Technological Advances

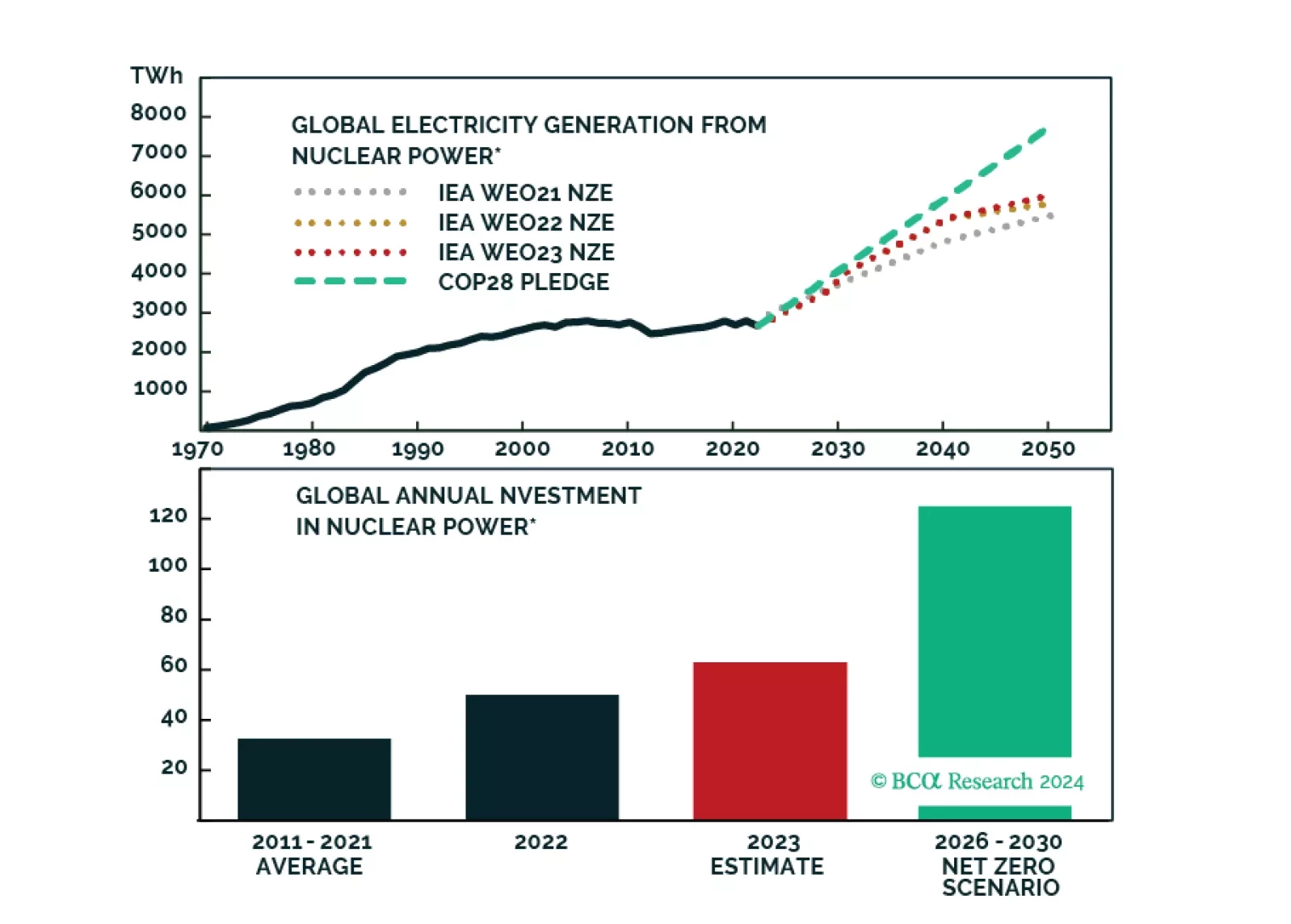

BCA Research presents a limited monthly special series about the Nuclear Renaissance.

