Tariffs

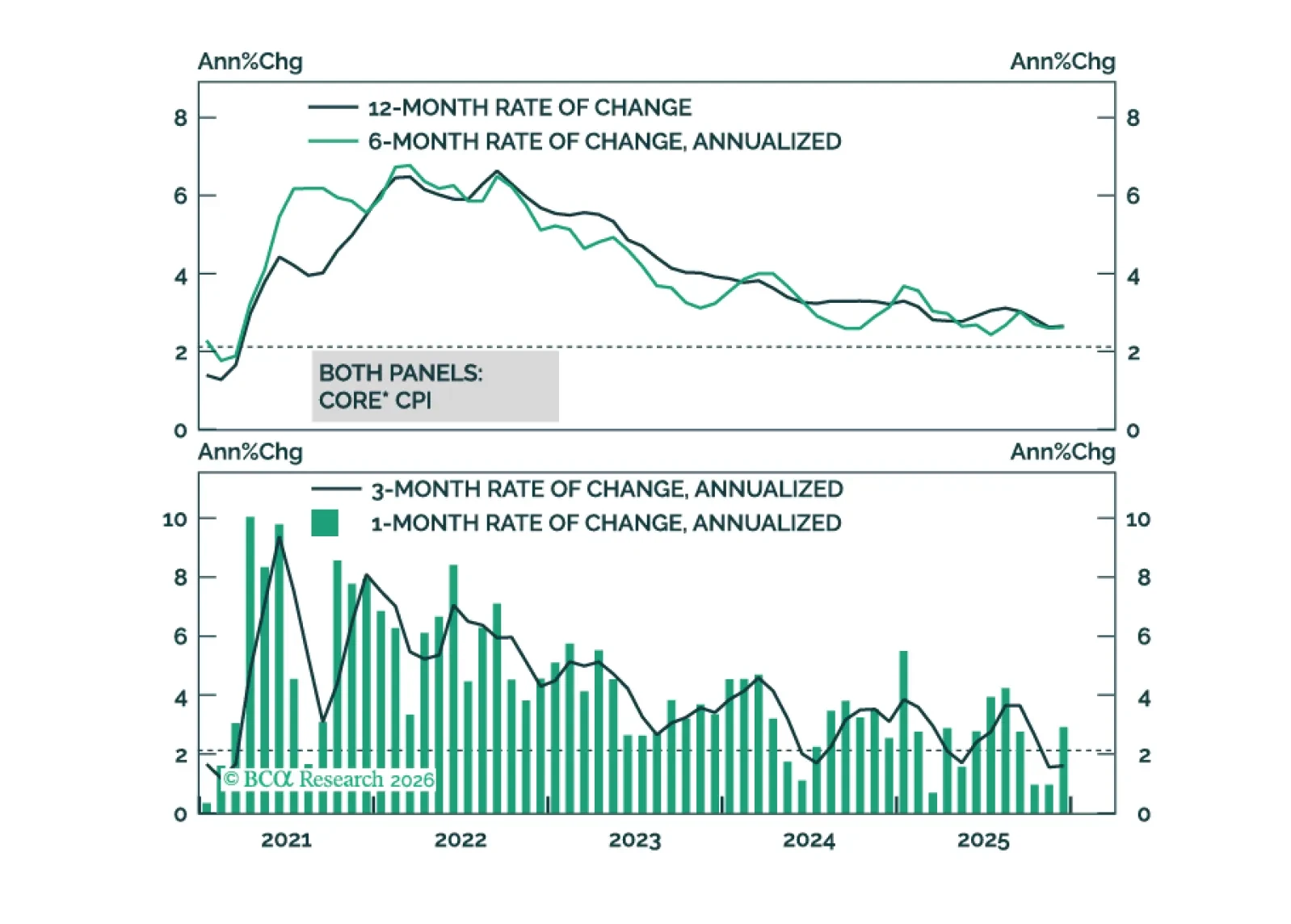

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

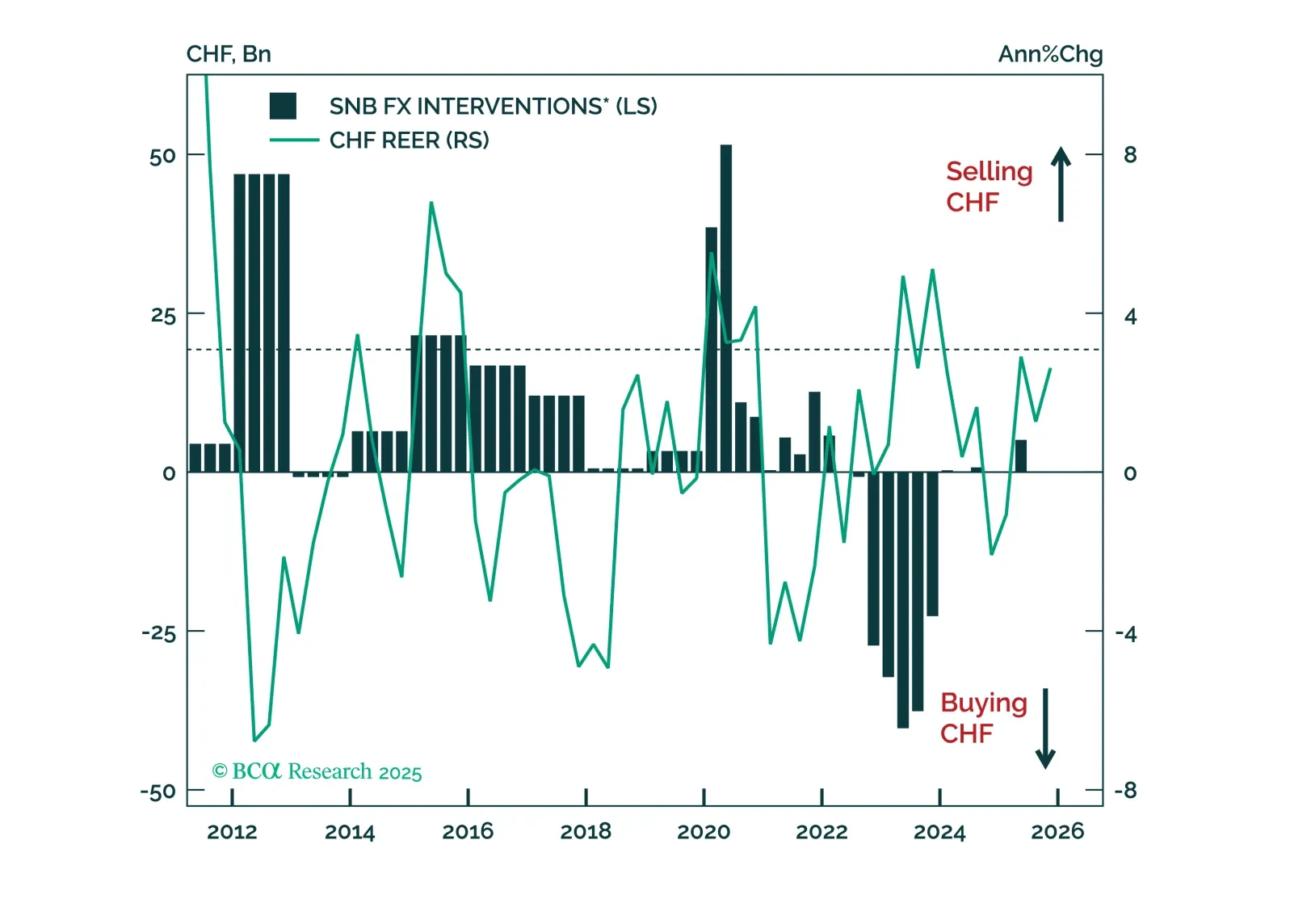

The SNB remains on hold, but the bar for further easing is falling quickly – even as Switzerland secures a breakthrough trade deal with the US. With CHF now pressing against a policy ceiling, the franc looks increasingly attractive as a funding currency.

