Sectors

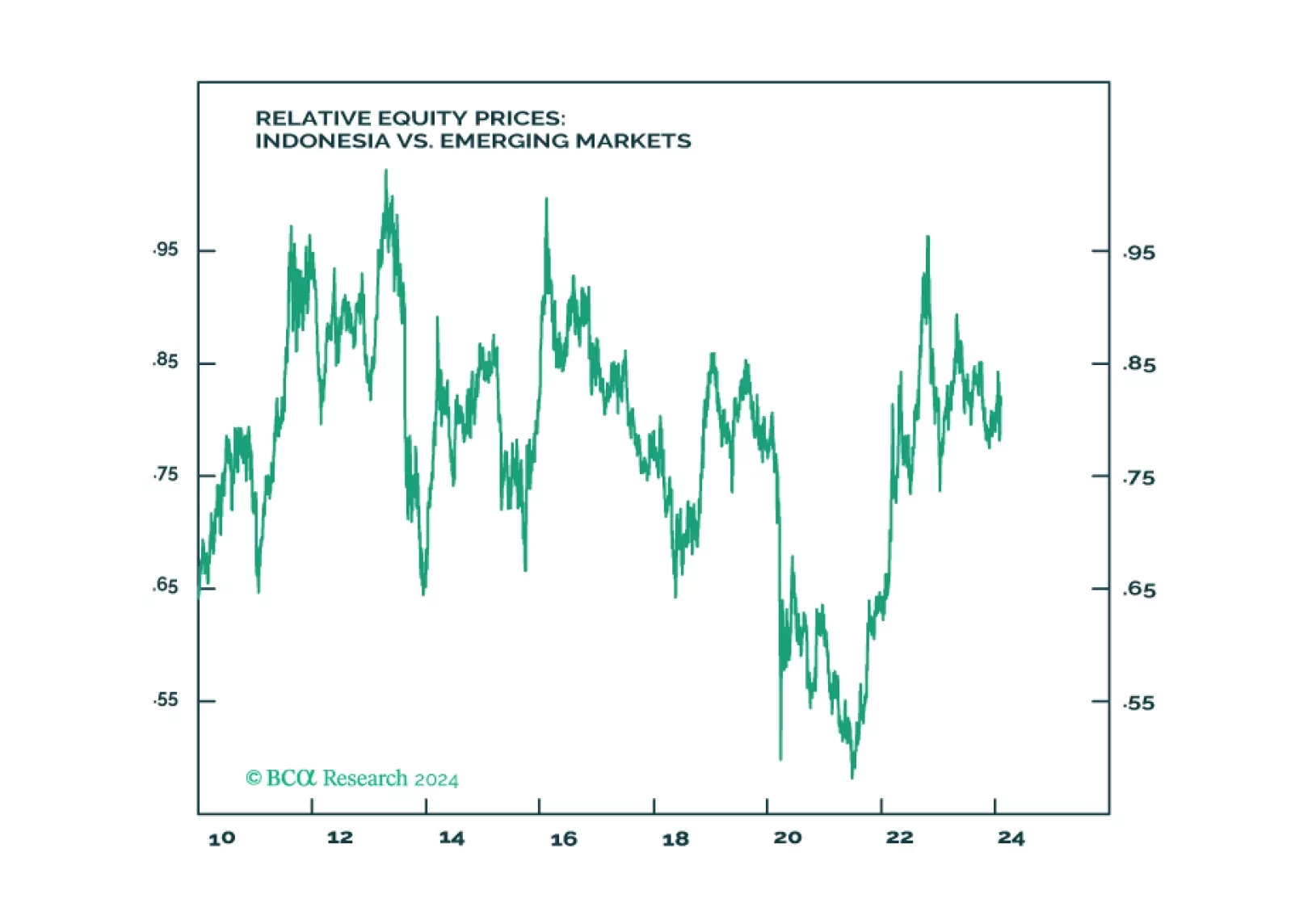

Indonesia will not revert to dictatorship. Yet the guardrails against authoritarianism are also constraining the actions of the next government in tackling near term domestic and regional challenges. For long-term positioning, use potential selloff from a “dictatorship scare” to build position as structural outlook for Indonesia is positive due to the China-West divorce and the global energy transition.

