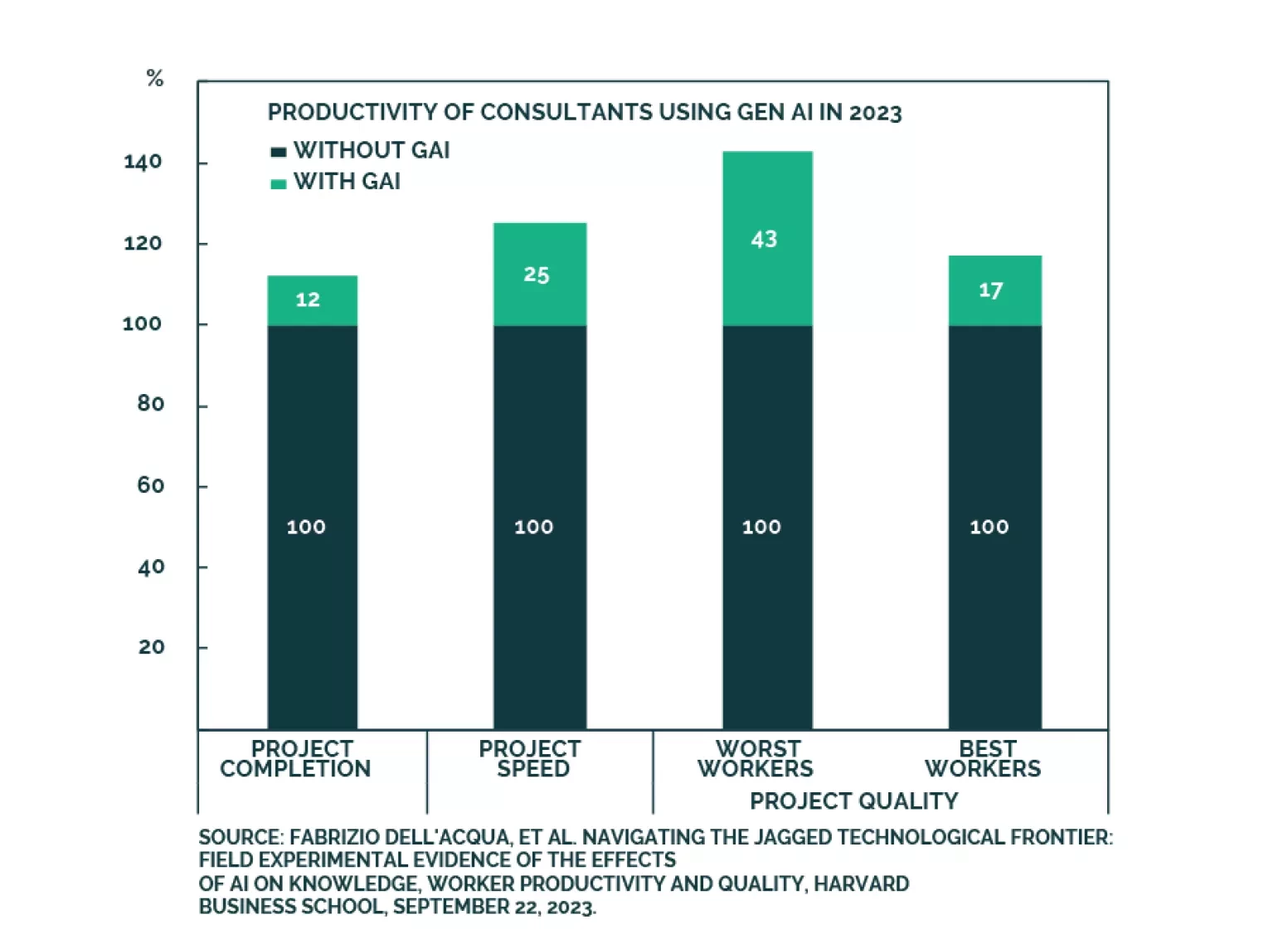

Technological Advances

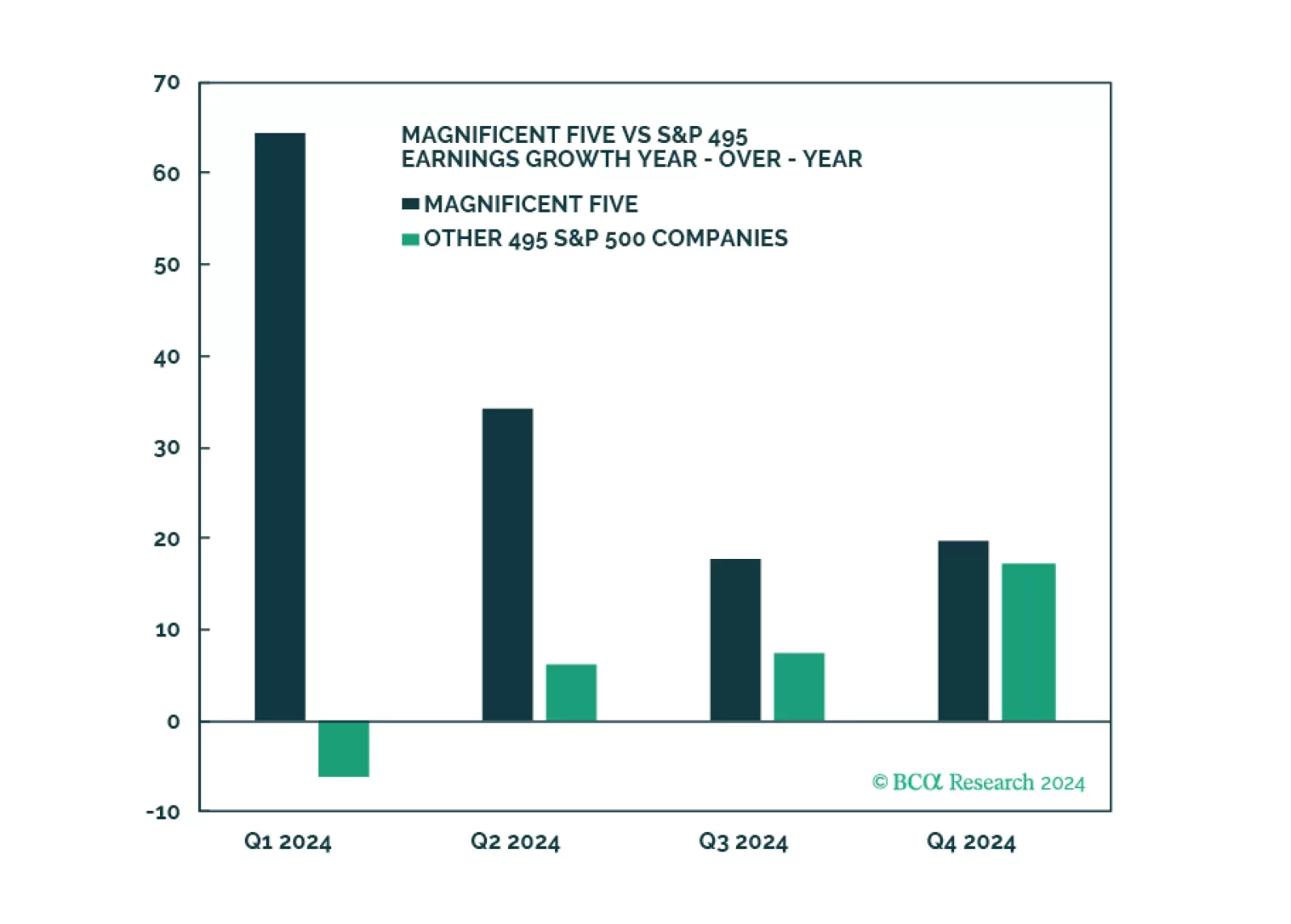

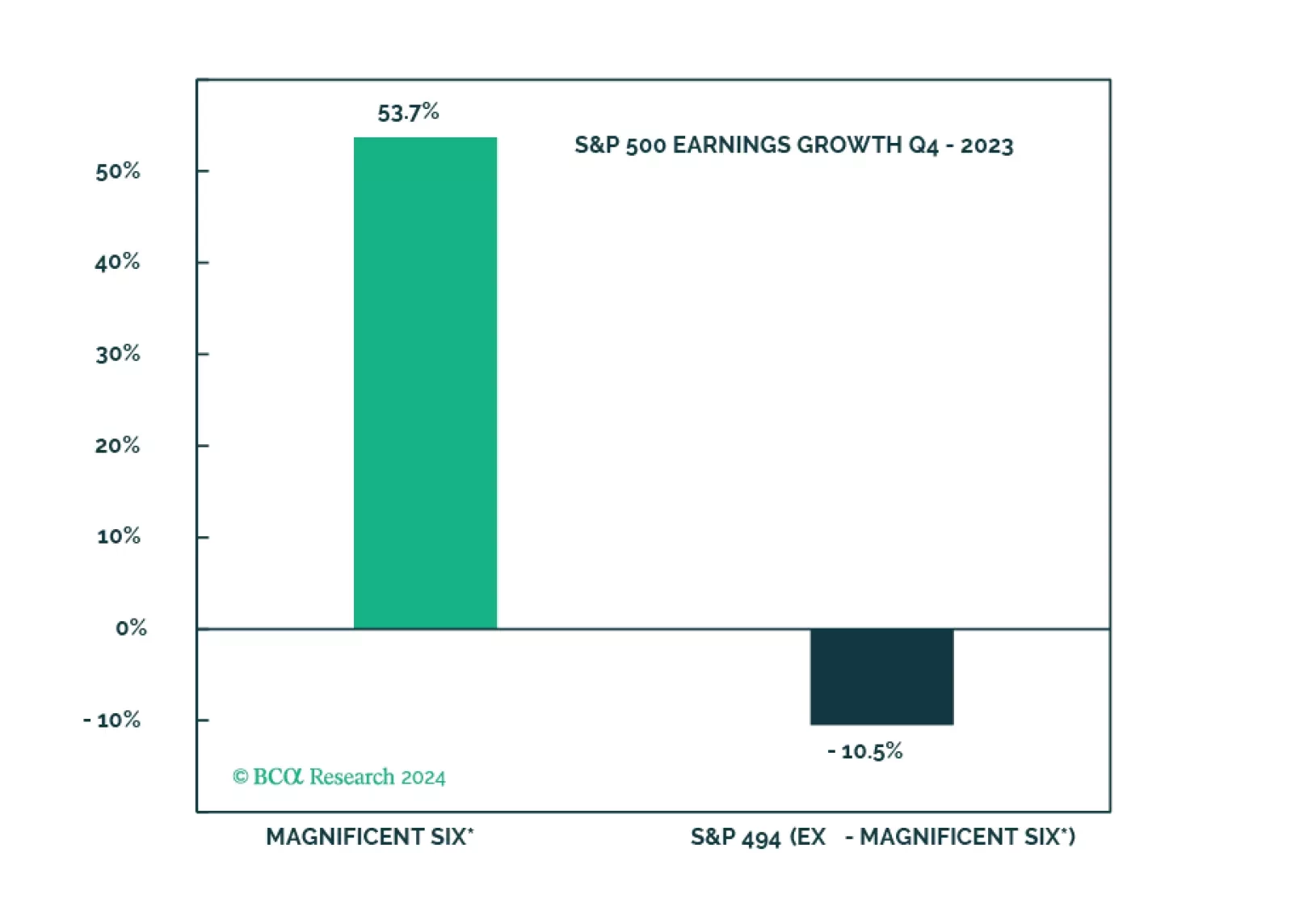

Q1 Earnings and sales growth were strong, but the devil is in the details: Without the Magnificent Five, earnings growth for the index would have been negative. On a positive note, margins have stabilized, and earnings growth is expected to broaden into yearend. Companies are optimistic about the economy. Development of AI applications is in full swing, but few companies are monetizing them yet. Consumer spending is strong but is slowing. We reiterate our underweight of consumer sectors, and overweight of Software and Services as the “don’t fight AI” adage holds.

