Recession-Hard/Soft Landing

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

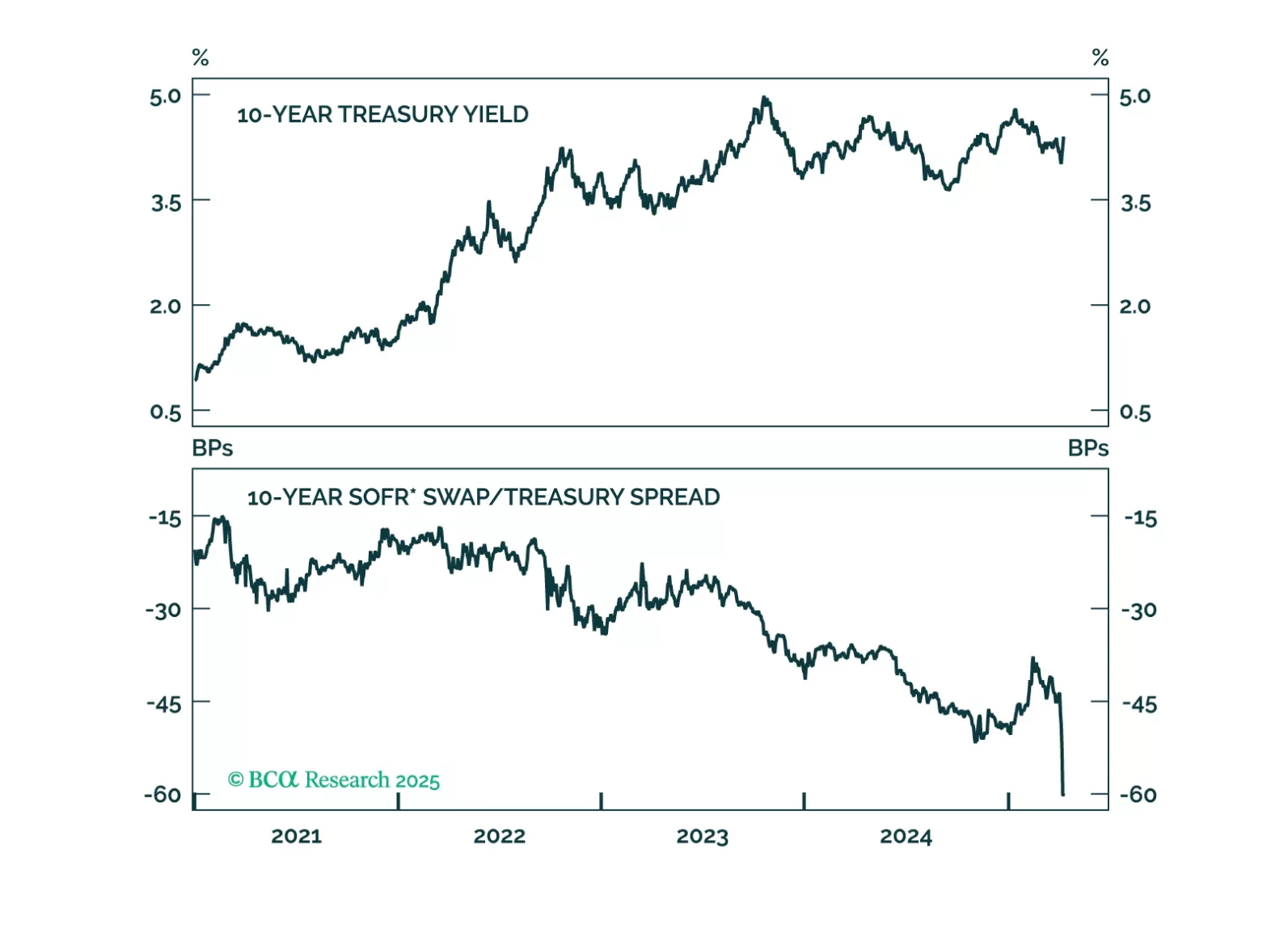

US Treasuries typically outperform both equities and global government bonds during downturns. Recent political shifts could lessen that outperformance this cycle, but we doubt it will disappear completely.

