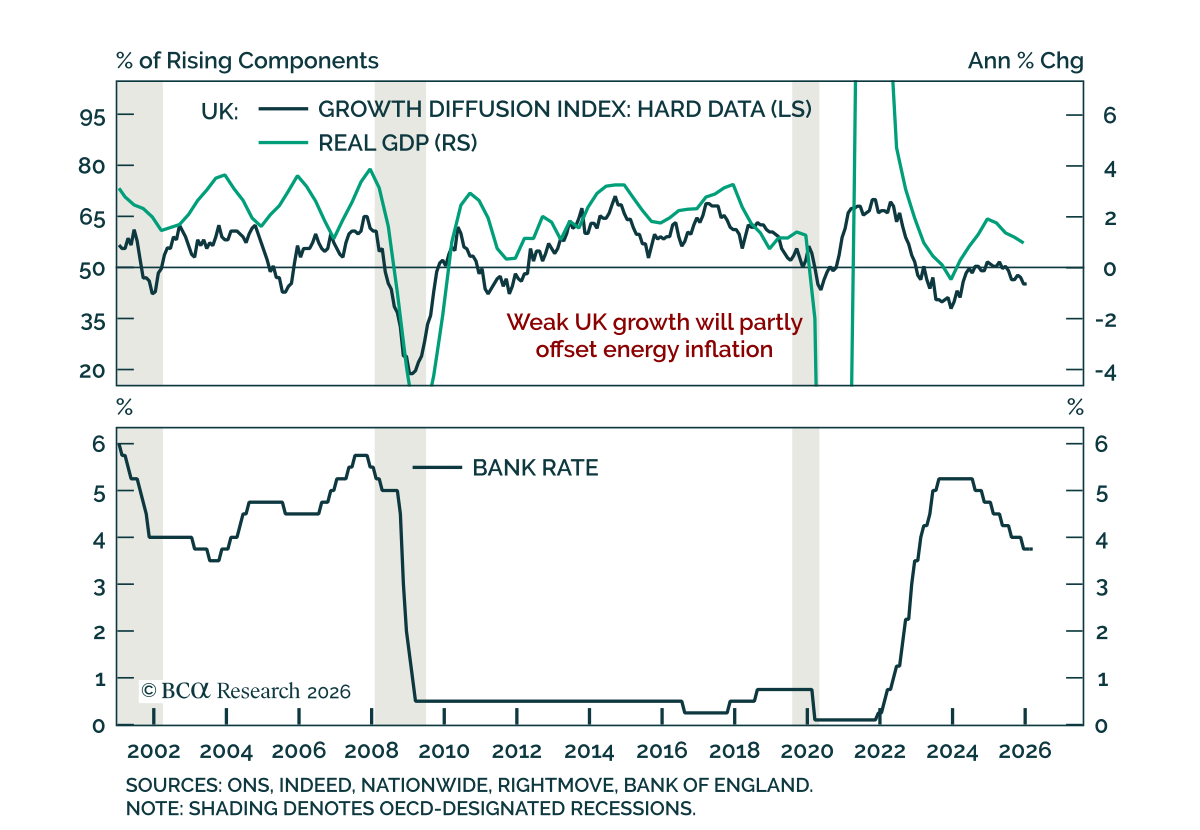

The Bank of England held rates, adopting a wait-and-see stance amid cooling growth and fragile inflation expectations. The BoE voted unanimously to keep rates at 3.75%. Prior to the geopolitical escalation, a cut had been expected as both growth and inflation…

