Tariffs

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

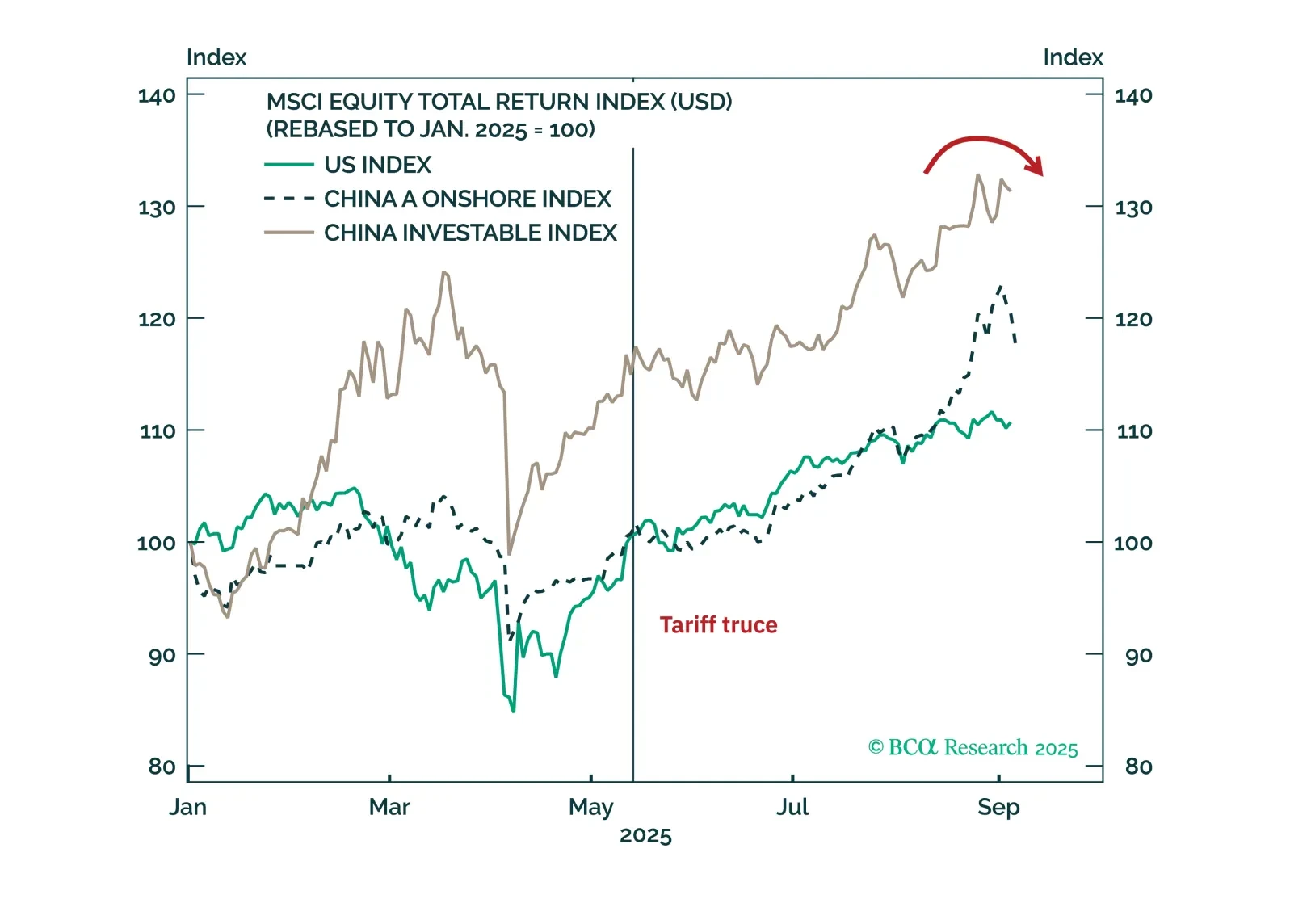

Investors will be disappointed if they buy into the China rally and then Russia escalates the war in Ukraine.

