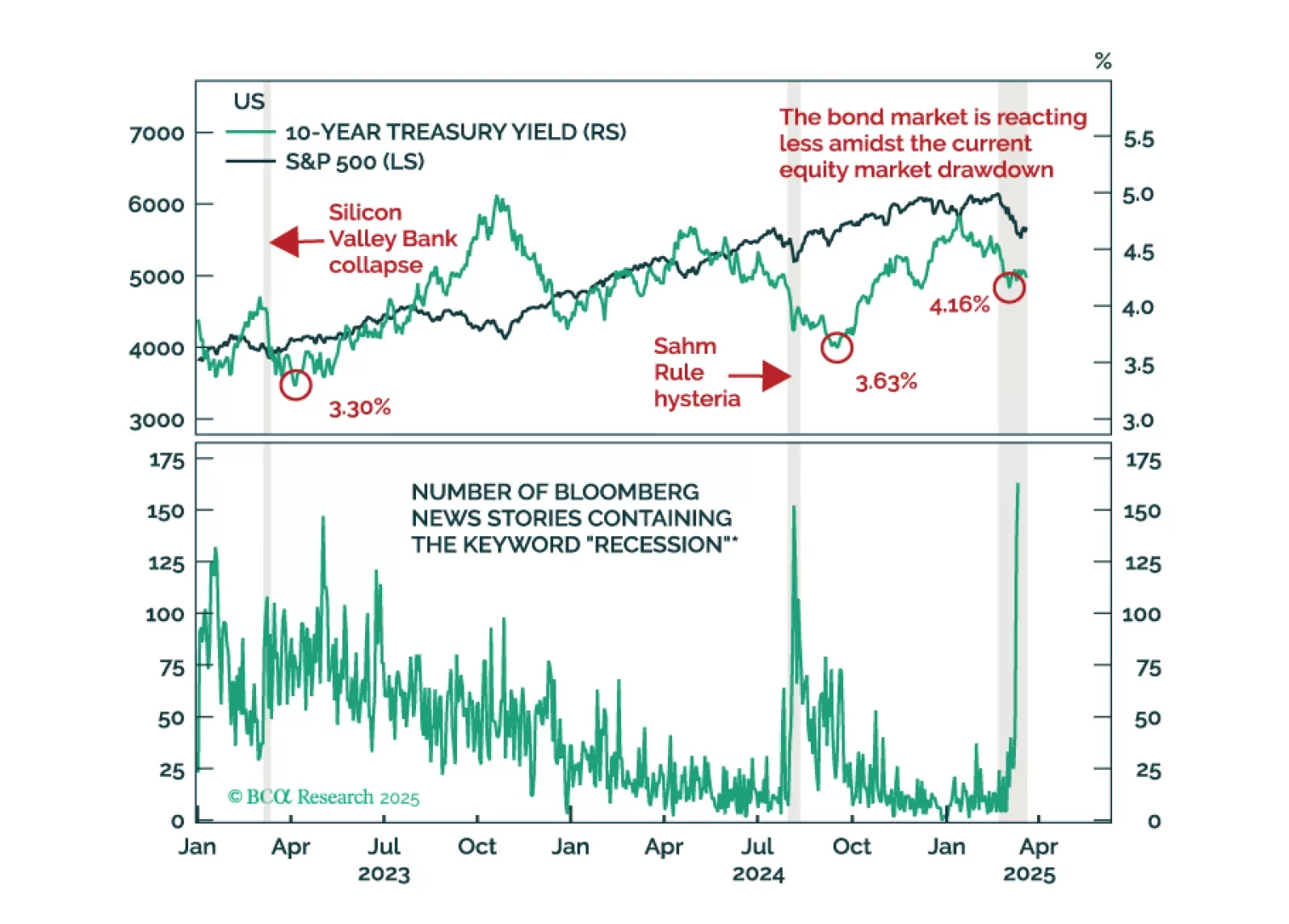

Recession-Hard/Soft Landing

This morning’s weak consumer spending and strong inflation data reinforce our sense that the US economy is heading toward recession.

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

In this Second Quarter Strategy Outlook, we explore the major trends that are set to drive financial markets for the rest of 2025 and beyond.