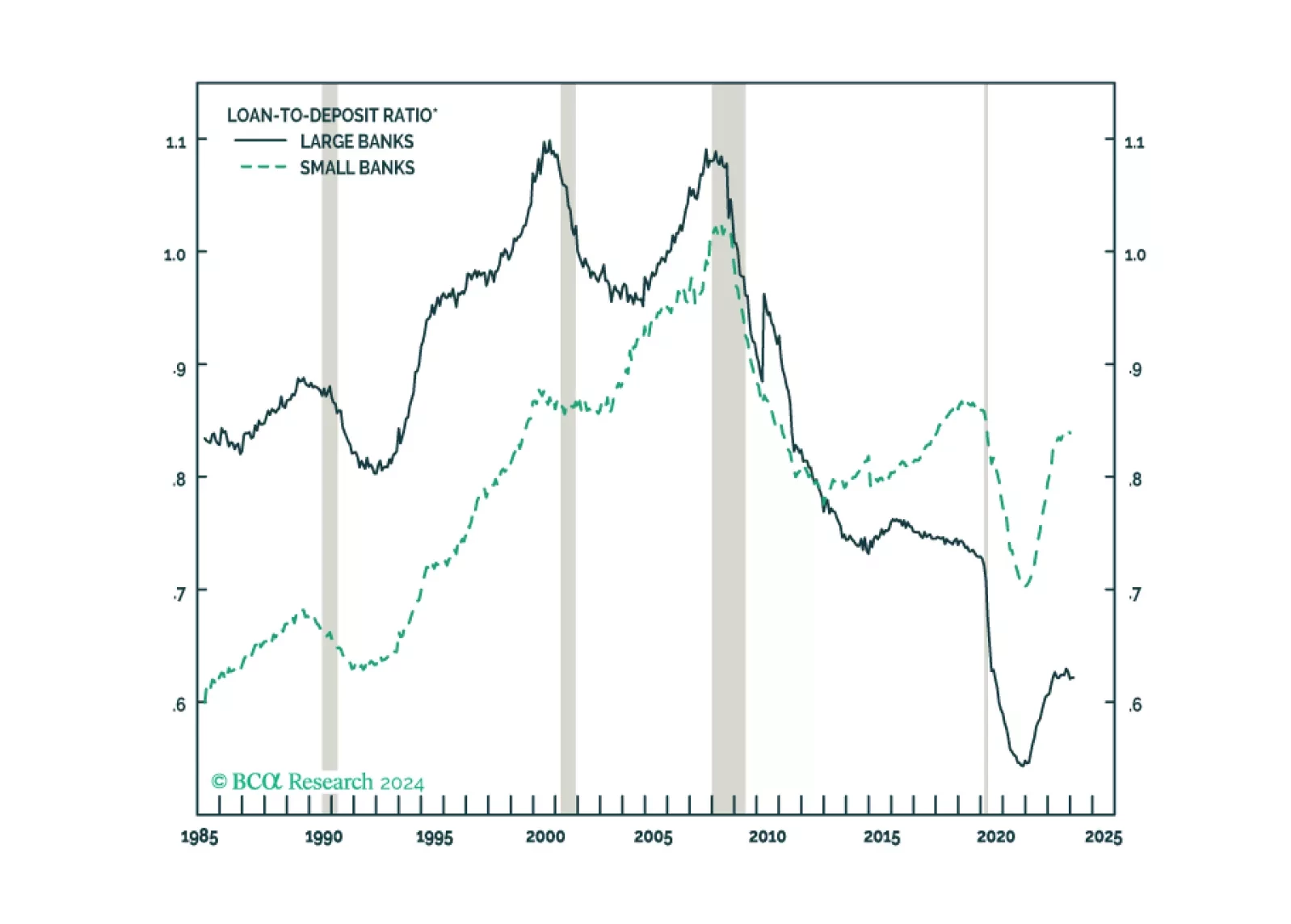

We do not believe that NYCB is a canary in the coal mine for a new round of bank distress. The MidCap 400 Regional Bank Index’s subsequent 10% decline looks to us like a juicy opportunity for stockpickers who can separate the wheat from the chaff. Our Special Report is meant to assist them with their initial winnowing.

