Softs

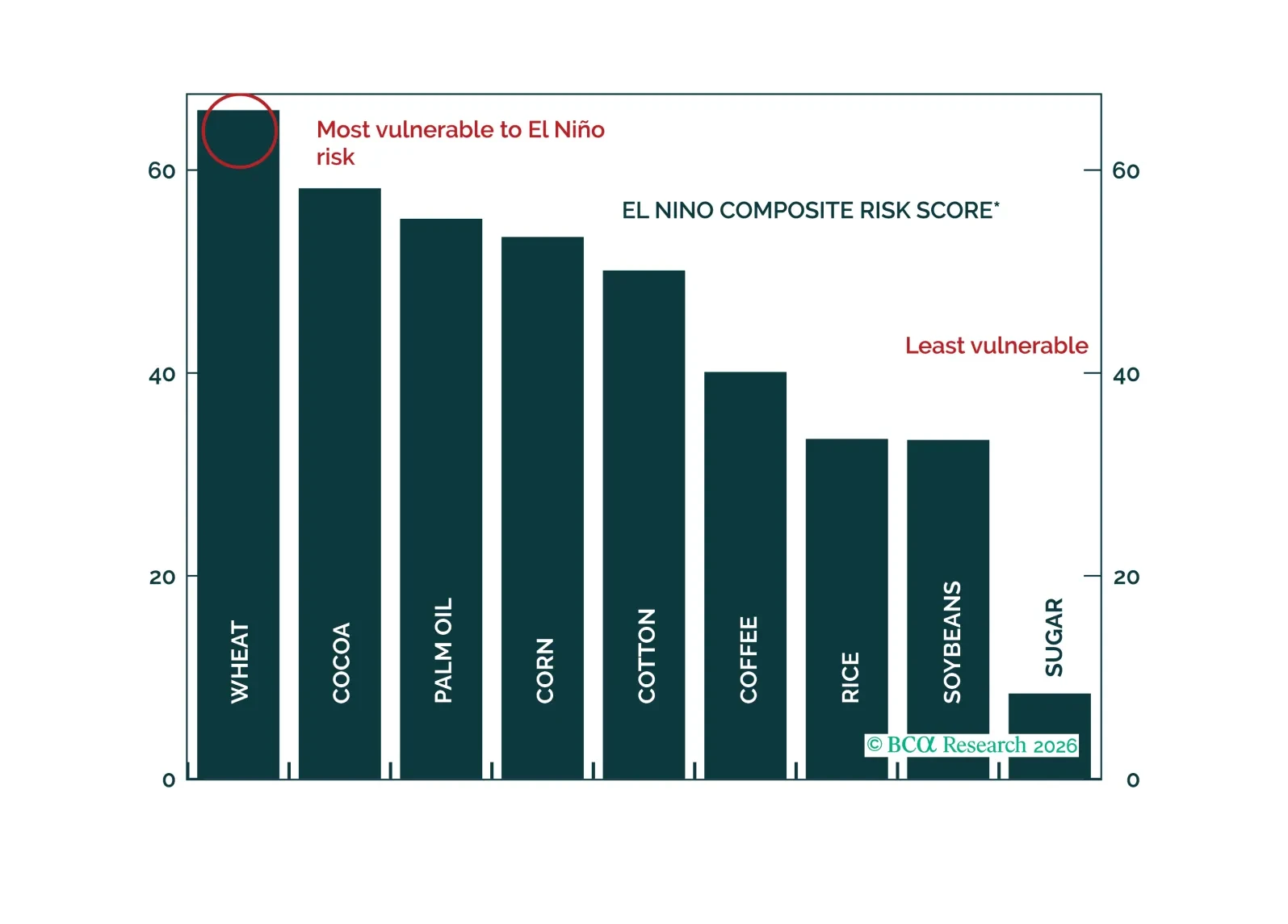

The risk of a “super El Niño” represents a meaningful threat to agricultural markets. Wheat, cocoa, and palm oil appear particularly vulnerable to El Niño-related supply disruptions.

A rise in food prices could also generate political — and potentially geopolitical — reverberations across frontier and emerging markets, where food prices are far more relevant than in developed economies.

