Technology

Global semiconductor stocks have returned 50% YTD in USD terms, and a whopping 200% since their September 2022 lows. However, they may have peaked back in July. Our Emerging Market strategists highlight a significant bifurcation between the revenues of…

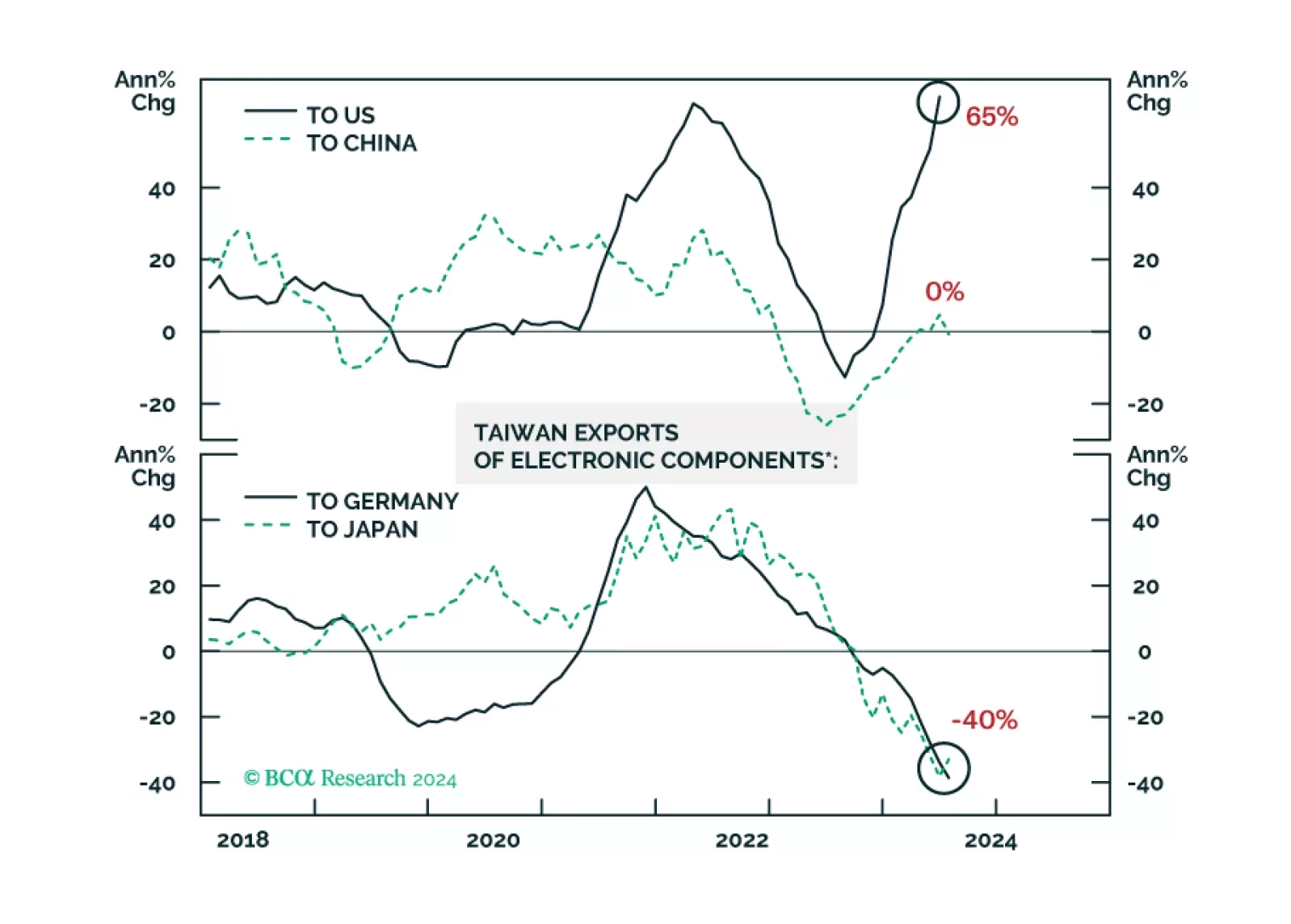

According to BCA Research’s Emerging Markets Strategy Service, China has been accumulating high-value memory semiconductors in anticipation of further US restrictions. Since October 2022, the US has been tightening rules that would limit China’s progress…

There has been a decoupling within the global semiconductor industry. Demand for AI and advanced chips has been booming. Yet, sales of legacy and non-AI semiconductors have failed to recover. Given their spectacular run-up, share prices of high-end and AI-chip producers might continue selling off even if their sales continue to grow rapidly.

The Q2 2024 earnings season is drawing to a close with 93% of S&P 500 companies having reported results as we go to press. Nearly 80% (60%) of companies have topped earnings (sales) expectations in Q2, according to Factset. Excluding Materials and Real…

According to BCA Research’s US Political Strategy service, in the final months of an election cycle, equities underperform relative to non-election years. This extends further into Q1 of the following year due to uncertainty. Once the election results are…

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.

Singapore is a small open economy sensitive to global trade dynamics. Its non-oil exports (NODX) are thus a good bellwether for global growth conditions. They rebounded sharply in July from a previous contraction, largely exceeding expectations. Notably,…

August’s selloff has featured a rotation out of Big Tech. The Nasdaq shed 8% across Thursday, Friday, and Monday, led by concentrated selling among several Mega caps. Nvidia, Tesla, Microsoft and Amazon shed 14%, 14%, 6% and 14% over the last three sessions,…

Today’s AI craze bears some resemblance to the late-1990s dotcom boom. We highlight three lessons from that period which are relevant today. Lesson #1: Productivity gains from the rollout of a new technology can take time to accrue. The dotcom…

According to BCA Research’s US Equity Strategy service, the market is overestimating the odds of a soft landing. Our colleagues’ client polls have shown that 59% of respondents expect the US economy to achieve a soft landing; this number has been bolstered…