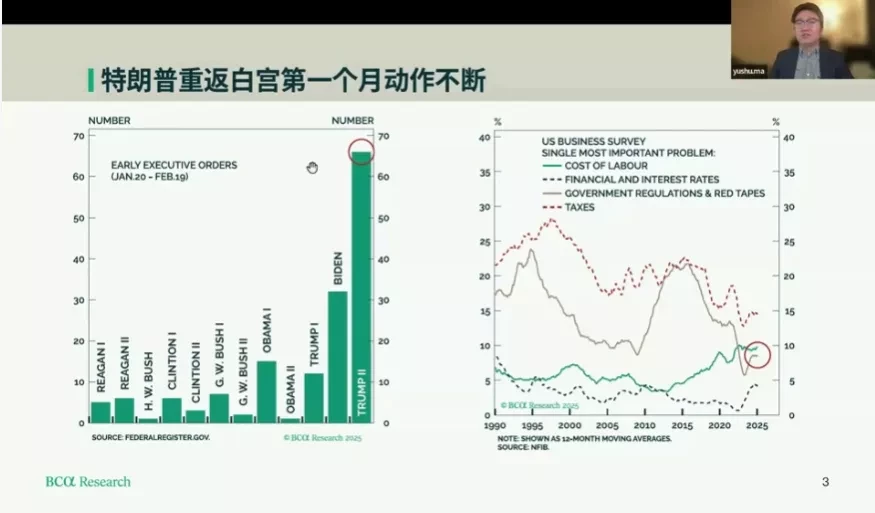

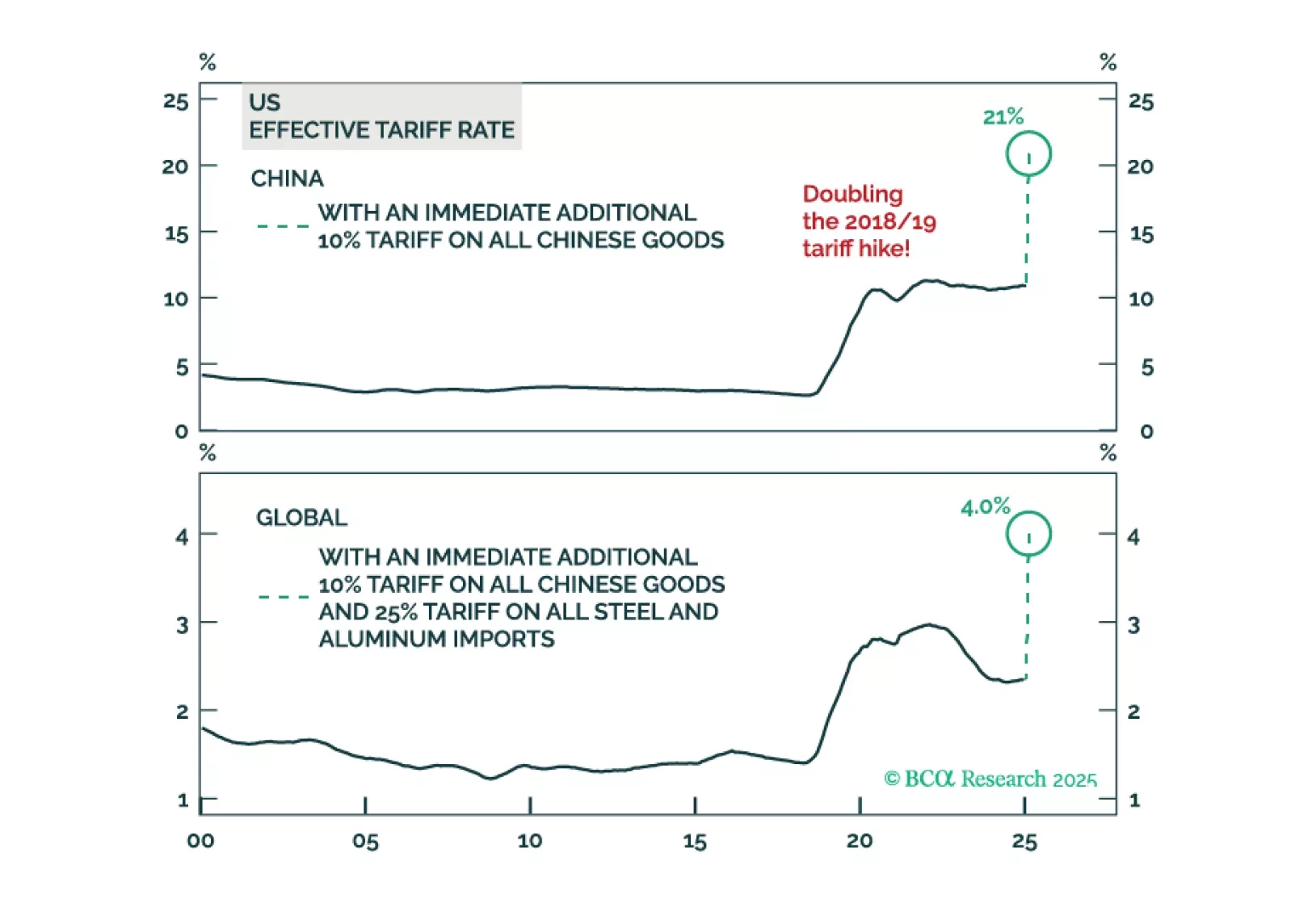

Trump's Policies

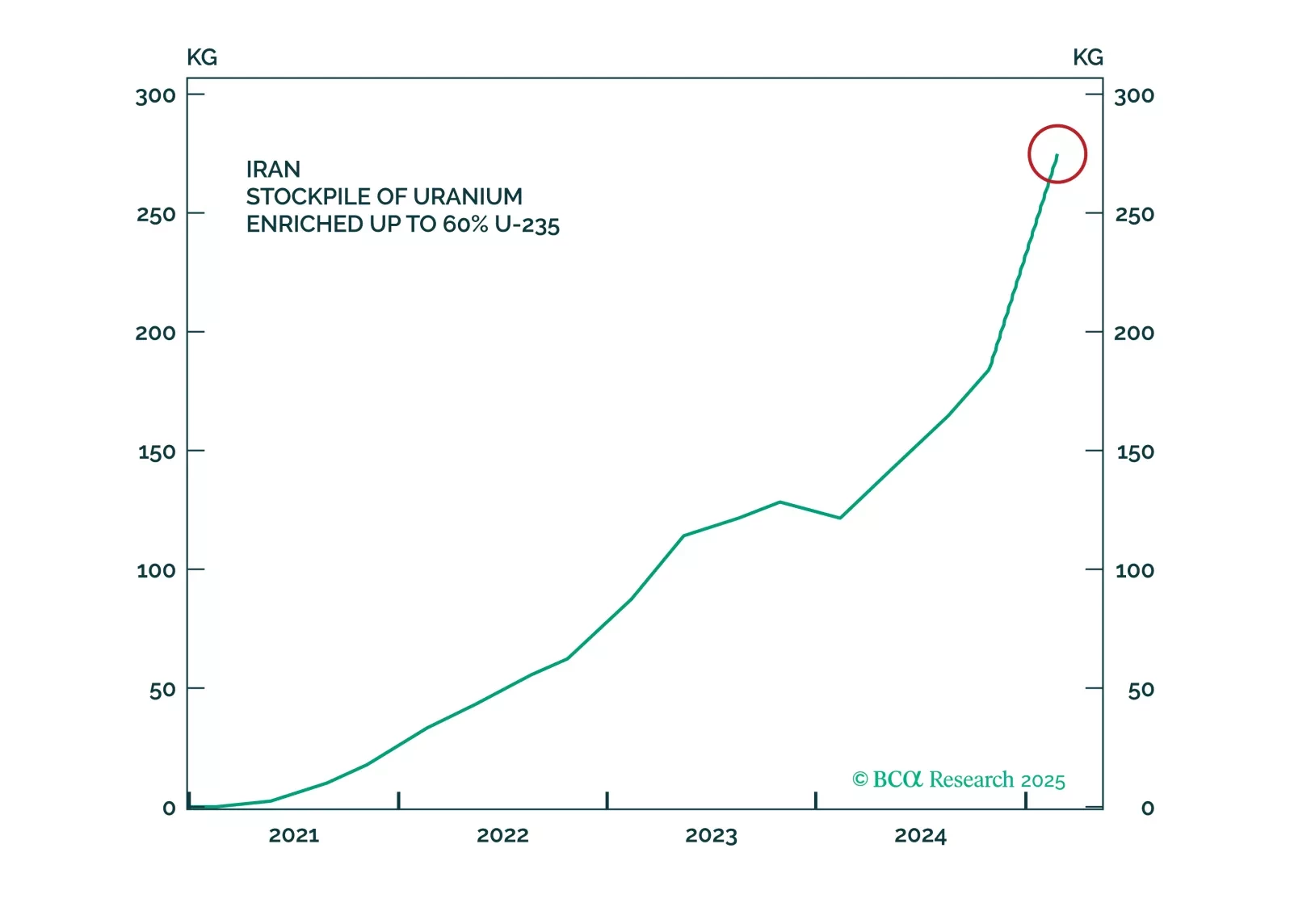

The tariffs on Canada and Mexico will come into effect as scheduled while the tariffs on China will be doubled. In the Middle East, Iranian response to any attack will threaten Middle Eastern oil supply. Meanwhile, Chinese fiscal support will surprise to the upside at the Two Sessions. But Trump's China policy will cause volatility. Now that the stock market is cracking, reinitiate defensive trades, such as long treasuries versus US stocks and long global defensives versus cyclicals.