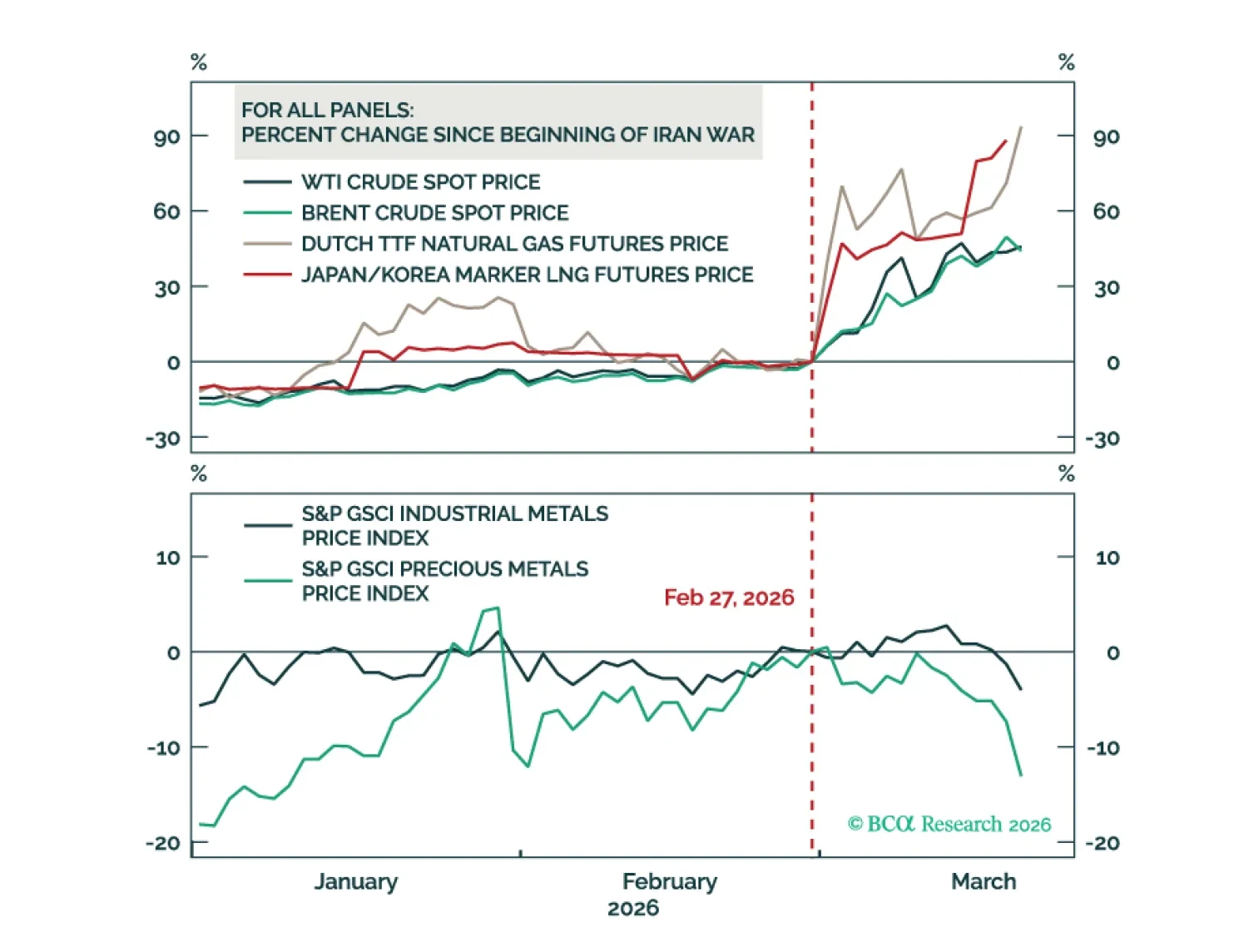

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

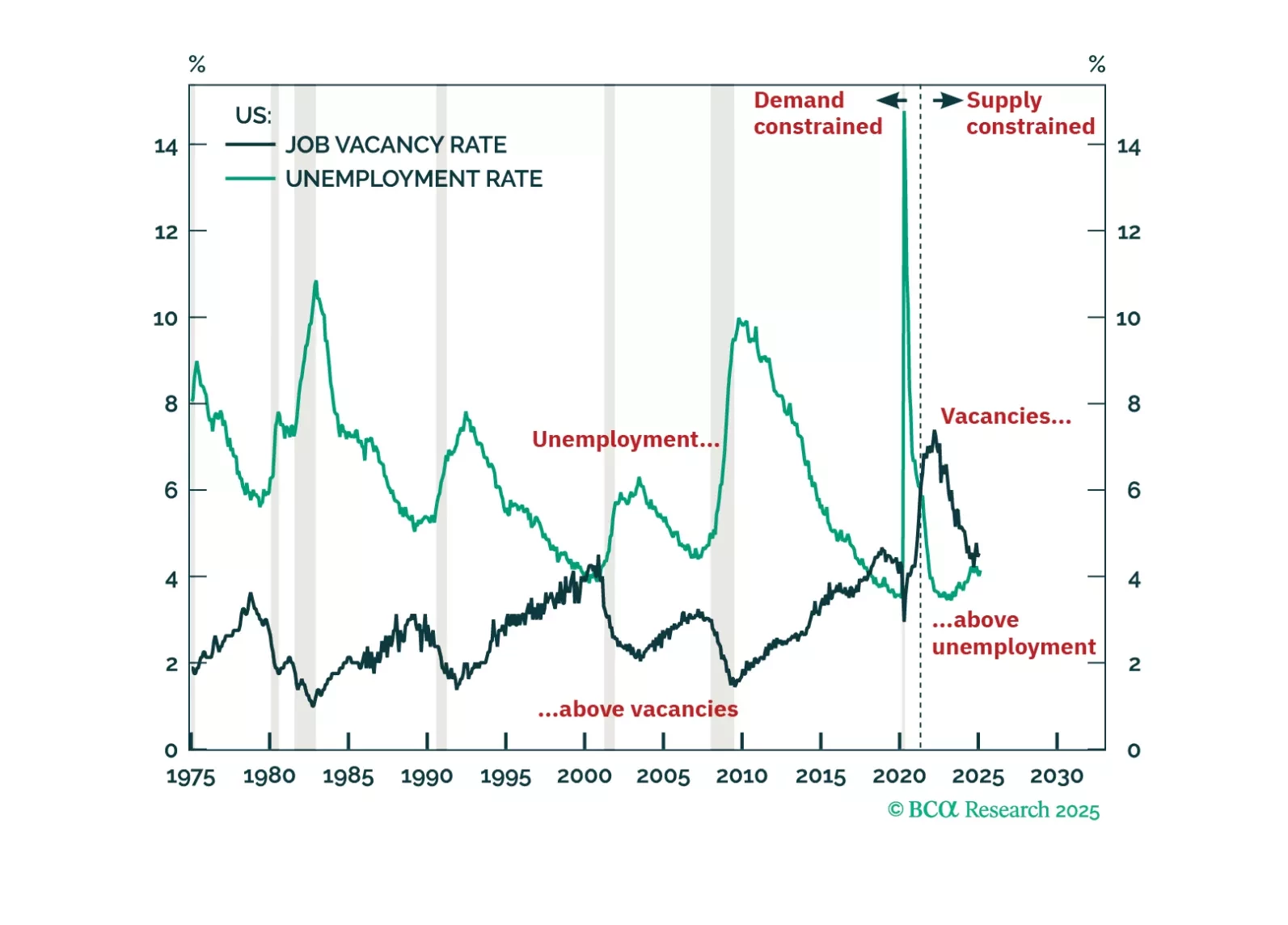

The US economy has never entered a demand-driven recession without labour demand running below labour supply and without the job vacancy rate running below the unemployment rate. Right now though, US labour demand is still running 1.7 million workers above labour supply, and the job vacancy rate is running comfortably above the unemployment rate. This suggests that the labour market is still supply-constrained, and that a demand-driven recession is not imminent. We discuss the investment implications. Plus, more about our ‘trade of the century’: long cotton versus coffee.

