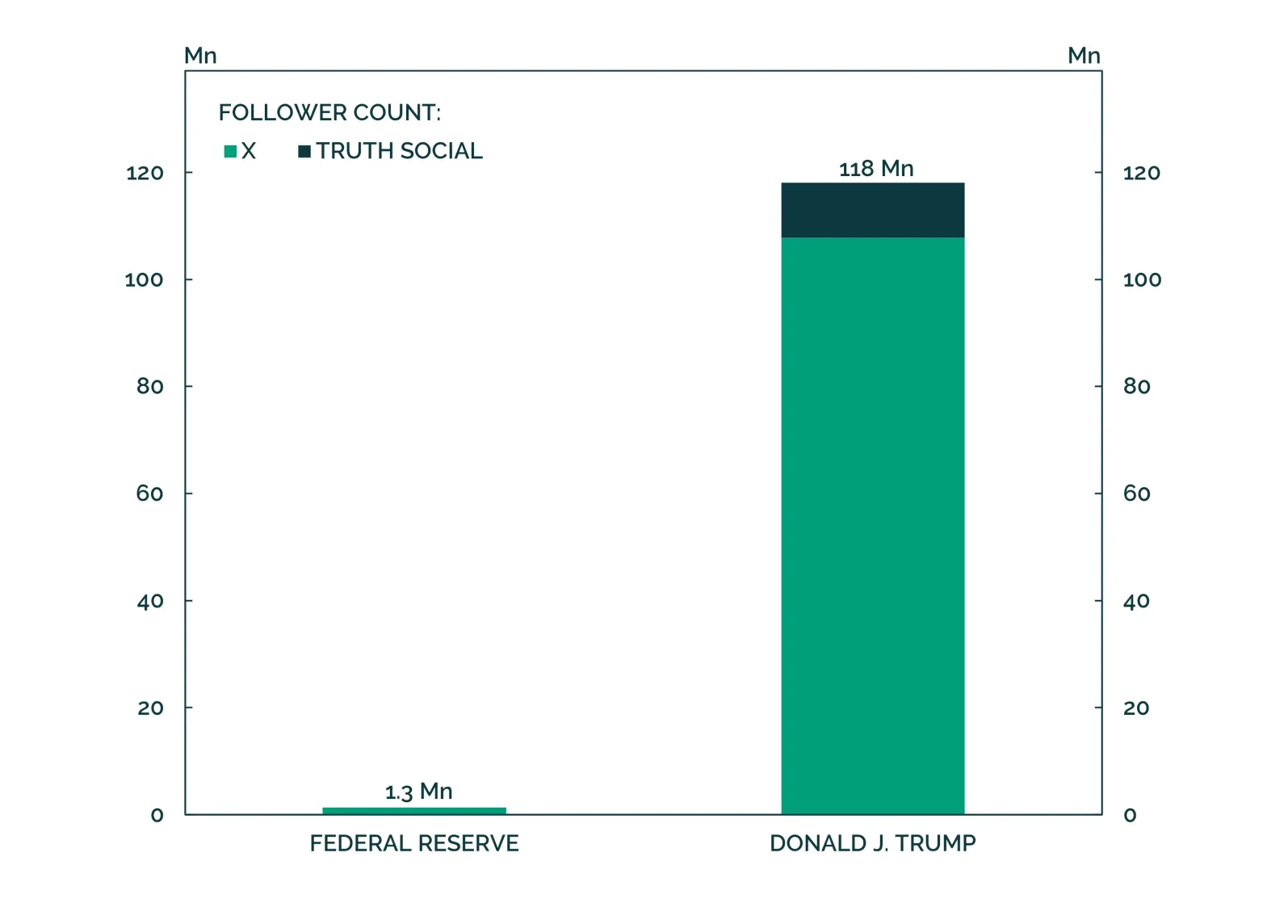

Trump's Policies

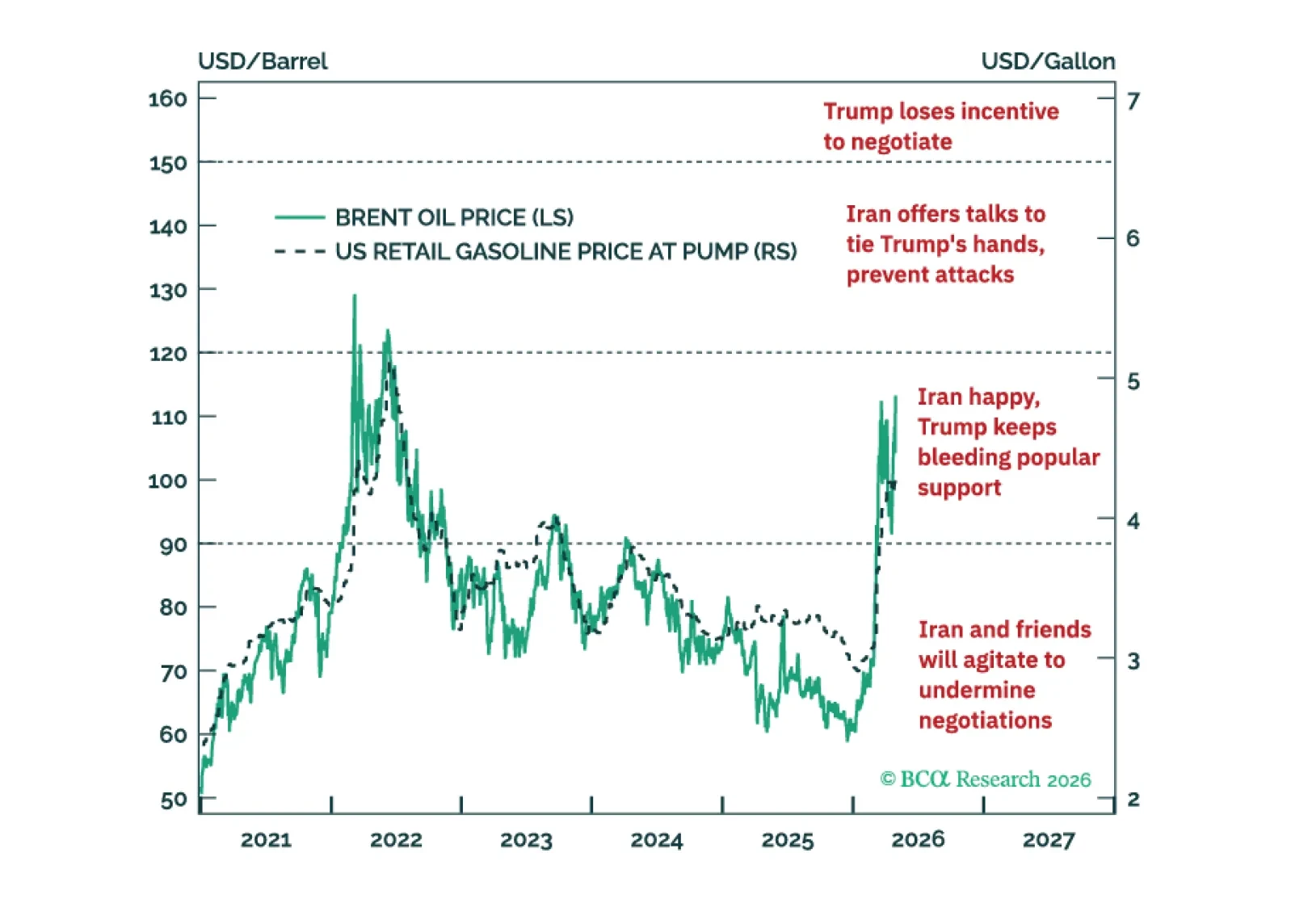