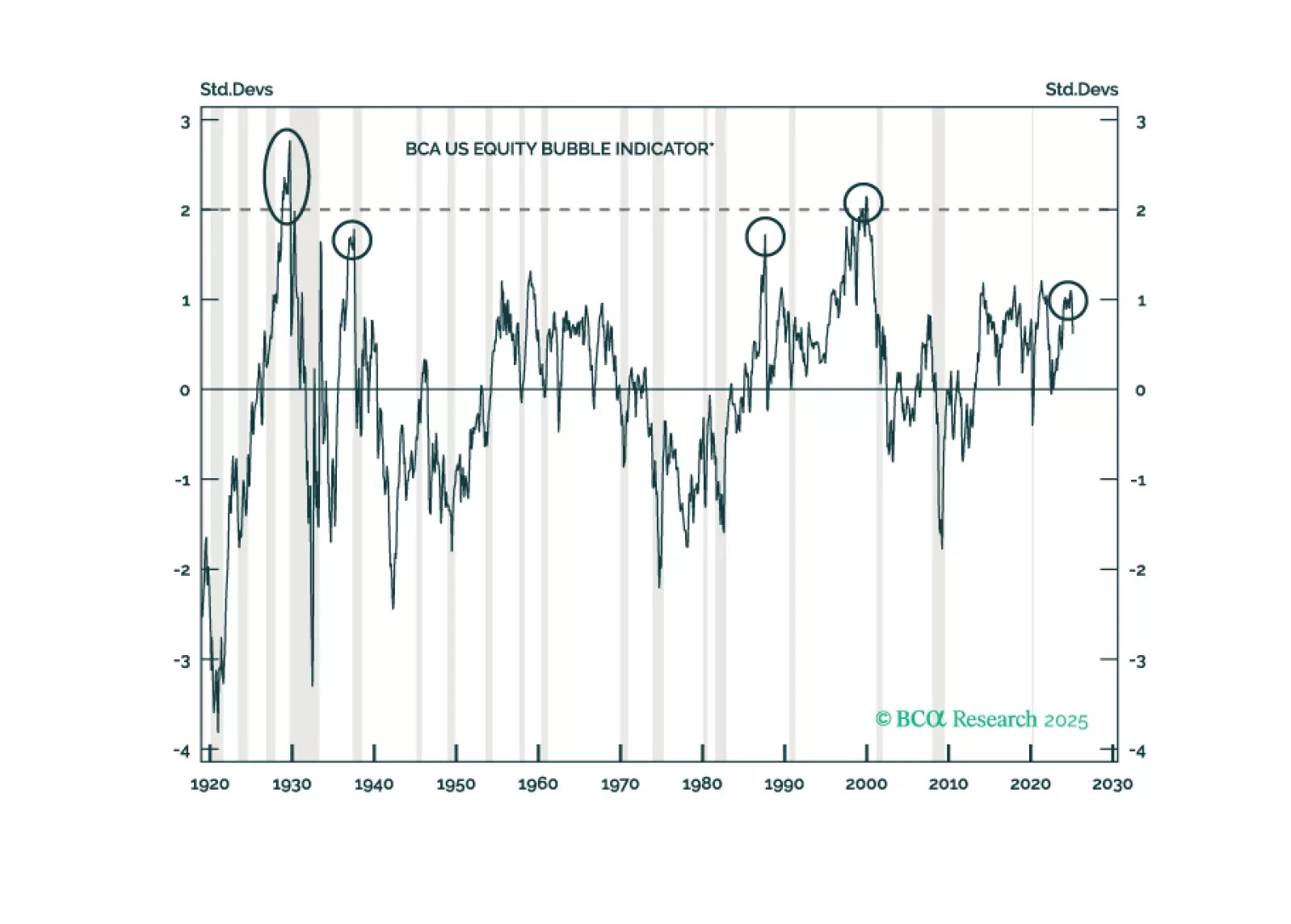

In Section II, Jonathan presents a new indicator that investors can use to track the odds of bubble formation in real time and shows how it fits into a larger framework that accurately explains US bear market severity over the past century. The US equity market is not in a bubble today, but it is meaningfully overvalued. Investors should expect a relatively severe cumulative loss from equities in a recession scenario.