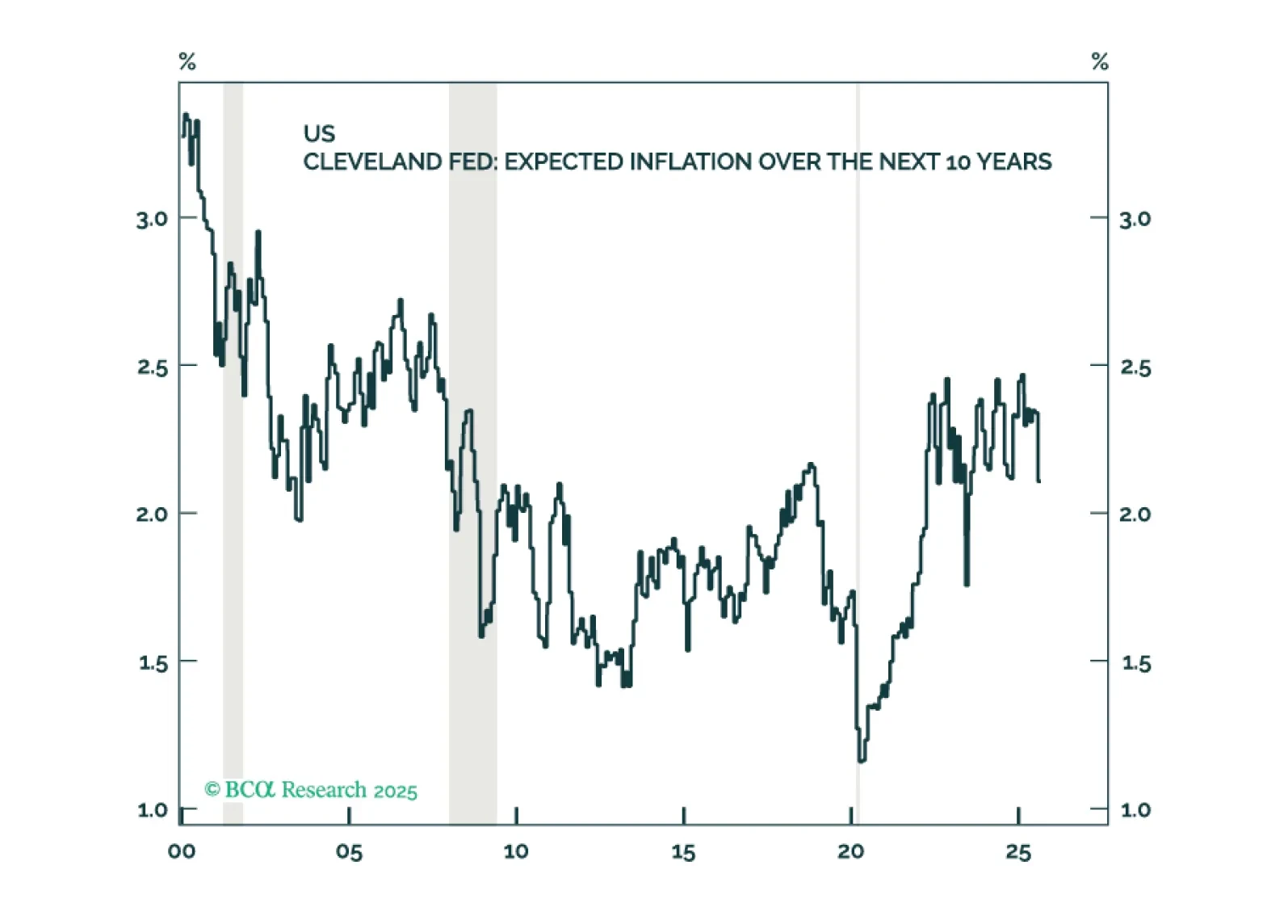

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.

