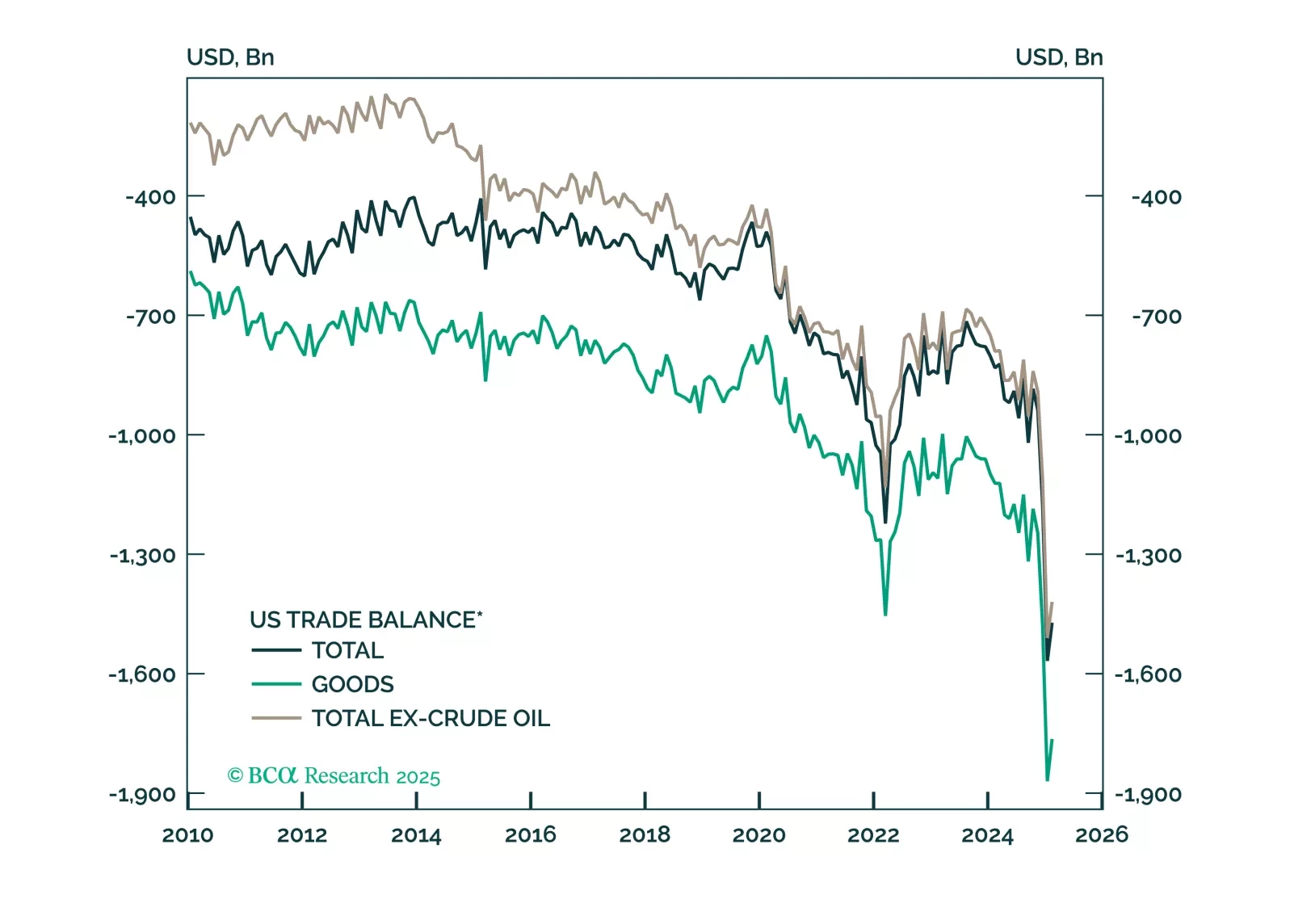

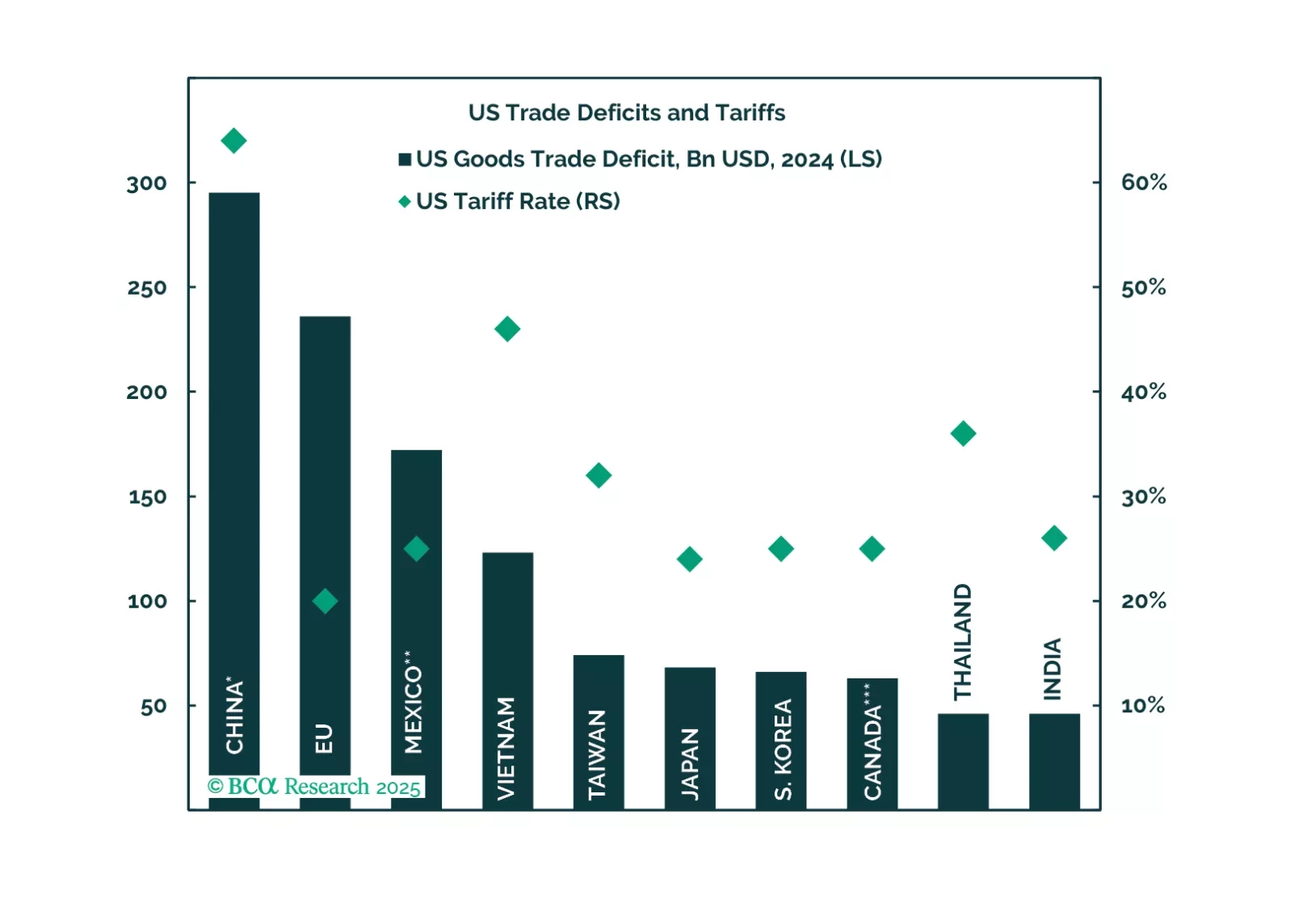

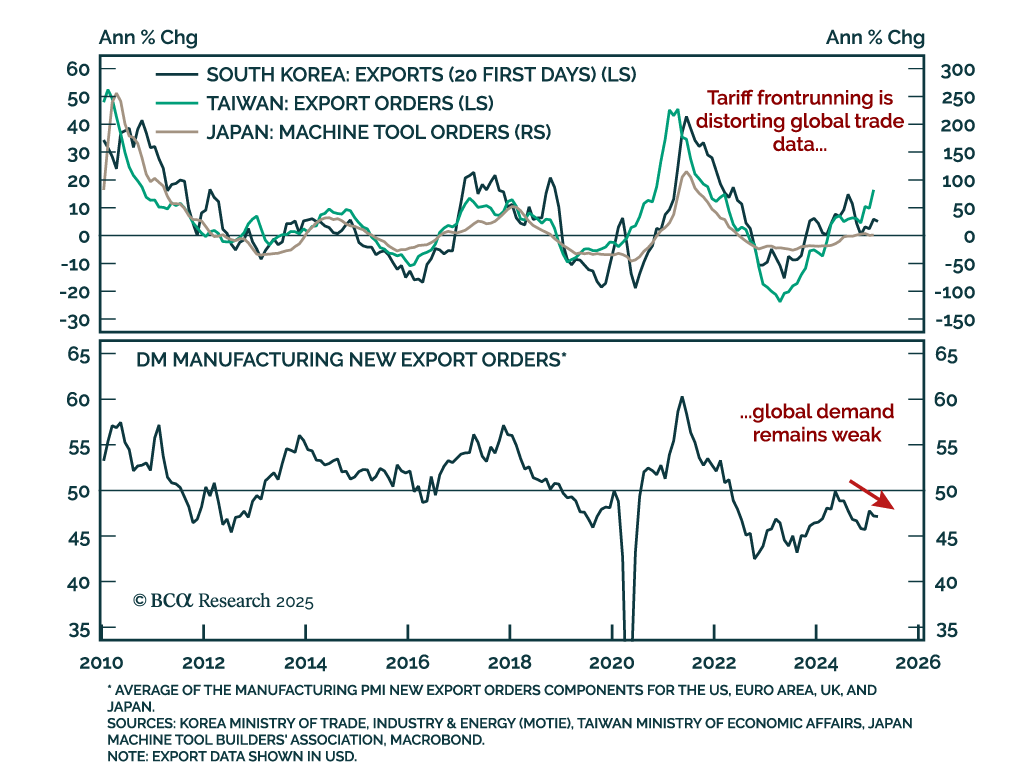

Trade / BOP

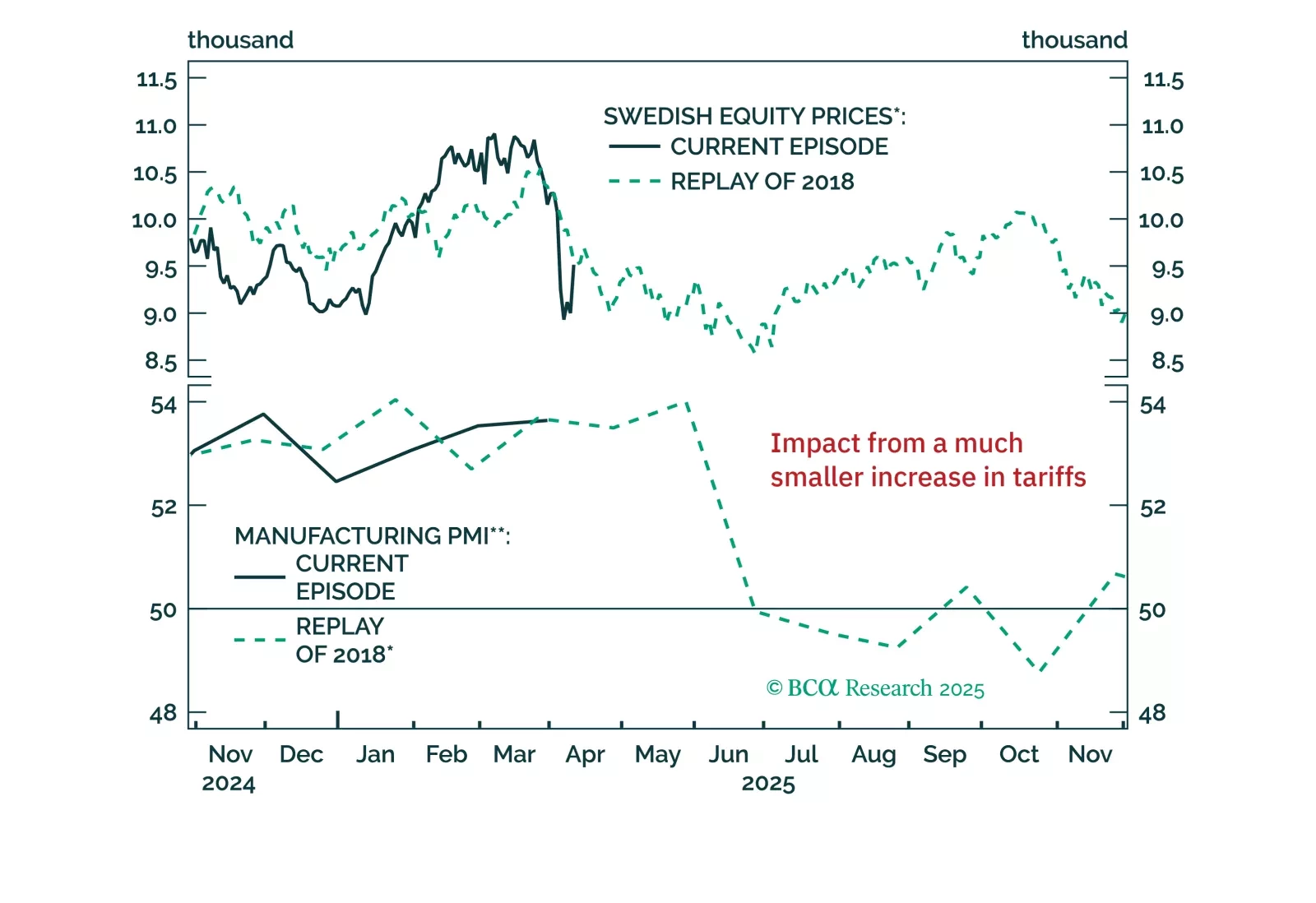

Europe’s near-term outlook remains clouded by uncertainty, even after the tariff reprieve. Our latest update breaks down why the risks to growth, profits, and financial conditions are still skewed to the downside — with Sweden standing out as a key bellwether.

This week, we look at the sustainability of the HKD peg as the next whale to move markets, given what is happening to tariffs. After careful analysis, our bias is that it is here to stay. With the DXY dipping below 100, we are likely to see a rebound, which is actually bad news for the Hong Kong region of China, since it will tighten financial conditions. We have no new short-term trades, but if the peg broke, you want to be short HKD/JPY.

Barring a dramatic further de-escalation of the trade war, the US and much of the rest of the world will enter a recession over the next few months. Investors should remain defensively positioned for now.