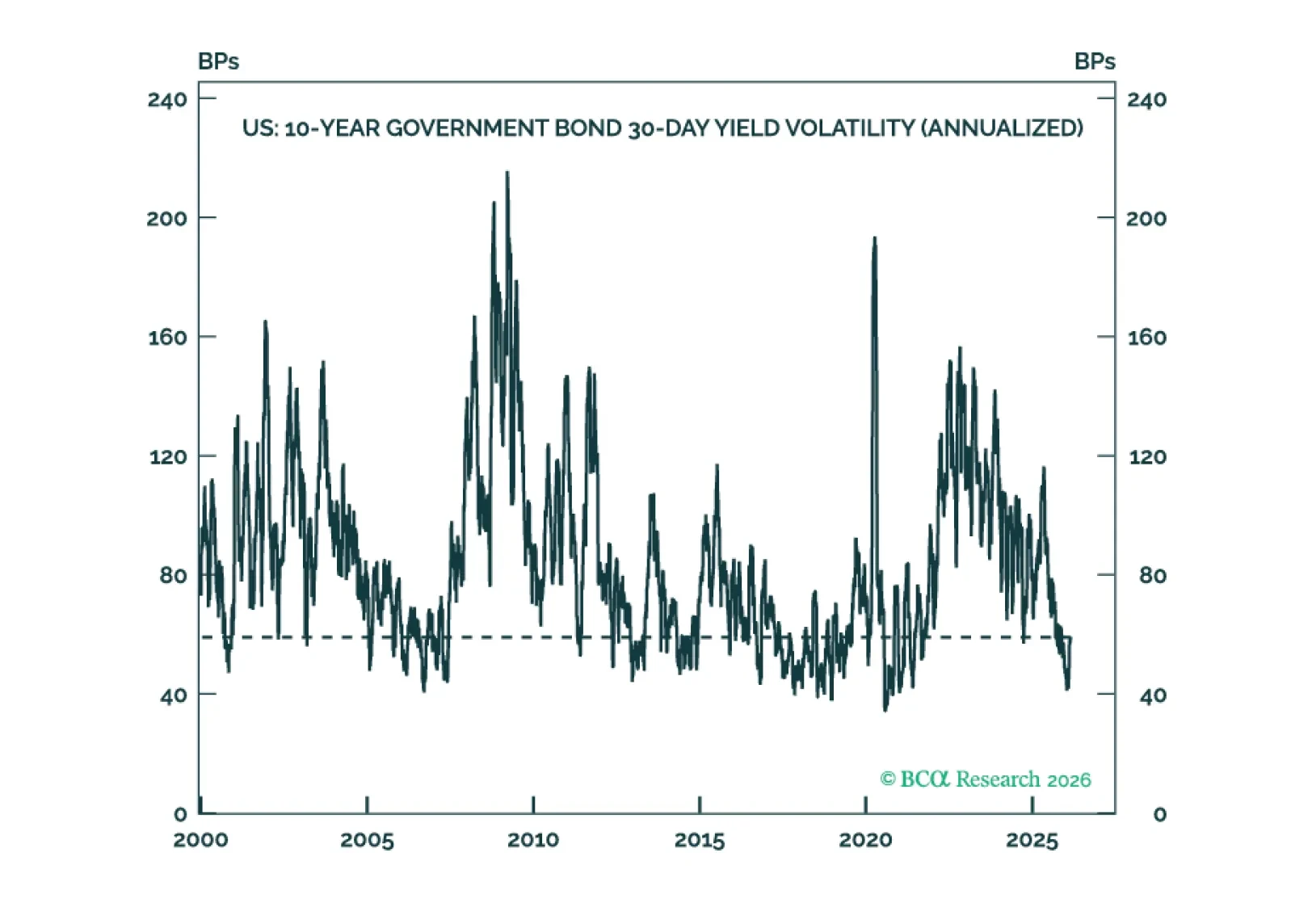

Interest rate volatility is very low across developed market fixed income. Investors should maximize the carry in their portfolios to outperform in a low rate vol environment.