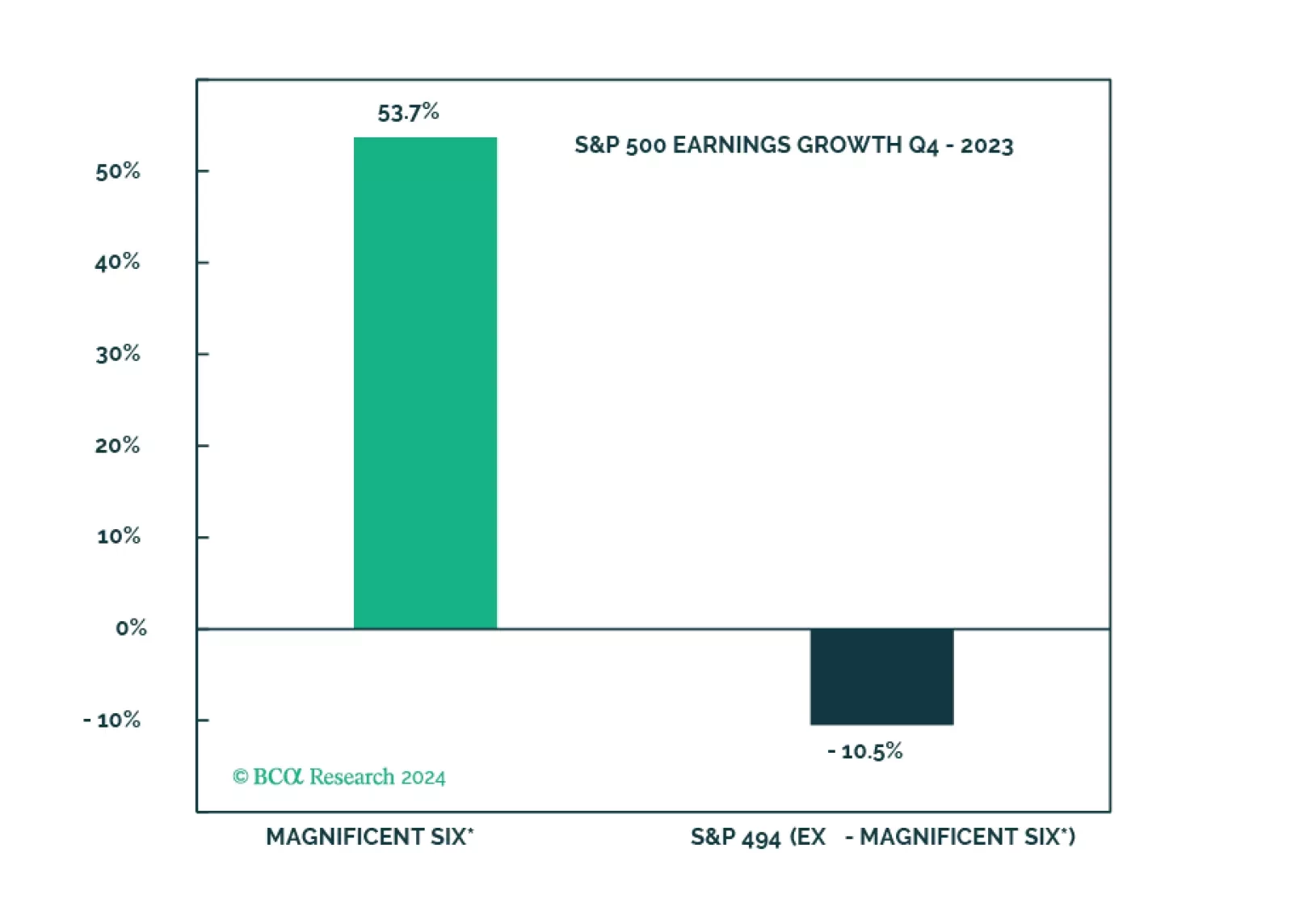

The soft landing and rate cuts narrative is being priced out, and the S&P 500 is overvalued and getting overbought. The Magnificent Seven are about to get a new moniker on the back of performance dispersion. However, without the cohort, S&P 500 earnings would have been even deeper in the red.