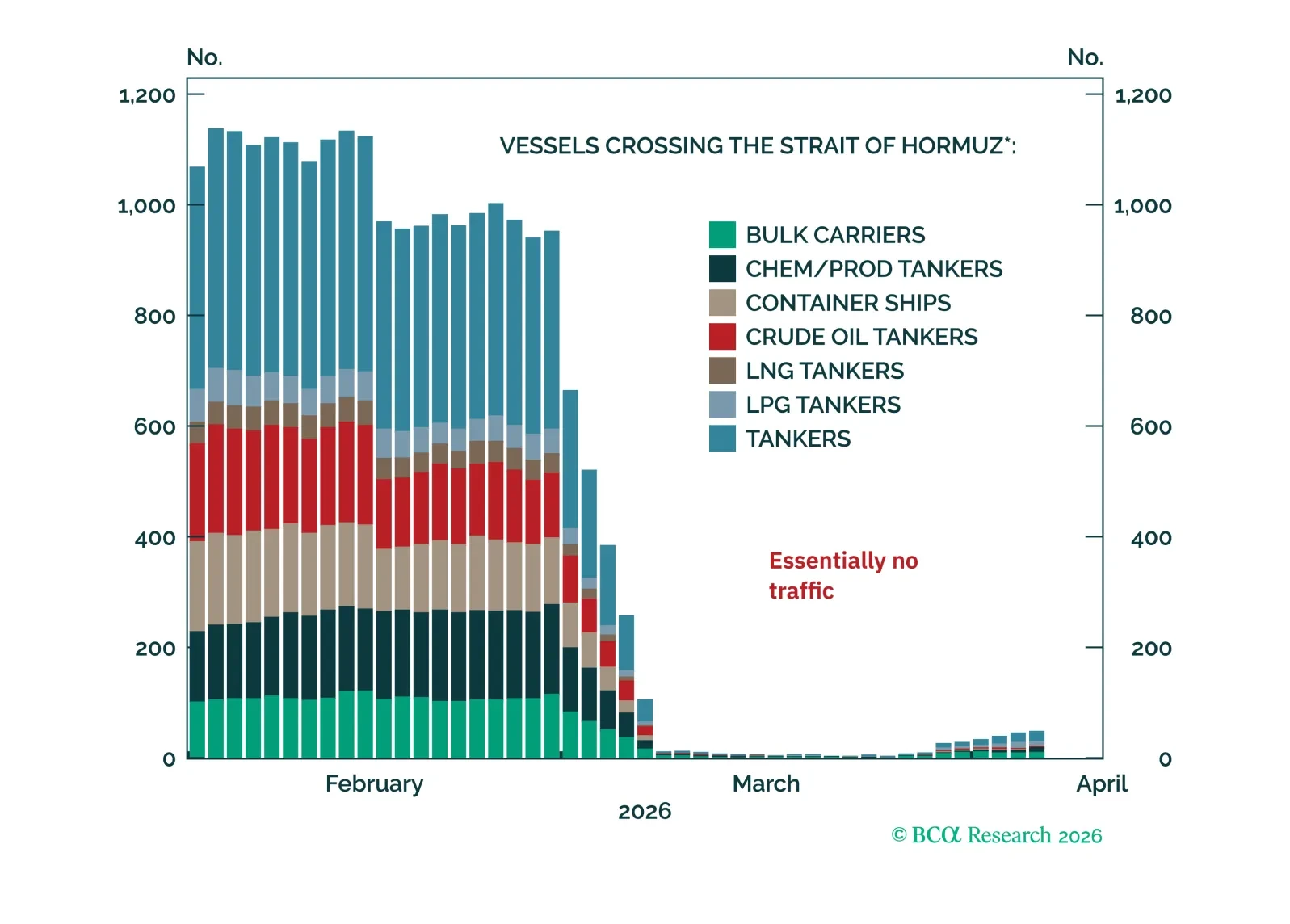

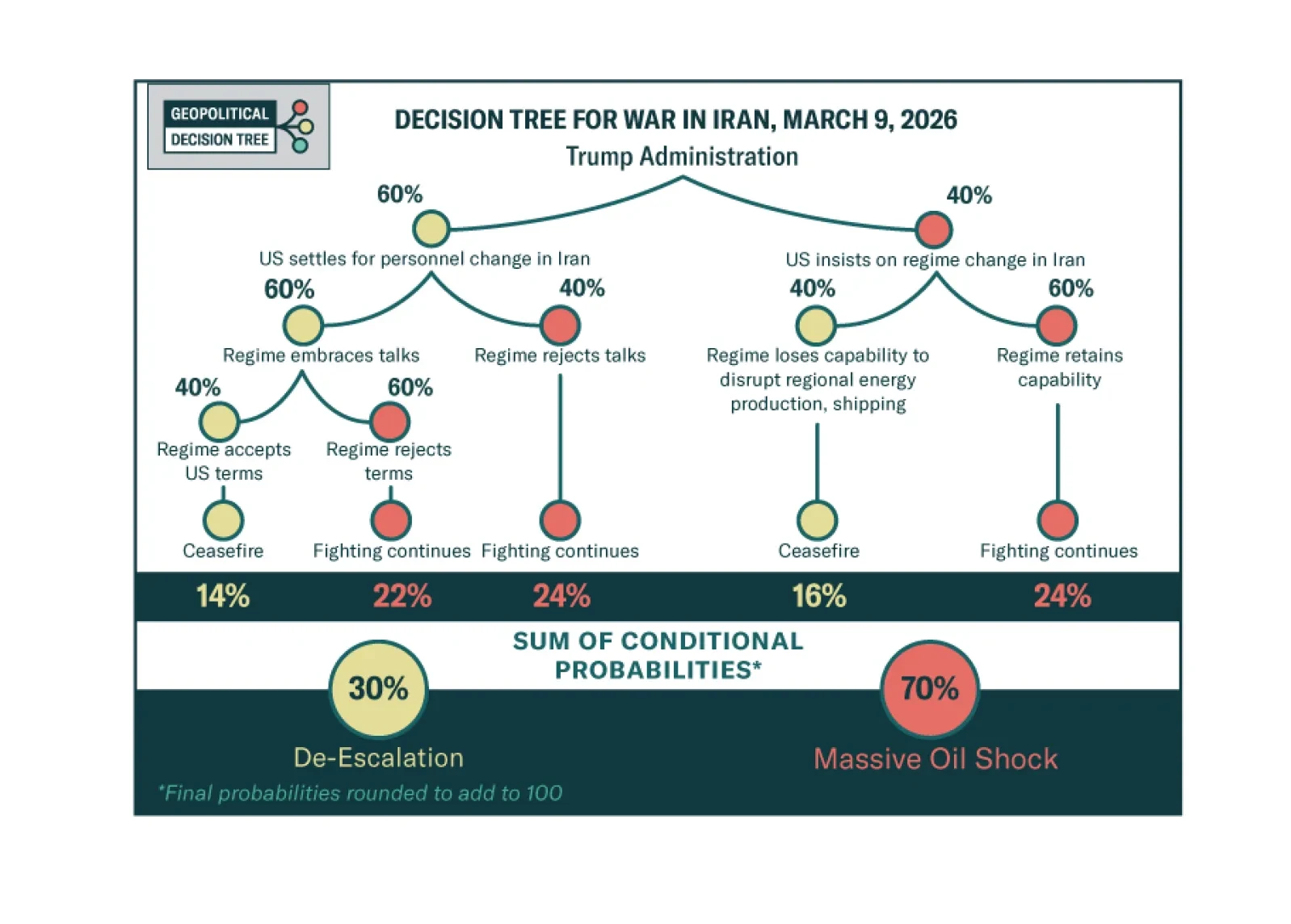

The Iran war is likely to re-escalate later this year even if shipping somehow resumes in the very near term — and yet an early reopening is looking less likely.