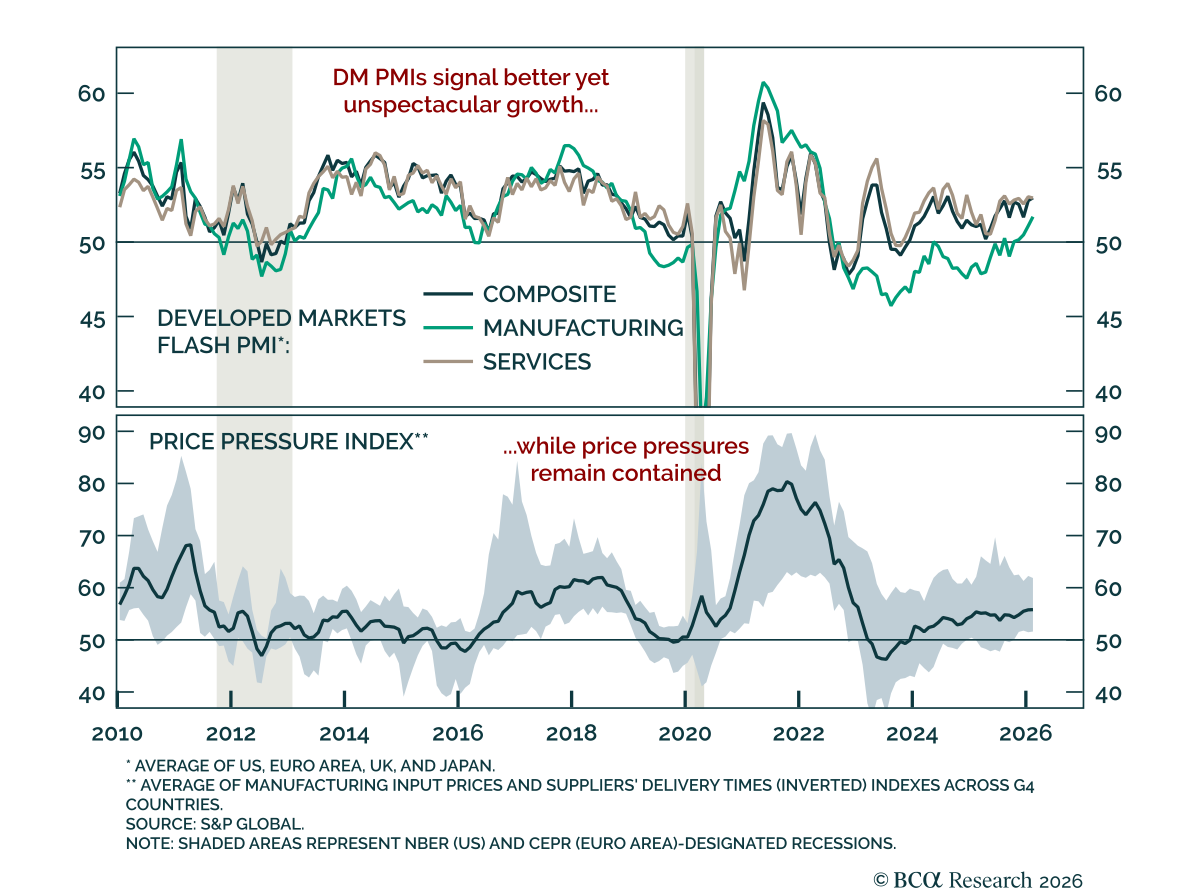

February flash PMIs edged higher, pointing to gradual improvement in global growth. After moving mostly sideways through 2025, developed markets PMIs are picking up. Manufacturing is showing decent momentum, rebounding after being weighed down by trade…