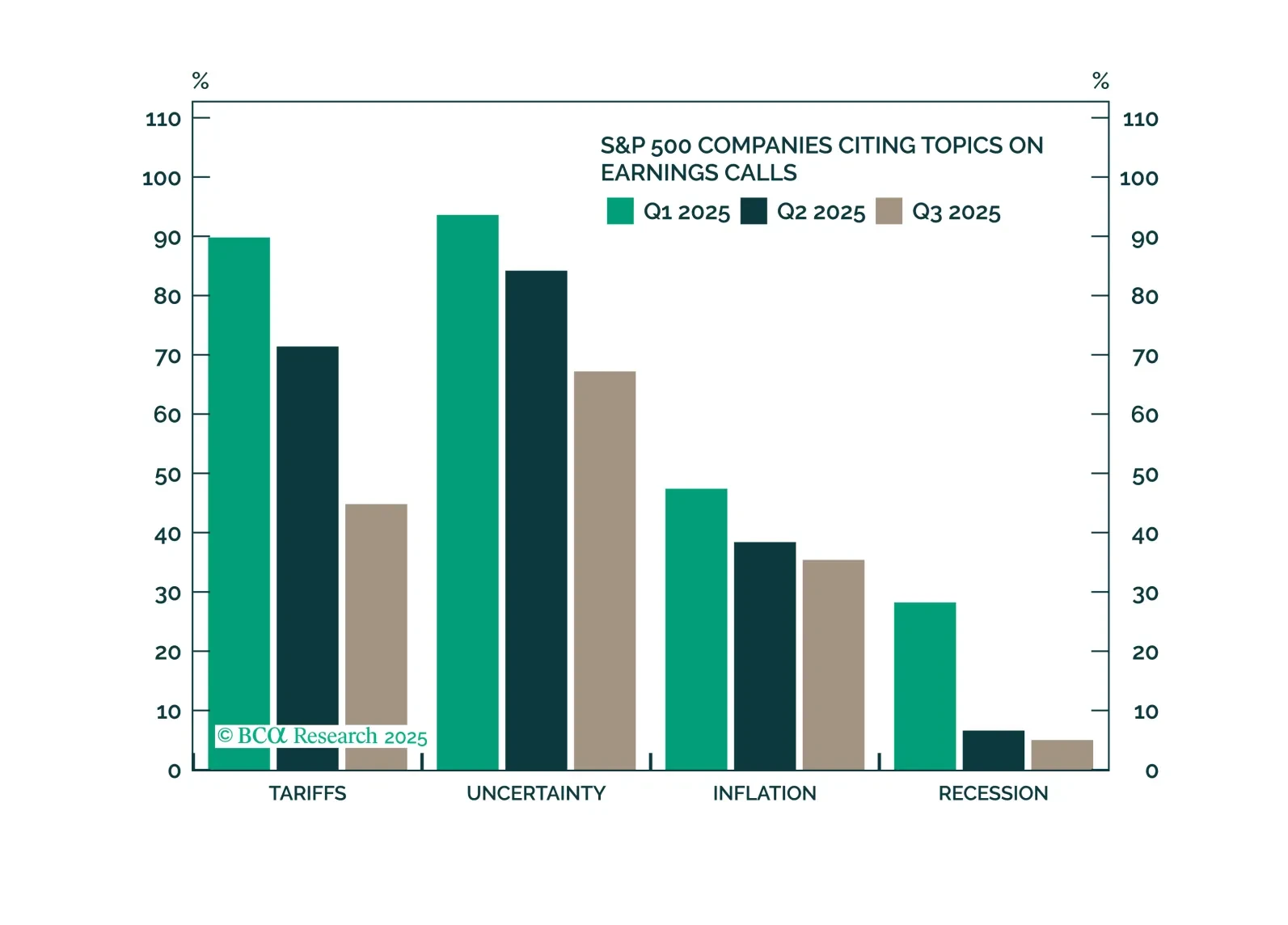

Tariffs are fading in importance as companies successfully mitigate cost pressures and preserve profitability. The recent wave of high-profile layoffs is more concerning, but there does not appear to be a systemic reason behind the announcements. However, emerging labor market softness could pose a major risk for equities. We remain vigilant.