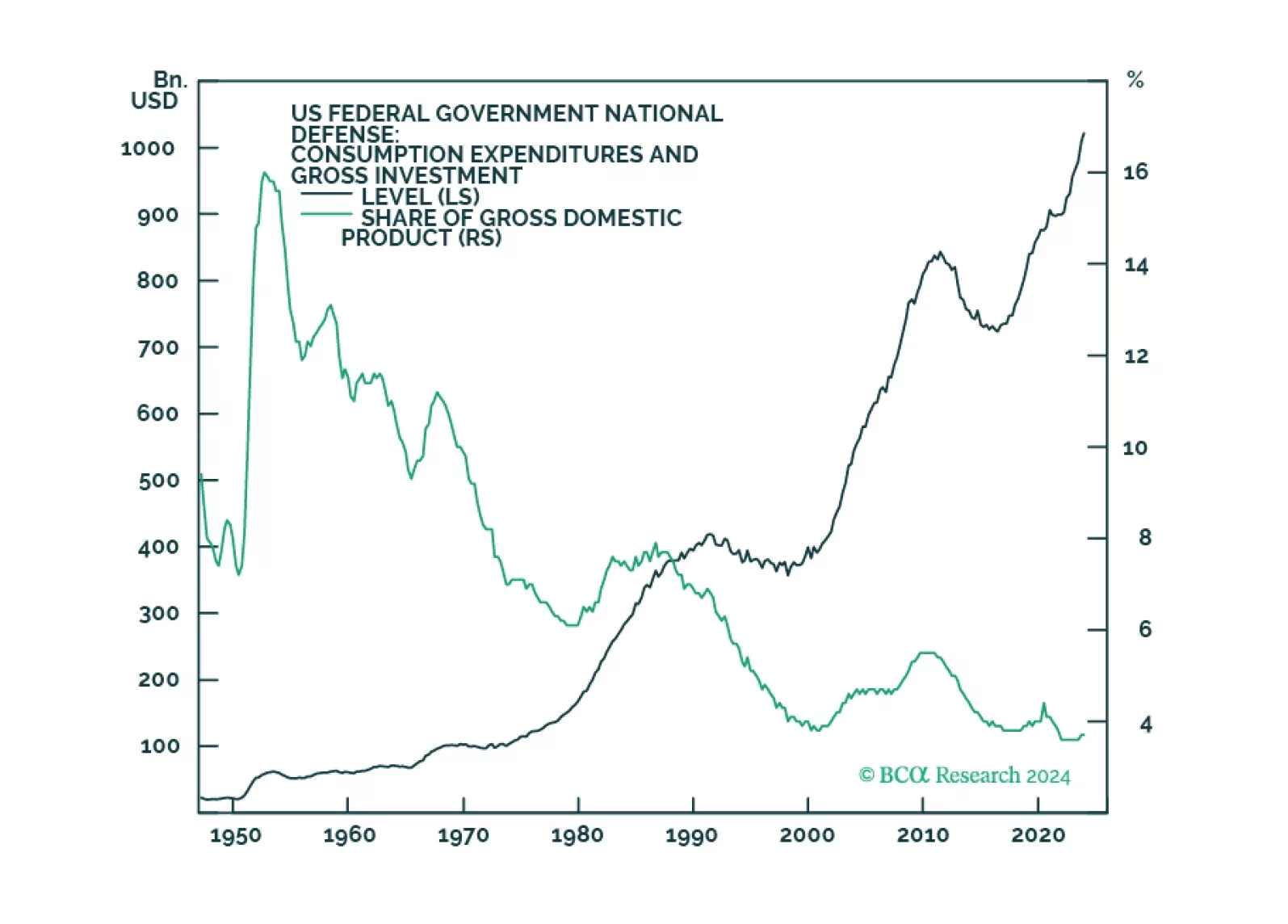

The US DoD rolled out its first-ever industrial policy designed to reverse decades of atrophy in its military-industrial complex. This left the US with diminished access to CMM commodities and supply chains, which are now dominated by China, and an industrial ecosystem to support its war-fighting mission that risks become uncompetitive. We remain long the XME and COMT ETFs to retain exposure to CMM producers and refiners. At tonight’s close, we will get long the Invesco Aerospace & Defense ETF (PPA), anticipating increased defense spending.

