Regulation

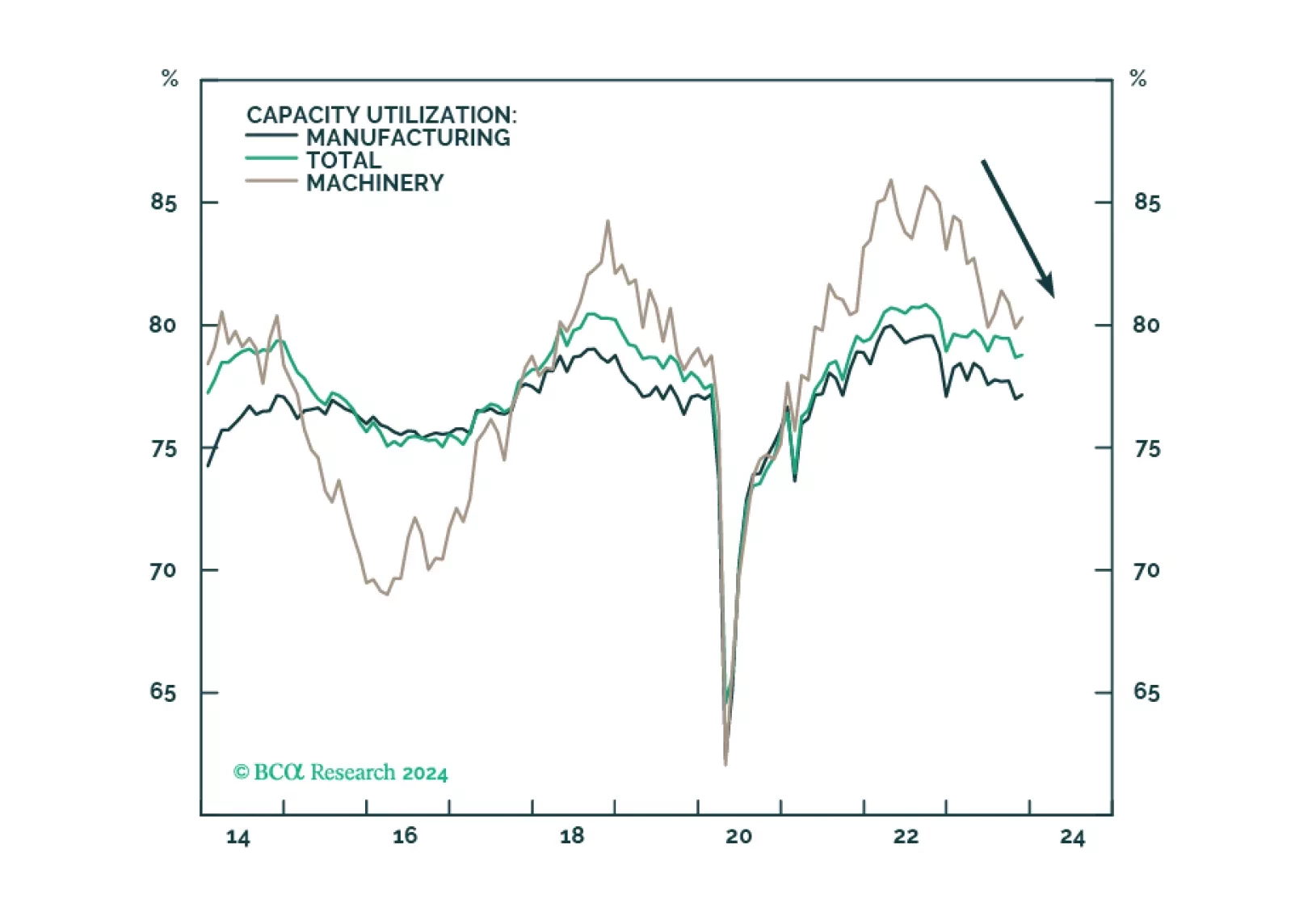

The US manufacturing renaissance, spurred on by reshoring, automation, and government spending, is running its course but progress has slowed on the back of tight monetary conditions and the manufacturing recession. The deceleration of these positive trends weighs on the outlook for the Capital Goods industry group, impeding its performance over the short term. However, we reiterate that positive long-term trends for the industry remain intact. We downgrade Capital Goods to a tactical underweight. It remains a strategic overweight.