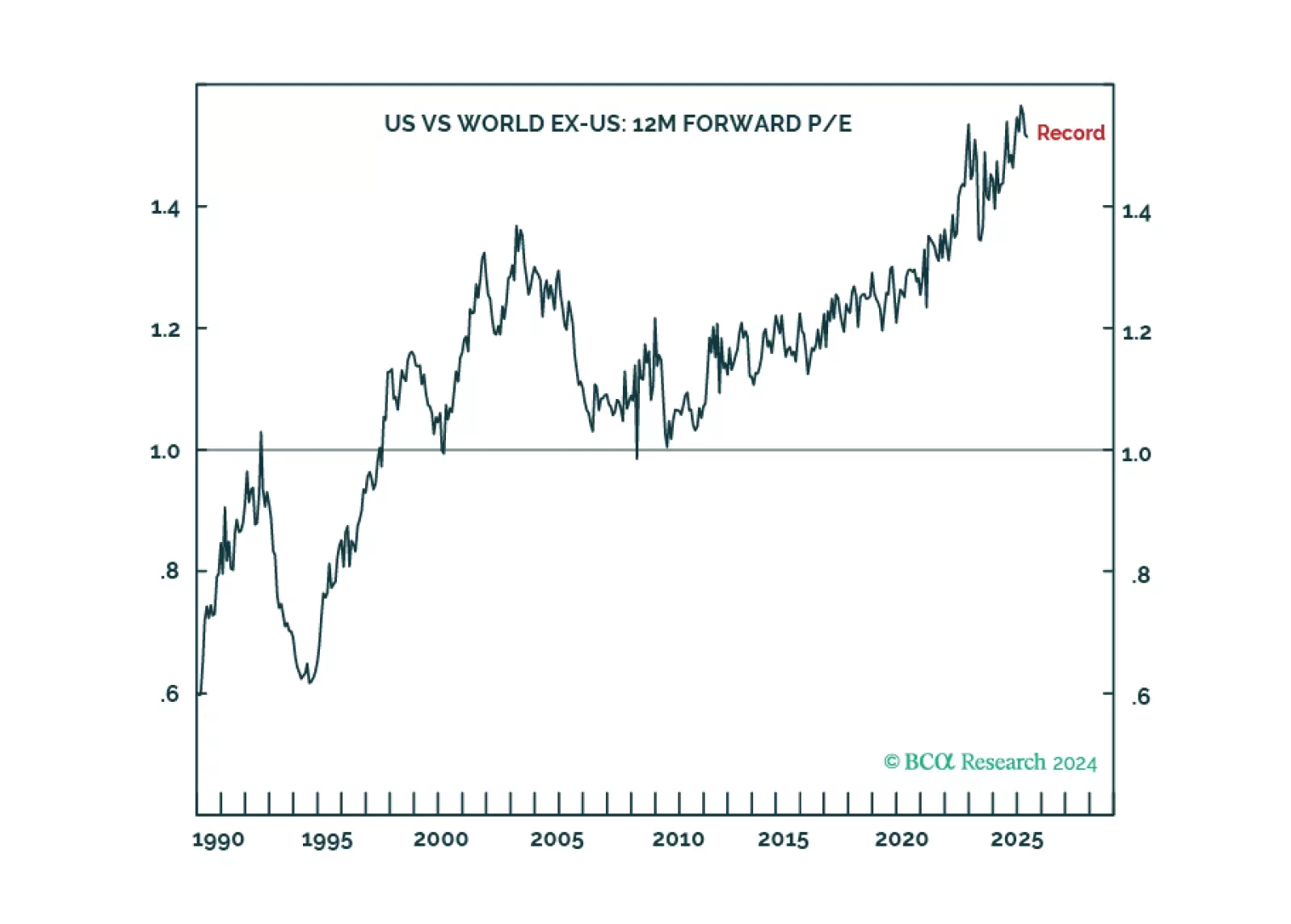

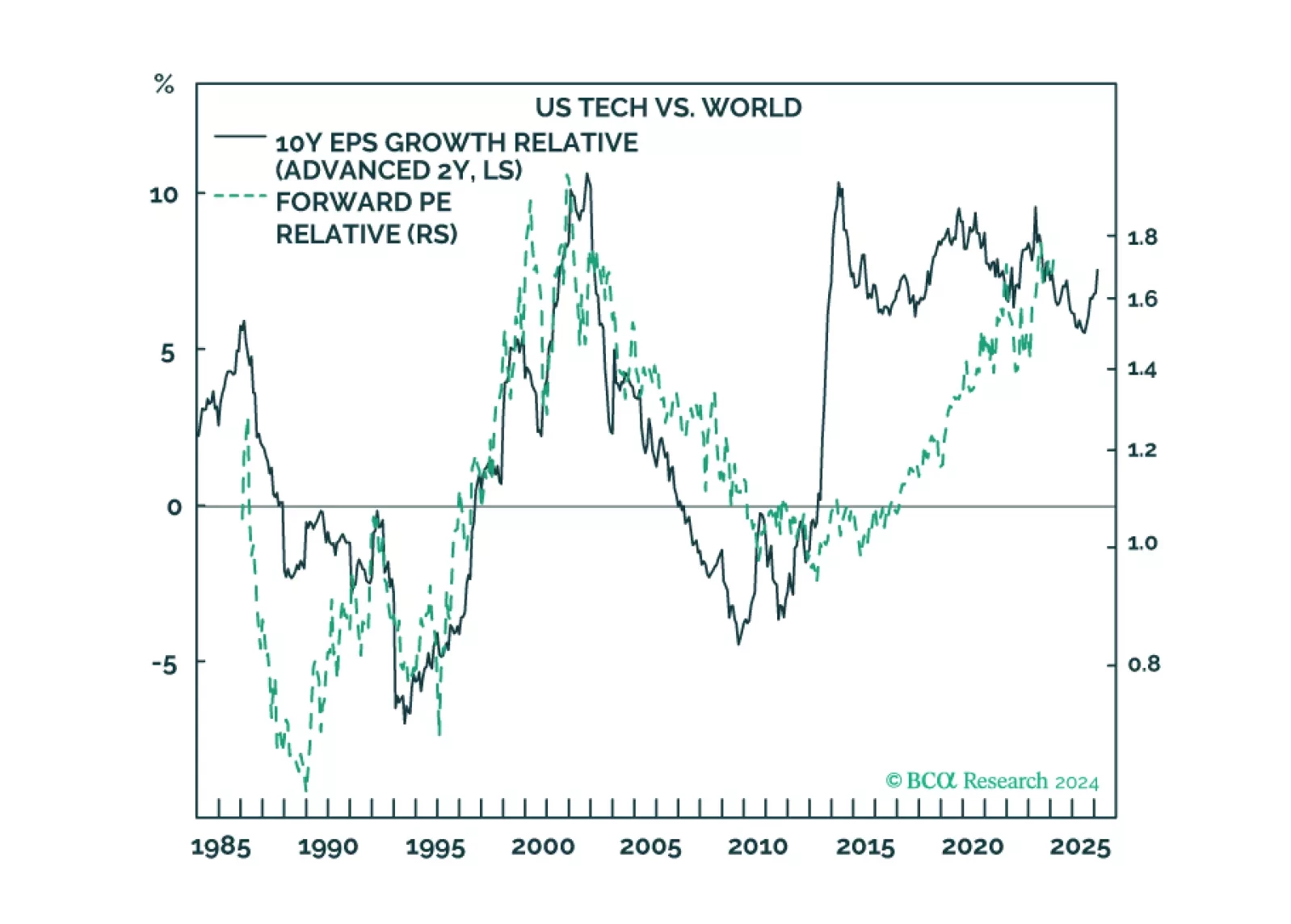

The US stock market’s record 50 percent valuation premium versus the non-US stock market is pricing generative AI to do through the next decade what the Web 2.0 network effect did through the last decade. But this is a huge ask, as it will be very difficult for the Web 2.0 superstar companies to become generative AI superstar companies, assuming there are indeed any lasting generative AI superstar companies. We go through the main long-term investment implications.