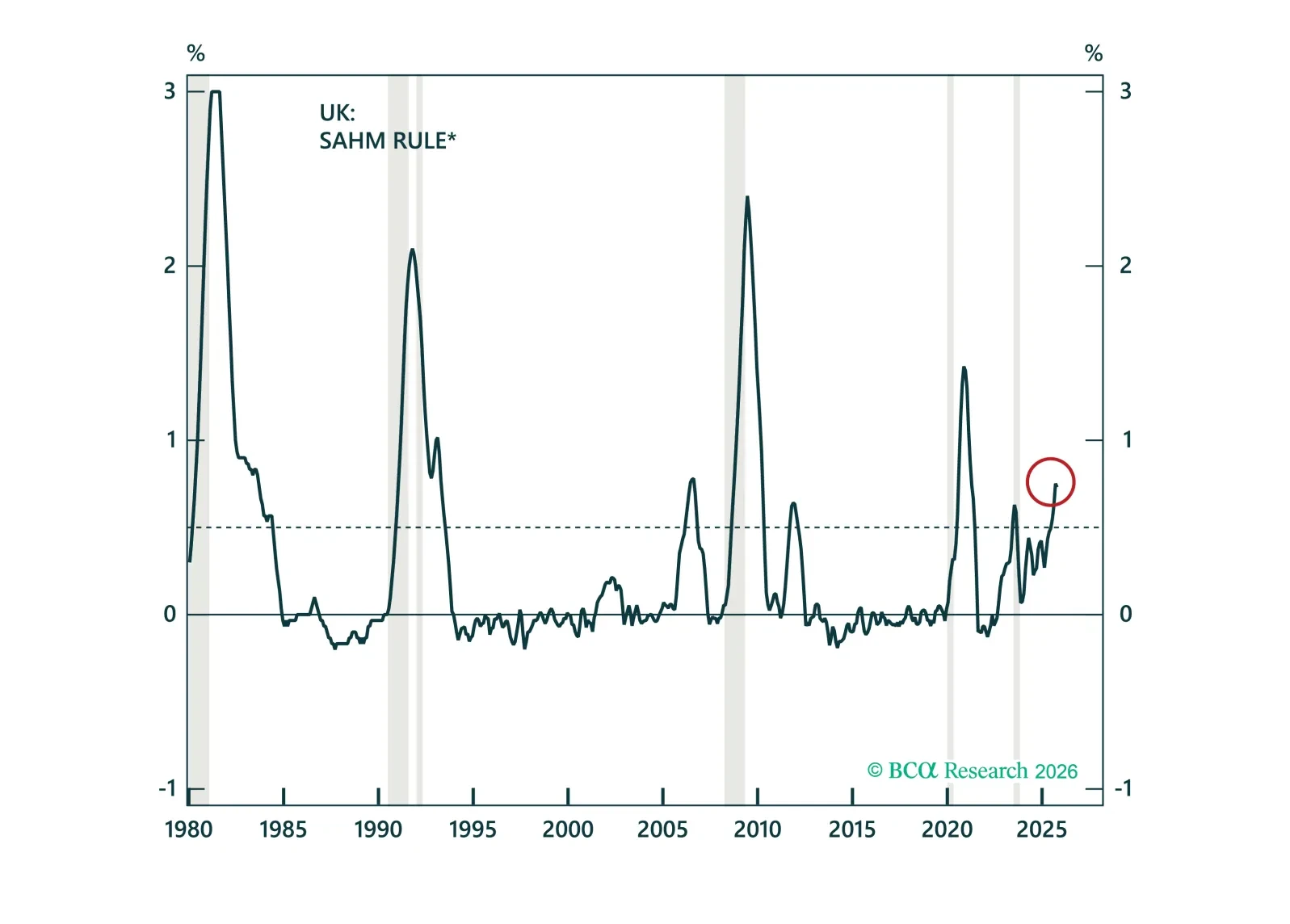

Weak UK employment and easing inflation reinforce the case for further BoE cuts. Payrolls fell by 11k in January, while the unemployment rate rose to 5.2% when steadiness was expected. Average weekly earnings slowed to 4.2% y/y from 4.6%, and the BoE’s…

UK December hard data surprised to the downside, reverting to tepid growth and reinforcing the case for further BoE easing. Industrial production fell 0.9% m/m, slowing to 0.5% y/y from 2.3%. Services were flat on a three-month sequential basis, while…

The Bank of England held rates but struck a dovish tone. The Bank of England held rates at 3.75%. The MPC voted a narrow 5-4 to hold, with Governor Bailey casting the deciding vote. Bailey nonetheless sent dovish signals ahead of the March meeting, noting the…

