Tariffs

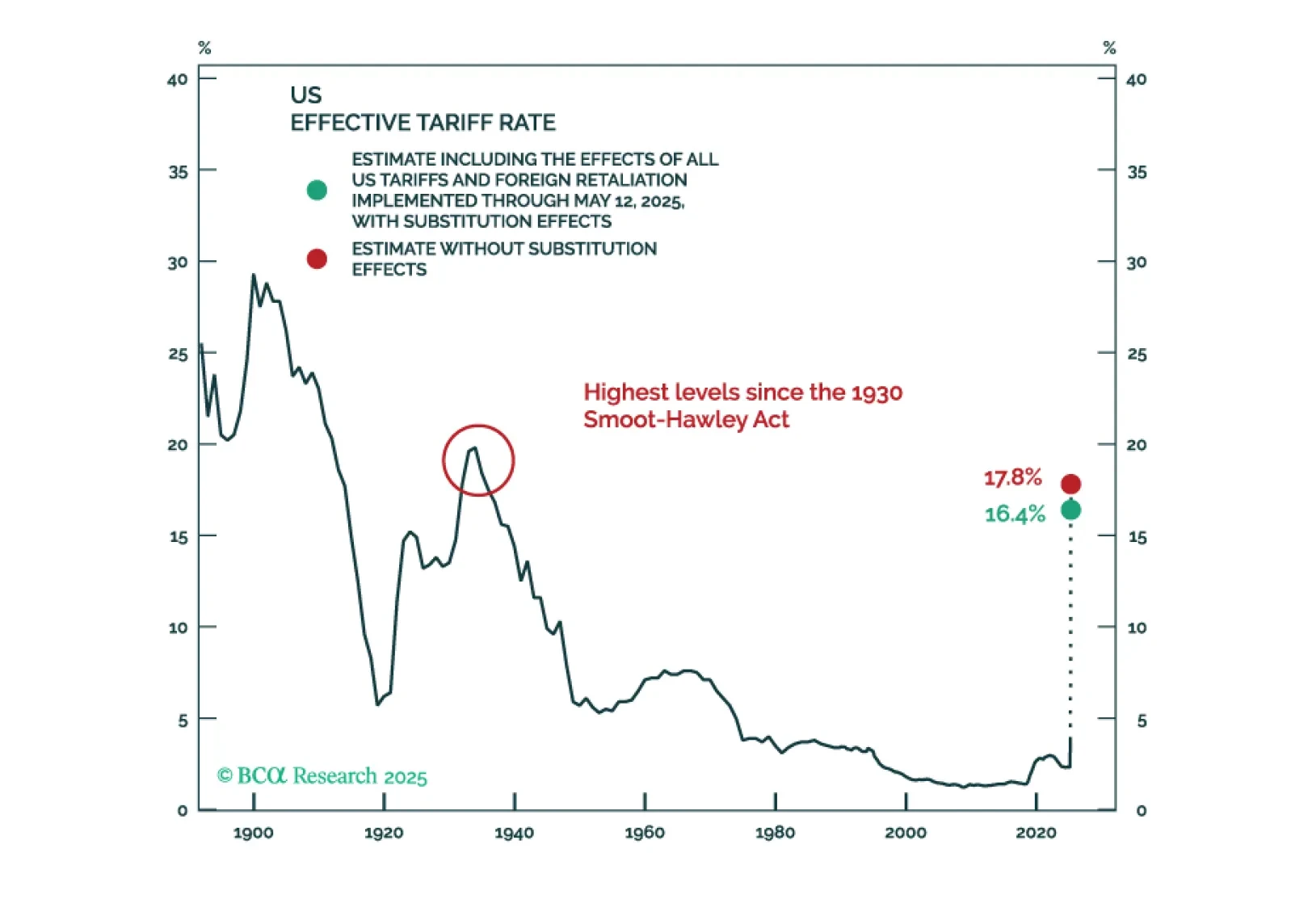

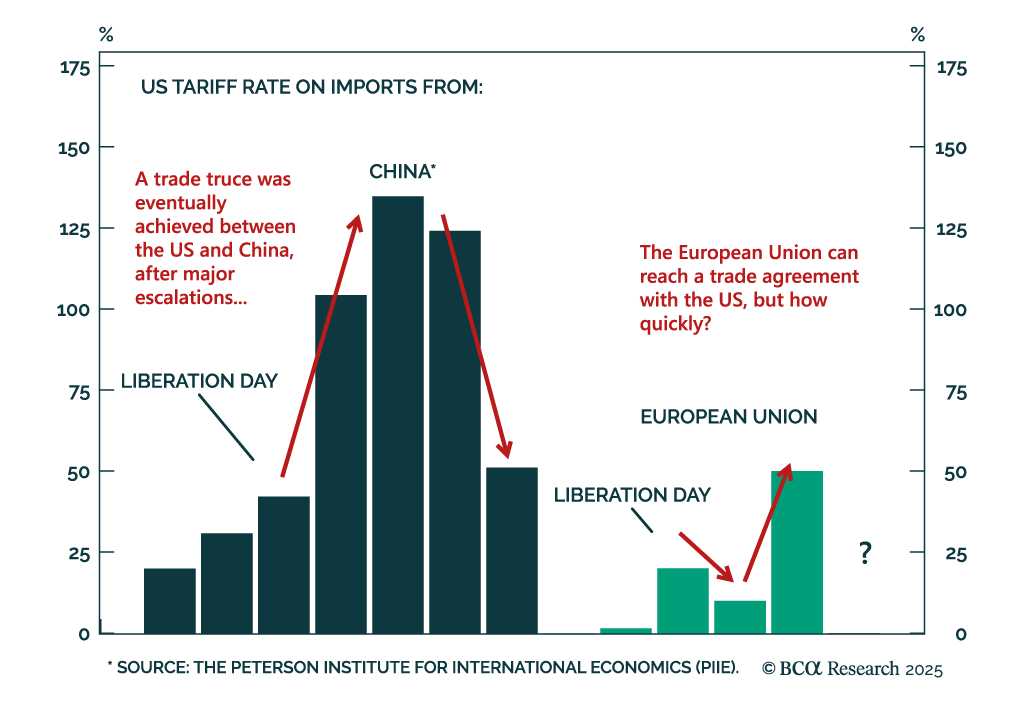

In Section I, Doug warns that US trade policy may produce a considerably worse outcome than investors currently expect. The administration’s apparent 10% tariff baseline is likely to be negative for the US economy and particularly the small business sector. Investors should remain defensively positioned for now, although judicial constraints on the administration’s ability to wage a trade war, if confirmed, would sharply reduce our estimated recession probability. In Section II, Jonathan discusses the arguments in favor and against the view that US inflation will be structurally elevated over the longer term. Our base case view remains that US inflation will not be significantly above 2%, but this view may change if US tariffs are put in place permanently and the US avoids a recession.