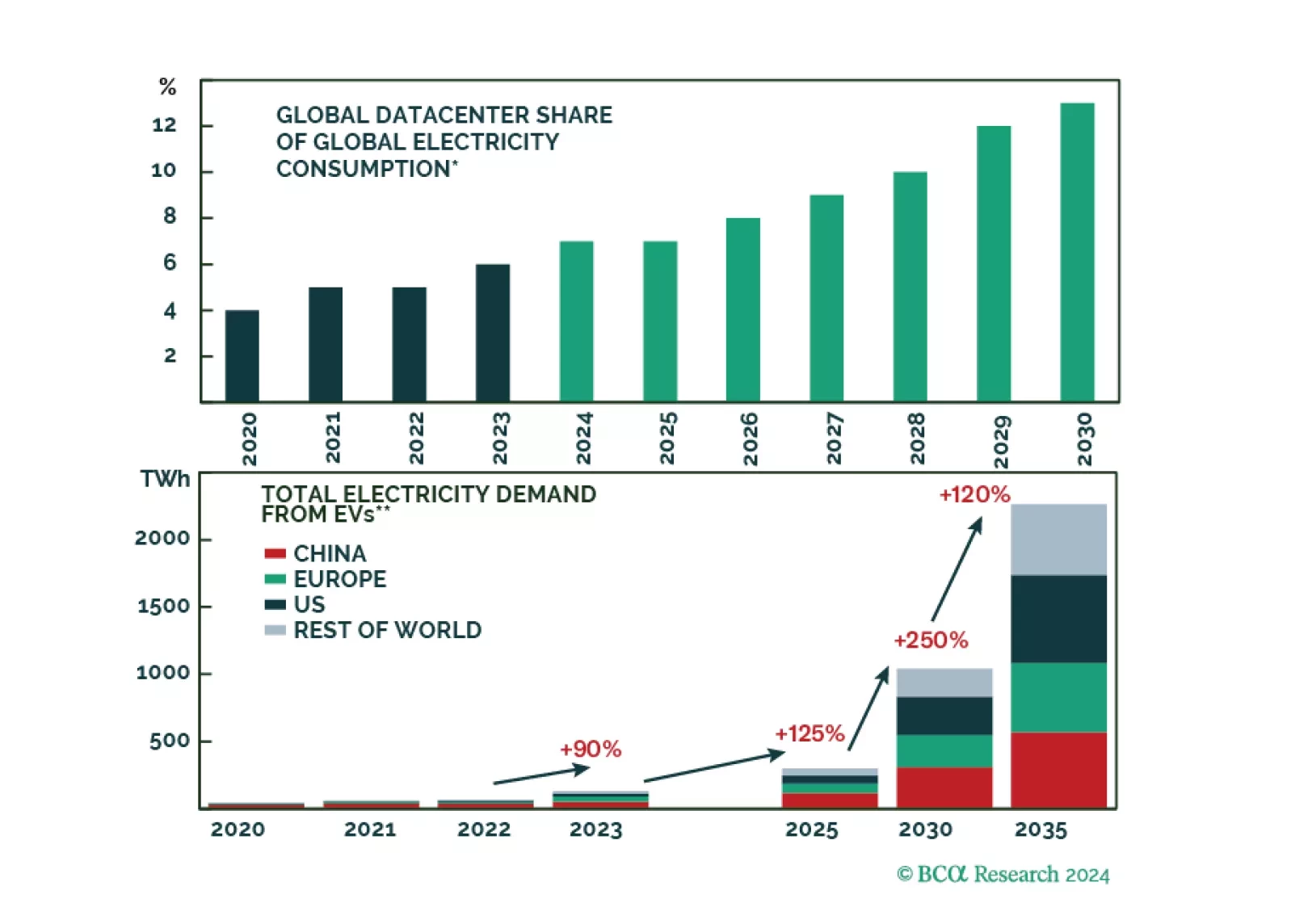

AI, EVs, and reshoring will lead to a massive surge in demand for electricity. Carbon-free, cheap, baseload nuclear energy stands to greatly benefit from these megatrends going forward.

