Secession/Breakup

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.

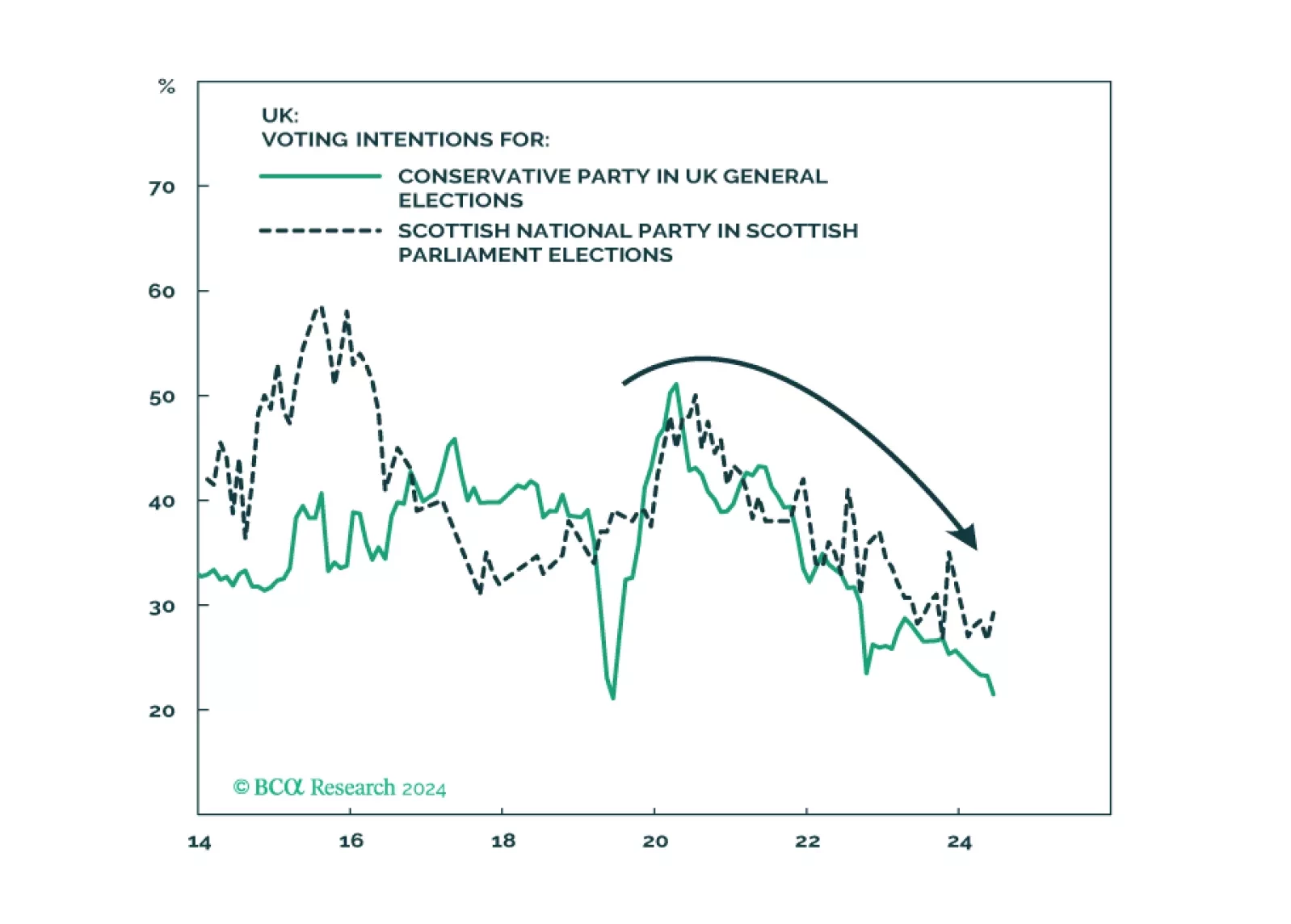

The Labour Party’s comeback in the UK is widely expected and will lead to fiscal stimulus consisting of increased public spending with minimal tax hikes. But a sweeping single-party majority will reduce social unrest only at the cost of higher taxes over the medium term. The paradigm has shifted away from the Thatcherite low-tax regime of the now-discredited Tories. v

