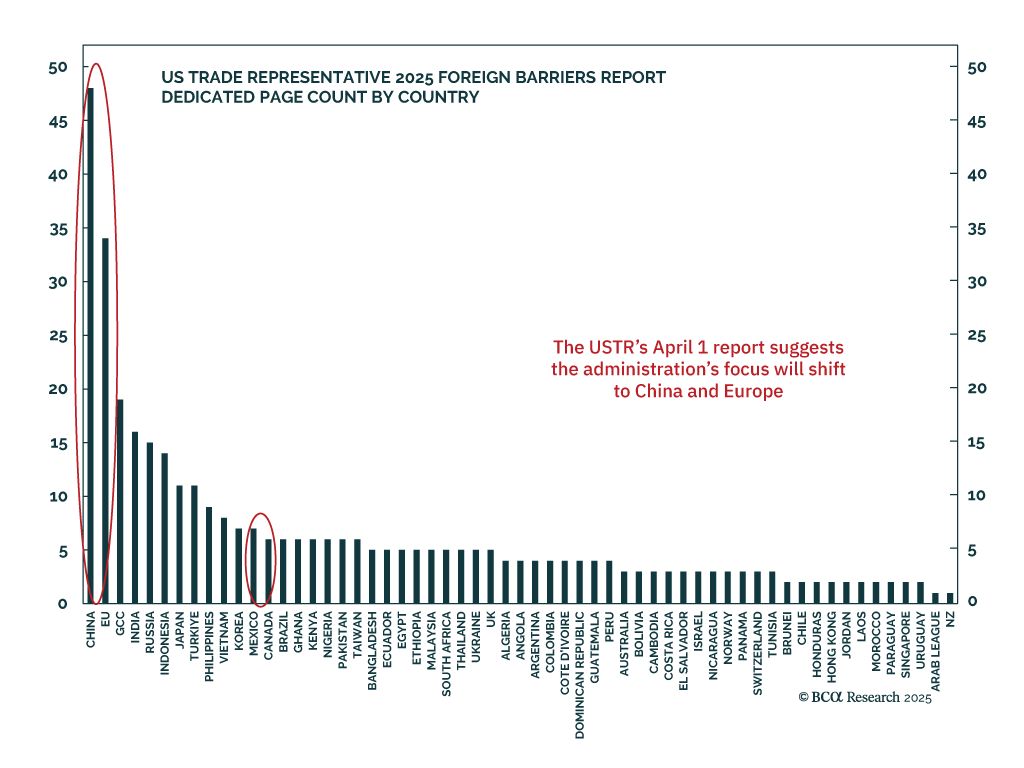

Tariffs

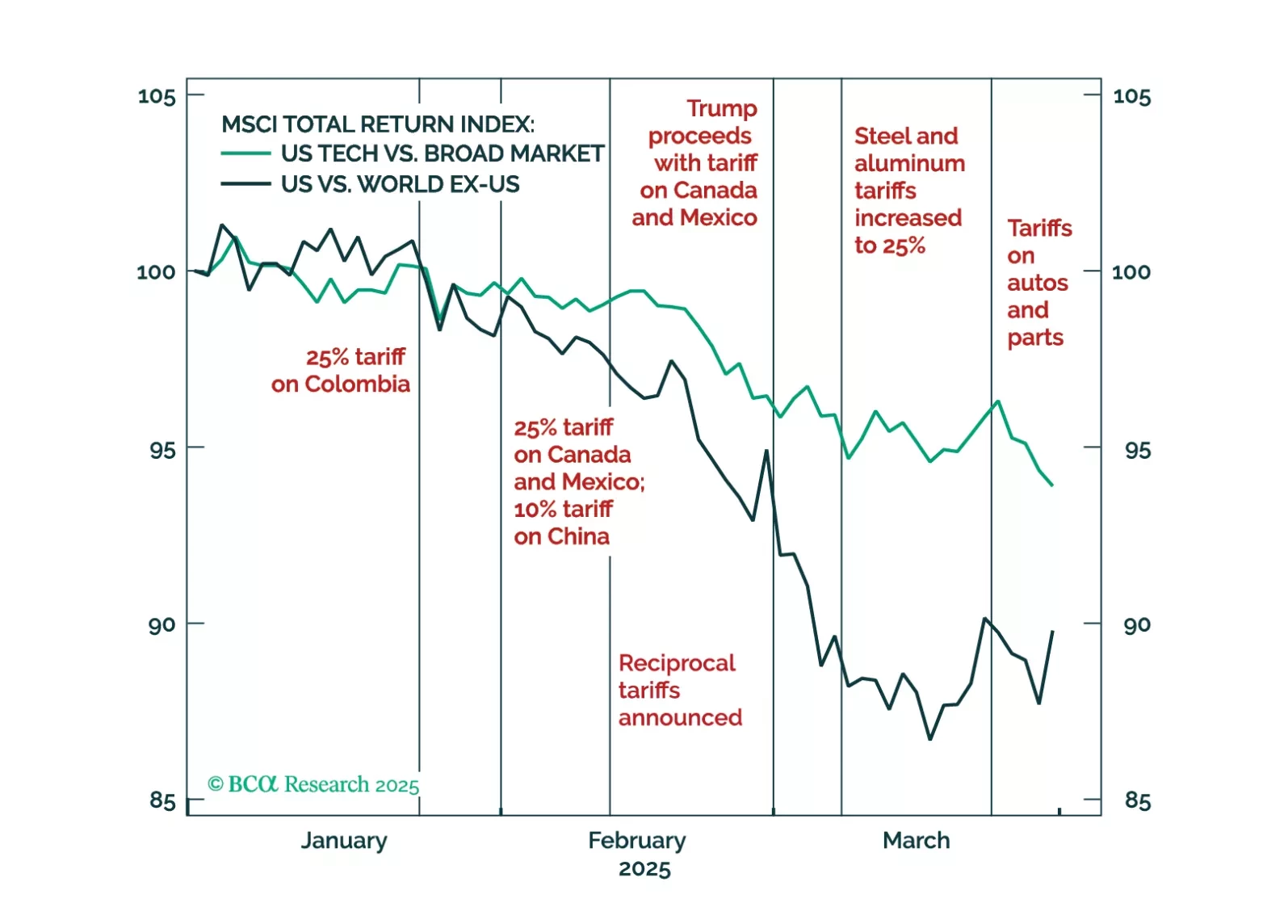

The trade war is on everyone’s mind with America’s “Liberation Day” upon us! However, the reality under the surface is that the main macro narrative has been a rotation – nay… exodus – out of US assets into RoW. This was not supposed to happen with de-globalization and a MAGA trade policy. US assets – form equities to the USD – were supposed to be the safe haven from “America First” policies by Donald Trump. Meanwhile, the noose of material constraints is tightening around Trump, suggesting that a pivot away from brinkmanship may not be long away from “Liberation Day.”