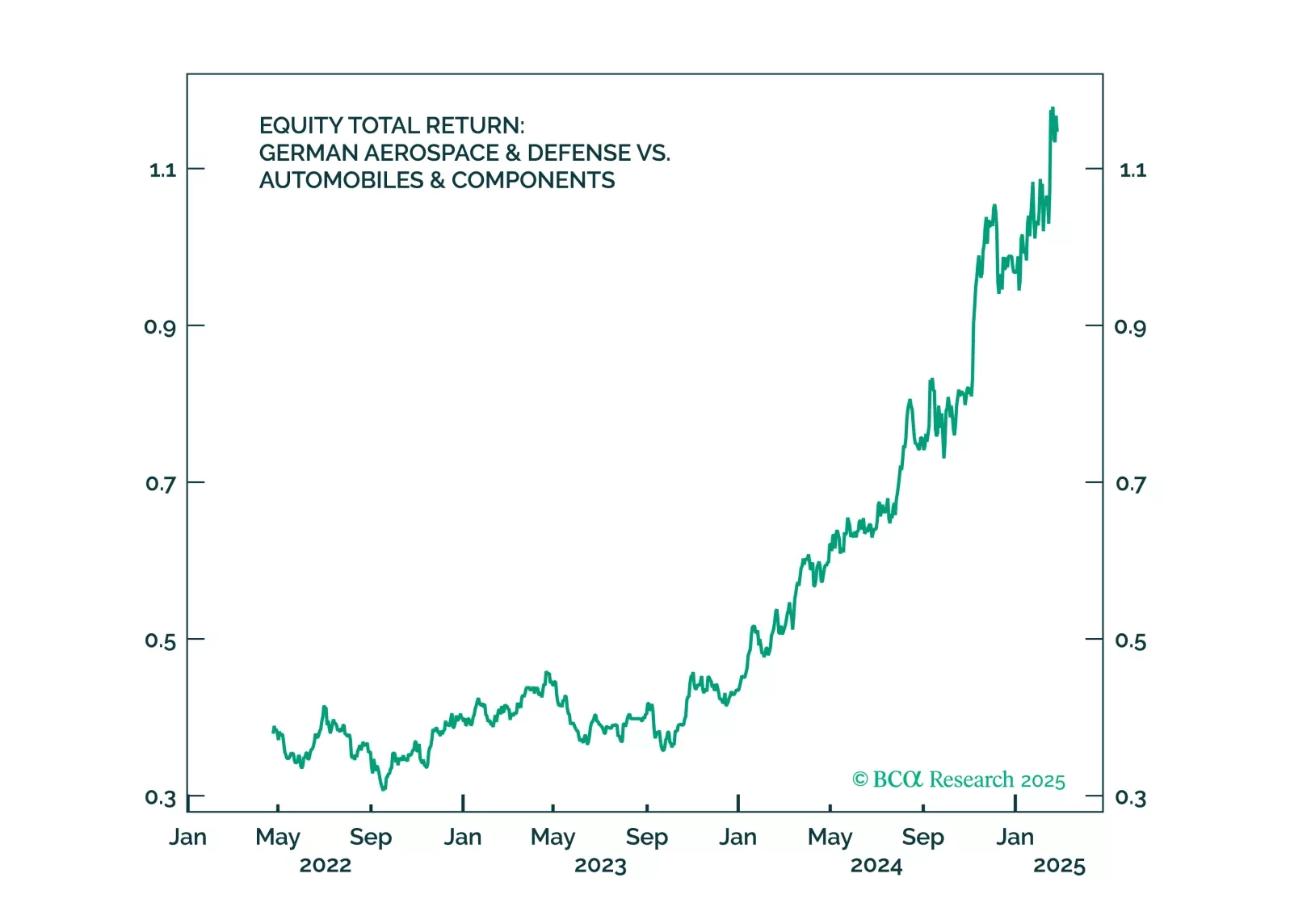

Trump’s ceasefire talks are positive for Germany – and so was the German election result. But Trump’s tariffs will hit Germany soon. Investors should use near-term volatility to increase exposure to Germany.

US growth has slowed in recent weeks. This can be seen in the weaker data on retail sales, consumer confidence, services PMIs, and a swath of housing releases (notably starts, existing home sales, homebuilder confidence, and stock prices). It can also be seen in the decline in GDP tracking estimates. The Atlanta Fed's GDPNow model projects growth of 2.3% in Q1, down from a peak of 3.9% on February 3. The Citi US Economic Surprise Index has also dipped into negative territory.