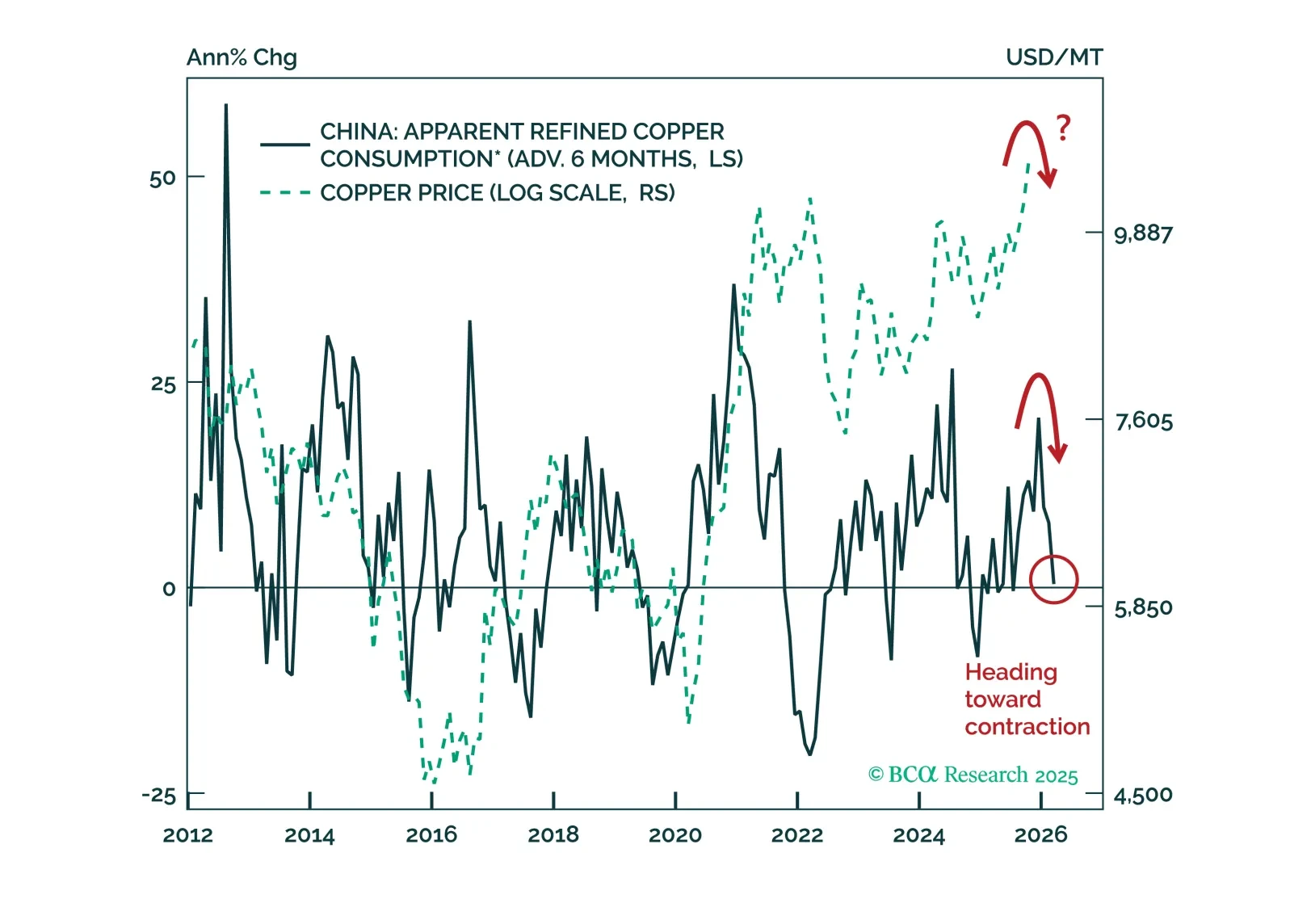

Should investors chase the copper rally or use the latest bout of strength as an opportunity to sell?

We warn that weakening Chinese demand and shrinking global manufacturing will weigh on the metal’s price over a cyclical timeframe.