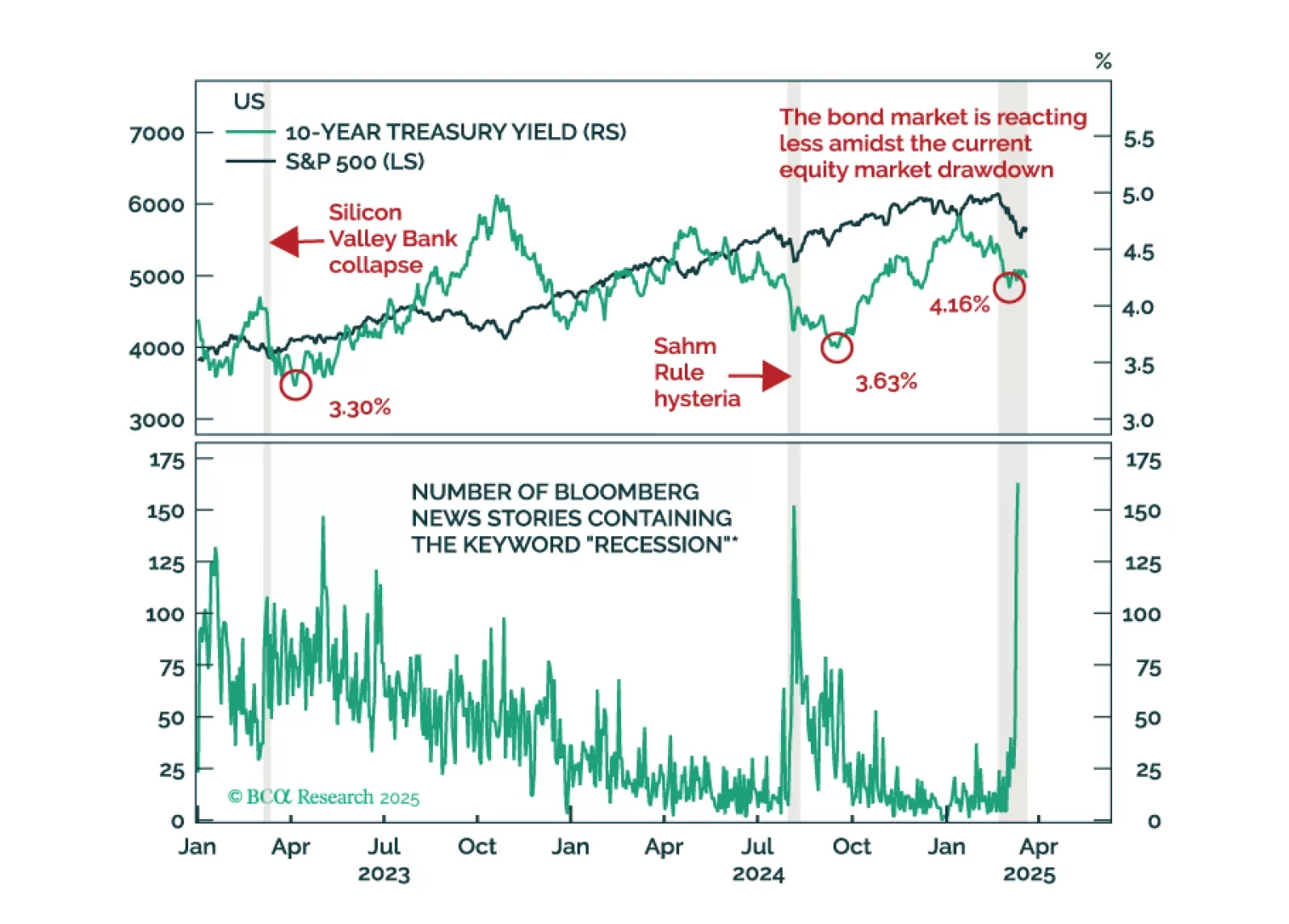

This morning’s weak consumer spending and strong inflation data reinforce our sense that the US economy is heading toward recession.

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

The US economy faces a new investment regime characterized by tighter fiscal and easier monetary policies. The market corrected fast, and a short-lived equity rebound is likely. However, over the long term, US equities face economic headwinds.