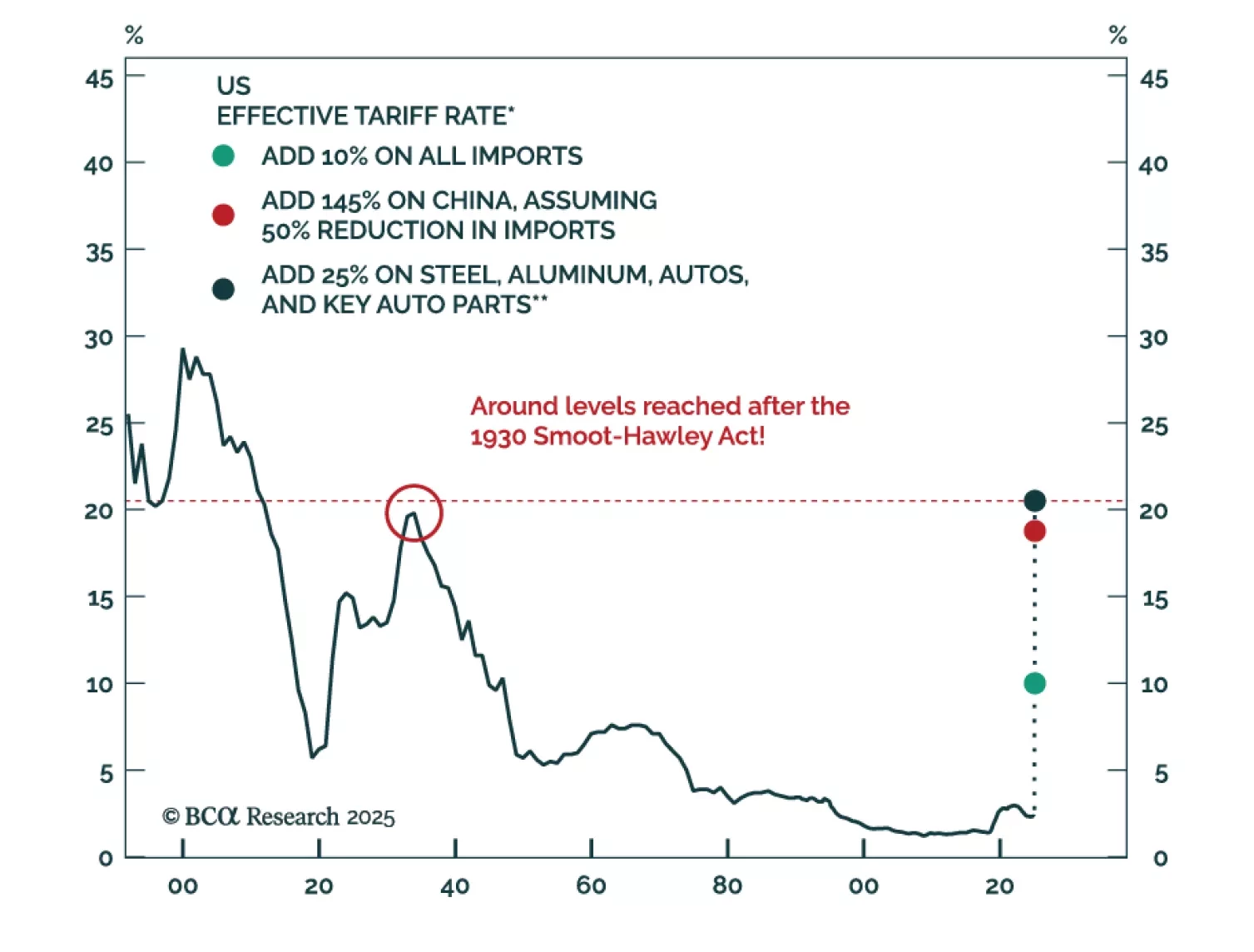

This report looks at the FX implications of the Trump tariffs, and the review of our Q1 trades.

Trump's Tariff D-Day brings a negative surprise to financial markets already anxious over a declining US cyclical economy. Investors should sell risky assets, increase safe havens, and overweight US assets in the near term.

