Russia

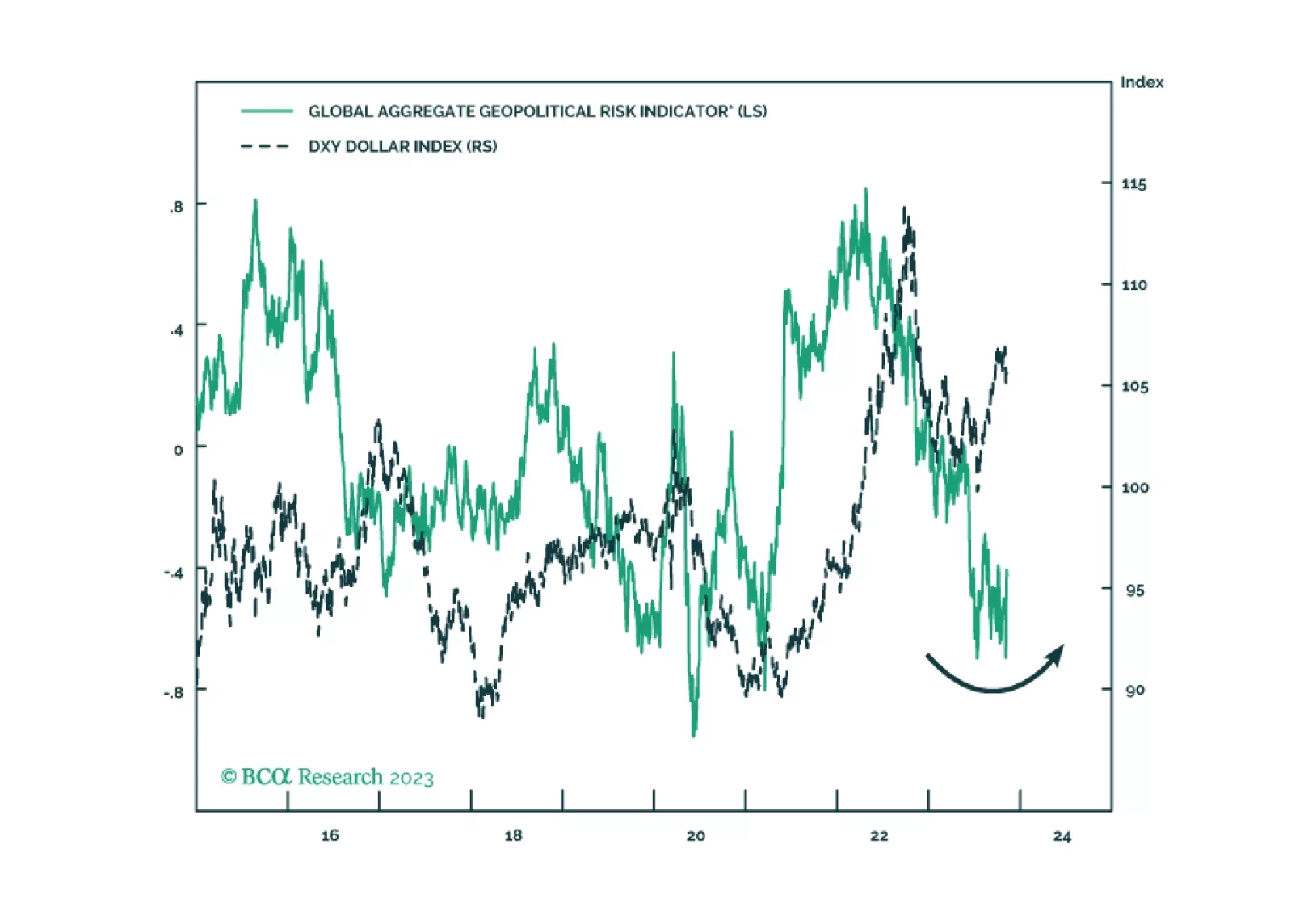

Amid a range of geopolitical narratives, what matters is that the US strategy of economic engagement with its rivals is failing, giving rise to a new strategy of containment that will reinforce the secular rise in geopolitical risk. Our market-based quantitative indicators of geopolitical risk are set to rise in the coming year.