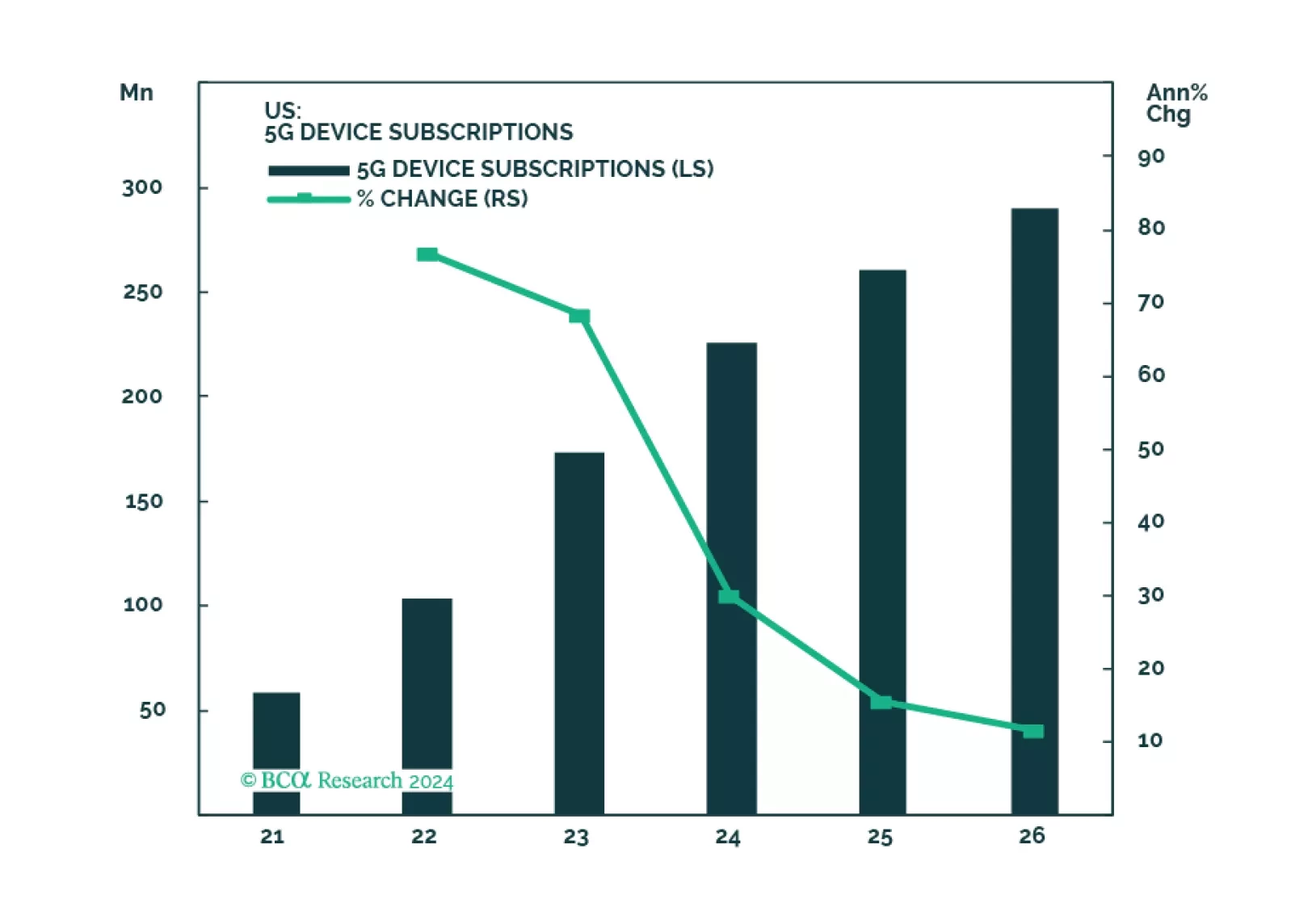

The Telecoms industry is highly concentrated, and carriers compete on price and quality of service in a slow growing market. Demand for capex is relentless. The roll out of 5G has disappointed. Recently, capex outlays have slowed, and operating cash flow has rebounded. Further, Telecoms is a quintessential defensive industry that will outperform during a market pullback.