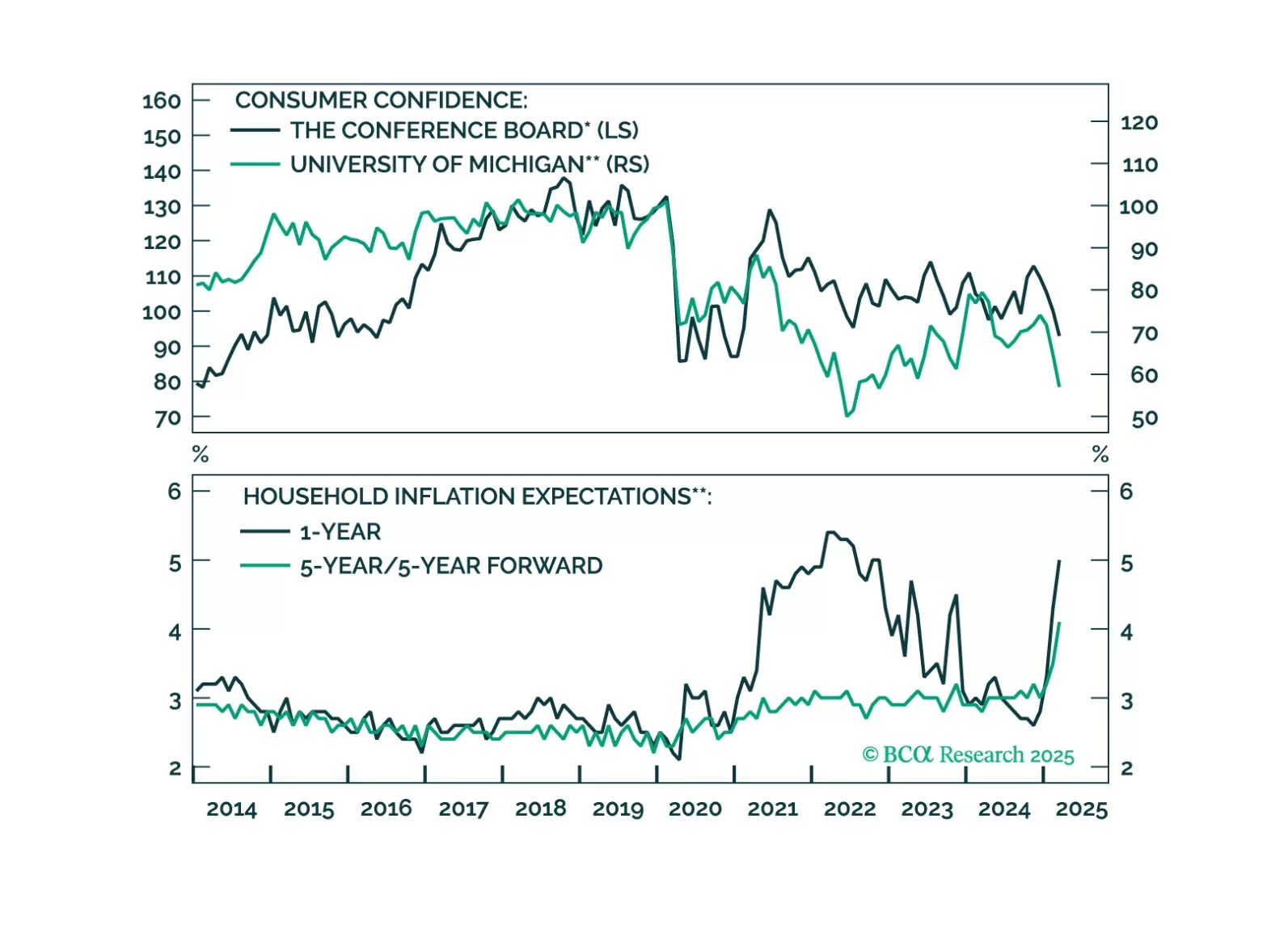

In Section I, Doug notes that weak US consumer sentiment is beginning to manifest. A wide sweep of consumer-facing companies have lowered guidance, and monoline credit card lenders shed nearly 20% over just three weeks across late February and early March. If the US enters a recession sometime this year as we expect, it will likely lead to a global recession and a global equity bear market. Investors should remain defensively positioned. In Section II, Jonathan presents a new indicator that investors can use to track the odds of bubble formation in real time and shows how it fits into a larger framework that accurately explains US bear market severity over the past century. The US equity market is not in a bubble today, but it is meaningfully overvalued. Investors should expect a relatively severe cumulative loss from equities in a recession scenario.