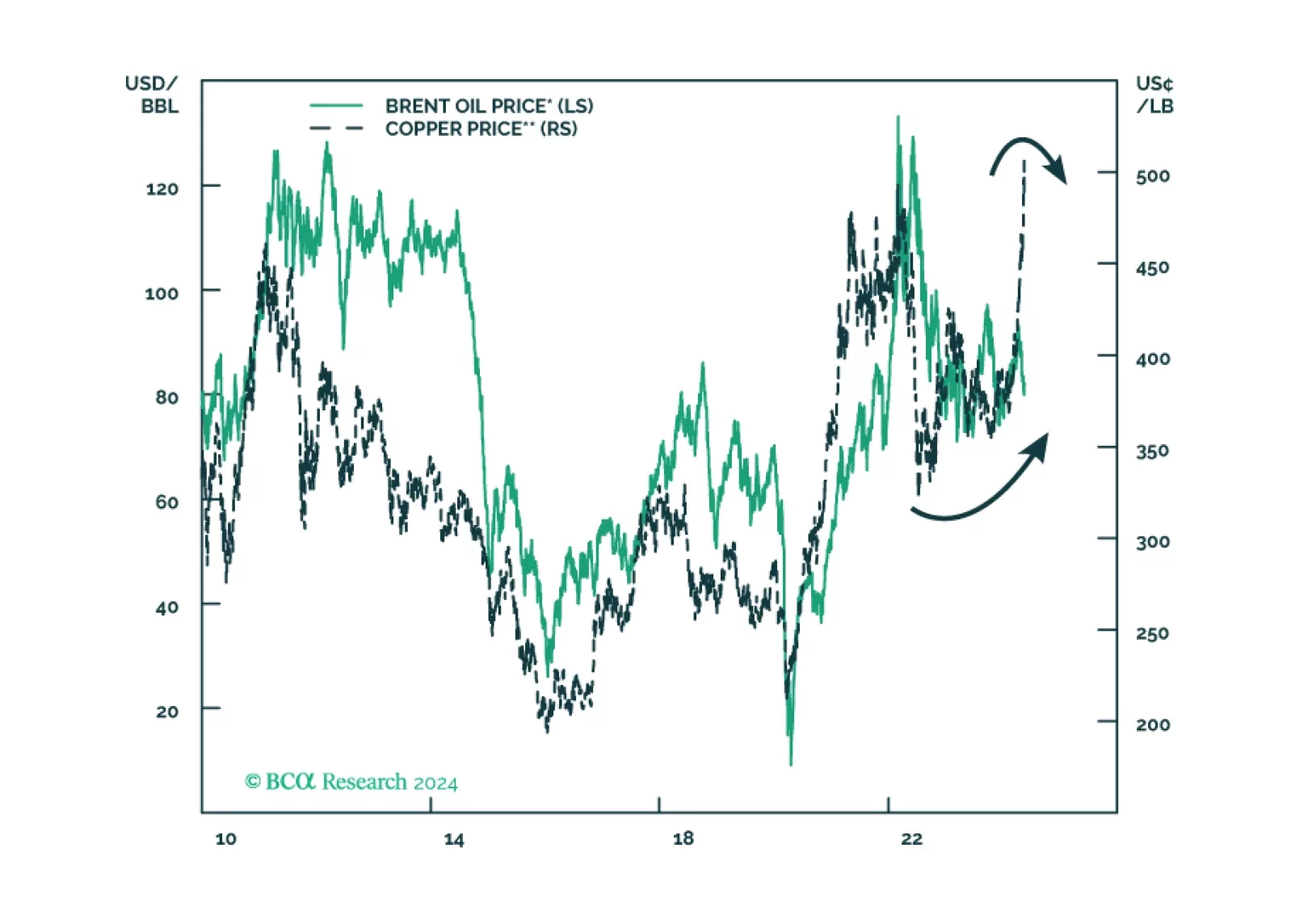

The death of the Iranian president reinforces our base case view of Middle Eastern instability and at least minor oil supply shocks. Rapid geopolitical developments in recent weeks are pointing to a new bout of global instability. The US is hobbled by its election. Conflicts with Russia, China, and Iran are all now escalating at the same time, at least marginally. Investors should reduce risk and shift to more defensive assets, markets, and sectors.