The expectation that China is best placed to win the global EV race presumes the persistence of the status quo. Reality, however, may differ as the sector looks set to be hit by a range of changes. If nonlinearity were to emerge in the global auto sector, as it often does, then the EV transition could end up spawning a very unexpected list of winners and losers.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

Global instability will continue in 2024 – whatever happens afterward. Slowing economies will exacerbate already high geopolitical risk and policy uncertainty stemming from the US election and foreign challenges to US leadership. Overweight government bonds, defensive sectors, the Americas versus other regions, aerospace/defense stocks, and cyber-security stocks.

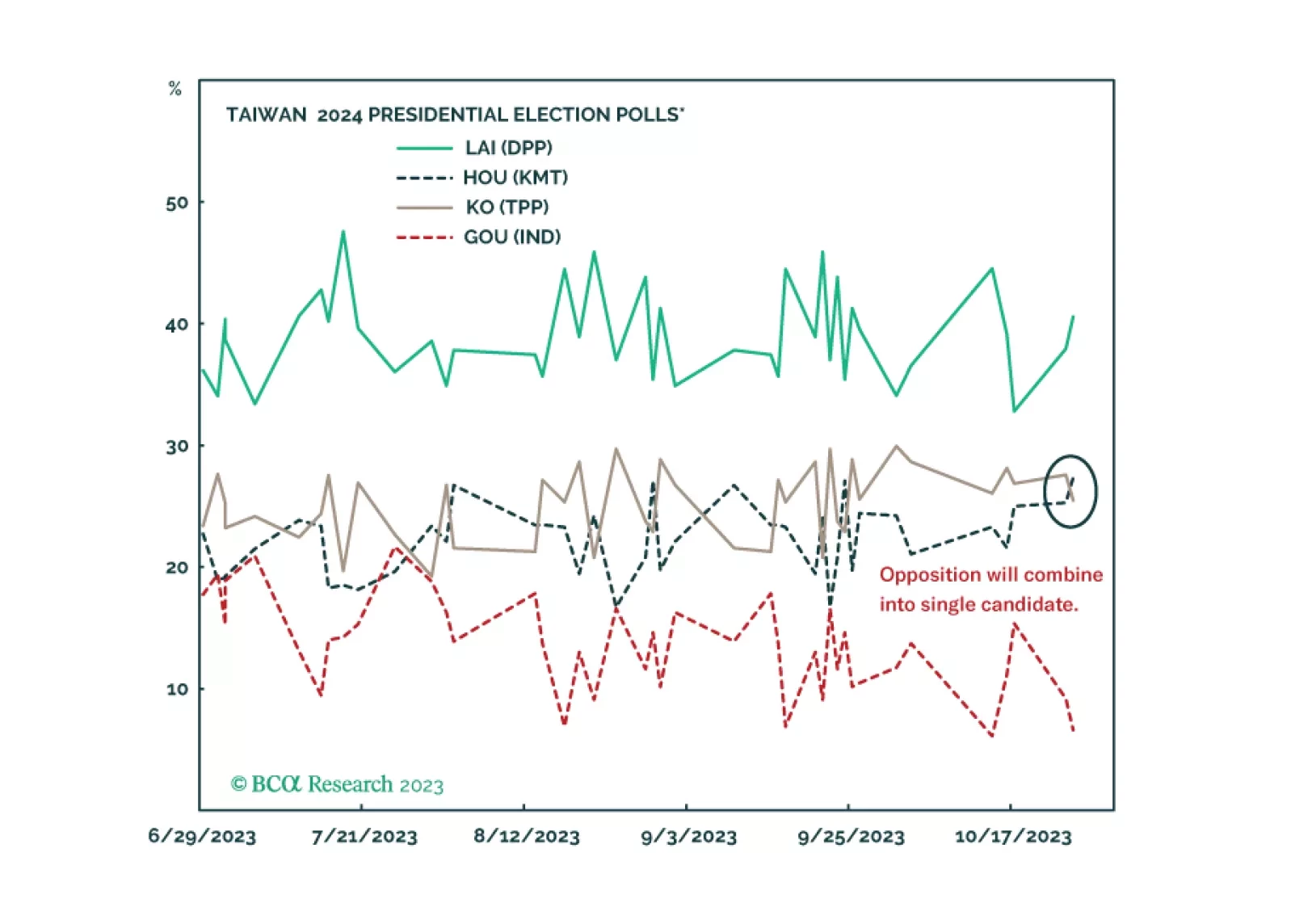

Investors should not get their hopes up about the Biden-Xi summit. Wait to see if a new ruling party is elected in Taiwan before downgrading geopolitical risk in the Taiwan Strait. US-China strategic détente is possible but neither the geopolitics nor the macro backdrop warrant a risk-on position next year.

