Services

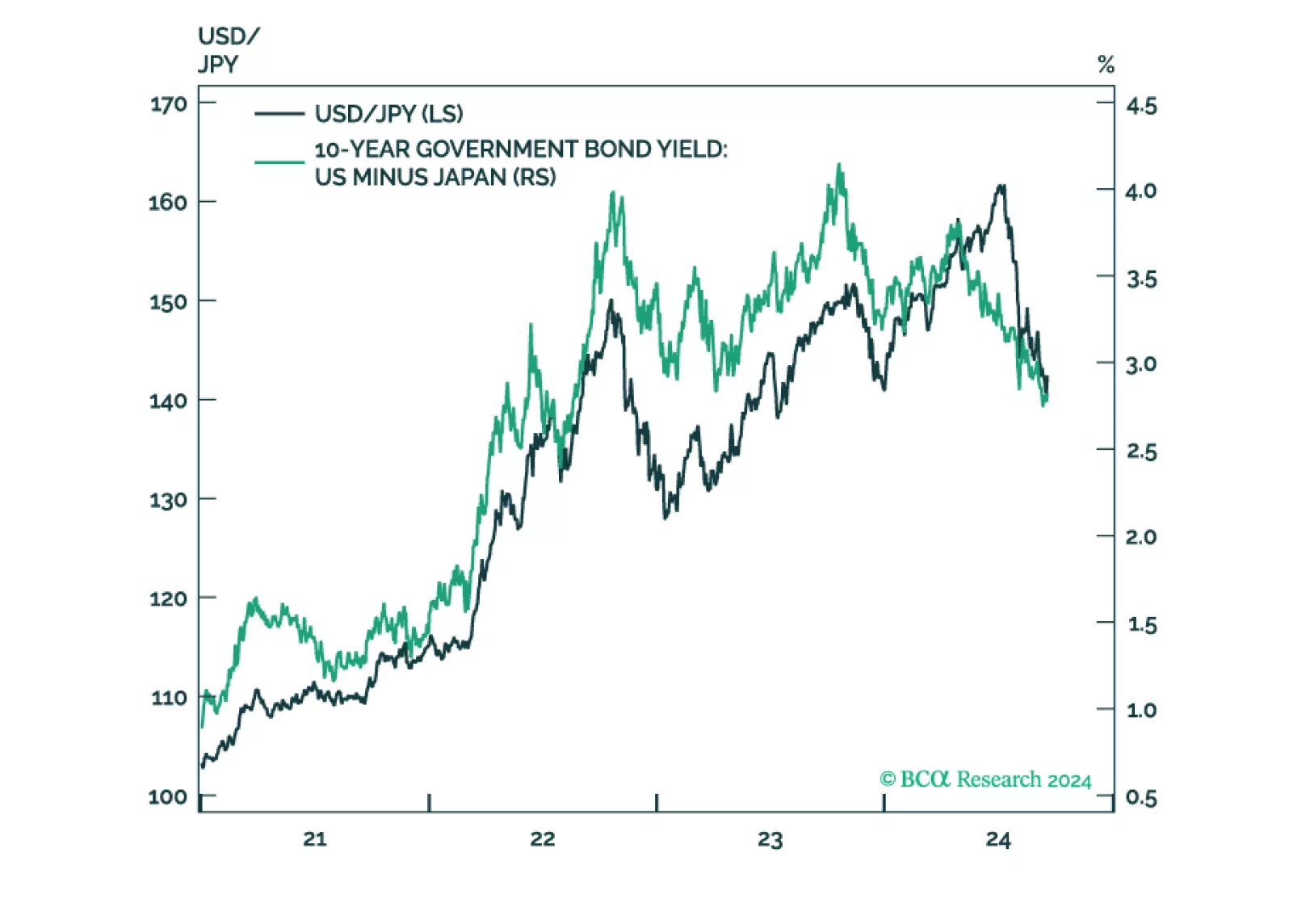

In this report, we argue that the Bank of Japan is unlikely to hike interest rates this week, but the relative trajectory of bond yields in Japan is higher. This warrants an underweight position in JGBs and a leveraged bet on a higher yen. The positioning for equity investors is murkier, as progress on corporate reforms is necessary for a rerating in Japanese shares. That is not yet very clear. The bottom line is: Stay long the yen.