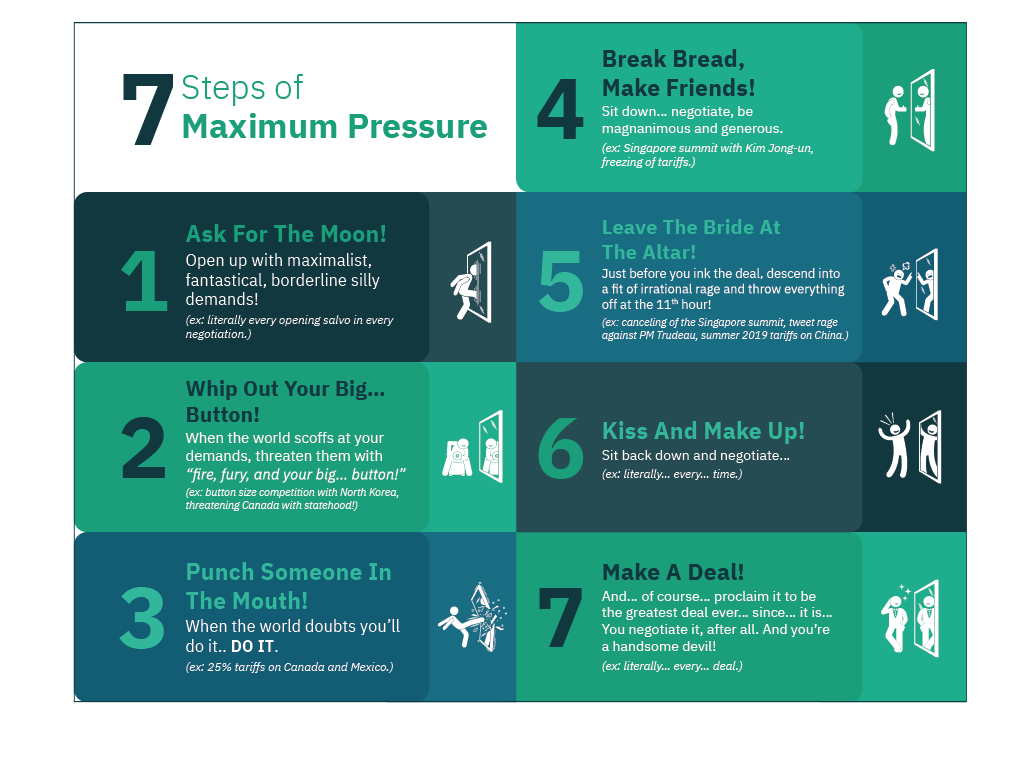

In this Special Report, GeoMacro Strategist Marko Papic argues that the Trump administration is flirting with high risk / low reward. Triggering a recession may be the end goal of the White House, but borrowing costs are not declining as much as they ought to be while President Trump’s political capital is on thin ice. Most recessions are caused by a “murder weapon.” It is rare that this weapon can be holstered. This may be one of those times.