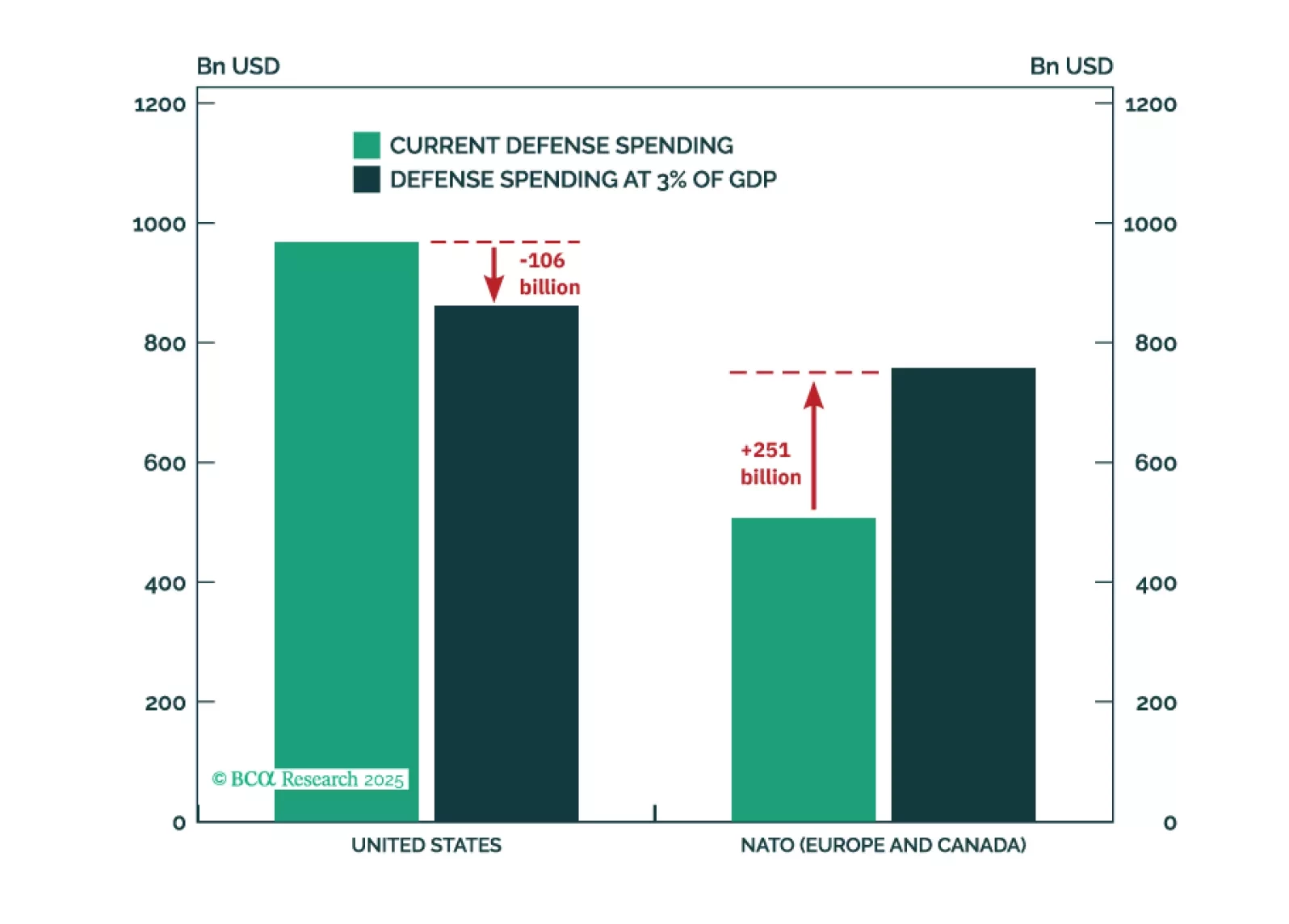

The Trump administration posits that the world owes the US for the provision of its security. In this report, we perform a quantitative analysis to come up with a naïve estimate of the cost of that peace. More importantly (and more seriously), our qualitative assessment argues that save for a number of frontline countries that rely on the US defense umbrella, the vast majority of the world faces manageable security threats due to the complex multipolar global environment and a growing number of alternatives to the US security blanket.