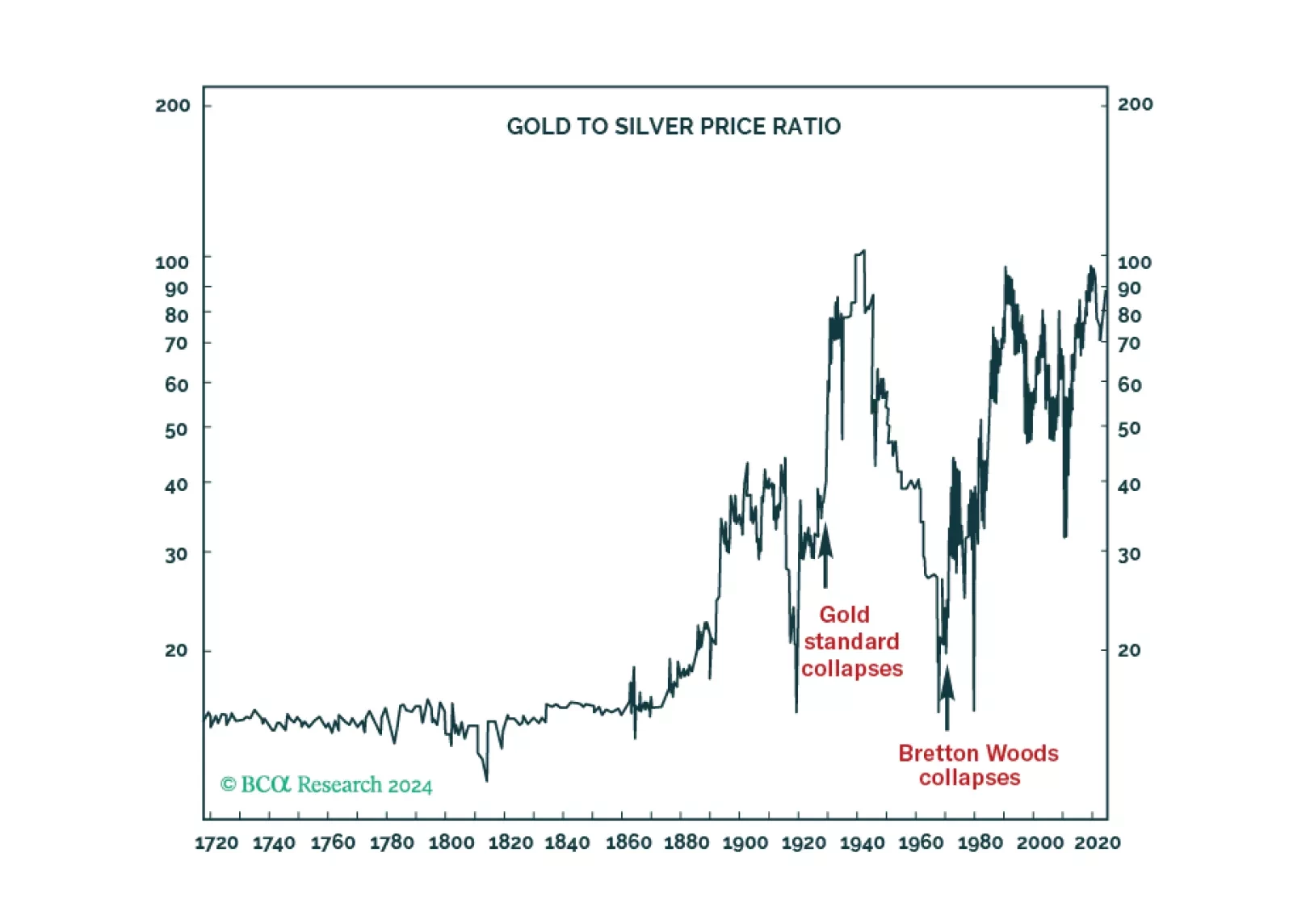

The SEC has just approved bitcoin spot ETFs, but does bitcoin have any ‘intrinsic’ value? In this Special Report we explain why the answer is yes, how bitcoin compares with gold, and why the bitcoin price could ultimately head well north of $100,000.