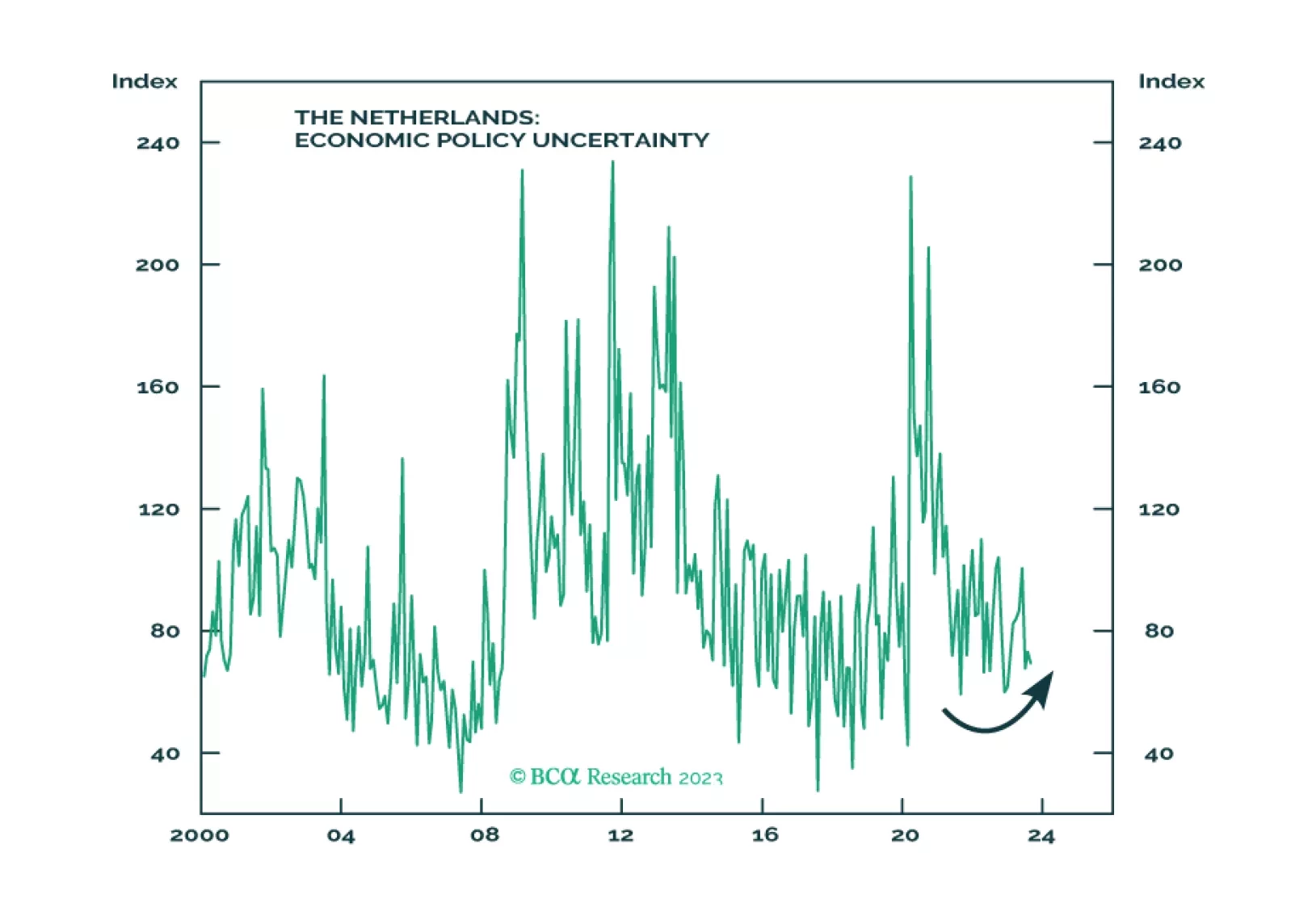

The Netherlands has a healthier and more stable economy and demography than its European peers. Investors should stay overweight developed European equities, including Dutch equities, relative to emerging European equities.