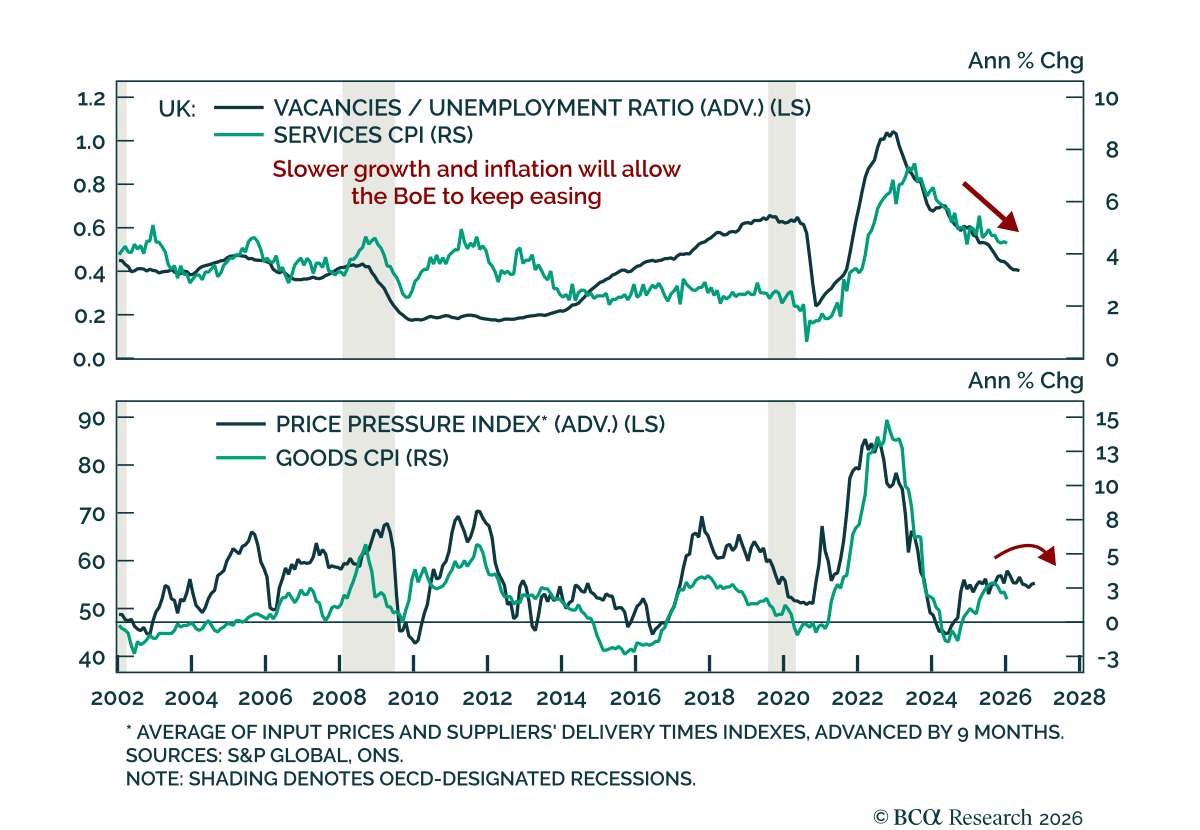

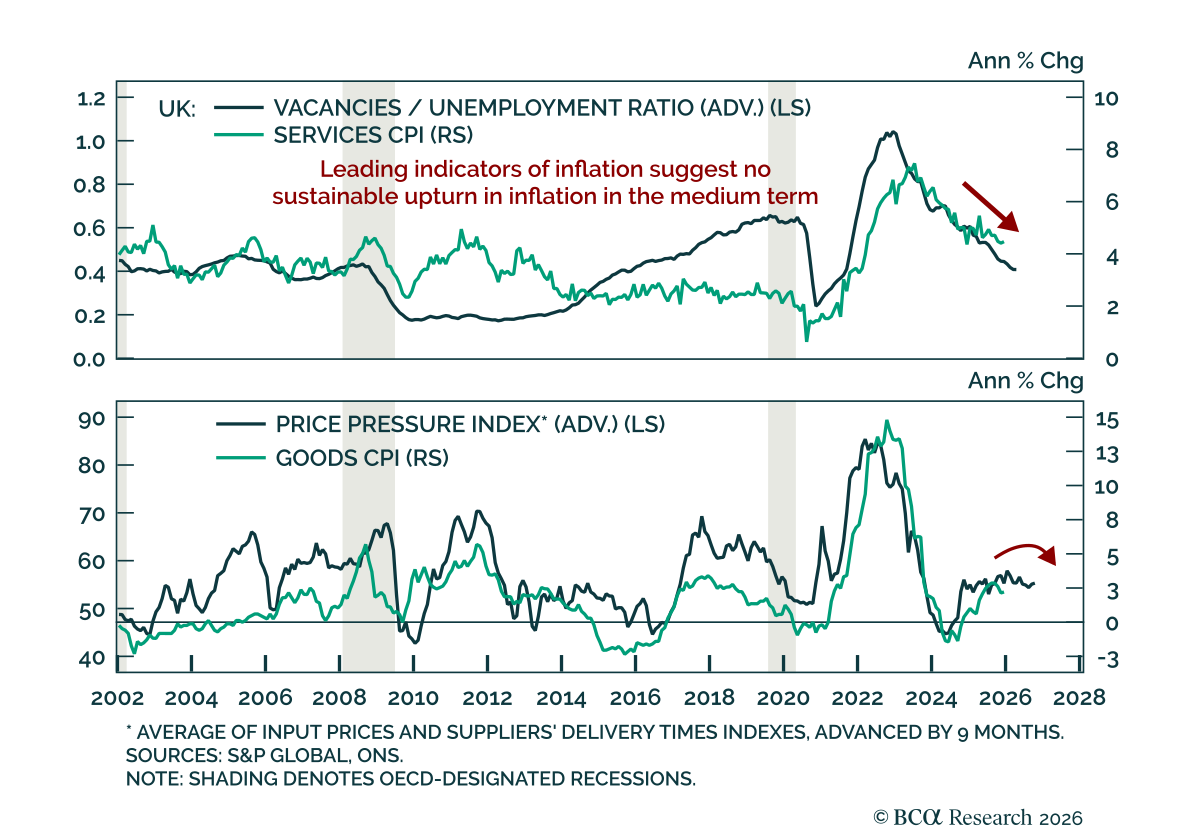

Recession risks in the UK are clearly rising. In this Special Report, we unpack why labor market deterioration, falling wage growth, and normalizing inflation support deeper BoE cuts ahead. We then discuss how to position across gilts, the pound, and UK equities.