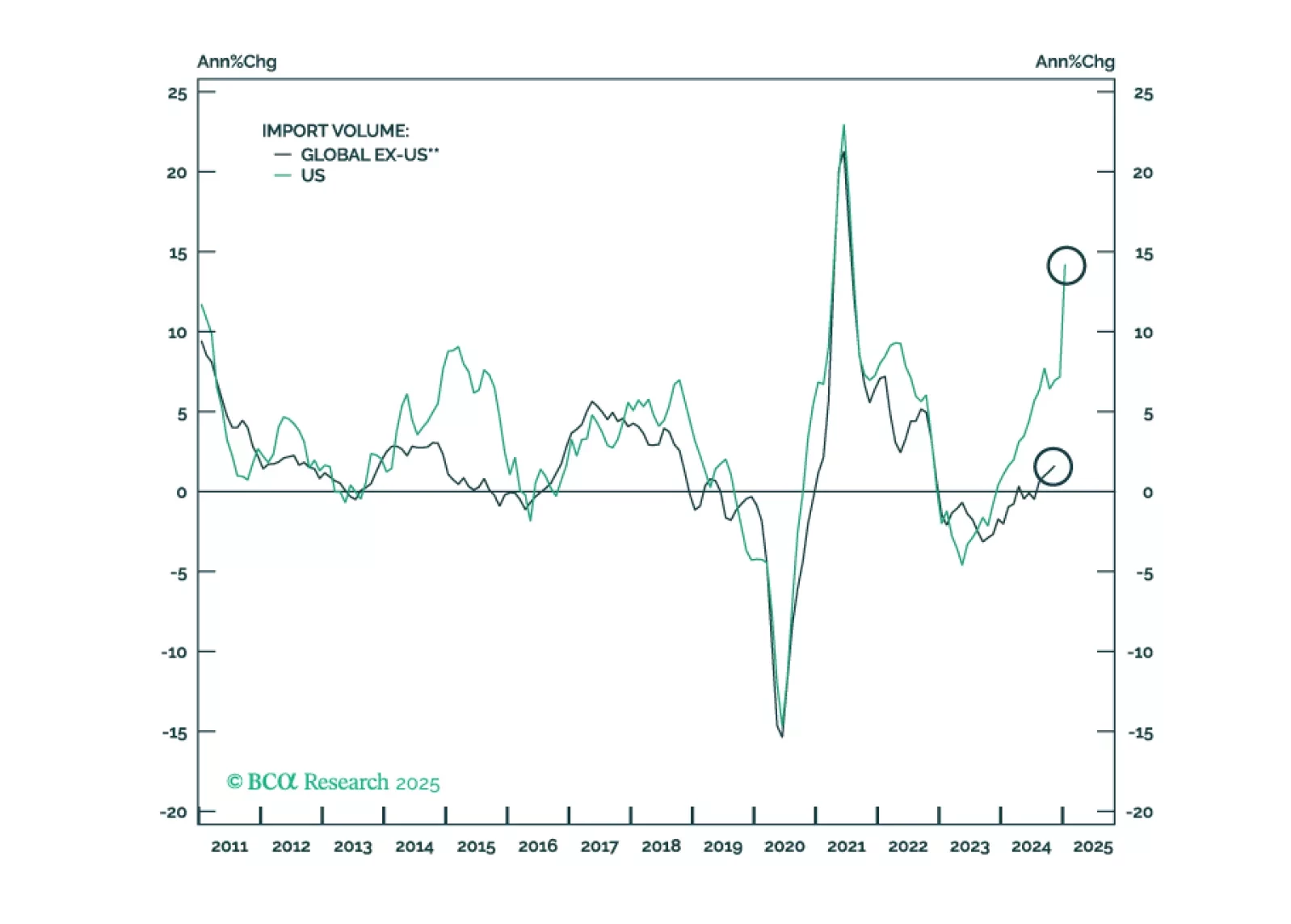

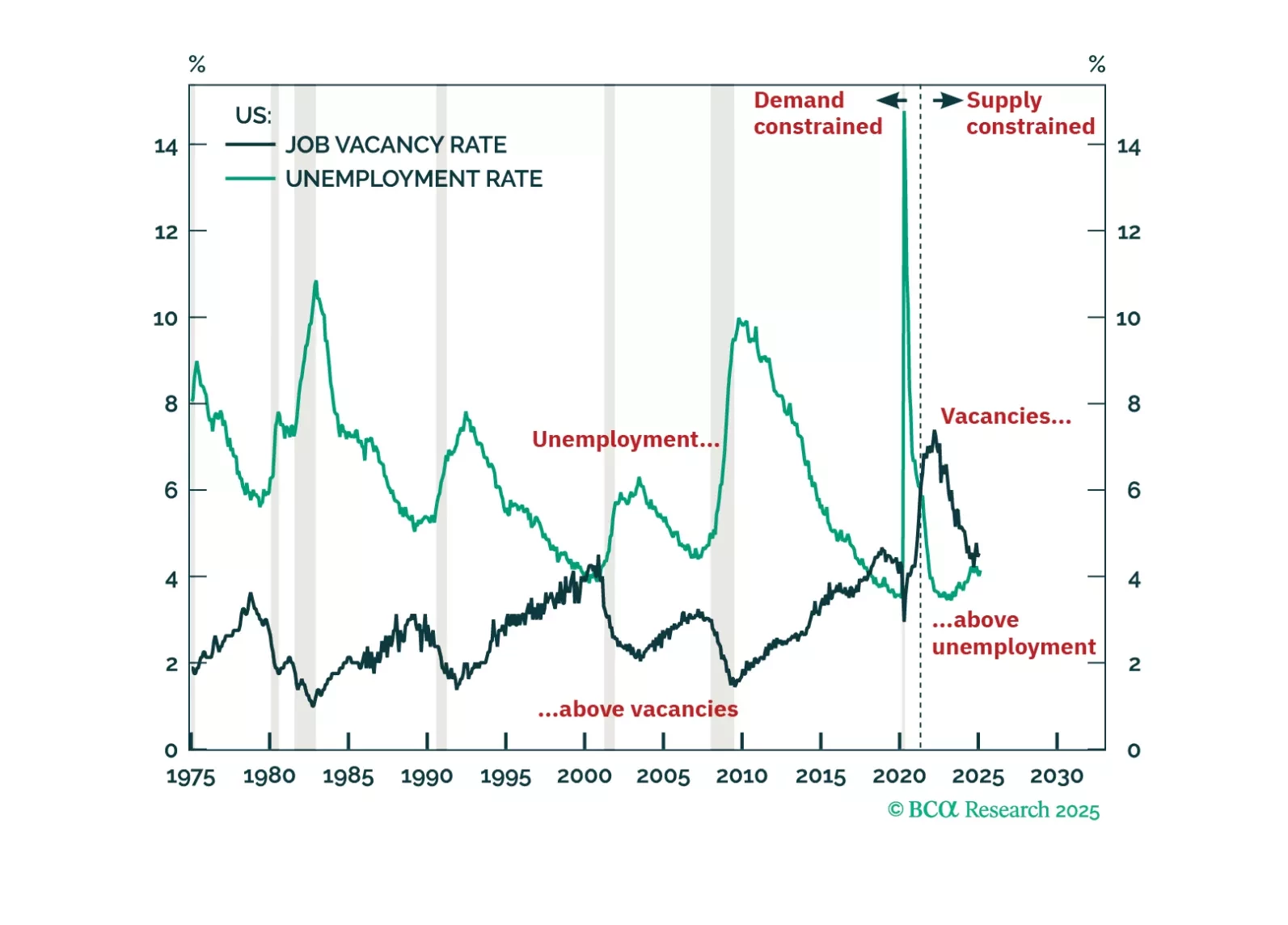

The US economy has never entered a demand-driven recession without labour demand running below labour supply and without the job vacancy rate running below the unemployment rate. Right now though, US labour demand is still running 1.7 million workers above labour supply, and the job vacancy rate is running comfortably above the unemployment rate. This suggests that the labour market is still supply-constrained, and that a demand-driven recession is not imminent. We discuss the investment implications. Plus, more about our ‘trade of the century’: long cotton versus coffee.