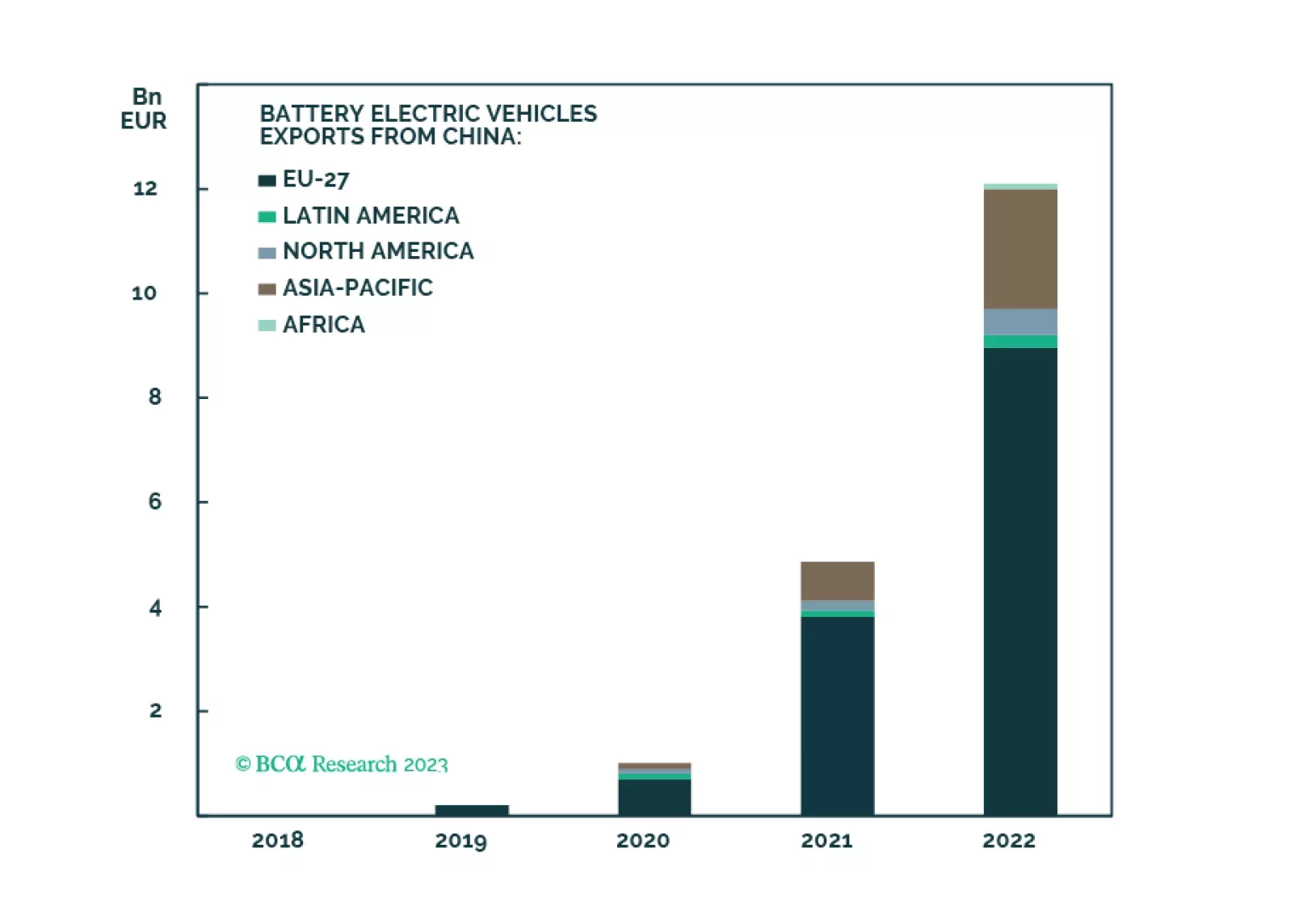

The expectation that China is best placed to win the global EV race presumes the persistence of the status quo. Reality, however, may differ as the sector looks set to be hit by a range of changes. If nonlinearity were to emerge in the global auto sector, as it often does, then the EV transition could end up spawning a very unexpected list of winners and losers.

Our 2024 outlook can be encapsulated into just 39 words and three key views. Key view 1: The end of China’s housing boom means the end of the world’s main growth engine. Key view 2: If the Fed and ECB don’t kill the economy, they won’t kill inflation. Key view 3: The AI gold rush will struggle to find any gold. We go through the investment implications for the year ahead.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

China’s push to dramatically expand its copper-refining capacity will be complemented by further vertical integration of mining assets. However, surplus refining capacity will push treatment and refining charges lower in the short run. The threat of EU tariffs on Chinese EV imports looms large, and could be costly to China’s expansion of its already-dominant supply-chain ecosystem for EVs and metals refining. We remain long the XME and COMT ETFs to retain exposure to metals miners and refiners.