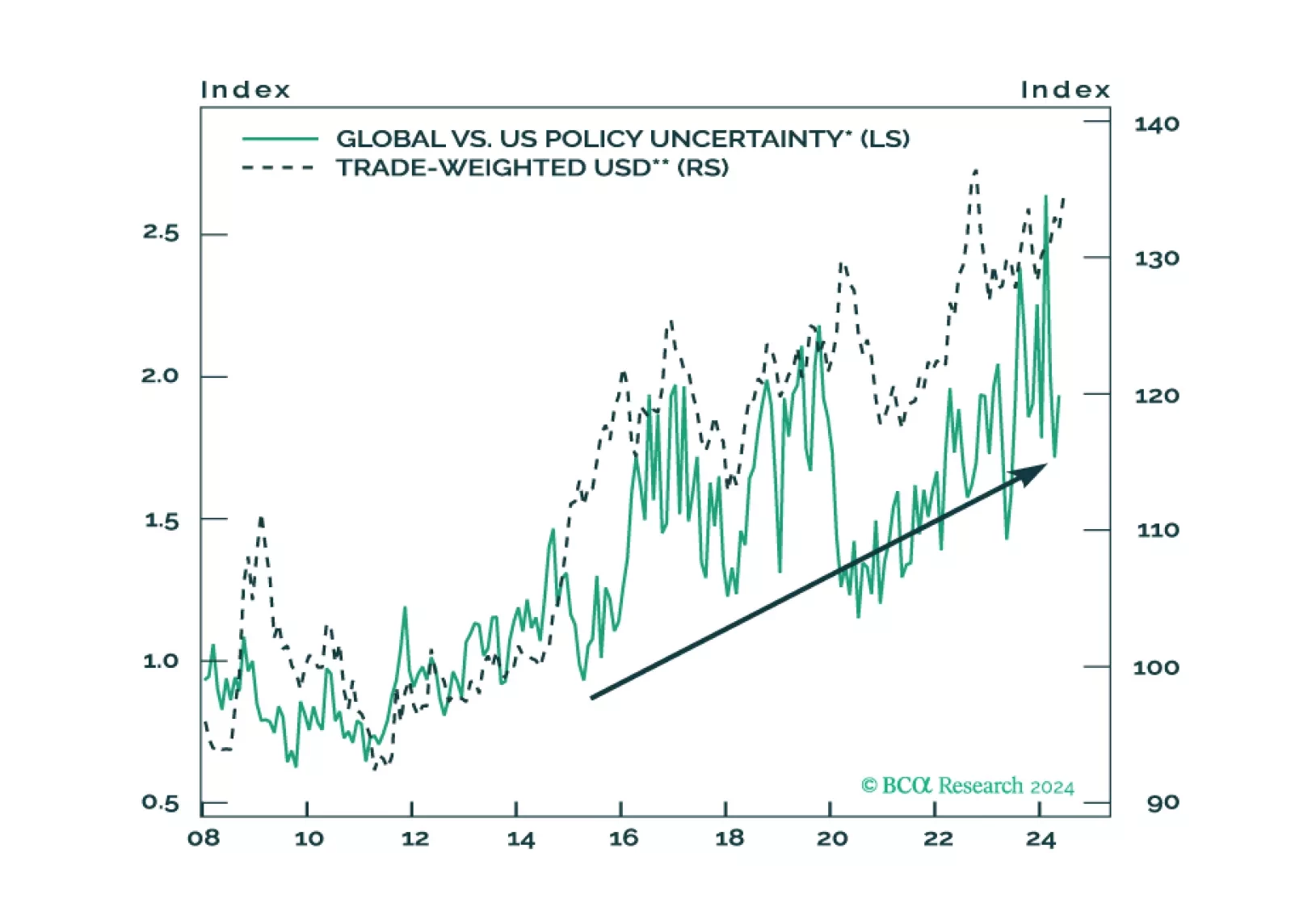

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

Global instability will continue in 2024 – whatever happens afterward. Slowing economies will exacerbate already high geopolitical risk and policy uncertainty stemming from the US election and foreign challenges to US leadership. Overweight government bonds, defensive sectors, the Americas versus other regions, aerospace/defense stocks, and cyber-security stocks.