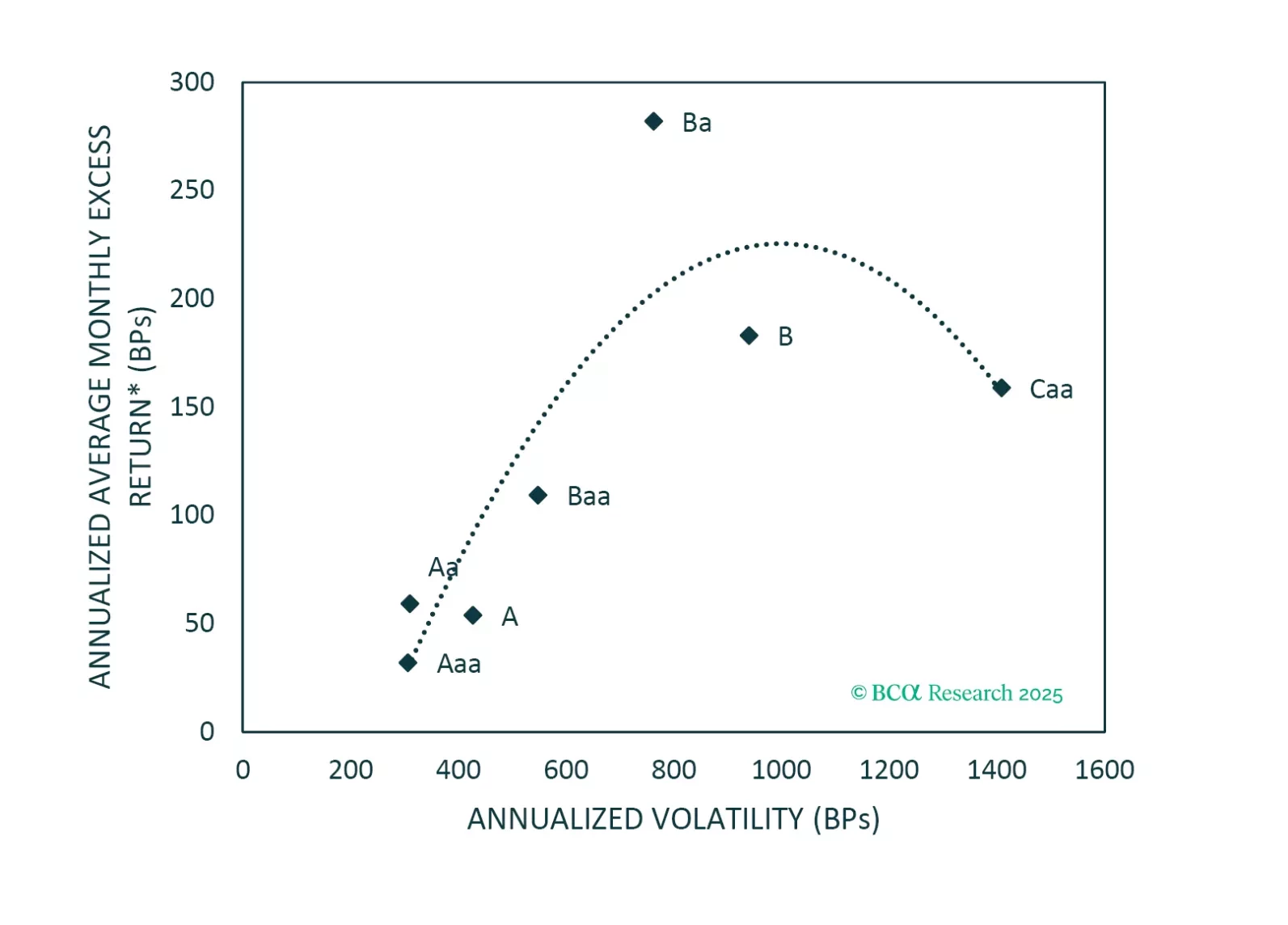

An analysis of historical data shows that Ba-rated bonds outperform other corporate credit tiers in the long-run on a risk-adjusted basis. That said, today’s fragile macro environment warrants a more cautious allocation.