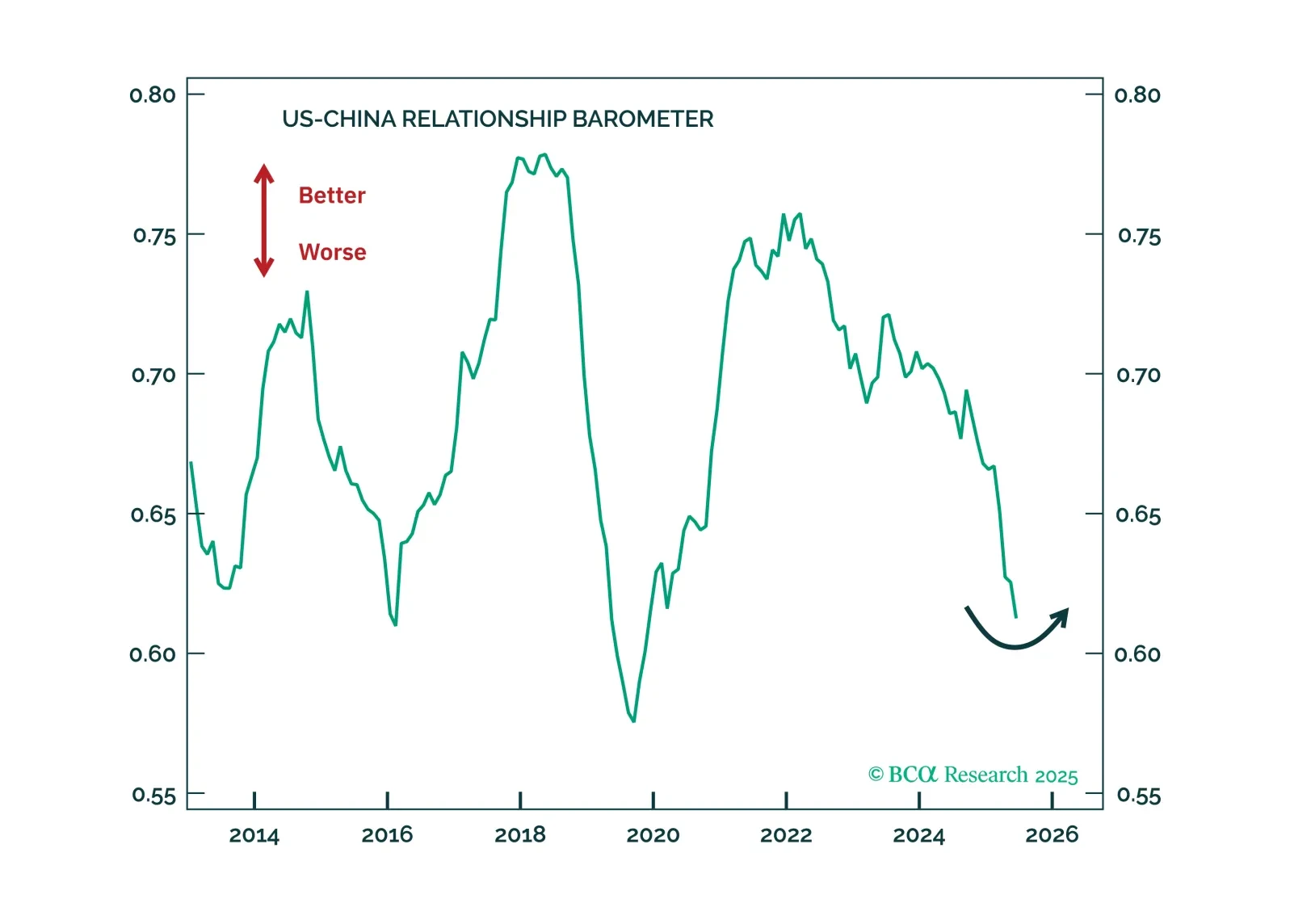

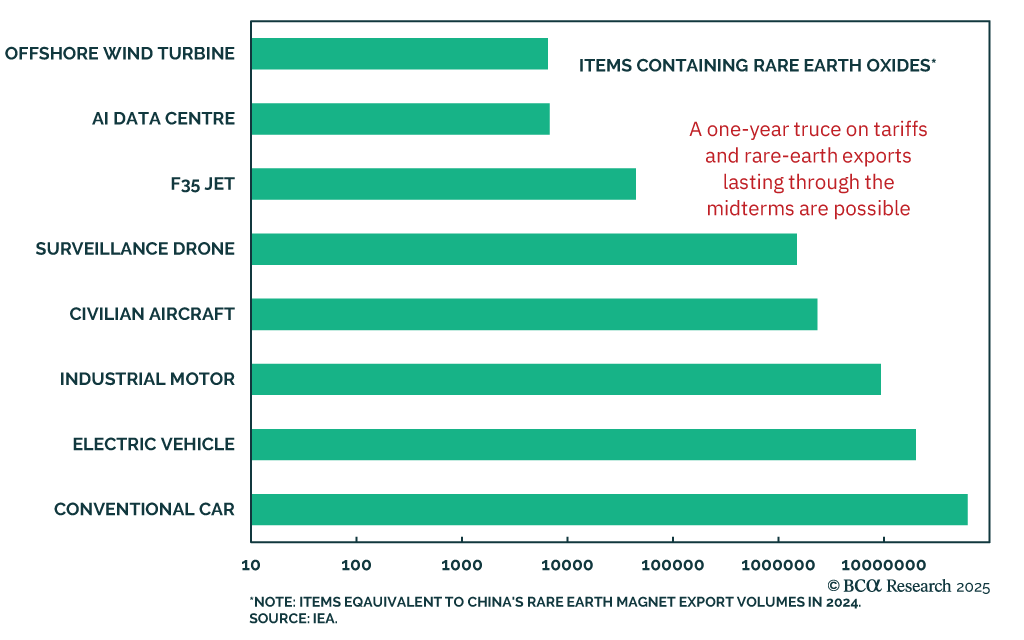

The Trump-Xi summit continued the trade truce and tentatively created a framework to contain tensions over 2026. That is not a trade deal but it is good enough for global financial markets, especially Chinese assets.