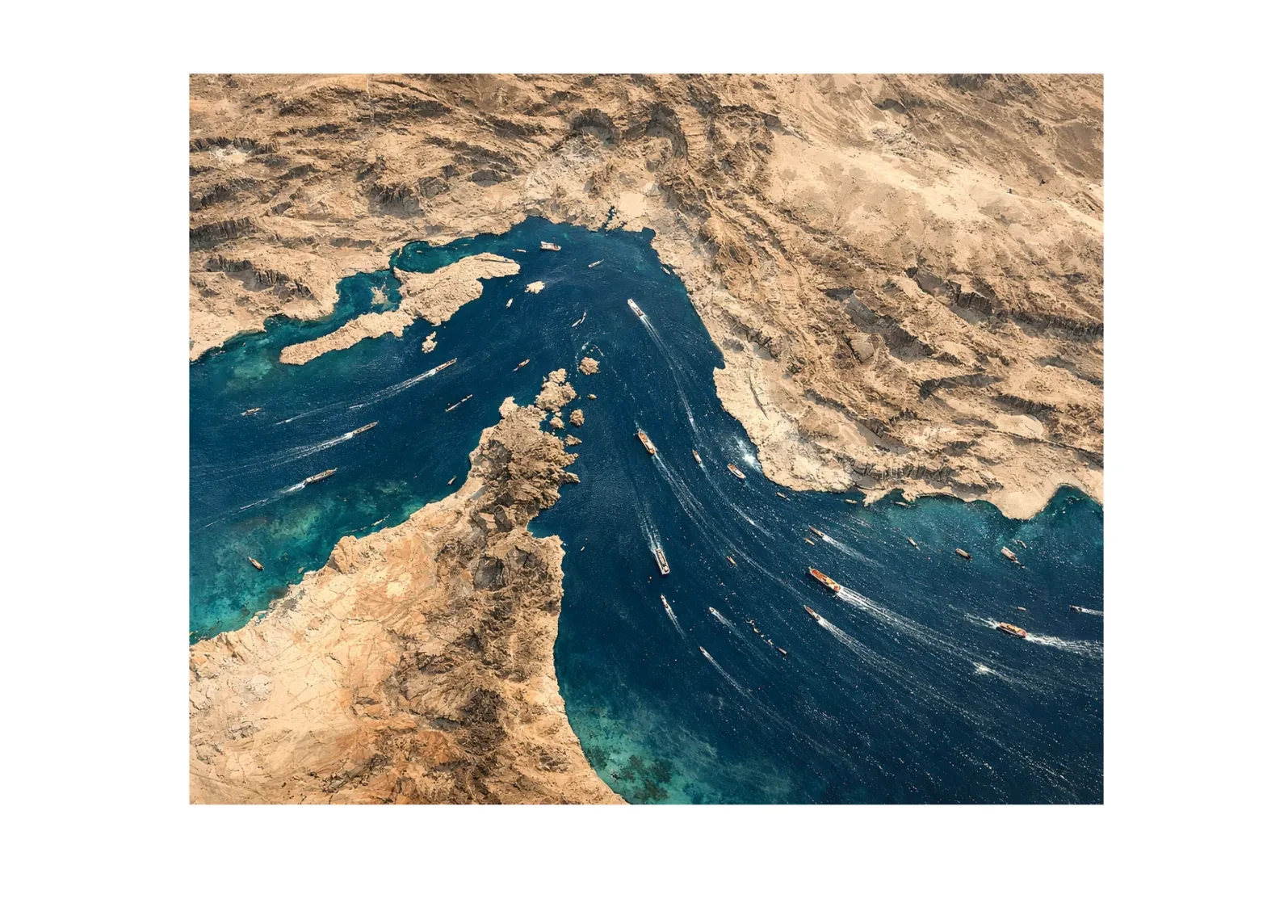

President Trump has announced that the US would impose a blockade on the Strait of Hormuz, in effect exacerbating the partial blockade that has already been in place due to Iran’s threats against shipping in the Persian Gulf. The threat comes after the direct negotiations between Iran and the US in Islamabad failed to make a breakthrough. Oil is up on the news and stock futures are down. How should investors read the situation?

Domestic politics suggest that President Trump needs to retreat from the war in Iran, but strategic factors suggest not. Stay defensive for now.