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.

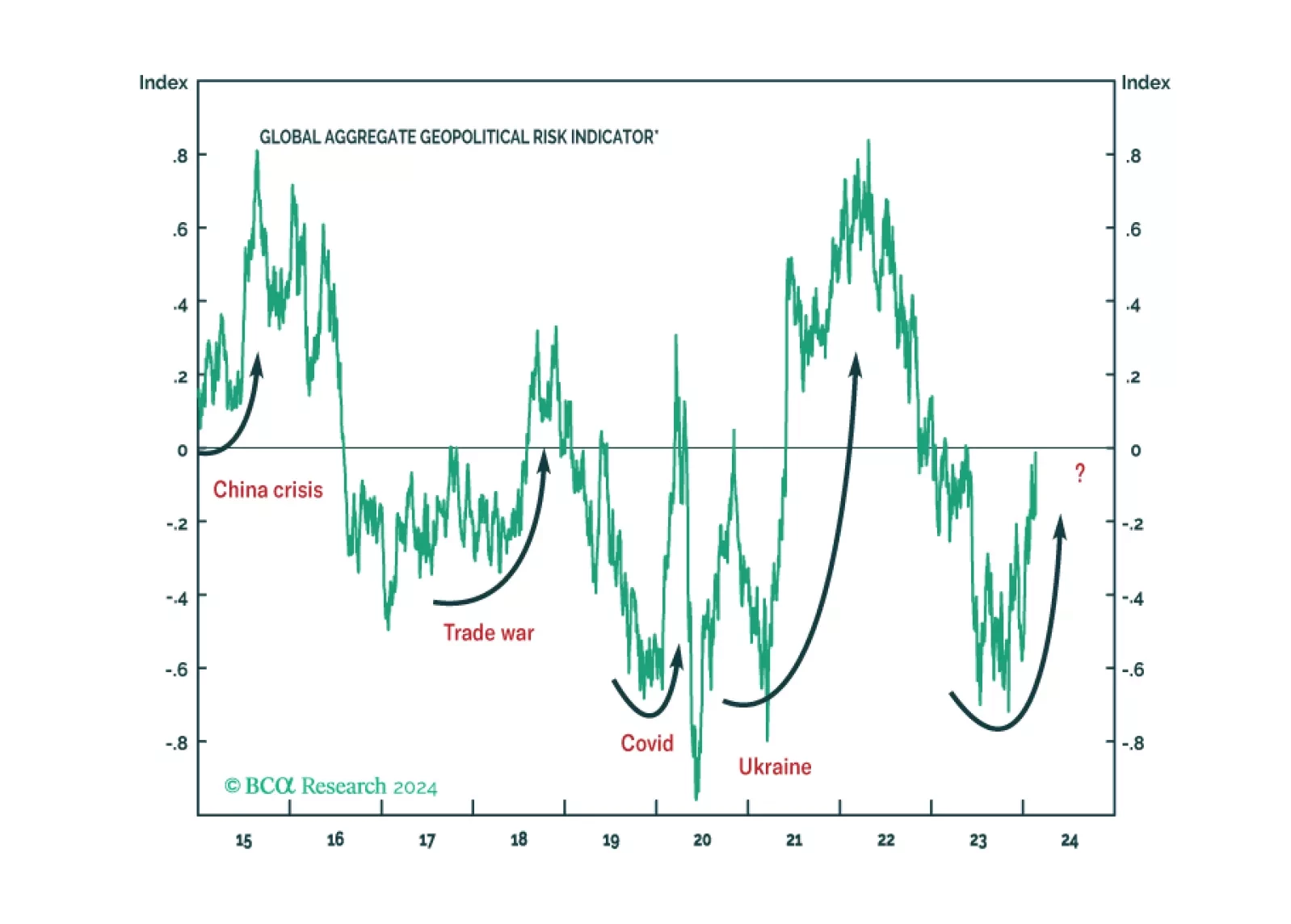

The Russian mutiny reveals the underlying trend of domestic instability. Russian instability is negative for global stability. The endgame of the war in Ukraine is exacerbating the problem, likely pushing up the equity risk premium.

Macro and geopolitical risks may spoil the narrow window for a stock market rally before recessionary trends rise to the fore.