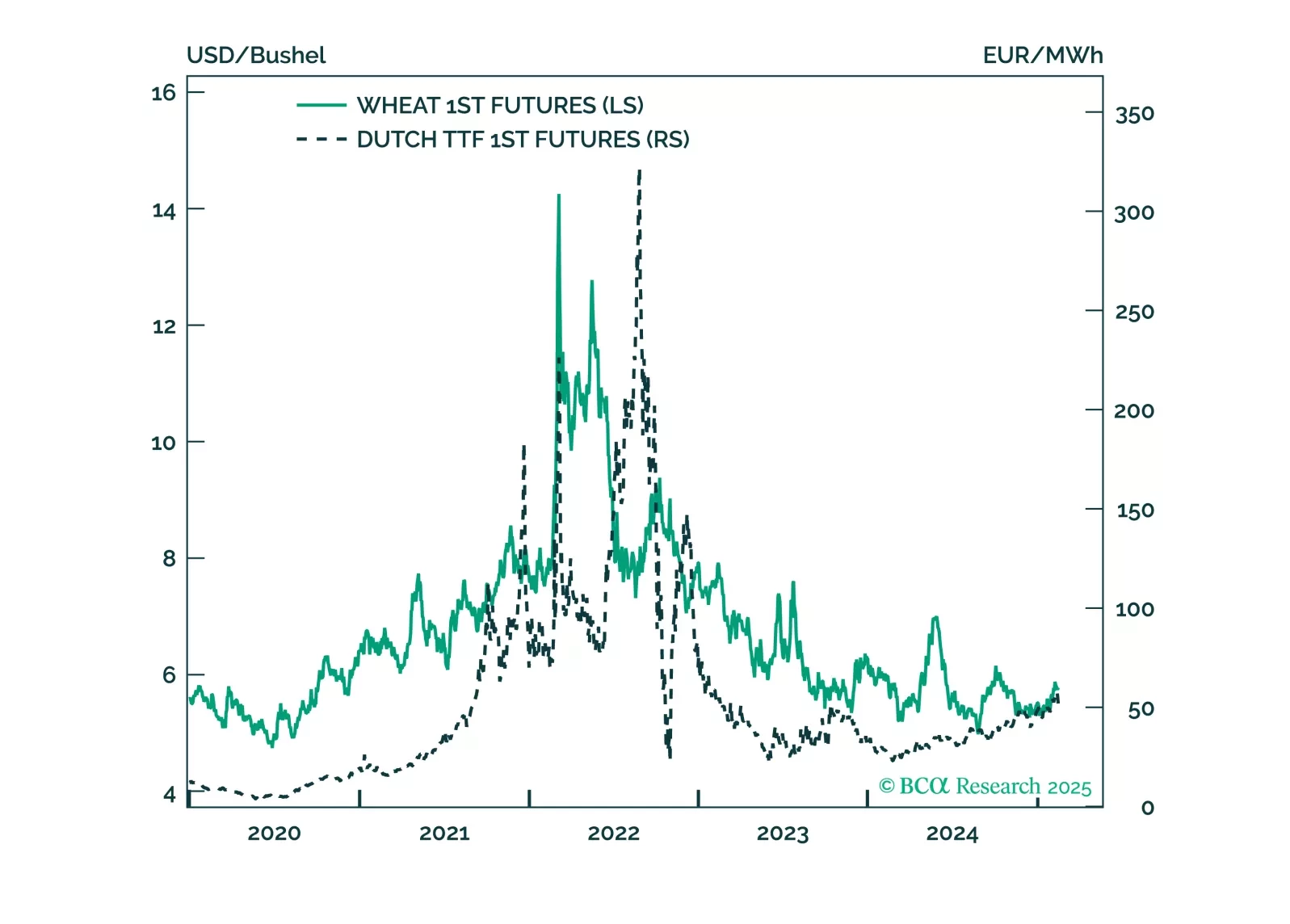

President Trump is negotiating a ceasefire in Ukraine. This will be a marginal headwind to some commodities which benefitted from the conflict like natural gas and wheat, and will be a marginal tailwind for European assets, specifically EM Europe. Use Trump’s tariff shock as an opportunity to buy European assets.