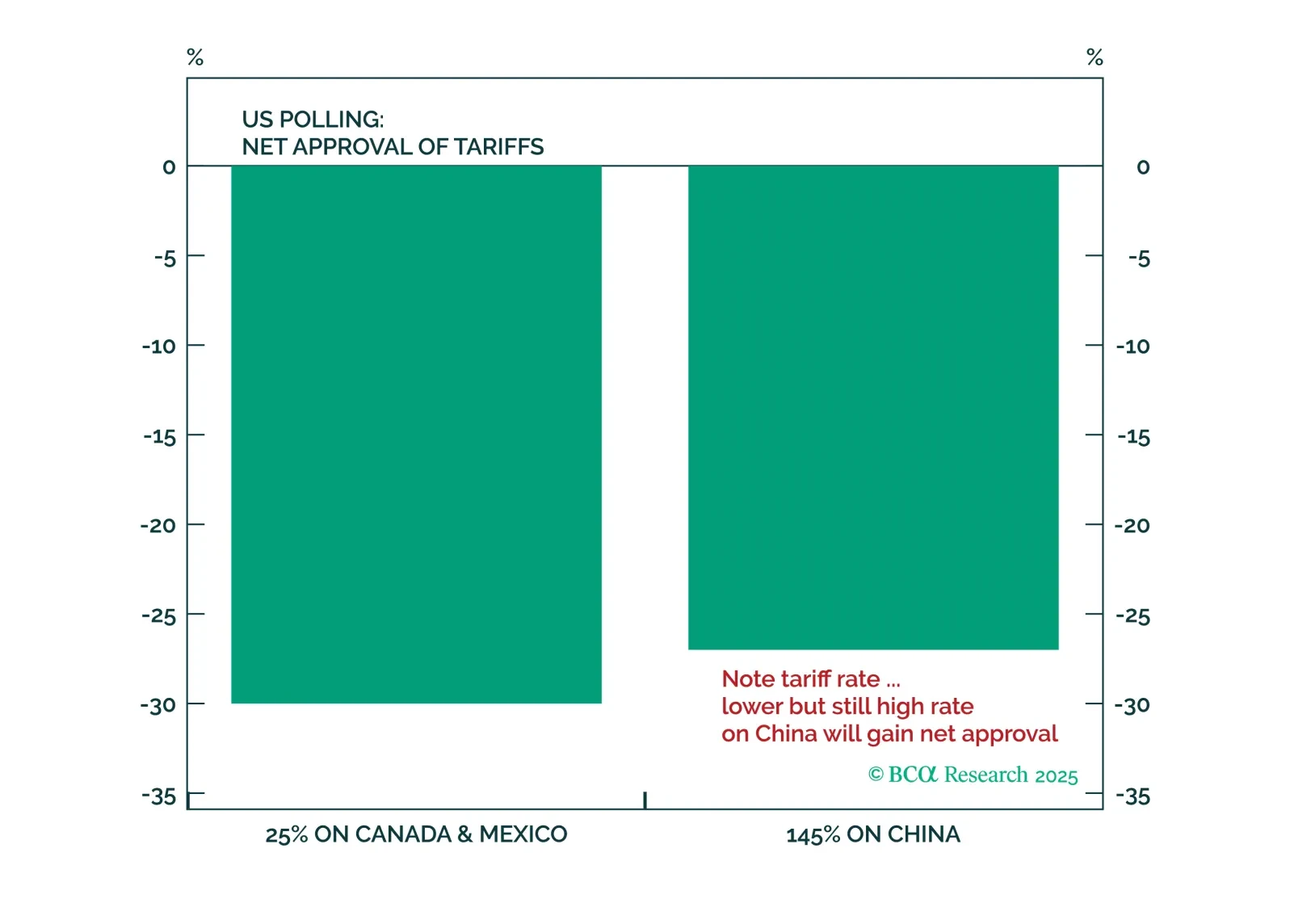

President Trump faces new restrictions on his trade powers coming from the US judicial branch, but they will not prevent him from continuing to restrict trade and investment with China. Rather, they will establish some curbs against entirely arbitrary executive tariffs, especially when wielded against US allies and partners.