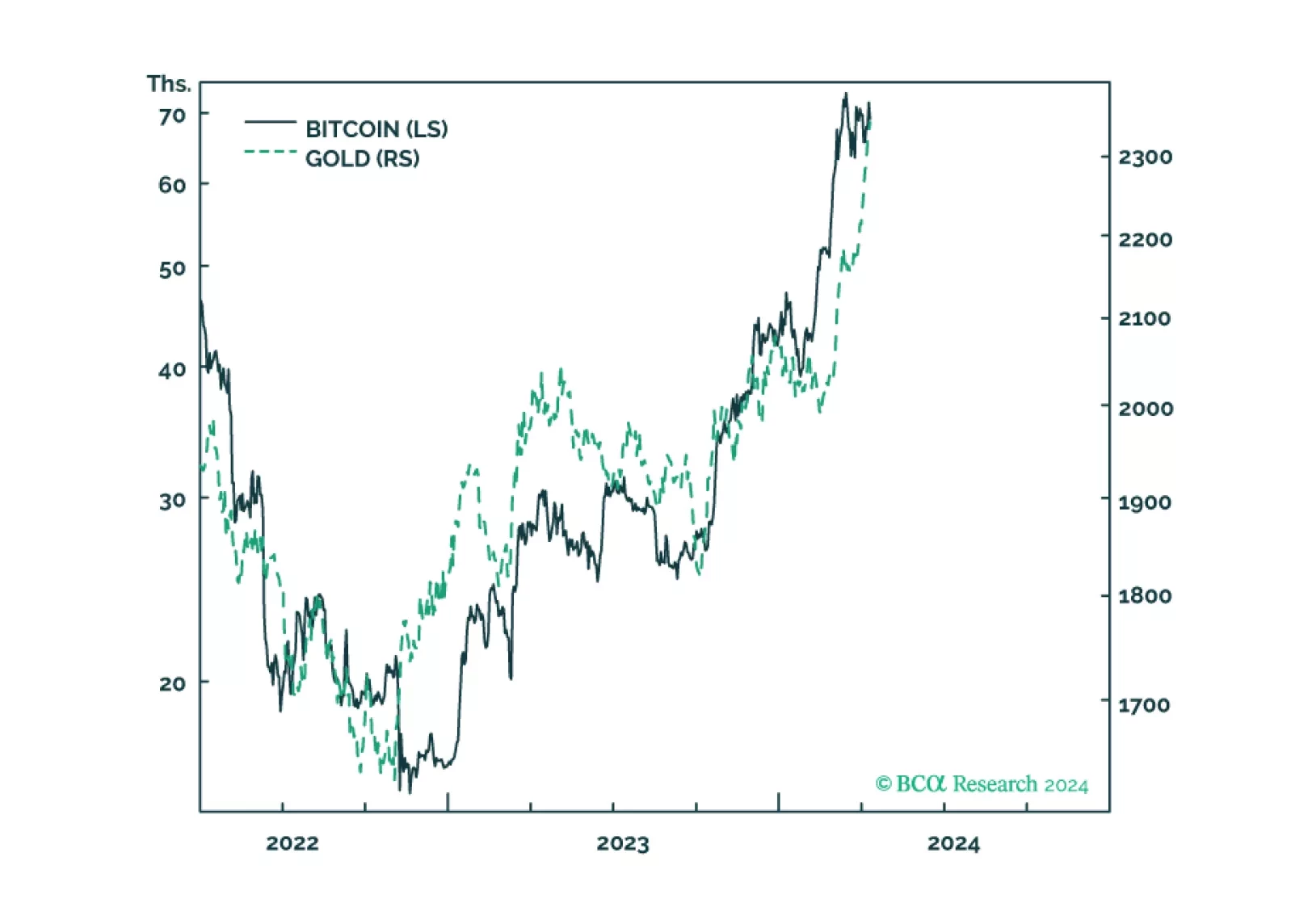

Gold and bitcoin are conceptually joined at the hip because the value of both comes from their ‘non-confiscatability’ by inflation, by bank failure, and in the case of bitcoin, by state expropriation. The sharp recent rallies in both gold and bitcoin reflect that the market has suddenly upped the value of non-confiscatability, and a plausible explanation is that recent US inflation data show that the journey to sustained 2 percent inflation has stalled, raising the risk that the Fed