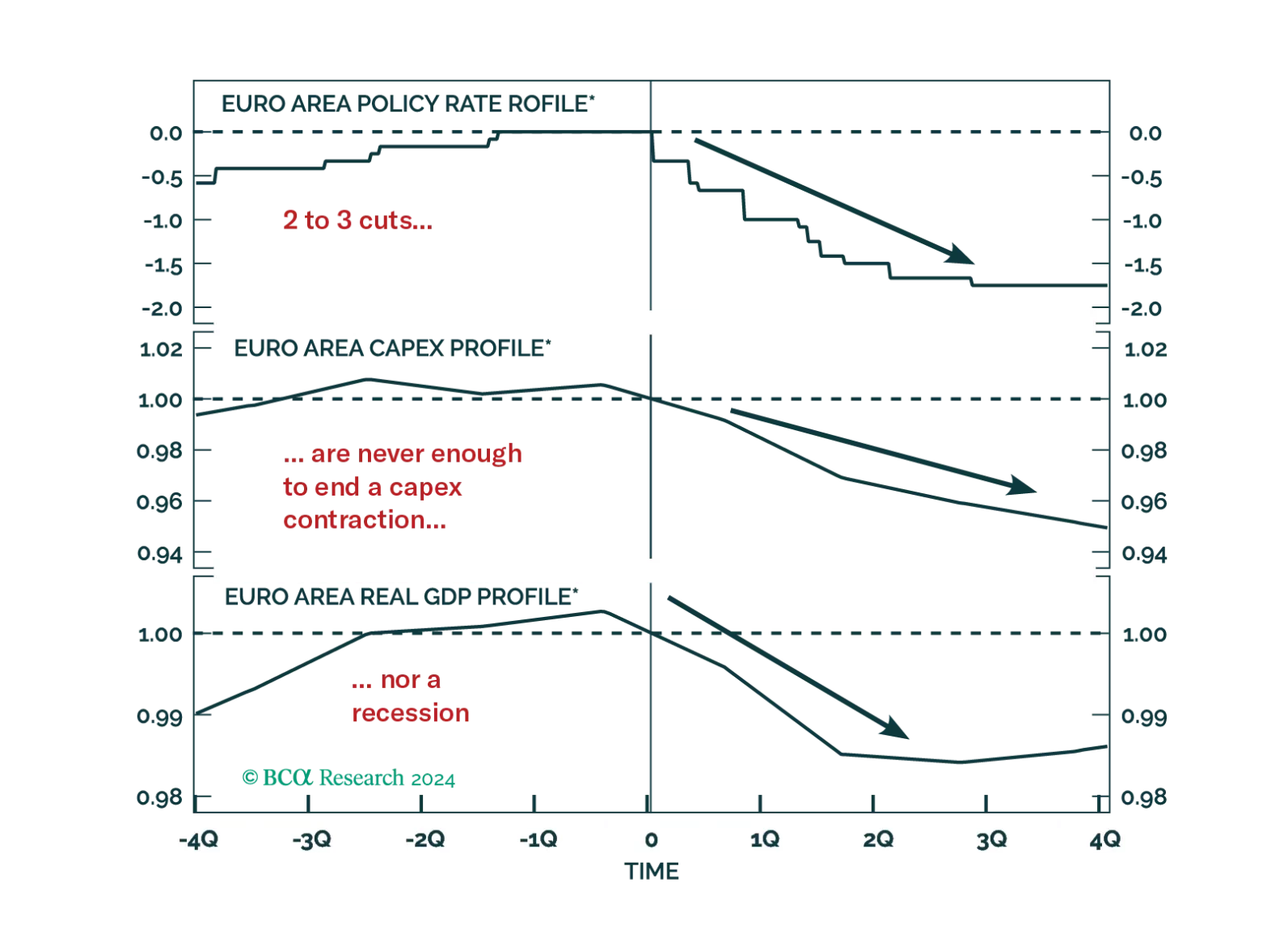

Investors hope that the ECB rate cuts priced into the curve will be sufficient to achieve a soft landing in Europe. History argues against this view, but will this time be different?

Looking at economic activity, global monetary policy seems restrictive, however, the behavior of financial markets tells a different story. What gives?