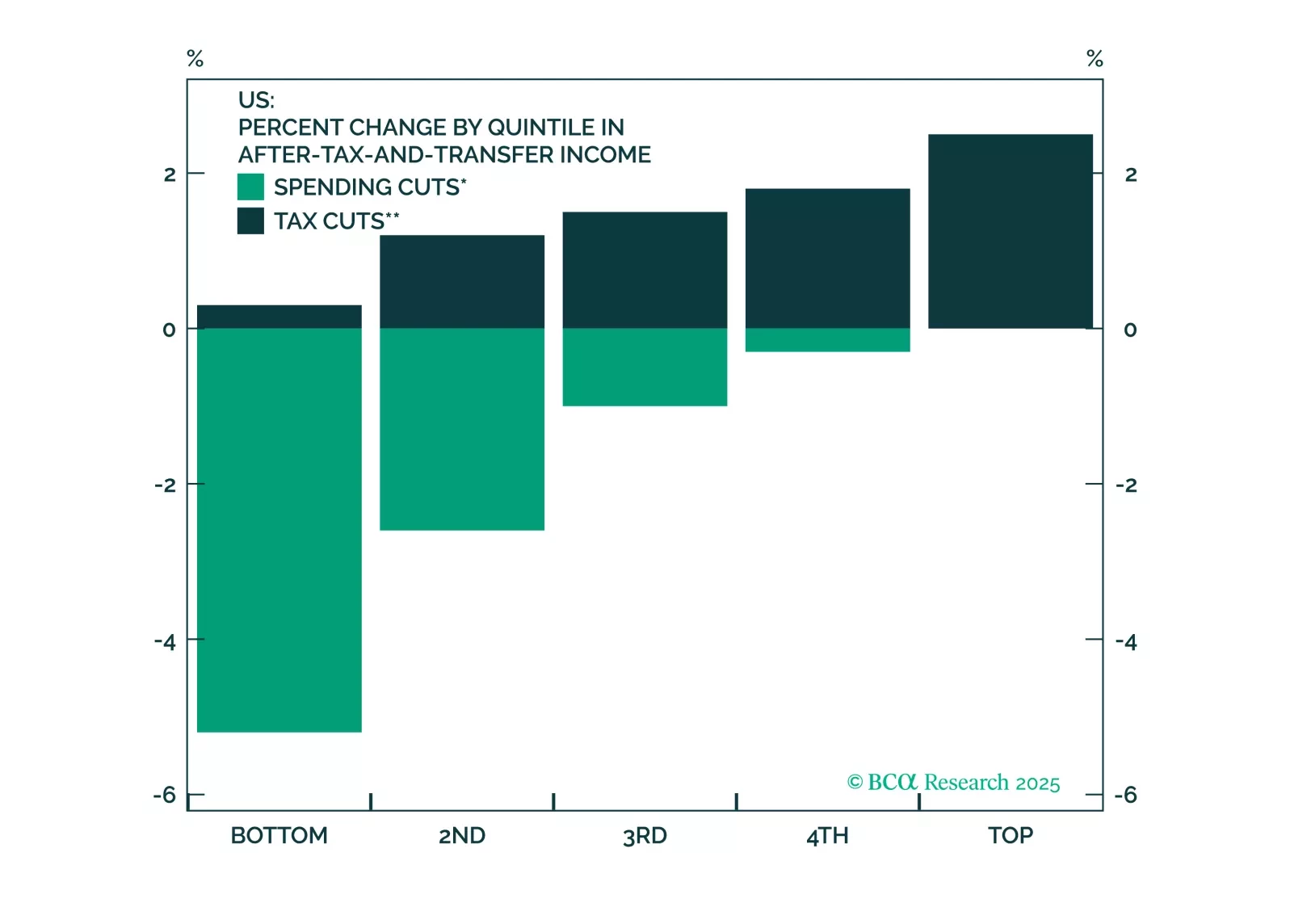

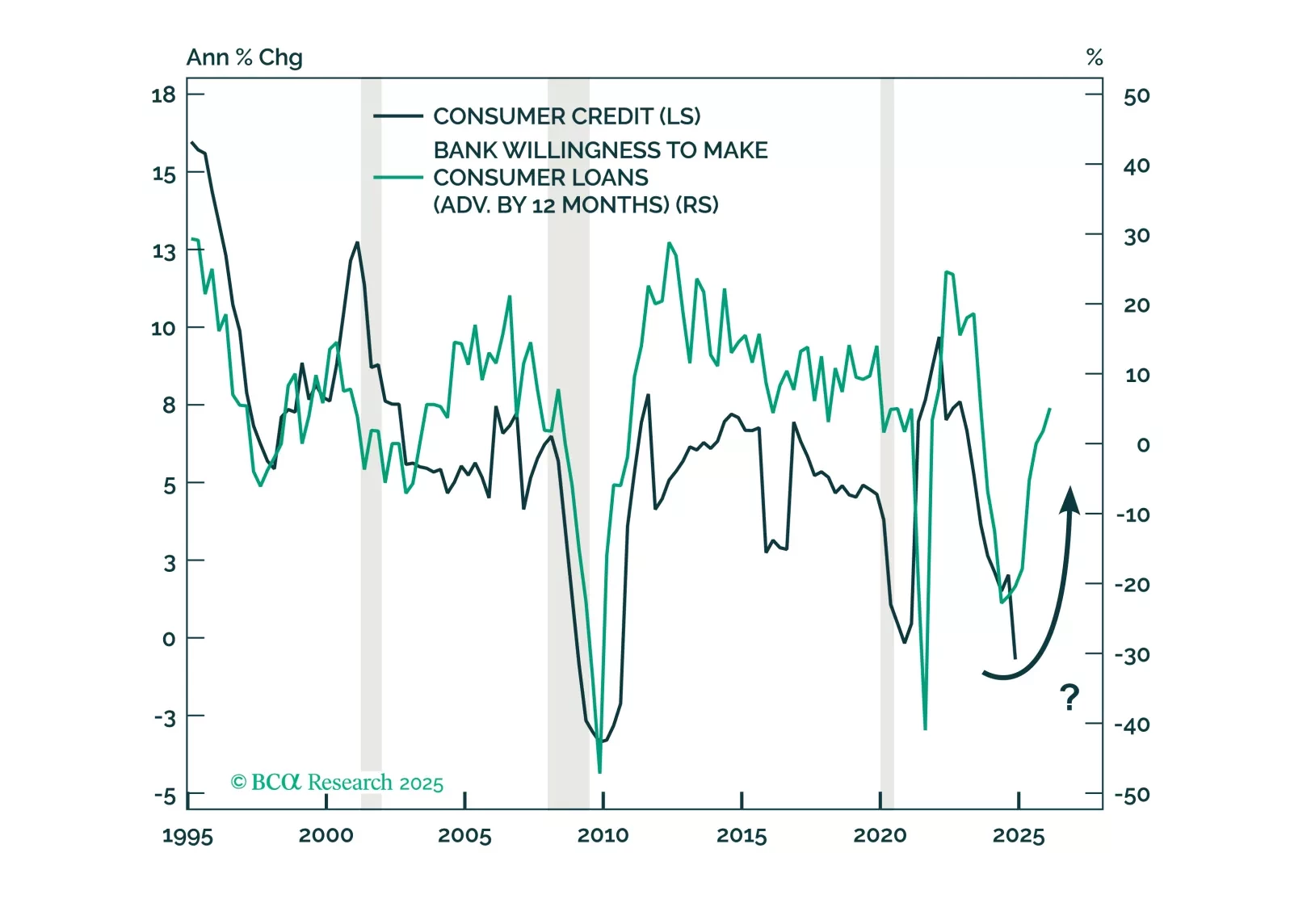

Households’ healthy balance sheets do not square with the rise in credit cards and auto loans delinquencies. The tailwinds that have supported higher-income cohorts’ spending have faded, presaging broad-based deterioration in credit performance.