might balk at finishing the journey. Plus: JPM, CL, and USD/CHF are tactical reversal candidates.

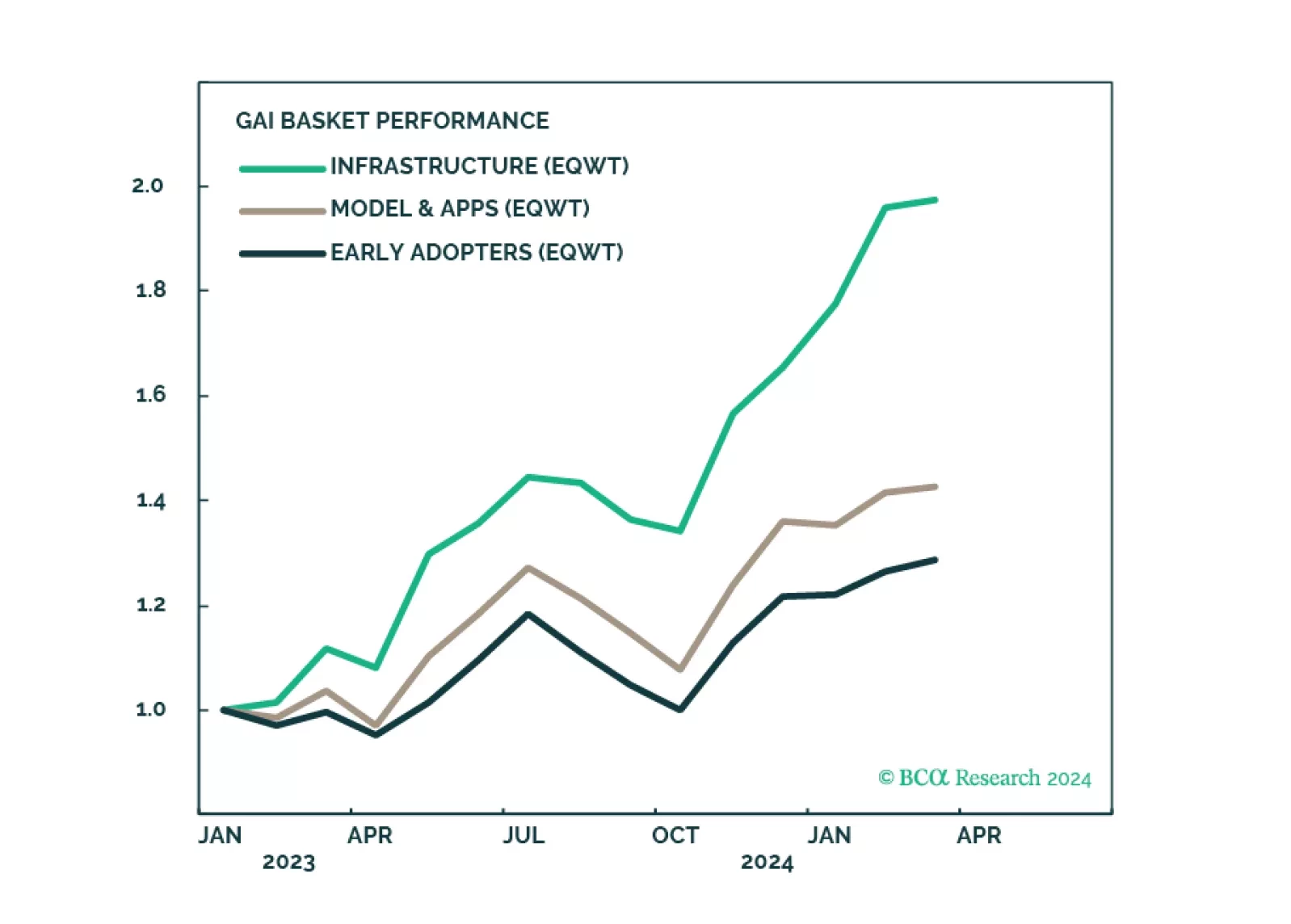

GAI is a powerful force that will revolutionize the global economy and we are sold on this long-term investment theme. To partake in the upward momentum, we recommend a nuanced approach. The GAI infrastructure cohort is now overbought - there should be a better entry point. The models and applications companies and early adopters are less of a crowded trade and offer more opportunities.