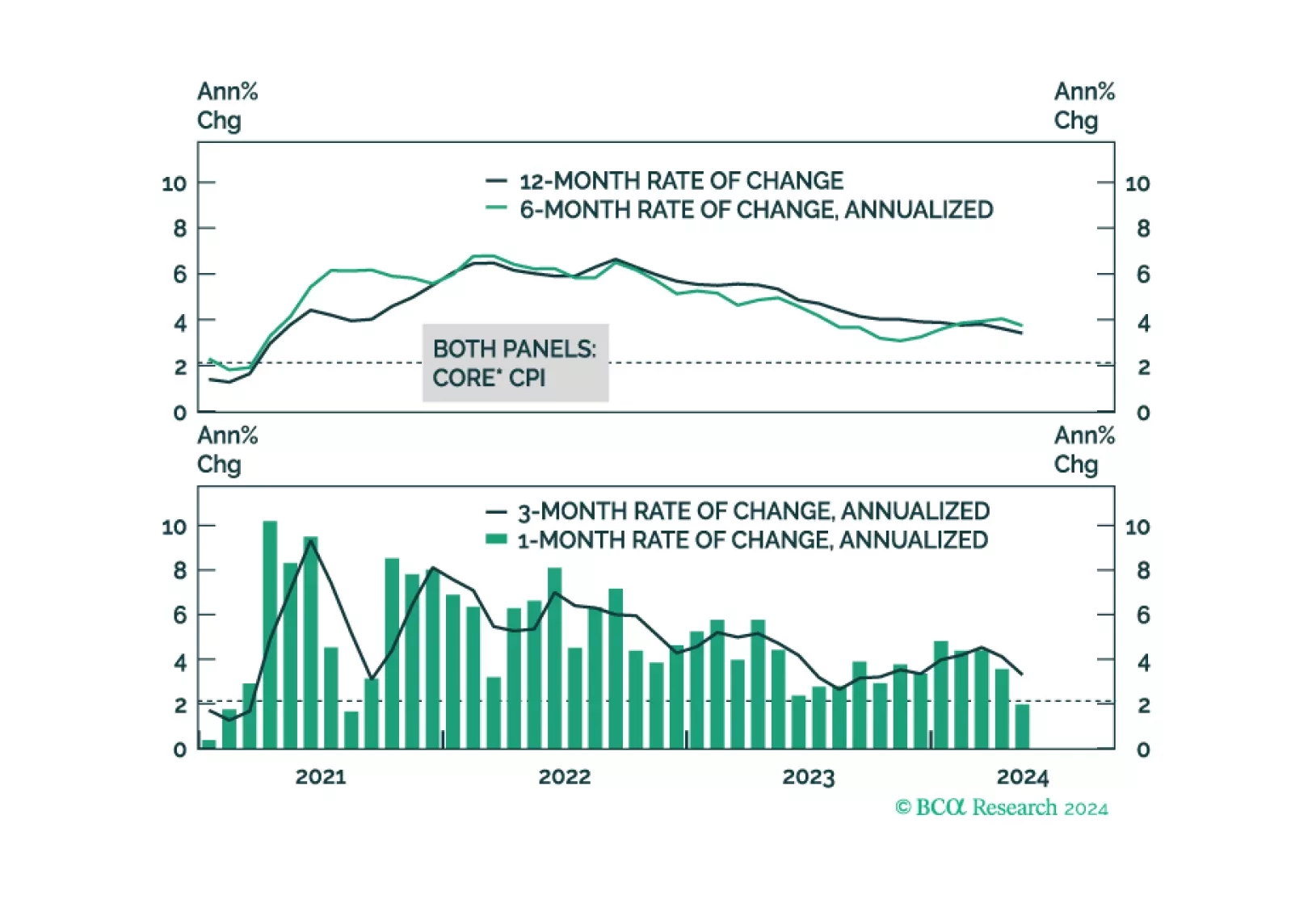

We consider the outlook for CPI inflation over the next 12 months. Our baseline forecast calls for core CPI to hit 2.40% during this timeframe and for headline CPI to fall between 1.74% and 2.49%.

In Section I, we examine some concerning signs of US economic weakness that emerged in June. We also discuss portfolio positioning in the face of falling interest rates and cross-check our recommended US equity overweight in the face of extremely optimistic expectations about AI’s impact on growth. We conclude that defensive positioning continues to be warranted. In Section II, we dig into those optimistic expectations for AI. We find that the US equity market is significantly overvalued unless the deployment of AI technology causes a 10-to-20 year productivity surge in line with what occurred during the IT revolution of the 1990s, with persistently high margins on the revenue generated from the improvement in growth. We doubt that AI will end up truly boosting economic activity by this magnitude.