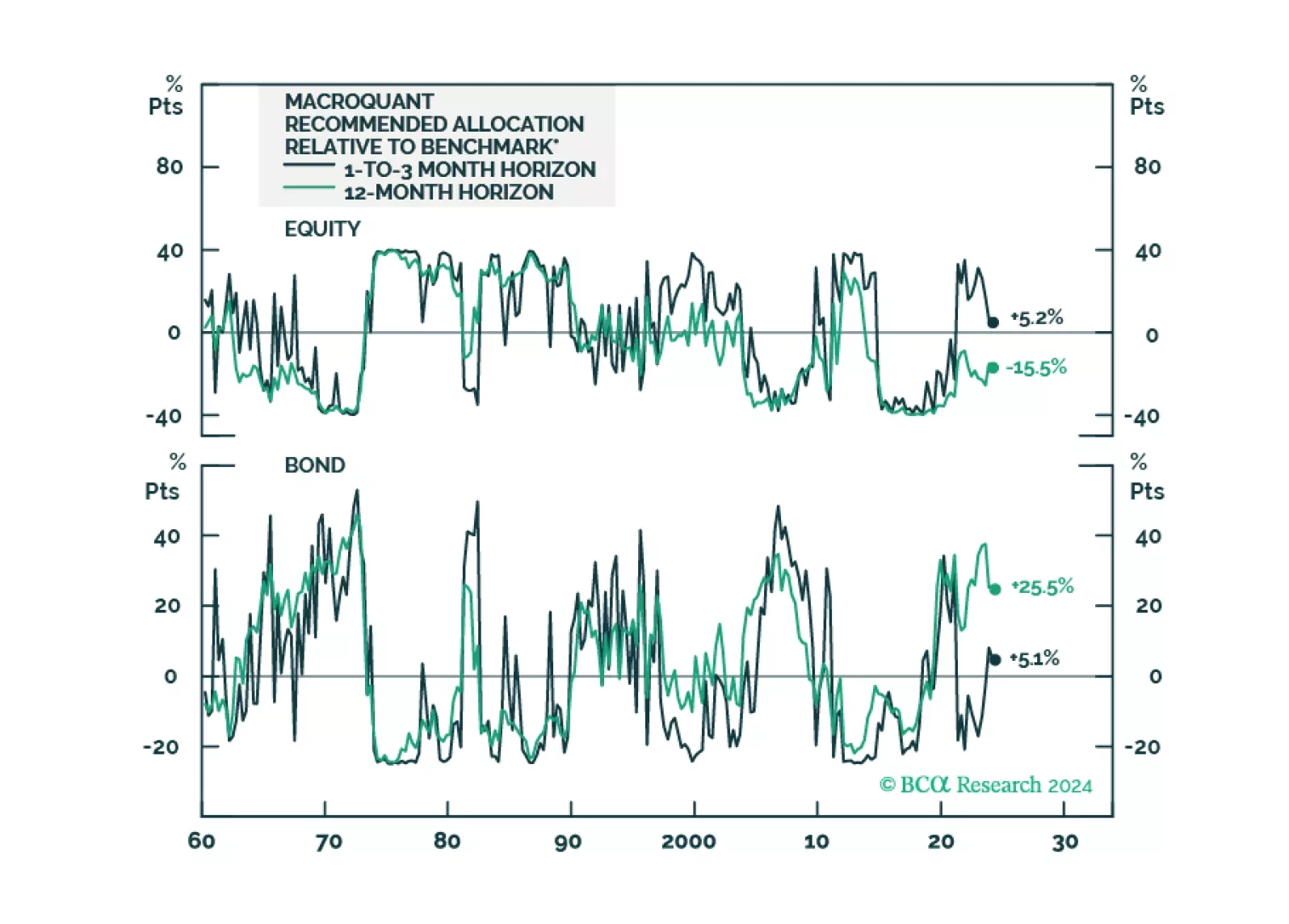

Following the release of the white paper yesterday, today we are sending you the inaugural issue of the MacroQuant Monthly, a report summarizing the output of our next-generation MacroQuant 2.0 model.