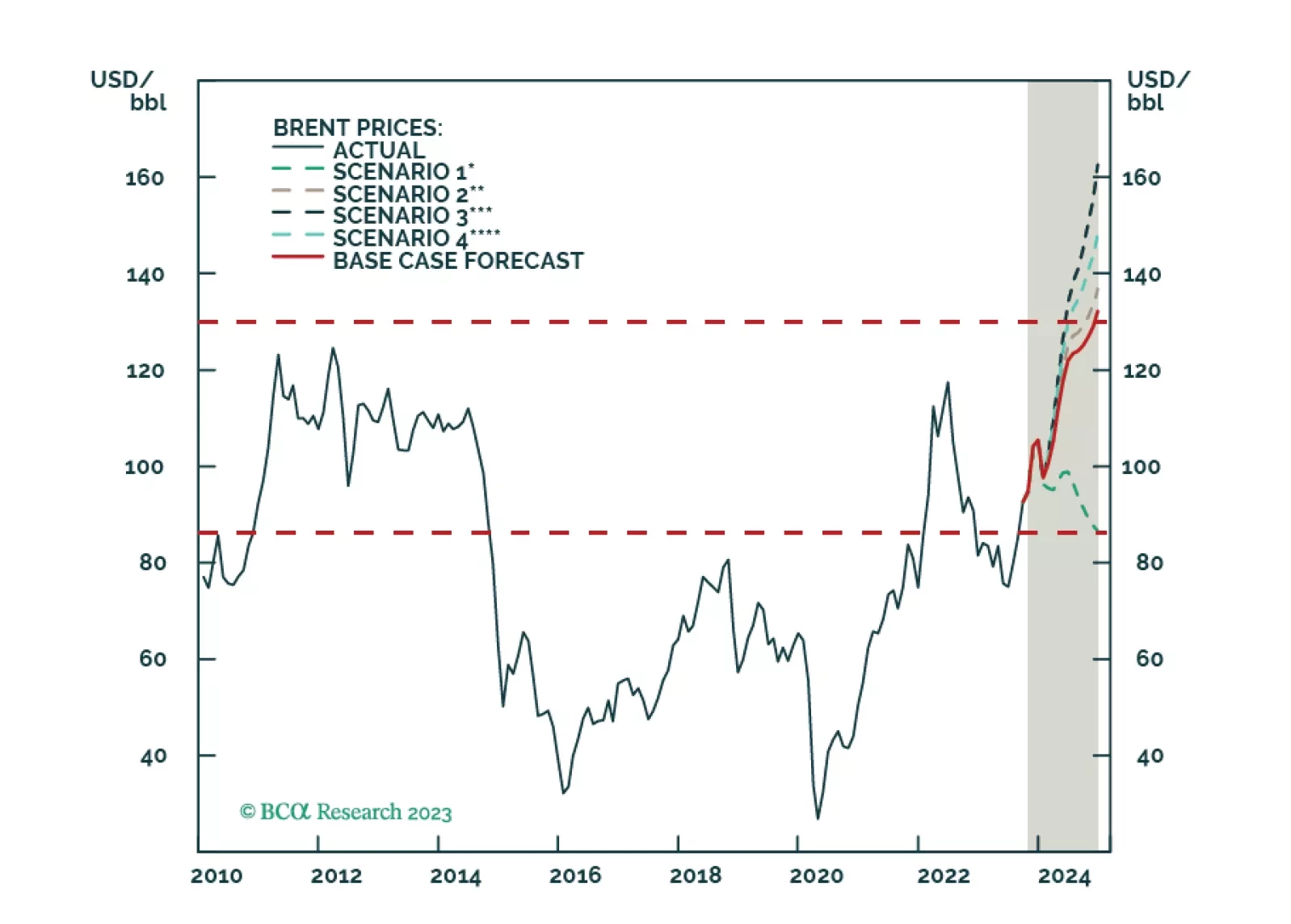

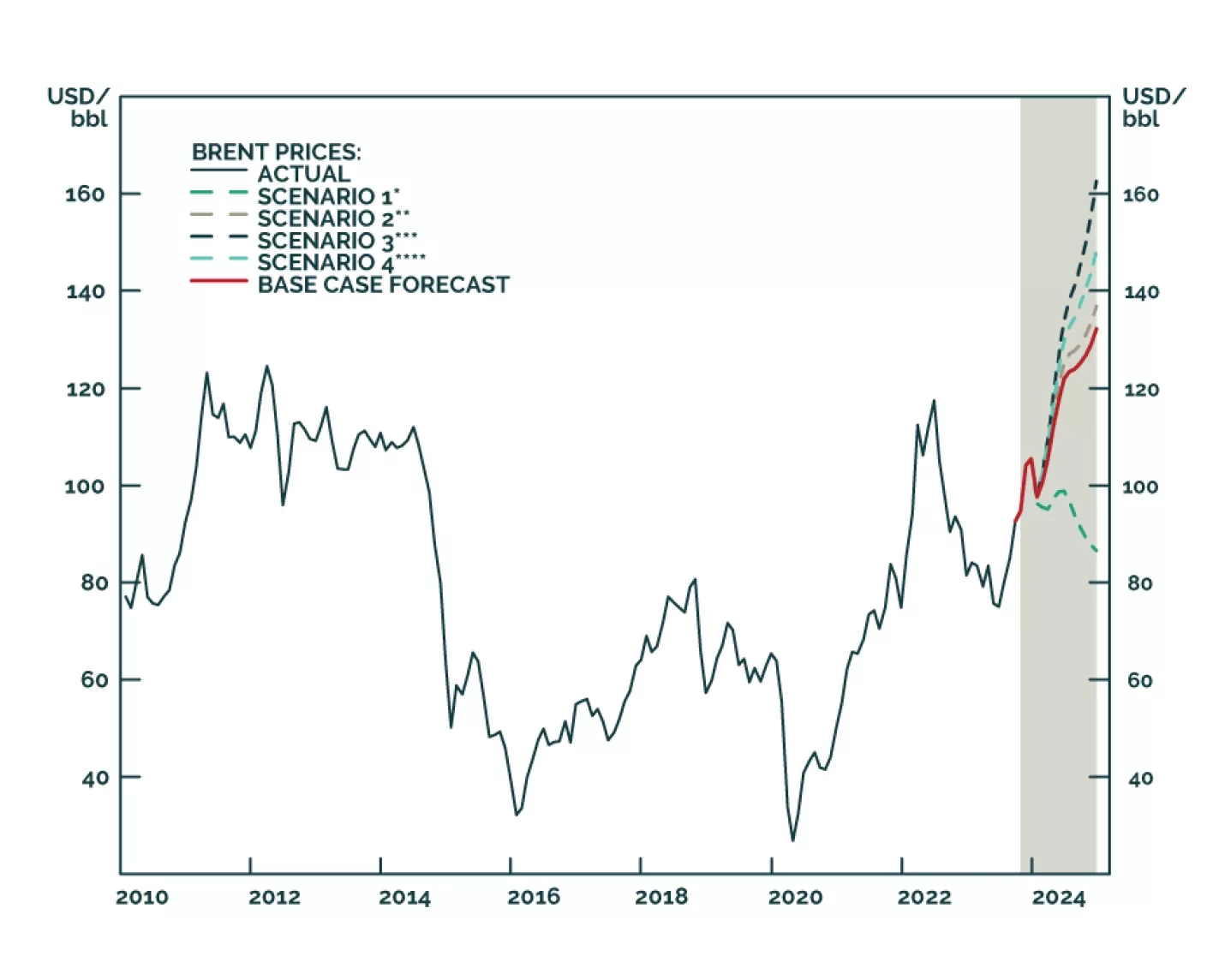

Economic fragmentation will accelerate in the wake of the Israel-Hamas and Russia-Ukraine wars. China’s fis-cal support for its economy; a still-strong US economy, and the preparation for a wider war in the Middle East involving Iran will elevate volatility and bias oil prices upward. We remain long equity and commodity exposure via the XOP, XME and COMT ETFs.

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.

The geopolitical backdrop remains negative despite some marginally less negative news. China’s stimulus is not yet large or fast enough to prevent a market riot. Two of our preferred equity regions, ASEAN and Europe, are struggling to outperform. Investors should stay defensive overall.

Investors should underweight global equities and risk assets; overweight US stocks relative to global; and overweight defensive sectors versus cyclicals.

China removed checks and balances in its political system to deal with a very dangerous economic transition. The transition is going badly, yet investors cannot rely on checks and balances to correct or prevent policy mistakes. The Taiwanese election is a looming bellwether.

The global economy will not enjoy an “immaculate disinflation” but will suffer a very maculate one due to China’s growth slowdown and restrictive monetary policy in the developed world. Investors should stay overweight low-beta assets.

The odds of Russia cutting oil output will rise going into 4Q23, as Ukraine’s endgame increases pressure on it, and it actively seeks to undermine President Biden’s re-election. We reckon a 2mm b/d cut would push Brent above $140/bbl by December 2024. This would push inflation and inflation expectations higher and raise the odds of more Fed rate hikes. BCA Commodity & Energy Strategy will remain long the COMT and XOP ETFs. At tonight’s close, we will be getting long December 2024 $100/bbl Brent calls.

Global oil demand growth is tracking with our estimate of ~ 1.8mm b/d for this year. Supply discipline is being maintained by OPEC 2.0, where the core (KSA and the UAE) and Russia have reduced production by ~ 240k b/d yoy in 1H23. In addition, KSA extended its unilateral production cut of 1mm b/d from July into August. We expect inventory draws in 2H23 as supply stays below demand. Our Brent forecast remains unchanged at $92/bbl this year, and $120/bbl next year. We remain long the COMT and XOP ETFs.