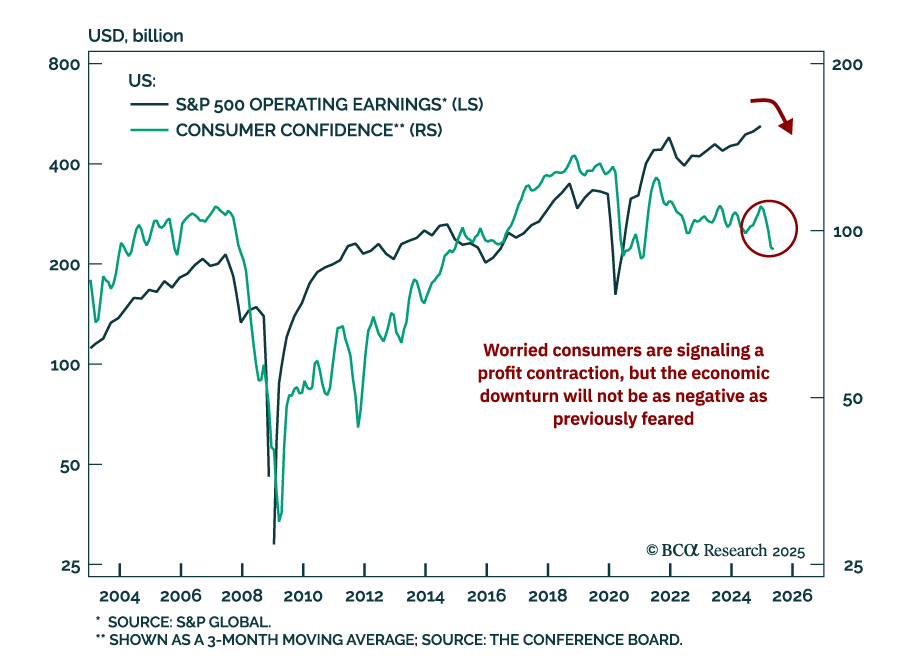

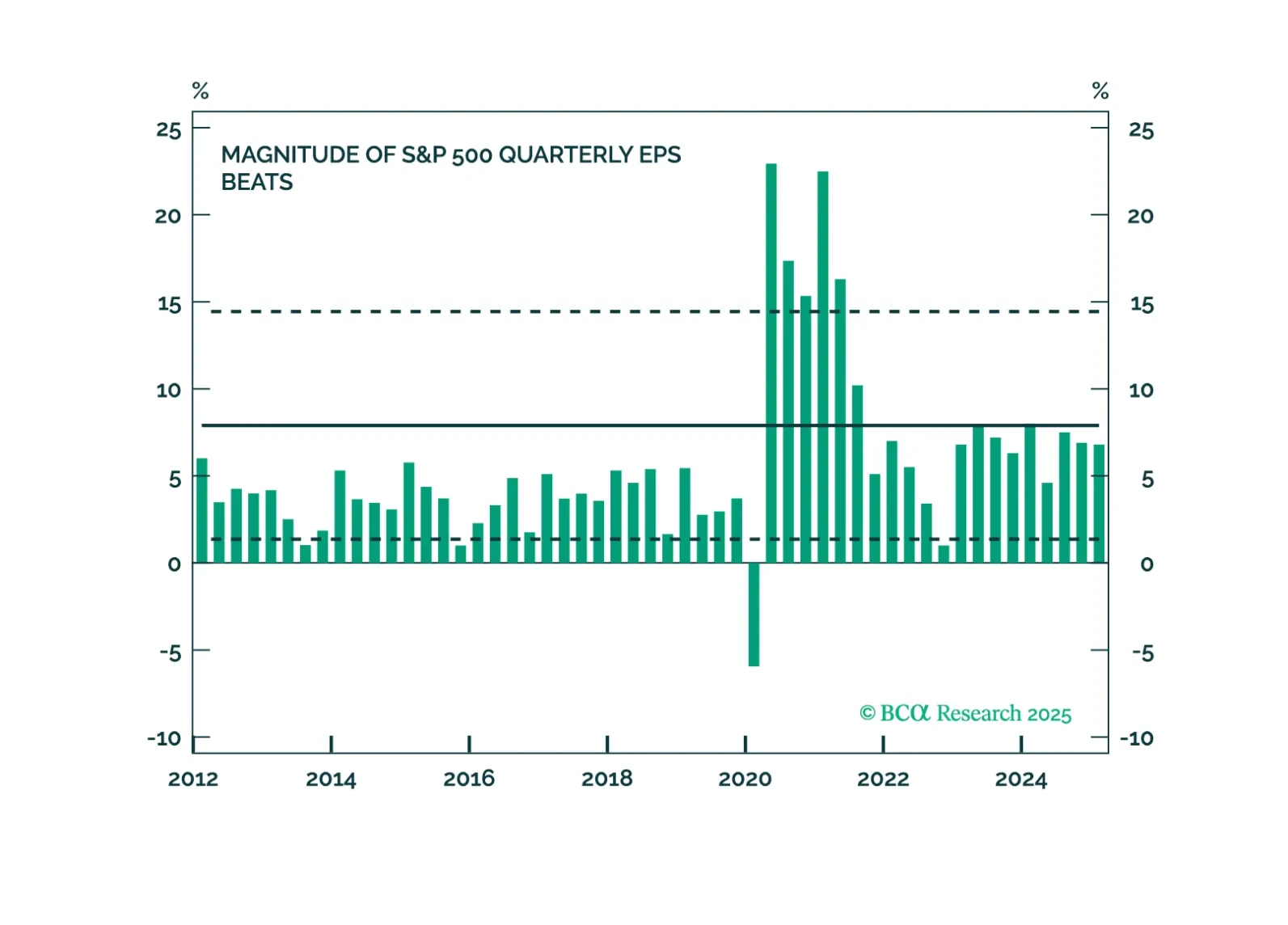

In this report, we take stock of the Q1 2025 earnings season. Corporate commentary and forward guidance provide valuable insights into the state of the economy, tariff mitigation strategies, and consumer spending.