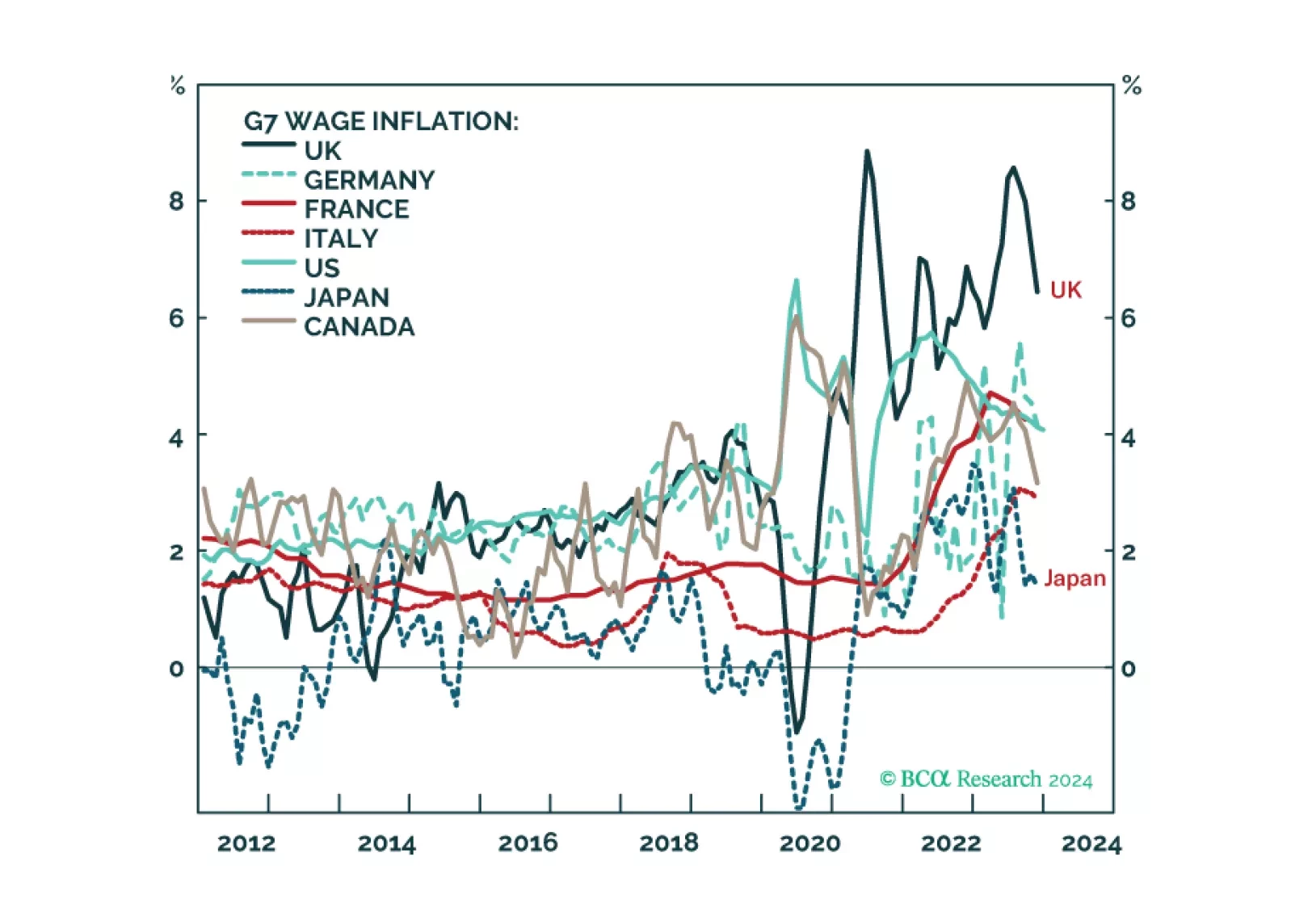

We describe and explain the wide disparity of wage inflation across G7 economies, and discuss what it means for the Fed, ECB, BoE, and BoJ policy moves in the coming year. Plus: we highlight two investments ripe for reversal, and two investments ripe for rebound.

A recent slew of macroeconomic data has reassured us that the runway to a recession is longer than many thought. However, that positive realization comes with two caveats. First, the Fed pivot is not imminent, and the magnitude of rate cuts may disappoint. Second, the recession has been delayed but not avoided. Further, geopolitical risk is elevated. We will overweight Tech on the next dip and upgrade Retail to an overweight.