GAI technology has made tremendous gains over the past year. It has advanced from being a mere “curiosity” to becoming an everyday helper. While the promise of GAI is enormous, its effects are still limited: Companies are still struggling with monetization while productivity improvement is still at least a year away. In terms of evolution, the focus is shifting away from “picks and shovels” infrastructure companies toward model and application developers.

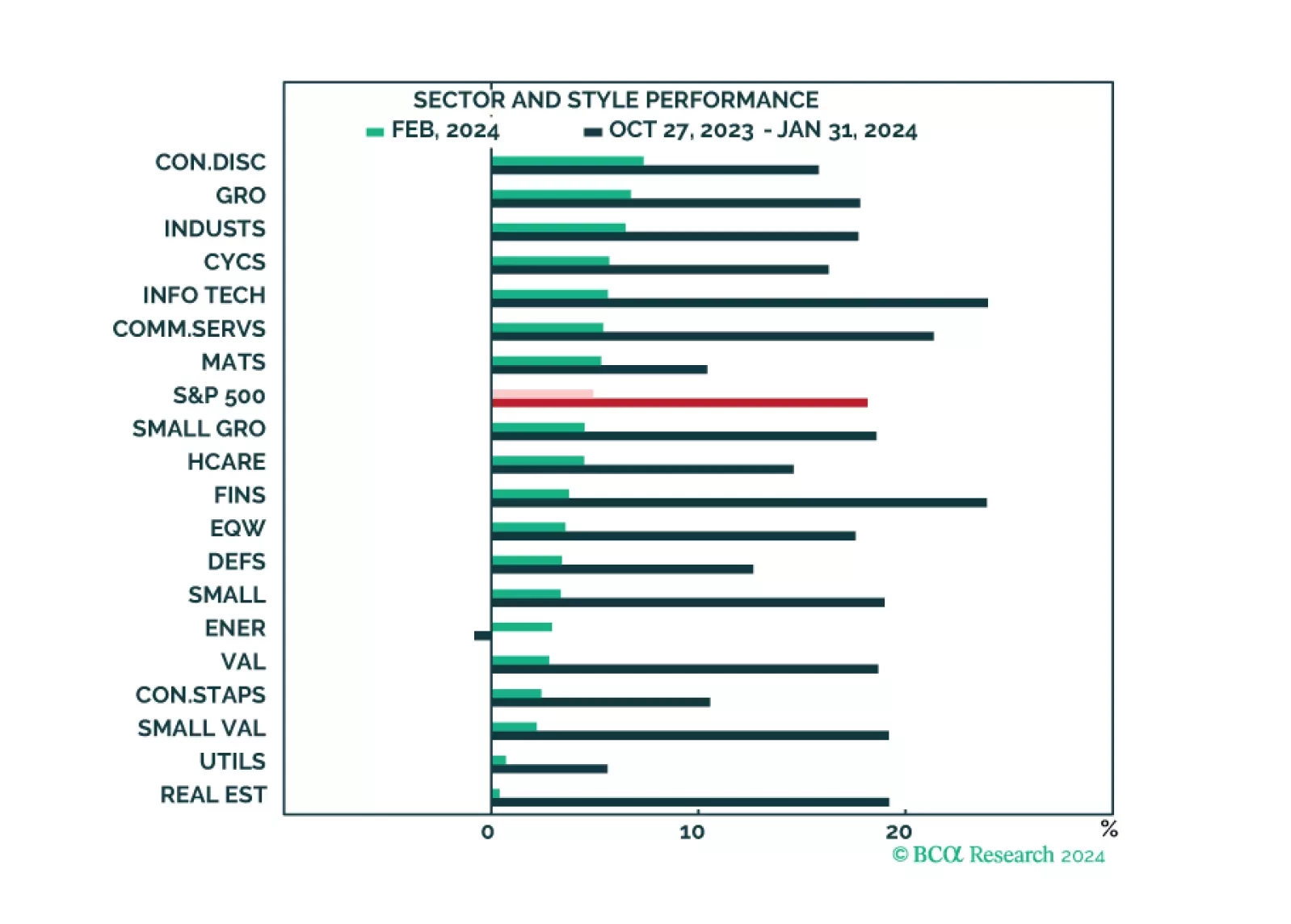

The market narrative continues to be dominated by the Magnificent Six, which drove both market performance and strong Q4 earnings results. While all sectors and styles have recently turned green, the rally is still mostly narrow. Earnings growth appears to be strong, but outside of the Magnificent Six, many companies are struggling. The market appears expensive and overbought, but that is mostly down to the high valuations and the popularity of the Magnificent Six.

Our Valentine’s Day report is about two love stories: the infatuation with US tech and China’s infatuation with housing. We describe how these love stories will end, and why Europe could be the winner.

The soft landing and rate cuts narrative is being priced out, and the S&P 500 is overvalued and getting overbought. The Magnificent Seven are about to get a new moniker on the back of performance dispersion. However, without the cohort, S&P 500 earnings would have been even deeper in the red.