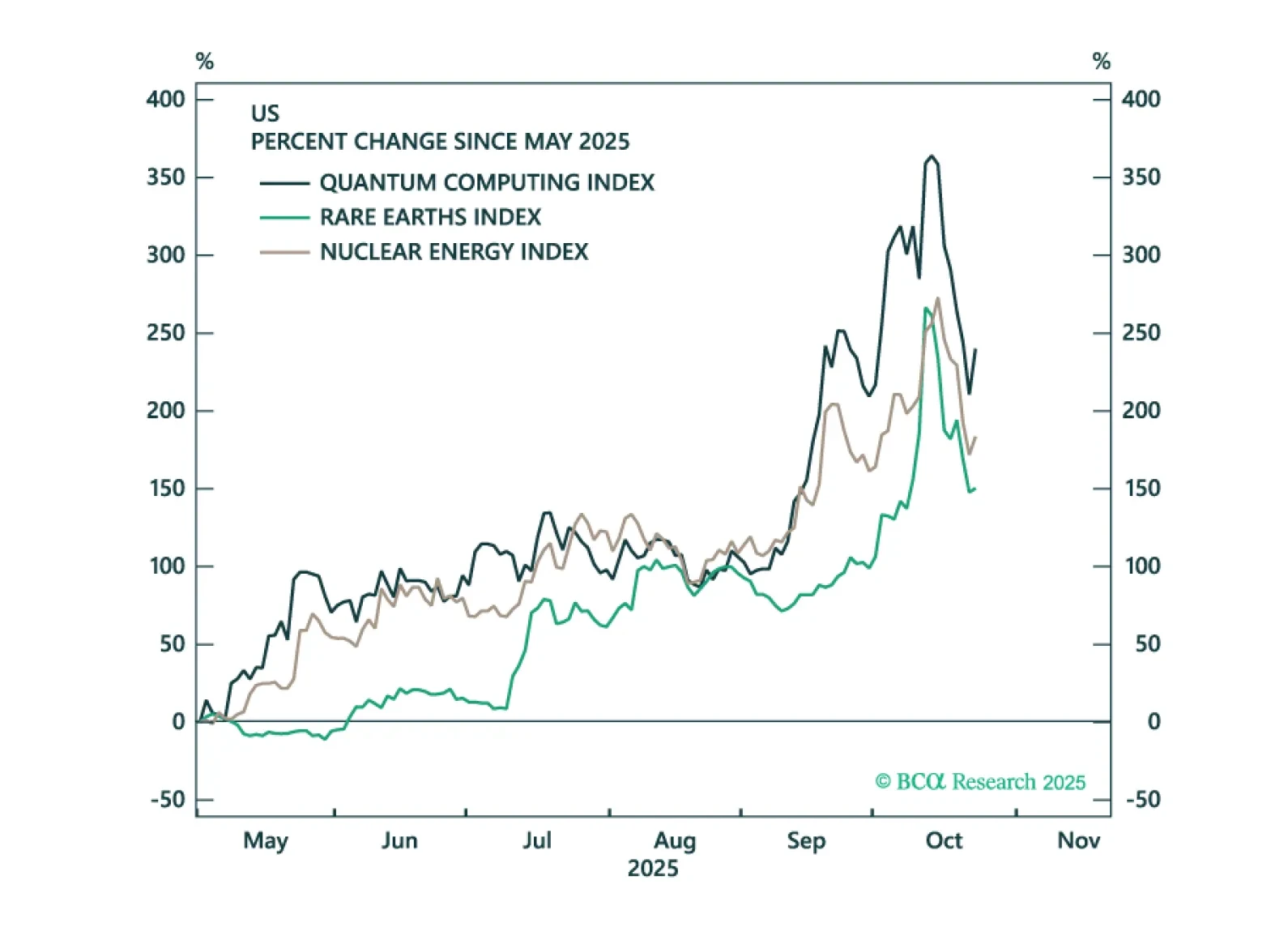

Precious metals, corporate credit, and tech stocks are all showing signs of late-cycle euphoria. We identify various trigger points that investors should monitor to turn more bearish.