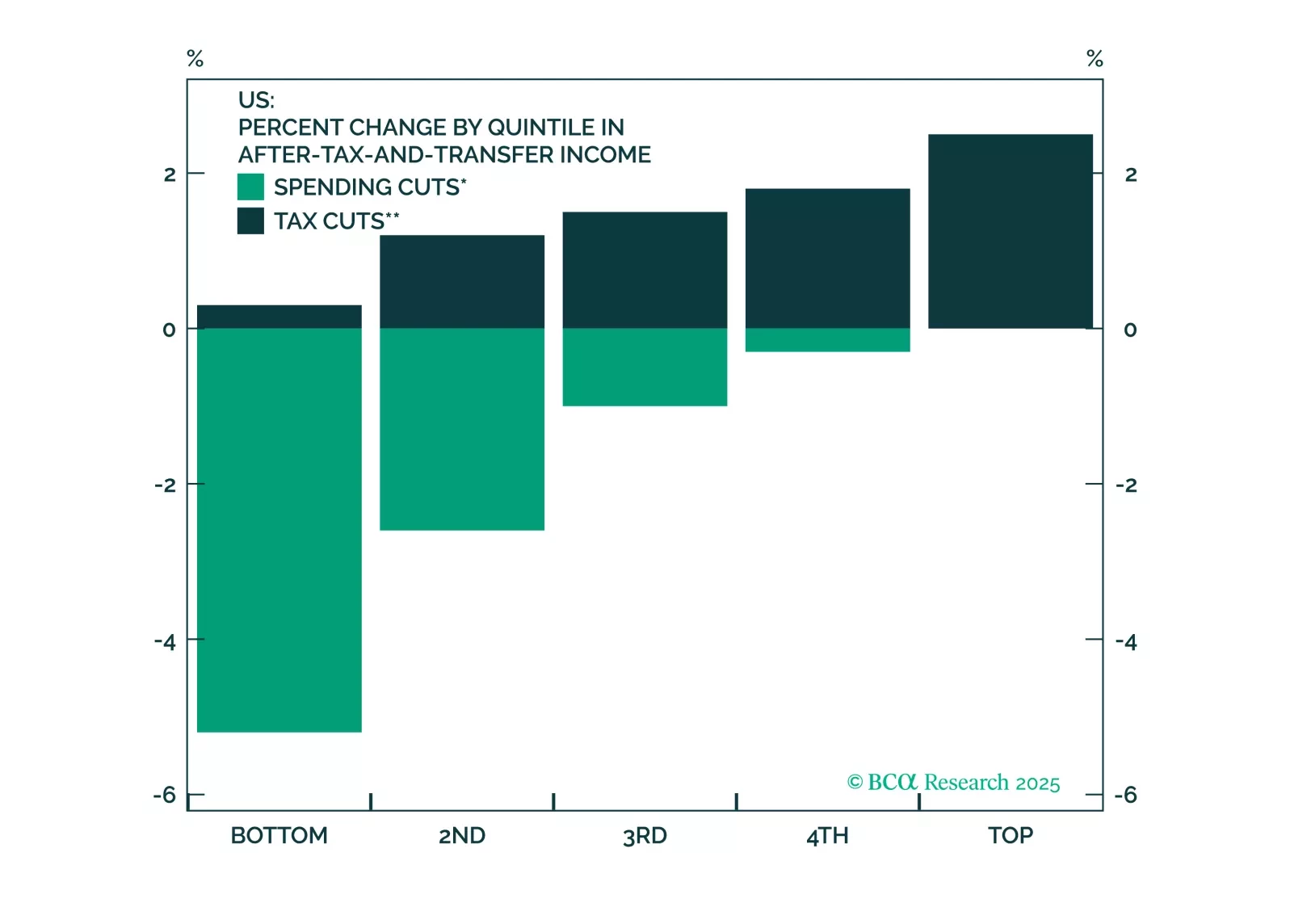

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

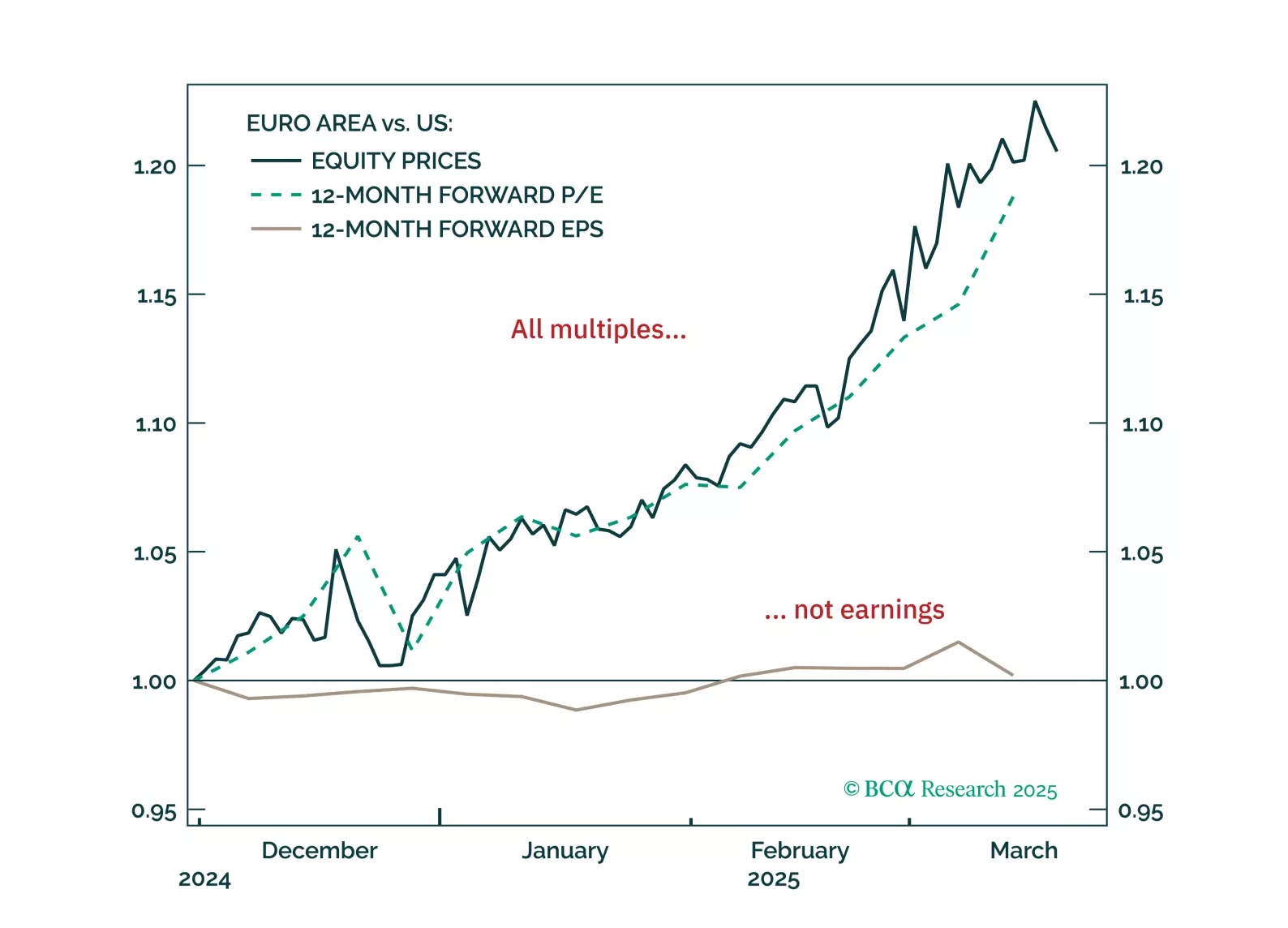

European equities have surged on hopes of a low-inflation boom—but the rally has likely gone too far, too fast. With a pullback now likely, how should investors position themselves over the next 3–6 months?