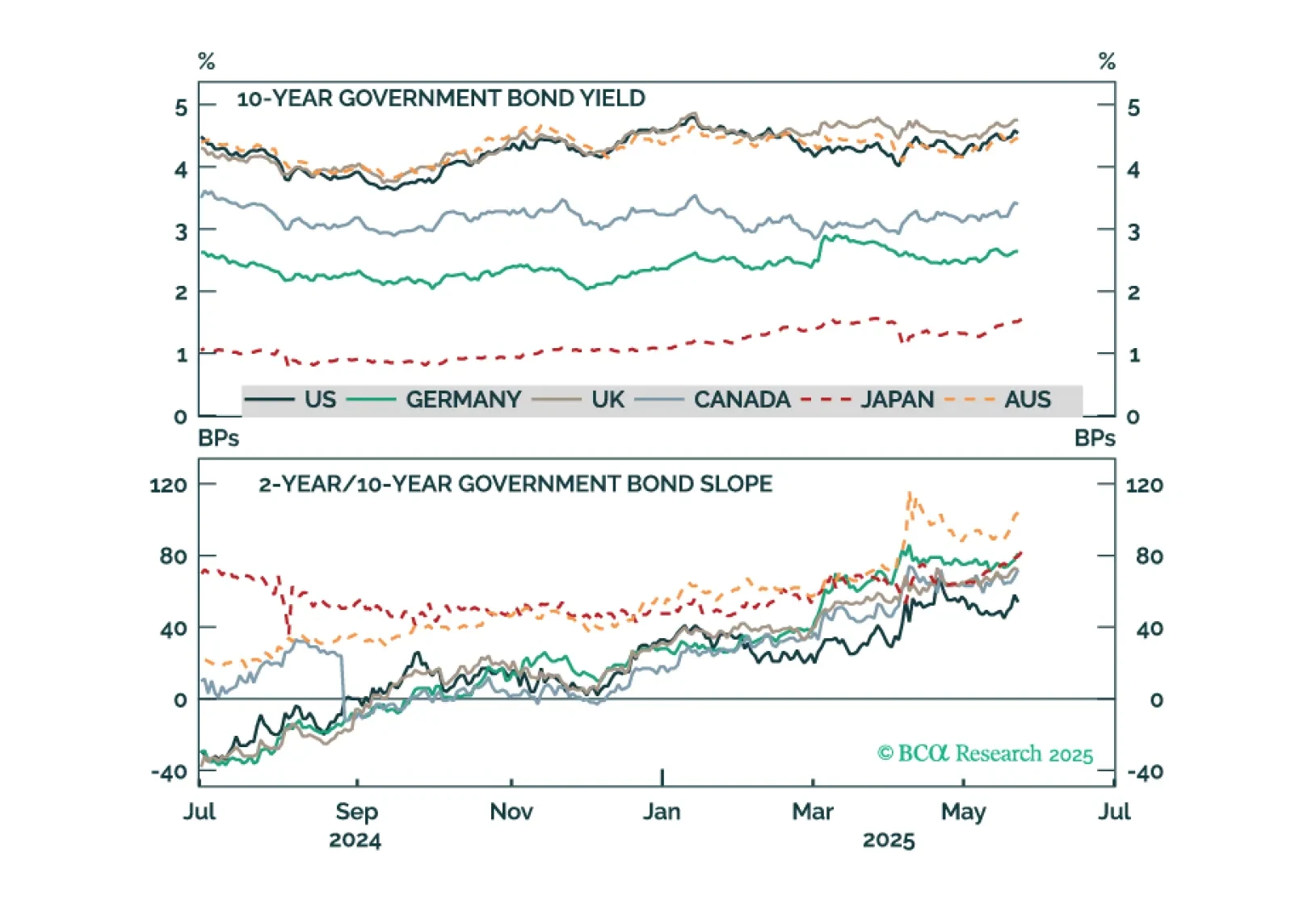

We perform a decomposition of yields moves across six major developed government bond markets to get to the bottom of what’s been driving the global bond selloff of the past eight months.