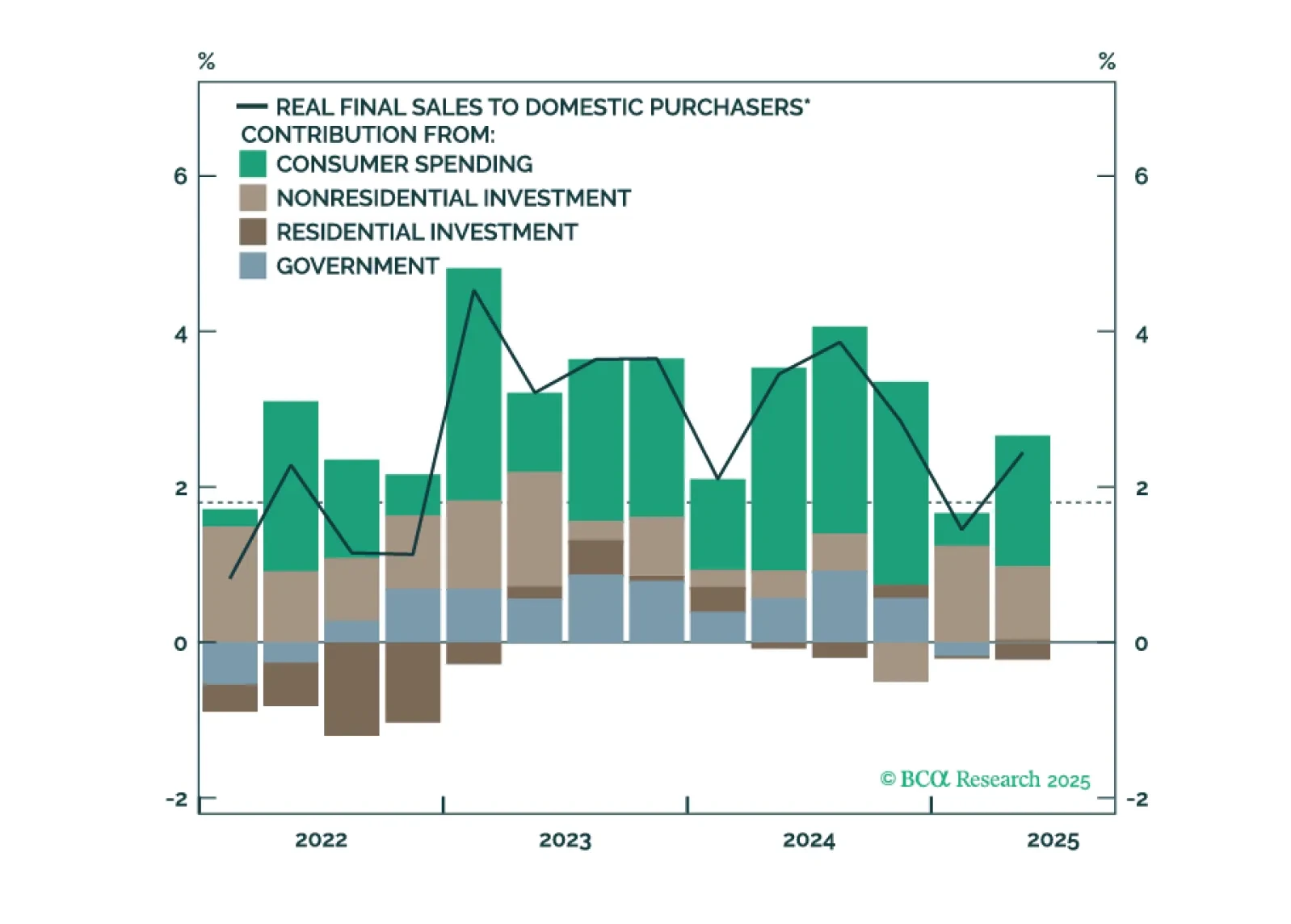

The Fed is poised to deliver a 25-basis-point rate cut this month, but a follow-up rate cut in December will depend on how the divergence between strong consumer spending and weak employment growth is resolved.

