Technological Advances

This Special Report is a timely reprise of a speech that I gave at the London School of Economics on our understanding and misunderstanding of generative AI. In neurological terms, generative AI has a ‘super-neocortex’ which means that it can thrash humans in abstract thinking, or IQ. But crucially, generative AI does not have a ‘limbic system’ which means that it will lag well behind humans in emotional intelligence, or EQ. I hope you find the speech insightful and provocative, especially on how we might have completely misunderstood human intelligence and super-intelligence, and the economic and societal implications for the coming decade.

Countries and commercial operators are racing into space to accrue economic gain from space exploration. In coming years, the space industry will continue to grow, as humans venture into space for tourism, mining, farming, and even habitation. The industry is still in its infancy but has tremendous potential. We believe it is one of the next big investment ideas. We will monitor the theme and take on investment exposure once it matures.

Outperformance of Growth sectors most likely has run its course. It is time to shift Growth vs. Value allocation to neutral, downgrade Semis, and upgrade Energy to overweight.

Investors should think probabilistically about the economy and financial markets. In the face of non-linear effects, the range of possible outcomes can be very large. A systematic application of Bayes’ rule can help improve decision-making.

Investors remain cautious about the US economy and still have significant cash that needs to be put to work which could extend the rally further. Earnings rebound later in the year will be supported by rising sales growth and surging earnings of the Magnificent Seven. A restocking cycle, and a pickup in freight activity support transports. Upgrade Transports to an overweight.

Among the critical materials needed for the global energy transition, Li is expected to see the largest increase in demand from 2022 to 2050. Li supply is not constrained, but continued investment in mining and refining will be required to meet increasing demand. We expect strong Li-ion battery demand in the major economies of the world – the EU, US and China – will keep a bid under Li, and allow growing supply to find a home. At tonight’s close we are getting long the LIT ETF, consistent with our view.

We recommend a small structural exposure to cryptocurrencies and blockchain tokens, given their incipient real-world uses as well as their proven hedging qualities against the debasement of fiat money and in banking crises. In this Special Report, we rank the major blockchains on five factors – developer activity, adoption, decentralization, scalability, and security – from which we arrive at our top five blockchains.

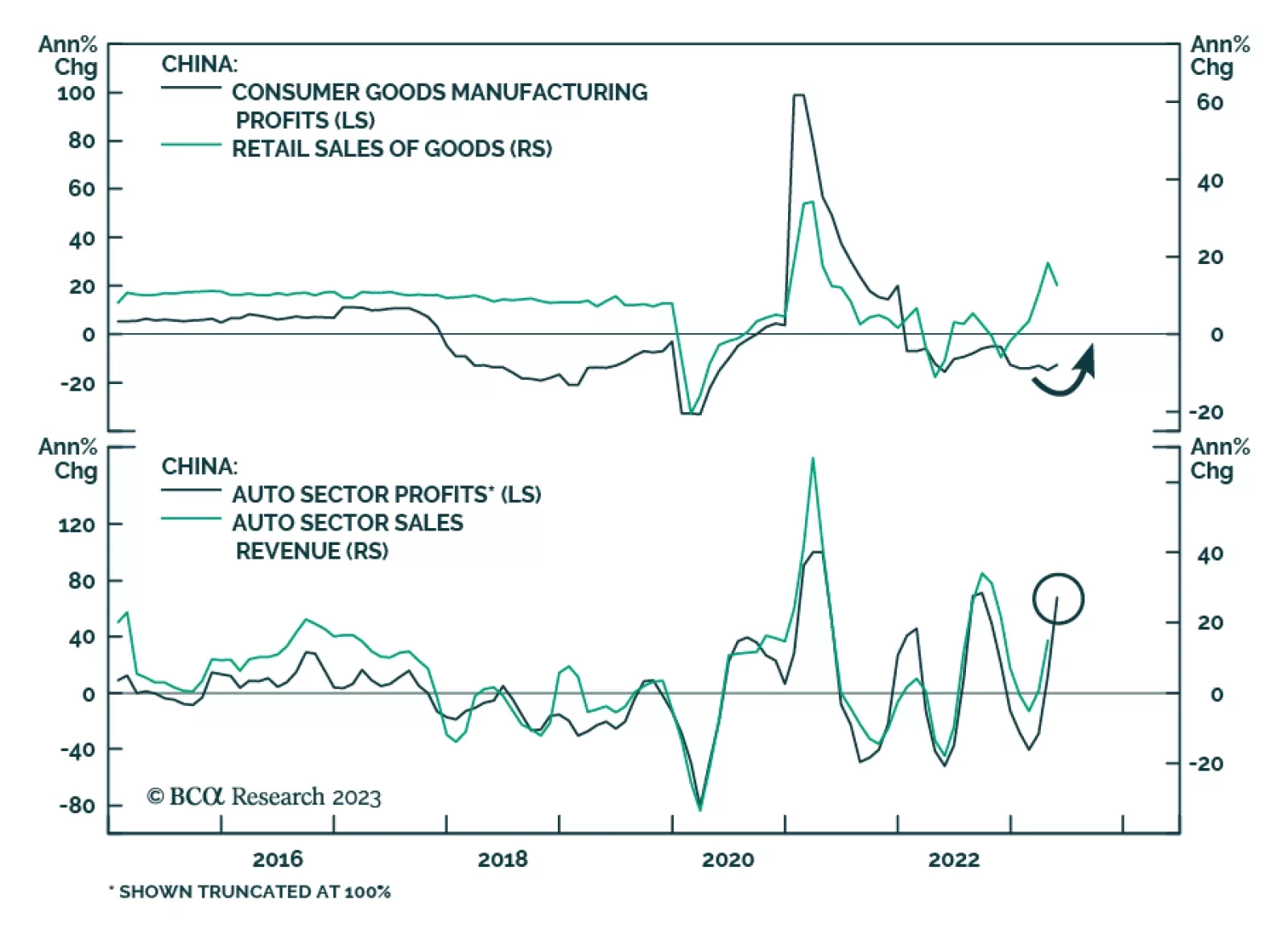

Both EV and Green Energy themes still hold strategic promise for investors, posing large upside, despite prevailing macro headwinds. While both themes have yet to claw back their pandemic peaks, a broadening of the rally supports a run for both, even in the face of high valuations.

The stratospheric valuation of this year’s AI mania is likely to deflate, just as it did after the Web 1.0 mania of the late 90s. We go through some long-term and short-term investment implications.