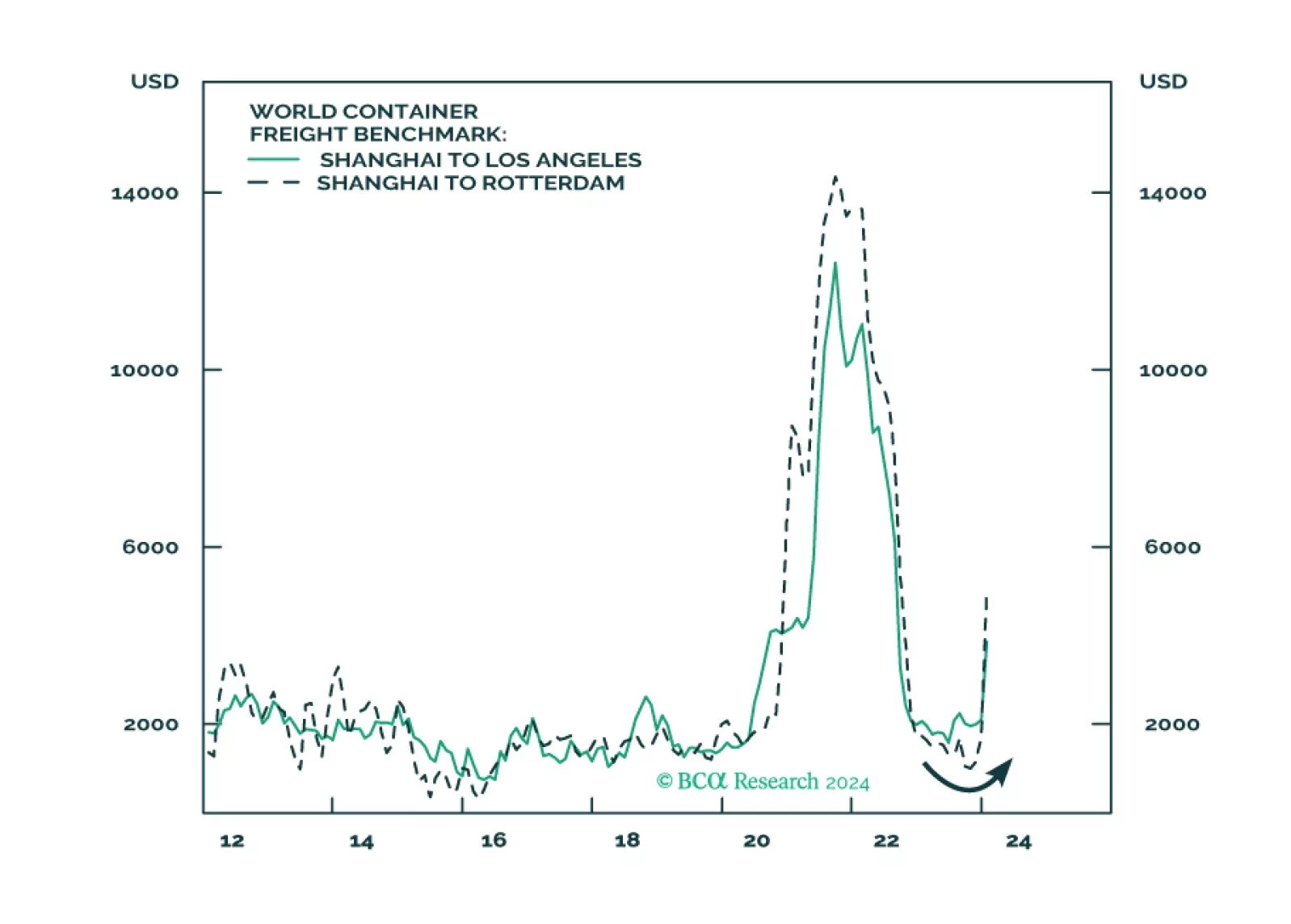

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

Middle East conflict, extreme US policy uncertainty, Chinese economic slowdown, US-Russian proxy war, and Asian military conflicts do not create a stable investment backdrop for 2024. Our top five “black swan” risks may be highly improbable, but they stem from these underlying trends.