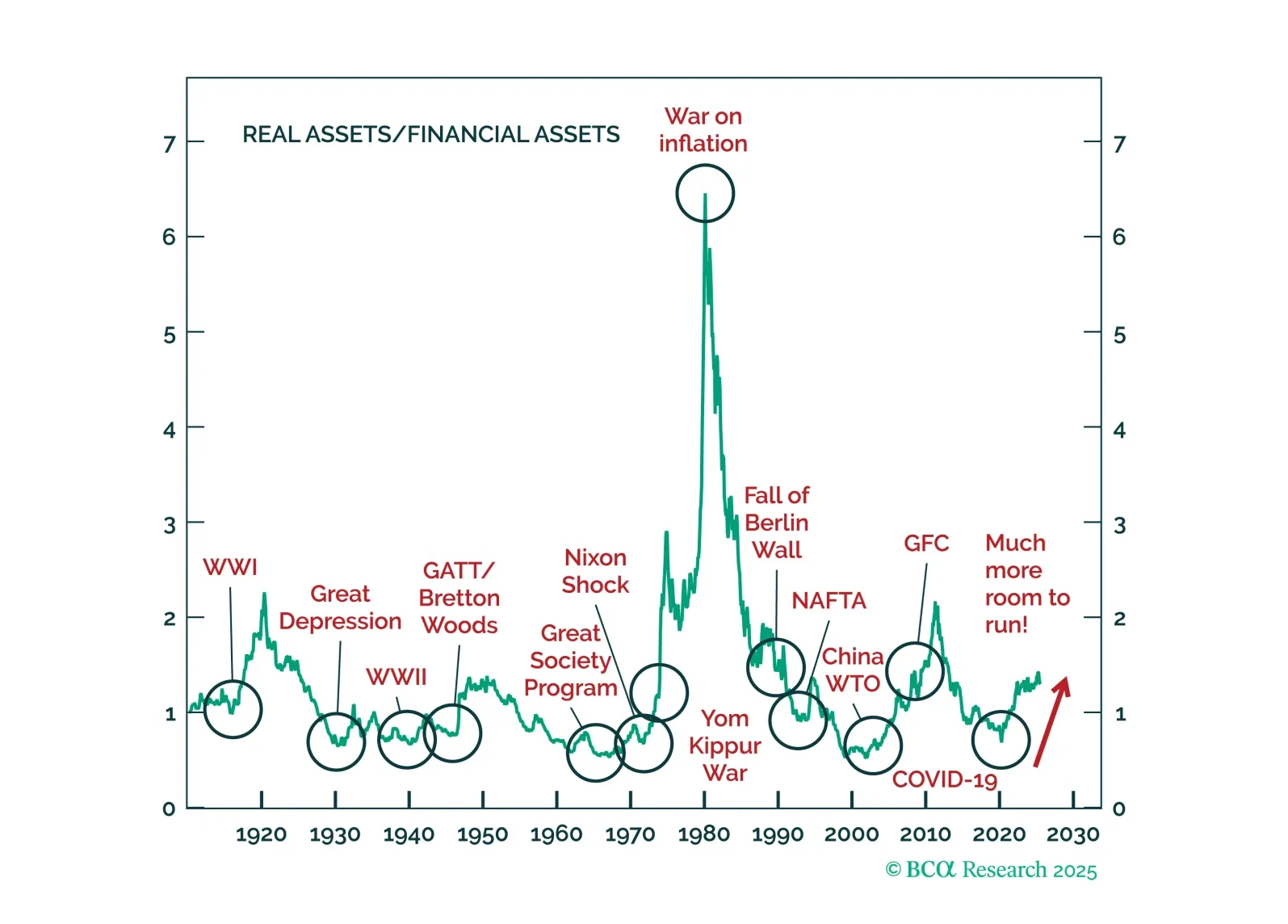

We remain bullish both bonds and equities, but conviction is falling. We are Luddites when it comes to the AI theme, but we have followed it regardless. A bubble is a bubble, not to be shorted. Yet Europe’s weak AI returns reveal 2025’s real story: the fall of King Dollar.