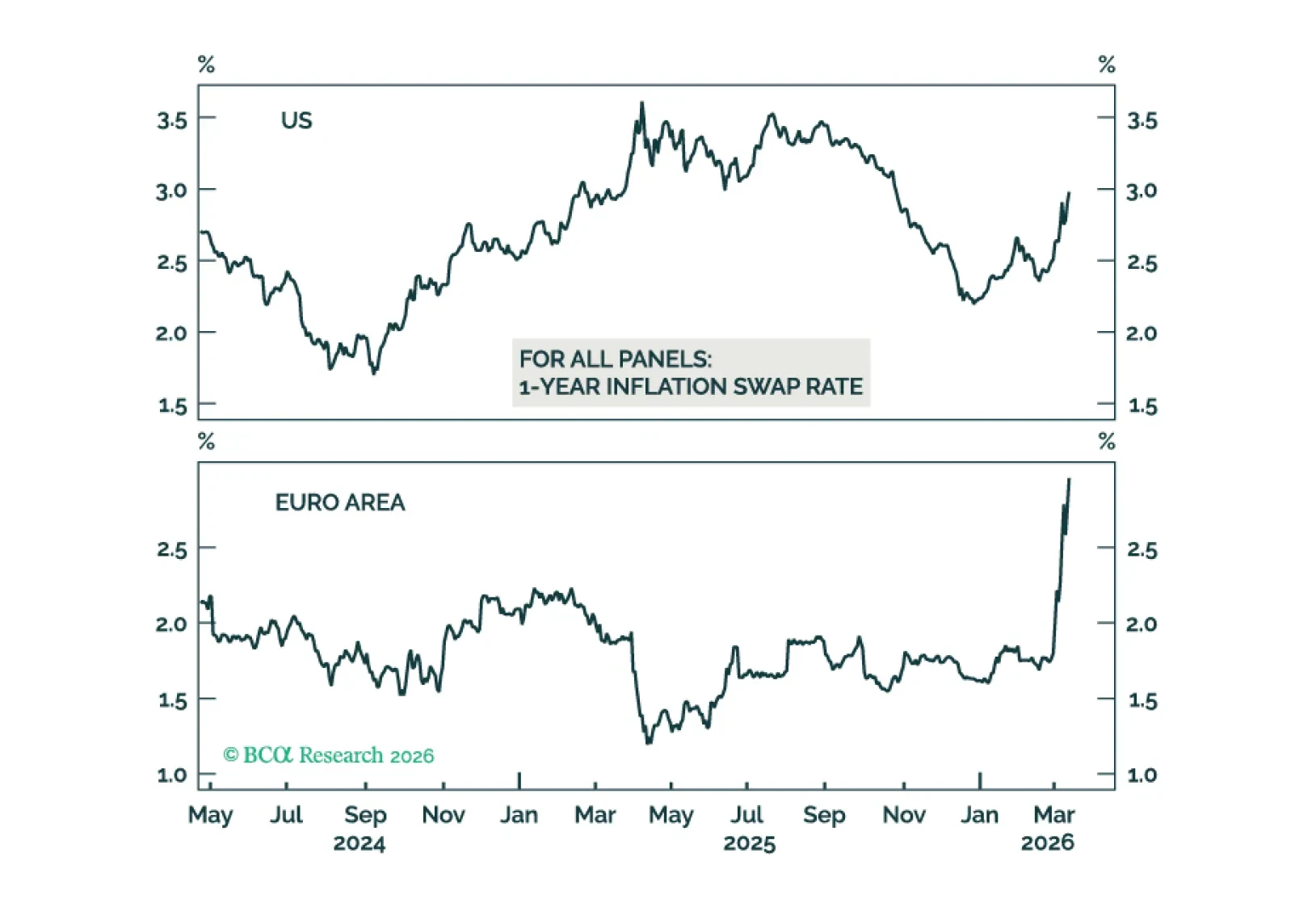

The spike in oil and gas prices has raised the odds of a global economic downturn. Combined with a more negative signal from our MacroQuant model, this warrants tactically downgrading stocks from neutral to underweight. Looking further ahead, the Iran war will lead to bigger defense budgets and a greater focus on energy self-sufficiency.

Close oil trades tactically, but beware lingering economic costs of the Iran war this year.

The president did not announce significant new tax cuts or economic stimulus.