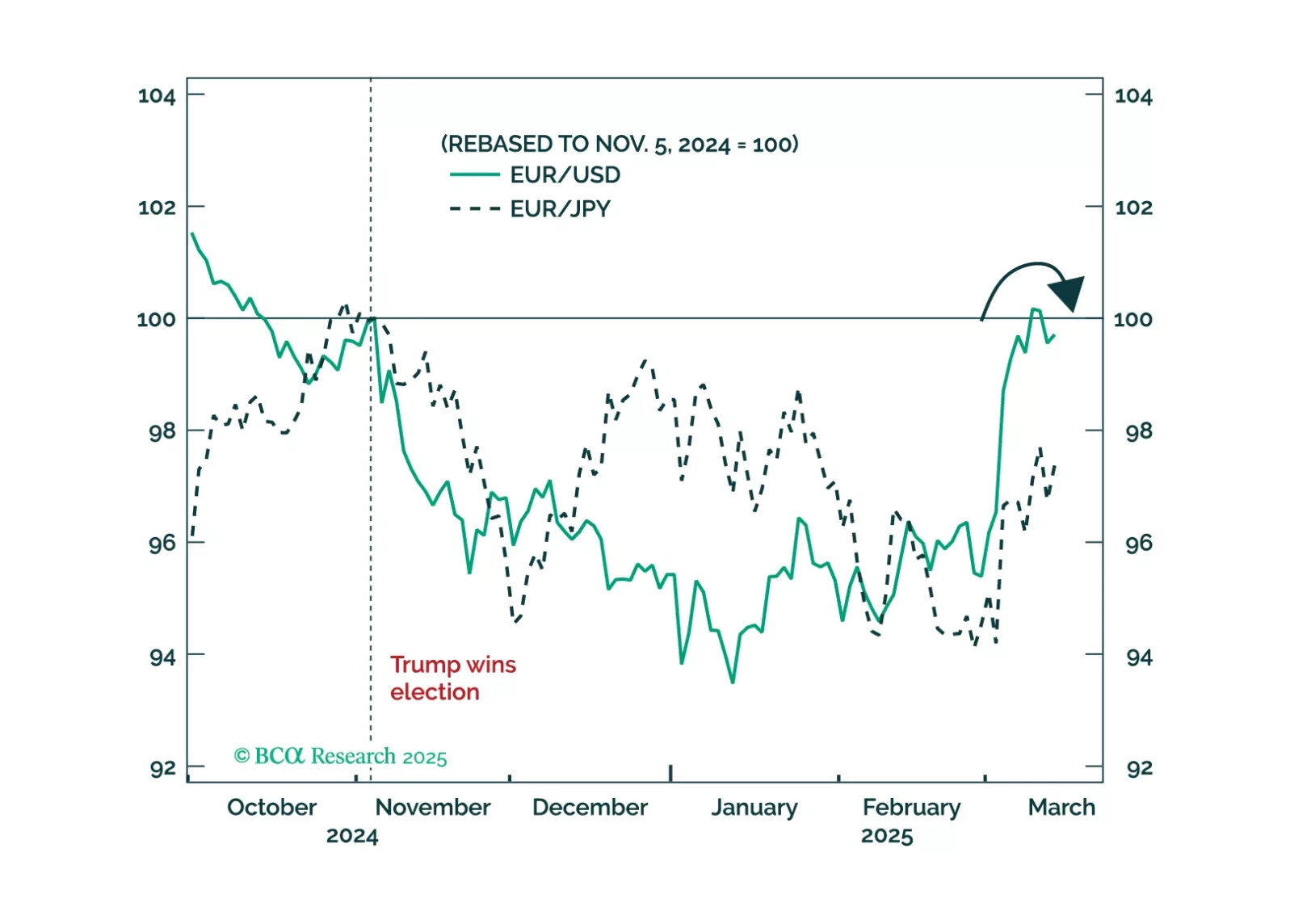

Trump’s foreign policy can be explained by rational US interests, but it requires settling the trade war with allies sooner rather than later. Book gains on EUR-USD for now.

Despite our bearish predisposition towards stocks, we are open-minded to anything that could challenge our thesis. As such, in this report, we review five upside scenarios for equities.