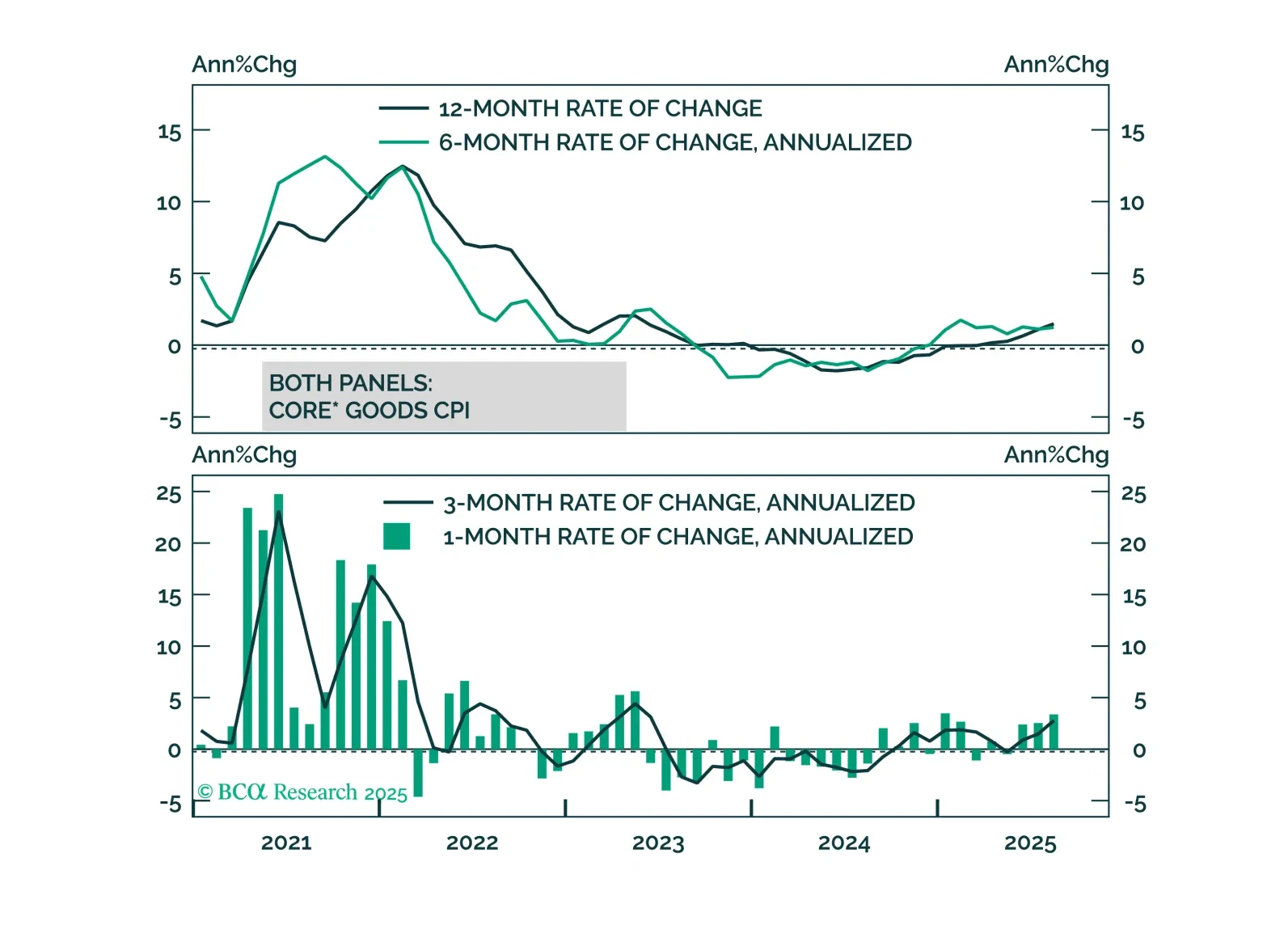

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.