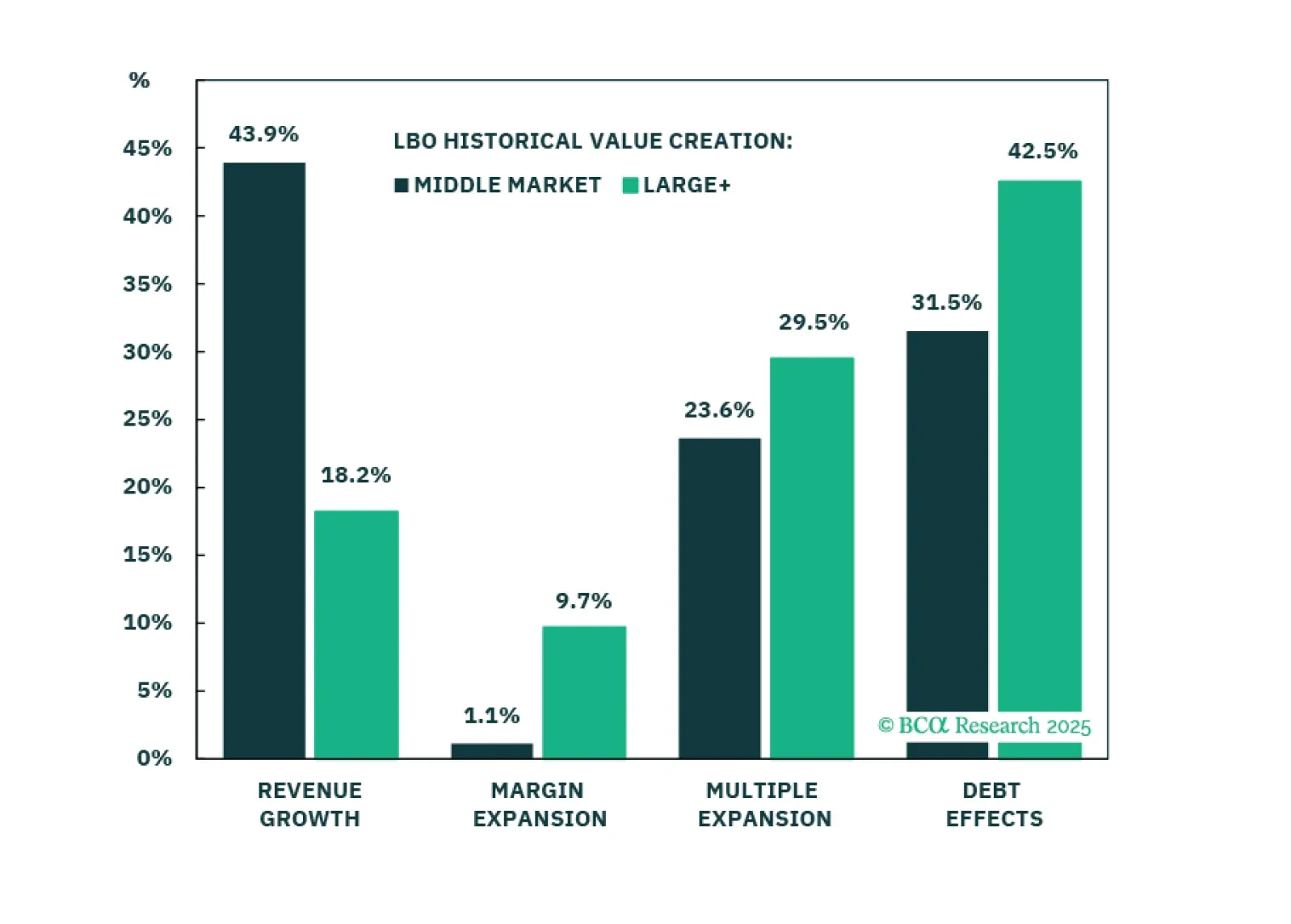

Return expectations have changed for Buyouts, but not equally for Large+ and Middle Market deals. While tariffs are dramatically reducing investor expectations, our return expectations are modestly increasing—with Large+ leading. In Part 2, we will tackle Private Credit.

Risk assets rallied hard following the Great Geneva De-escalation, but we are not enamored of risk assets’ risk-reward profile. Forward-looking survey data remain awful on balance and we continue to recommend a defensive asset allocation profile.

Tariff front-running behavior makes the April hard economic data difficult to interpret, but we take the strong reading from Food Services spending as a signal that the US consumer has not yet buckled.