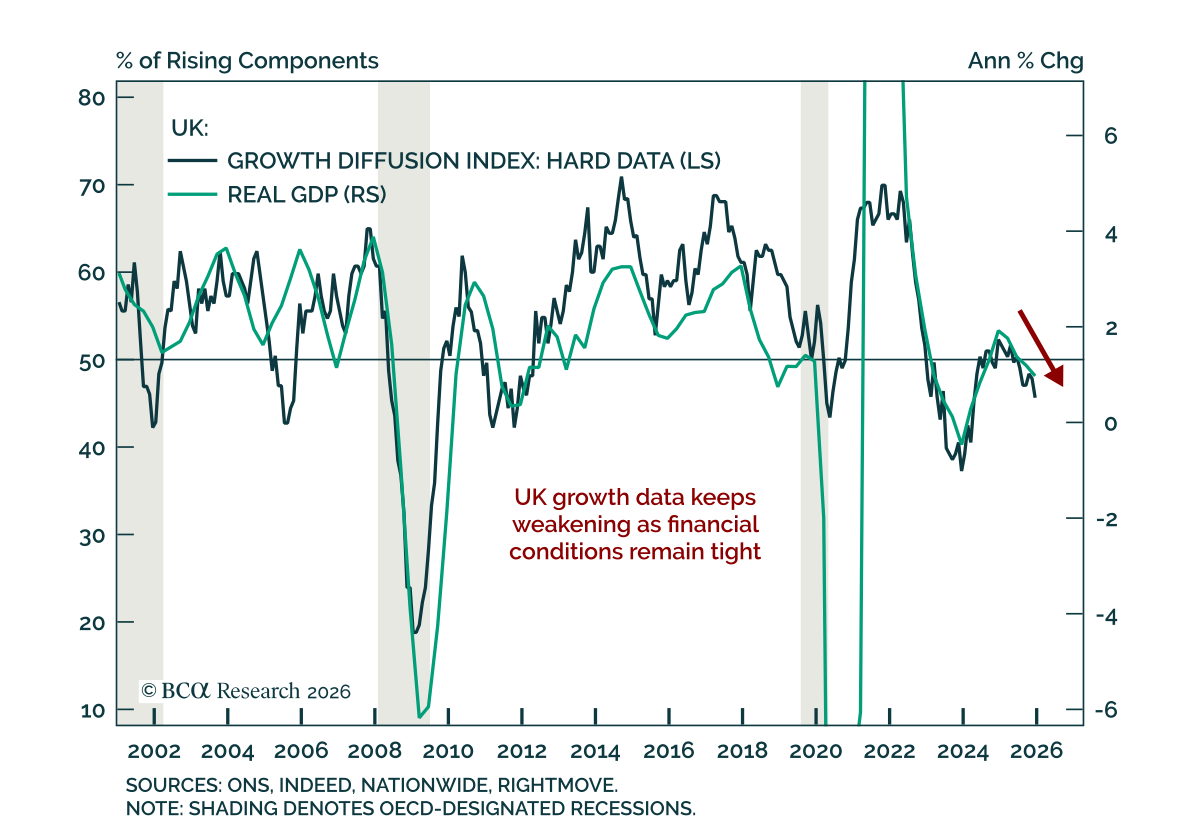

Stay overweight UK gilts and favor GBP 2-year/10-year steepeners as fundamentals remain weak and financial conditions restrictive. Recent strength in UK economic data reflects pent-up demand rather than underlying improvement. Manufacturing rebounded after…