In this Special Report, GeoMacro Strategist Marko Papic argues that the Trump administration is flirting with high risk / low reward. Triggering a recession may be the end goal of the White House, but borrowing costs are not declining as much as they ought to be while President Trump’s political capital is on thin ice. Most recessions are caused by a “murder weapon.” It is rare that this weapon can be holstered. This may be one of those times.

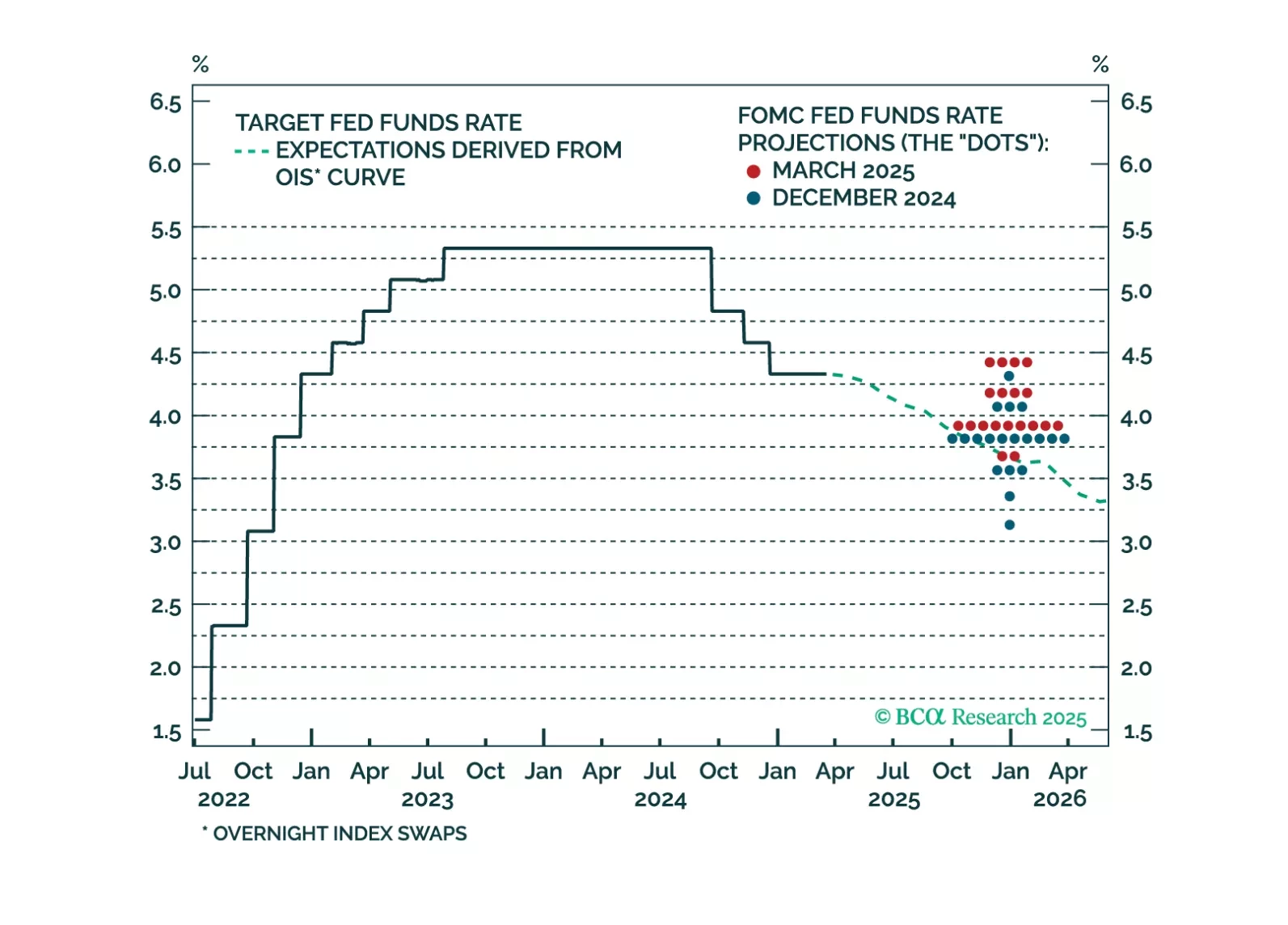

The market reaction to this afternoon’s Fed meeting looks overdone. Investors could be in for a hawkish surprise when it becomes apparent that the Fed won’t ease policy into higher tariff-driven inflation prints.