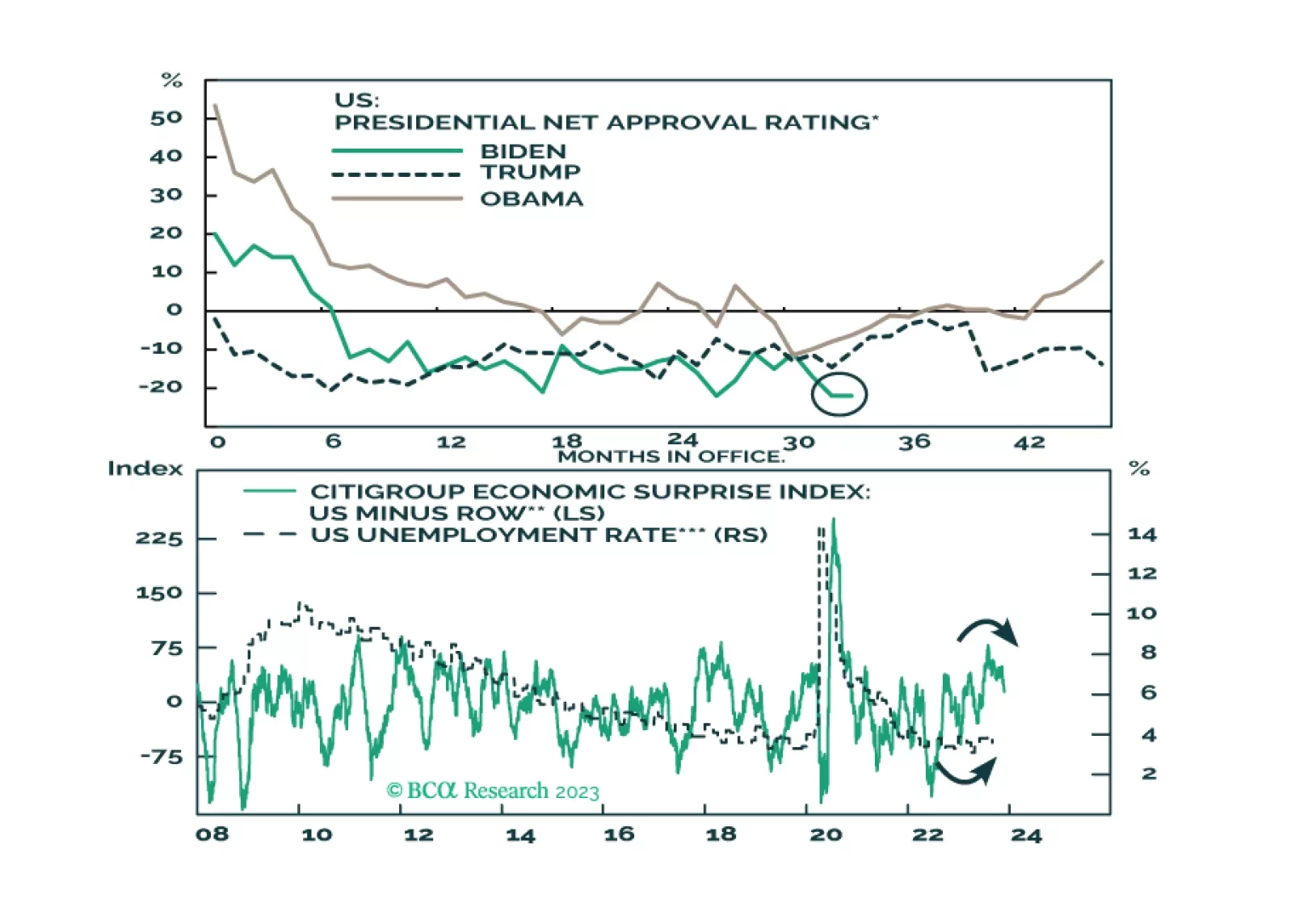

There is a connection between the bond market meltdown and Republican Party’s meltdown. Investors should expect more short-term financial market volatility as a result of the triple whammy of high bond yields, high oil prices, and a strong dollar.

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.