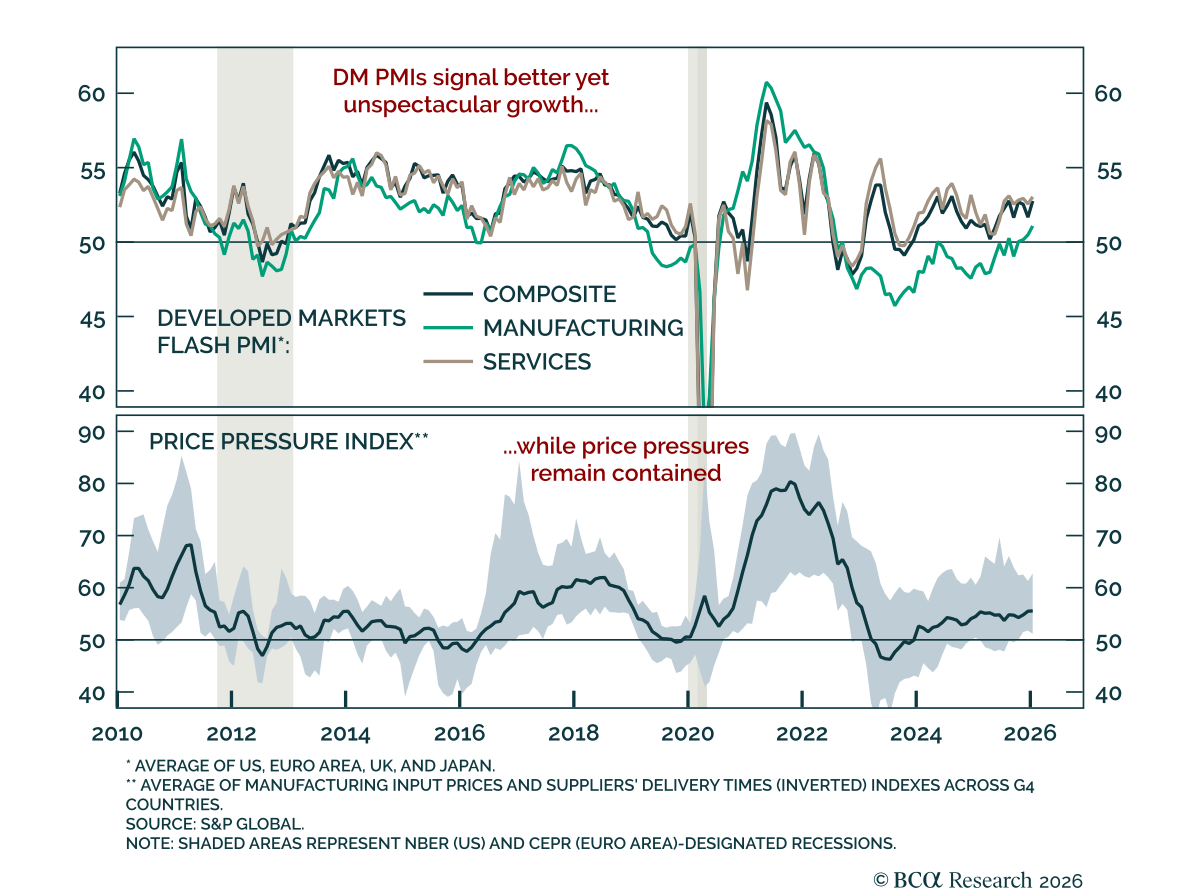

January flash PMIs point to better, though unspectacular, global growth momentum. Developed markets PMIs showed improvement in global growth momentum. PMIs have largely moved sideways through 2025, with manufacturing now recovering after trade uncertainty and…