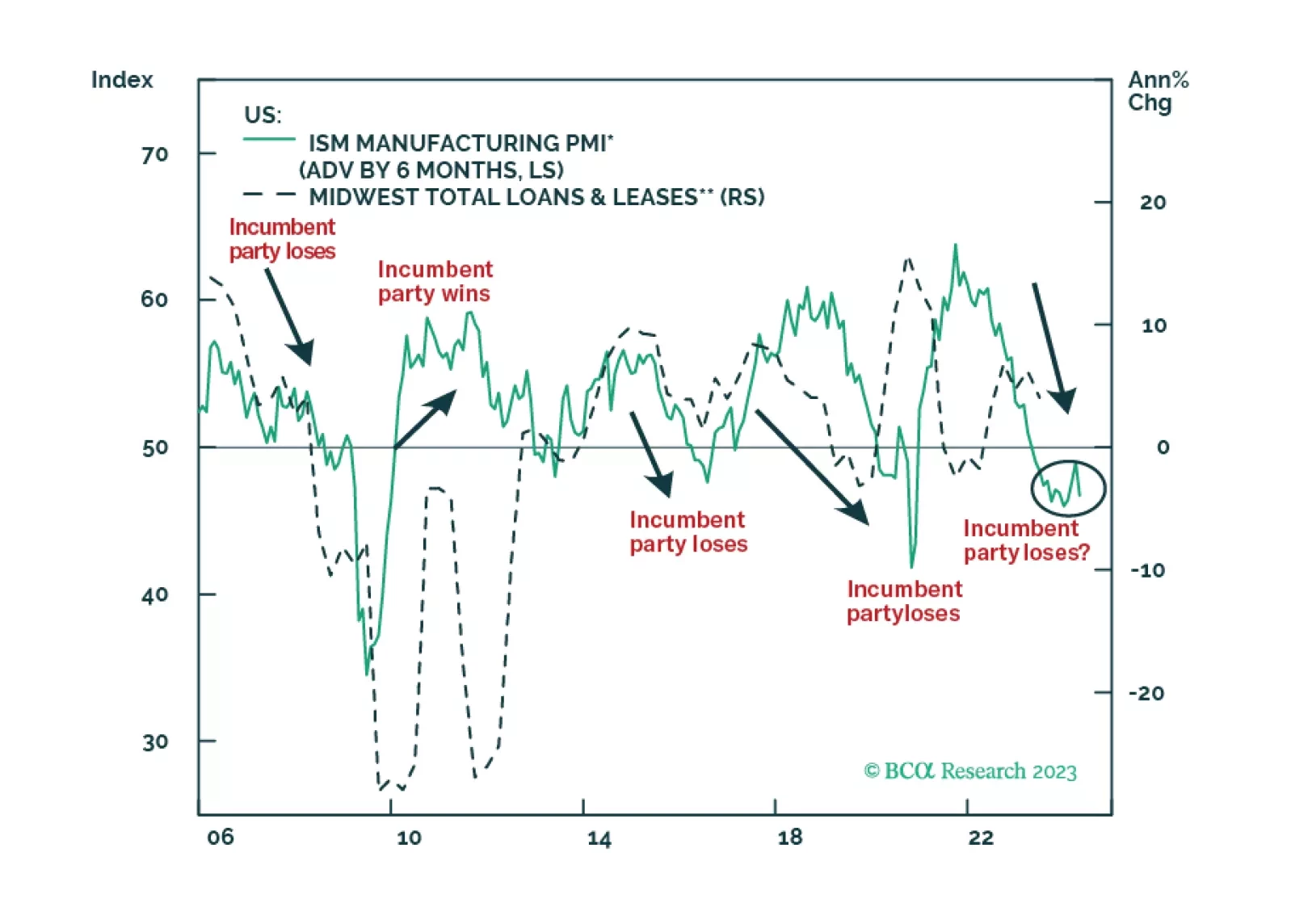

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.