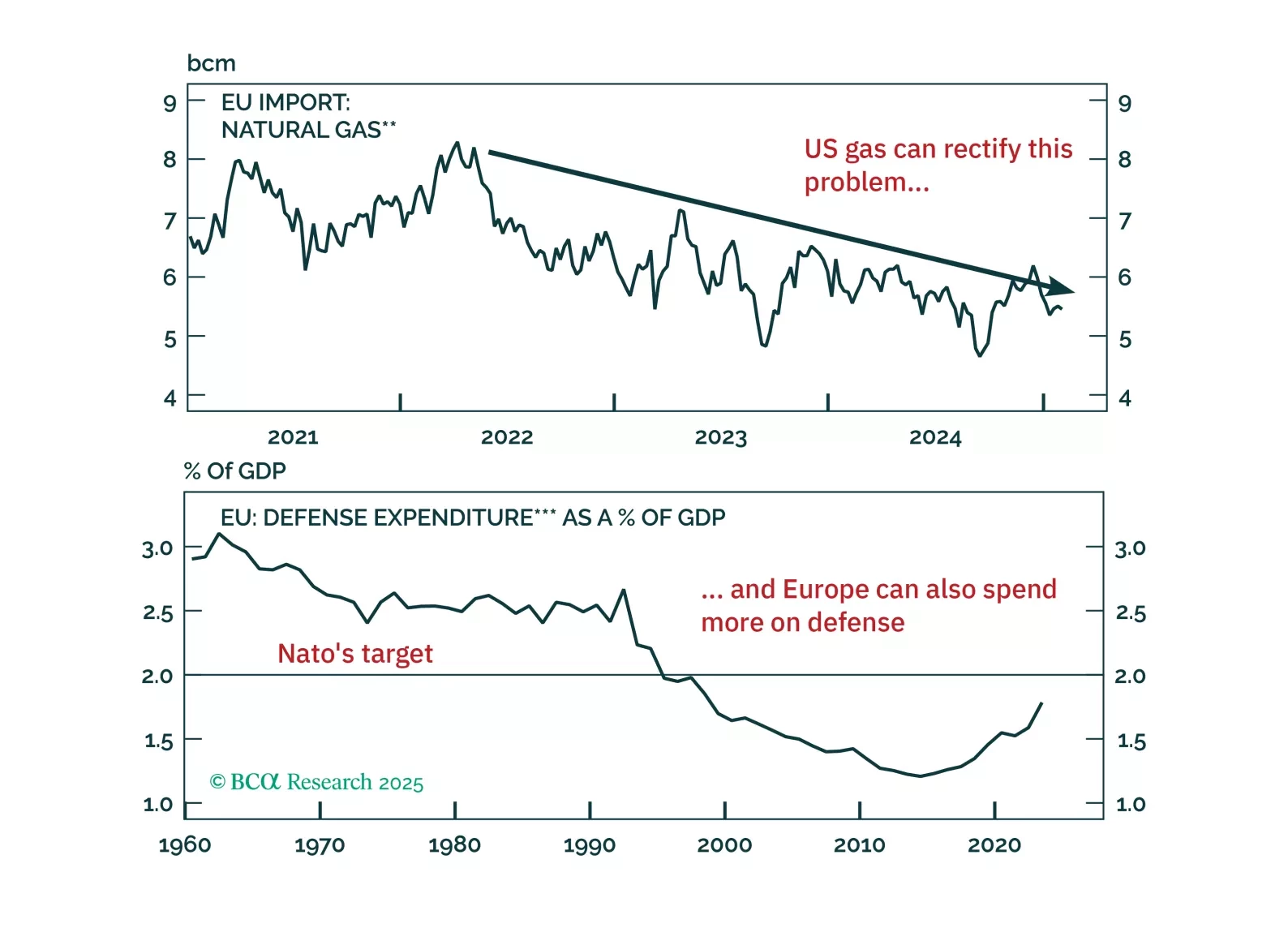

Europe is about to become President Trump’s next target. The good news: a US/EU trade war will be short as common ground to achieve a deal exists. The bad news: European assets remain at the mercy of heightened uncertainty. How should investors position themselves in this tricky context?