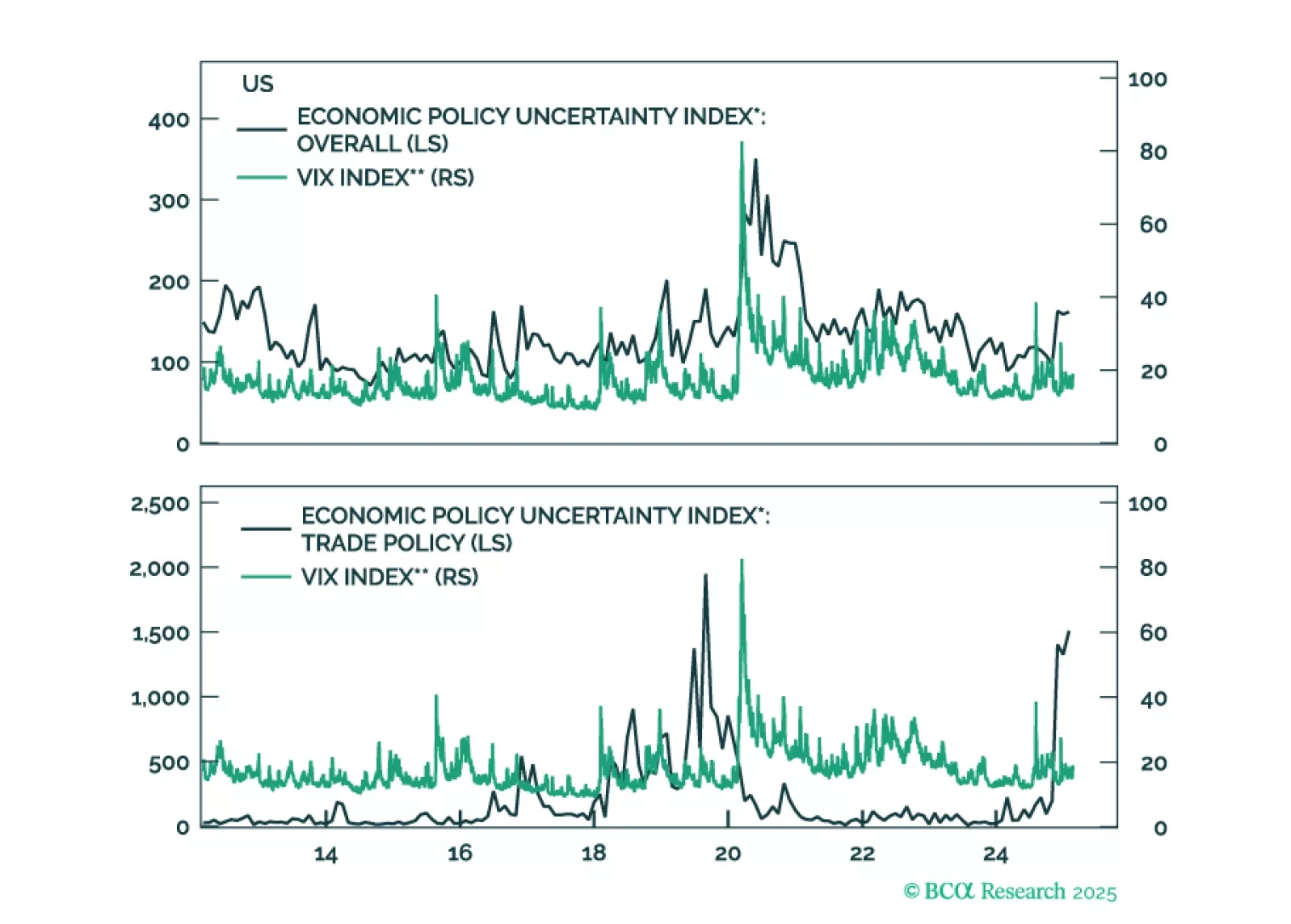

The budget process and debt ceiling will cause stock and bond market volatility. US trade policies will provoke foreign pushback at a time of stretched valuations. Hence US politics and geopolitics will be bullish for US energy, but bearish for the internationally exposed US tech sector.

In his latest Thoughts Of The Day, Peter Berezin discusses the different moving parts of the global economy today and the potential impact of Trump's policies.