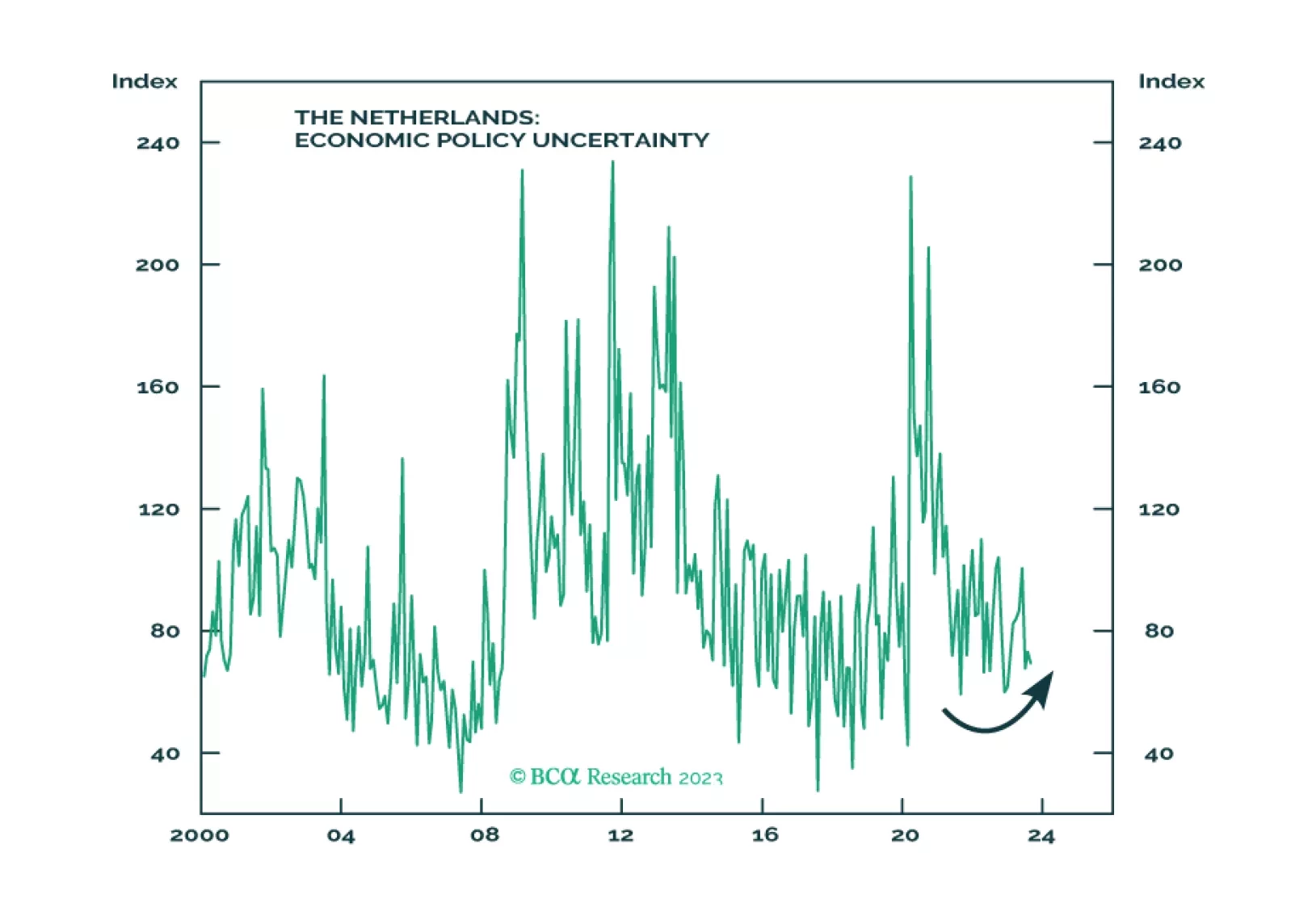

The Netherlands has a healthier and more stable economy and demography than its European peers. Investors should stay overweight developed European equities, including Dutch equities, relative to emerging European equities.

The EU’s transition to a carbon tax launched this week via its Carbon Border Adjustment Mechanics (CBAM) will lead to higher inflation in the medium term (3 – 5 years out), and will stoke consumer (i.e., voter) antipathy if it becomes effective in 2026. As a result, the tax will be watered down. Food and energy prices are particularly at risk, as imported fertilizers, and electricity-generation and -transmission components made from steel and aluminum are affected by the CBAM. We remain long oil, gas and metals equity exposure via the XOP, XME and COMT ETFs. We also remain long gold to hedge inflation.

Bulls and bears have capitulated, and the majority of the clients surveyed expect a rangebound market in the near term. Our fair value PE NTM indicates that the S&P 500 is only modestly overvalued. The continued outperformance of the Magnificent Seven faces multiple hurdles. Meanwhile, fiscal spending is unlikely to create an impetus for another leg up in equity performance.