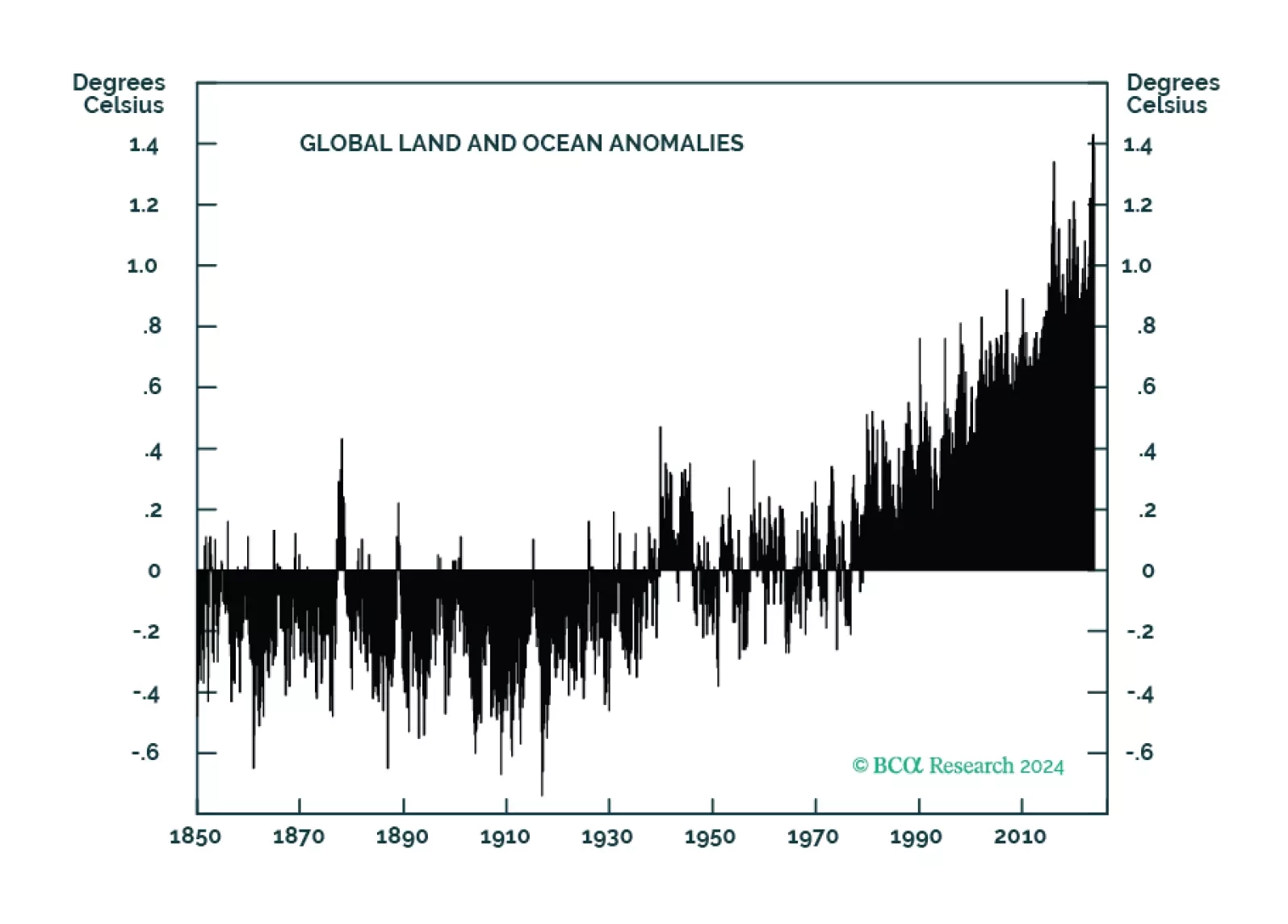

Global ag markets will become more volatile as anthropogenically induced climate change continues to degrade farmland. This will make price signals emanating from these markets less efficient in terms of processing supply-demand fundamentals. All else equal, food prices likely move higher, which will contribute to inflationary biases in the medium-to-long run. Investors will continue to seek out farmland investments as a way to diversify portfolio risk and raise absolute returns.