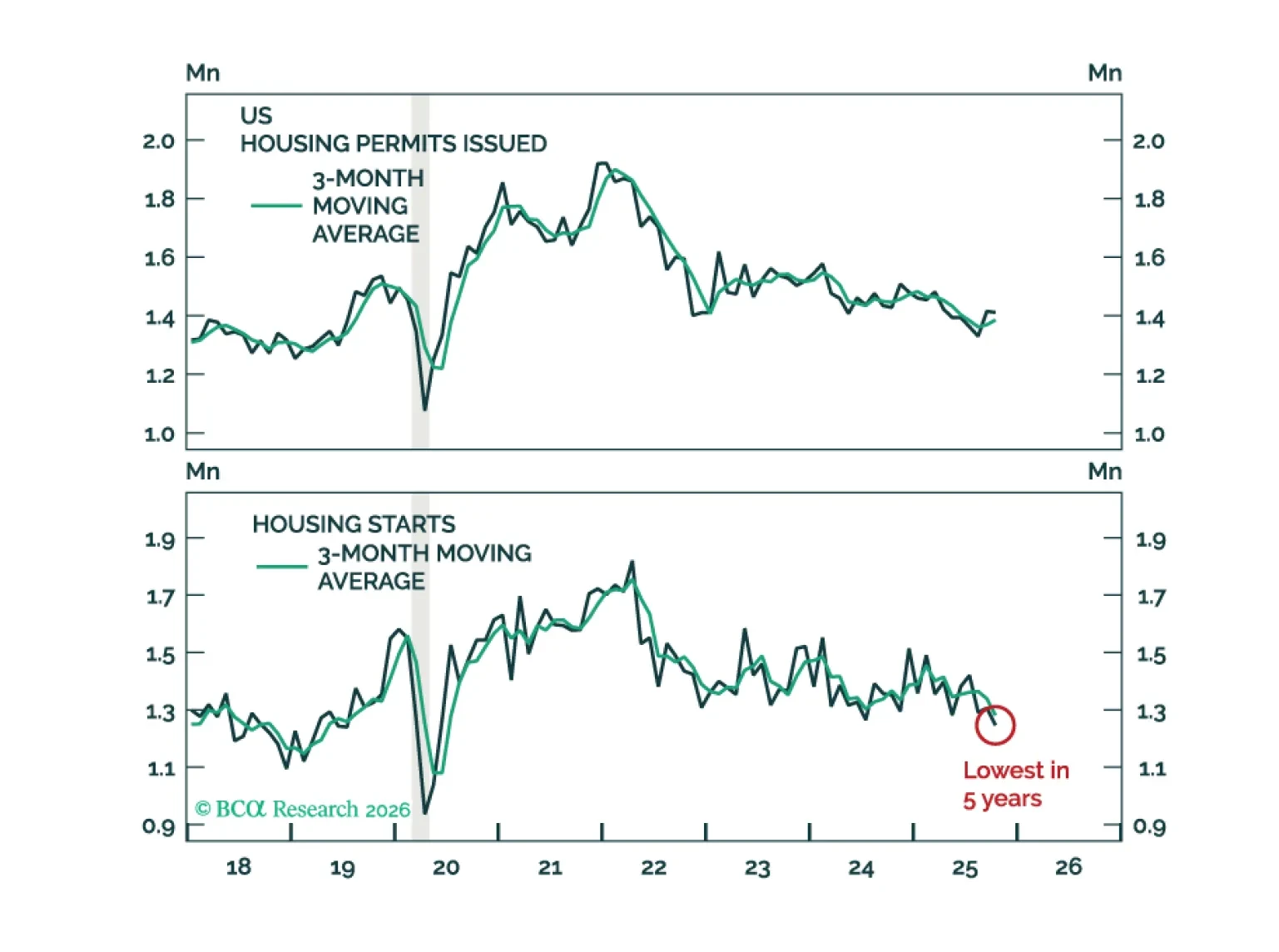

The US residential real estate market remains soft. While the decline in mortgage rates is a positive, it is too early to bet on housing becoming the engine of growth for the US economy this year.

Recent economic data have been reasonably firm. We will cut our 12-month US recession probability to 40% from 50% if the Supreme Court strikes down President Trump’s tariffs. This would take our scenario-weighted year-end 2026 price target for the S&P 500 to 6375 from 6200.

The US is ripe for a third major political party, but the two-party system will probably prevail in the 2028 election. The macro context will determine whether the US elects a left-wing populist.

Markets have ripped in July, ignoring underwhelming payrolls and retail sales figures. This was our bet, so we don't think this is a mistake. The economy is transitioning from one catalyzed by cash to one led by lower borrowing rates. The combination of a growth slowdown tempered fiscal policy, and an uber-dovish Fed is good for bonds and equities, which has not yet been priced by markets.