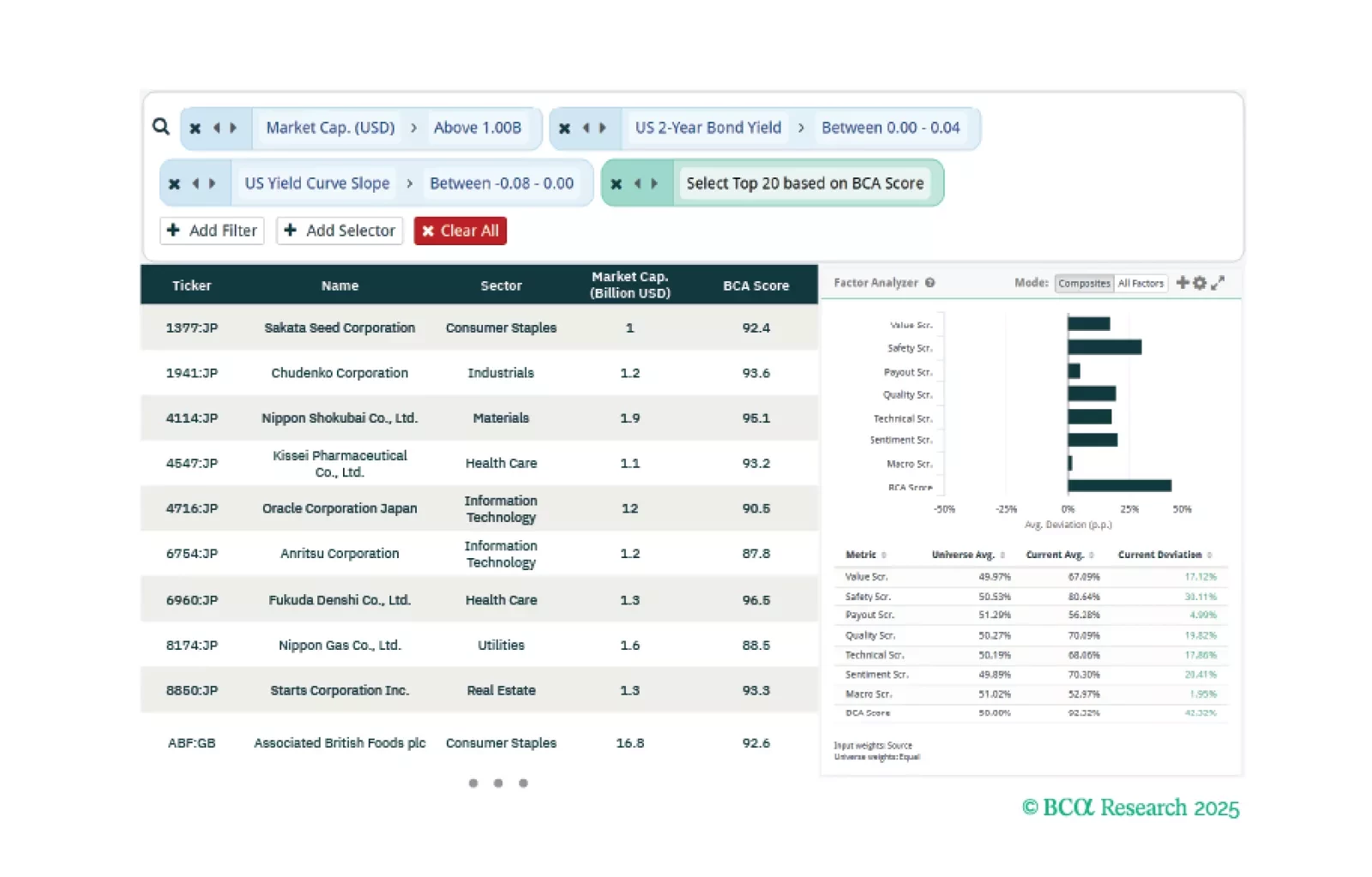

This week, our three screeners focus on providing equity insights based on the impact of tariffs, and trade policy uncertainty in general, helping clients identify stocks exposed to these shocks.