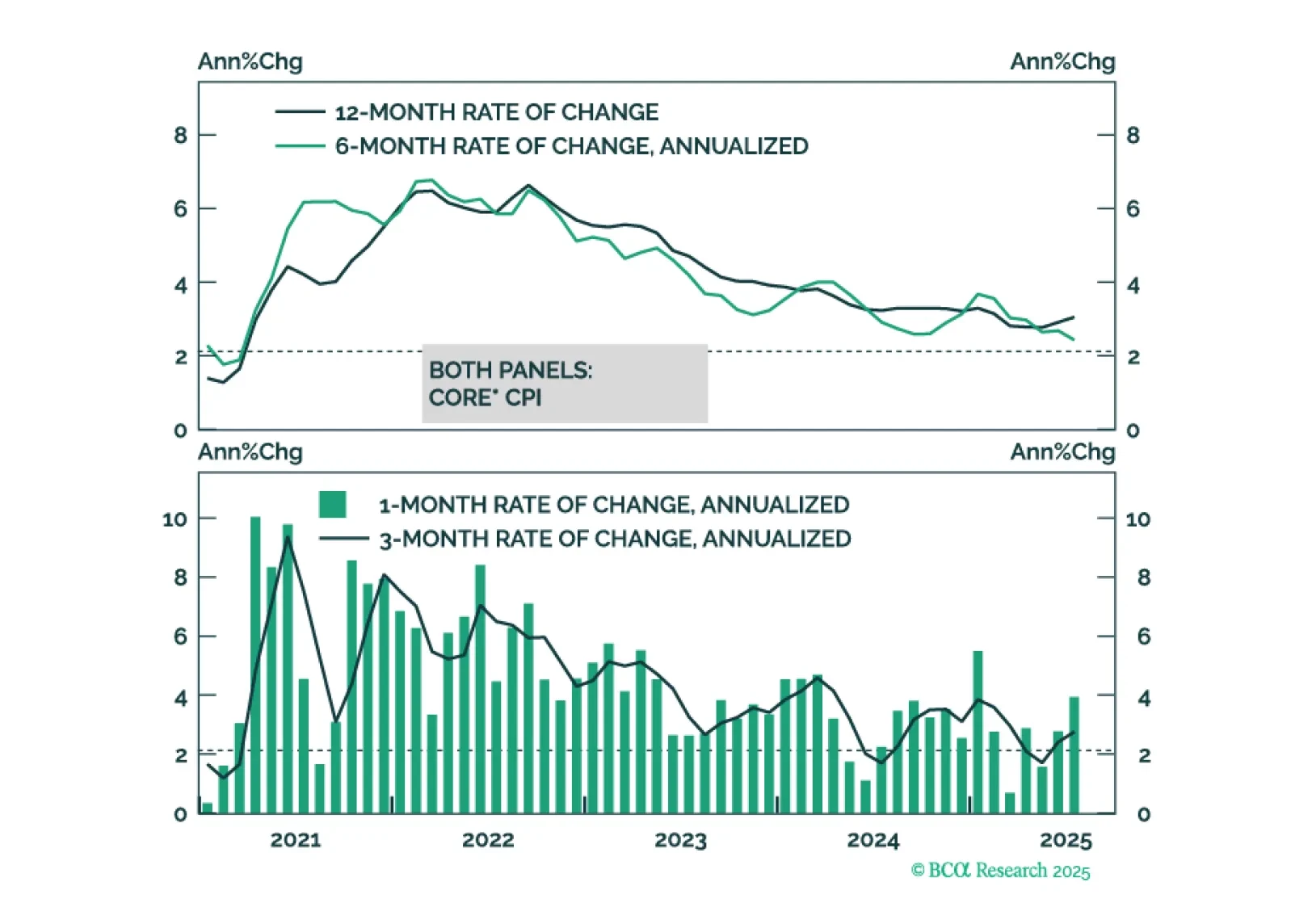

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

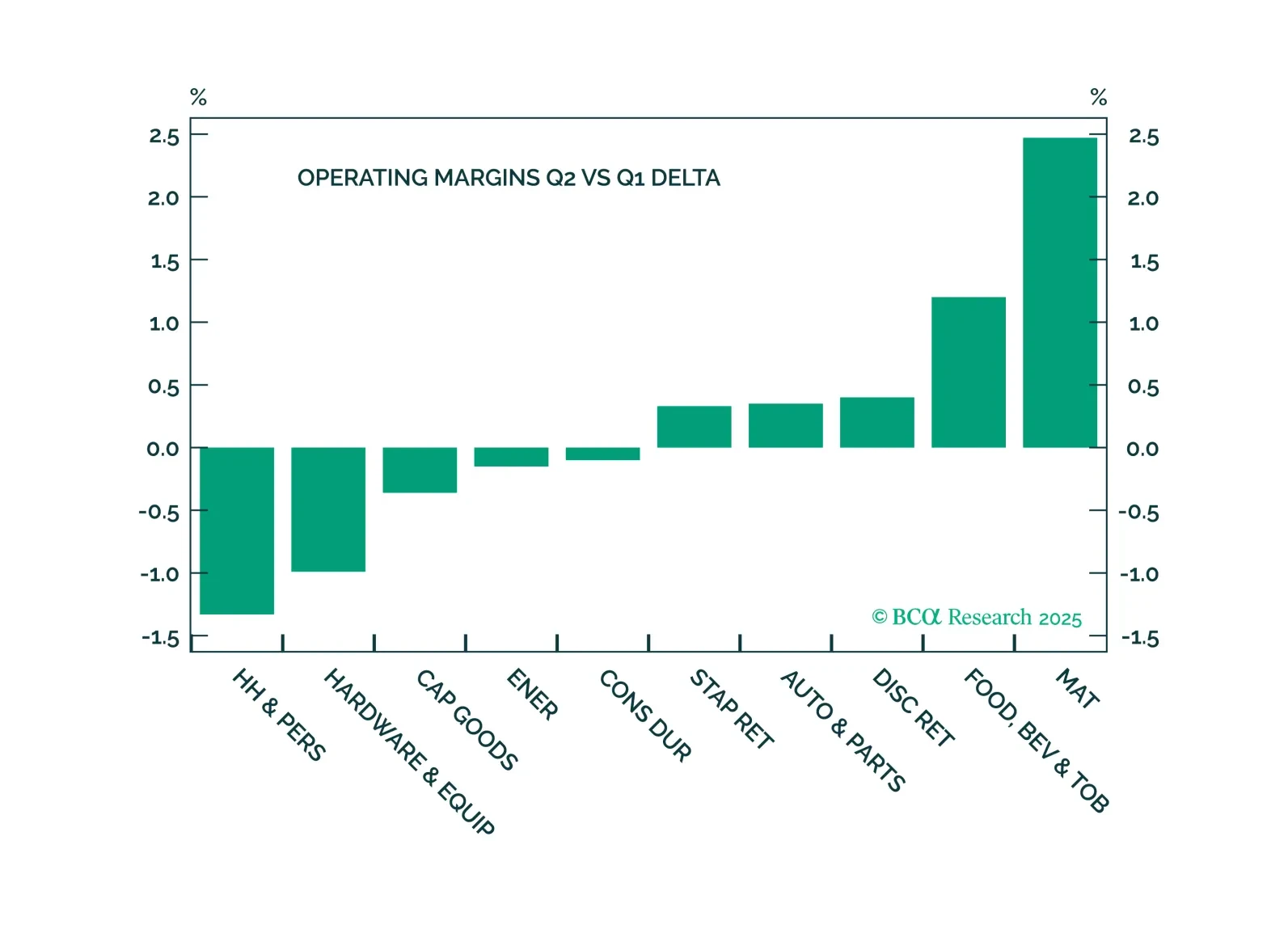

The Q2 earnings season delivered solid earnings and sales growth and resilient margins, reassuring investors that corporate America remains in good health and is capable of navigating economic uncertainty while mitigating the impact of new trade levies. The outlook is generally positive, but with one important caveat: The full effect of tariffs has yet to materialize.