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.

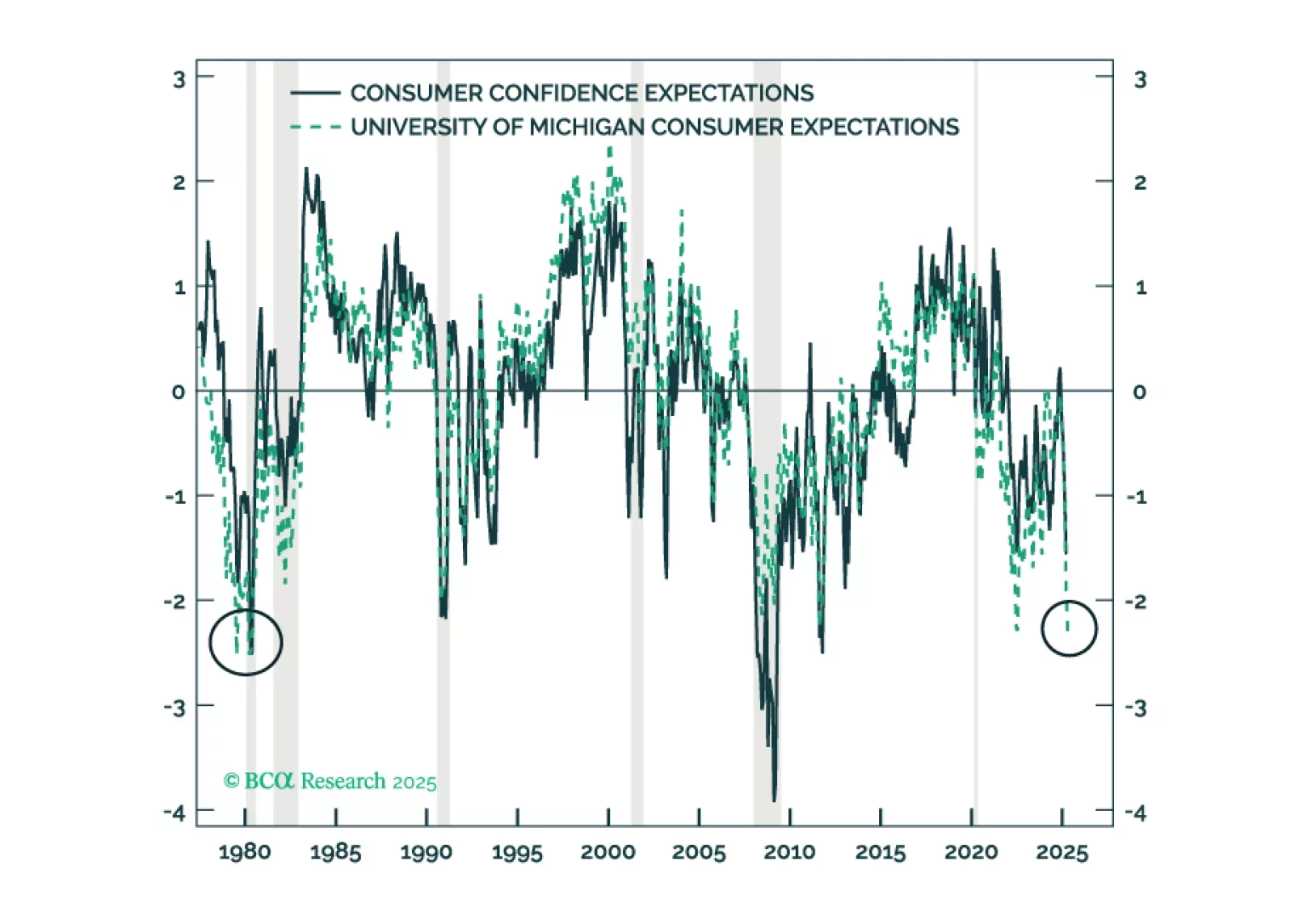

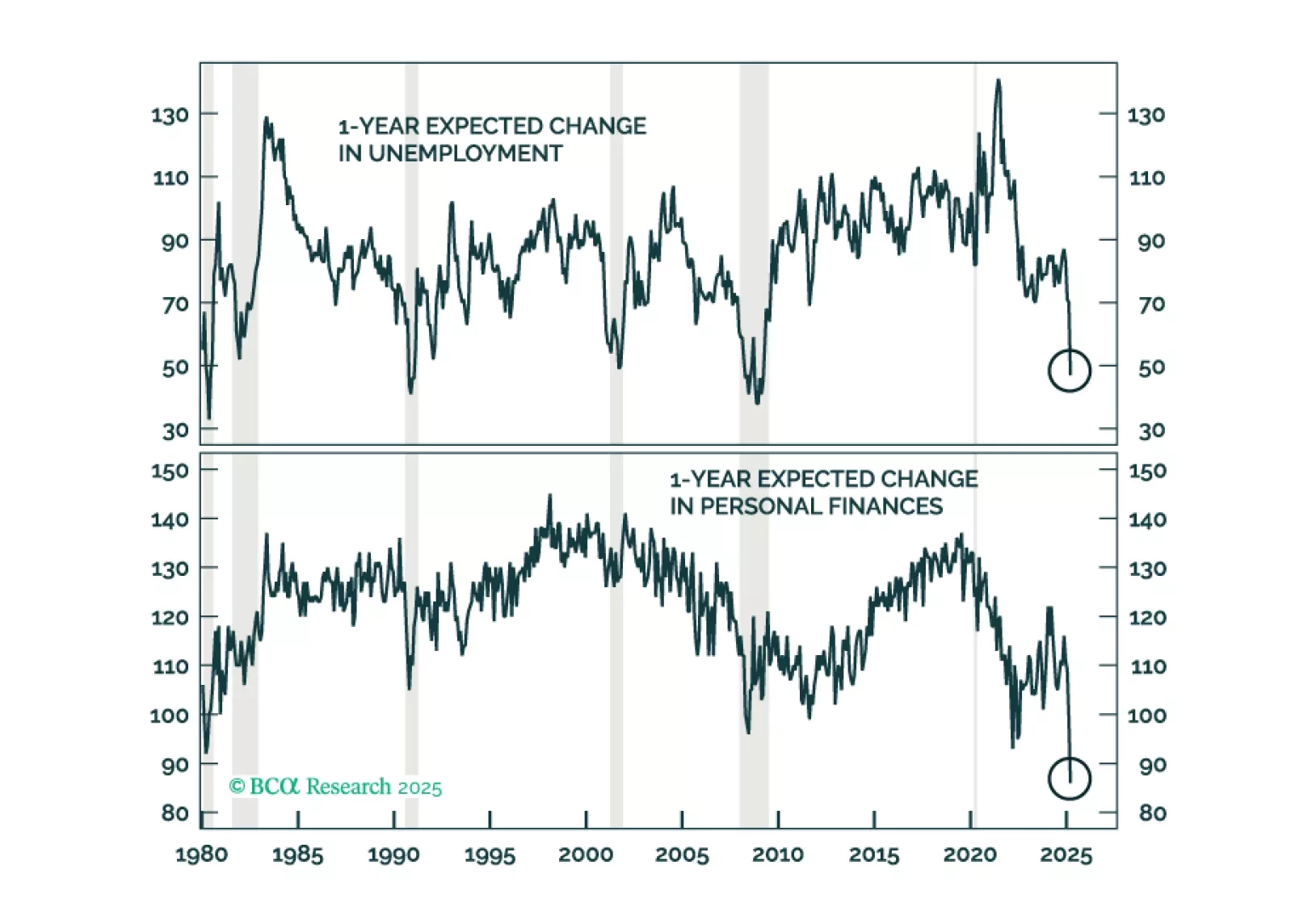

The policy-induced decline in consumer confidence has spread to businesses and investors, increasing the probability of a recession even if the administration reverses field on its aggressive tariff measures. We reiterate our defensive asset allocation recommendations.

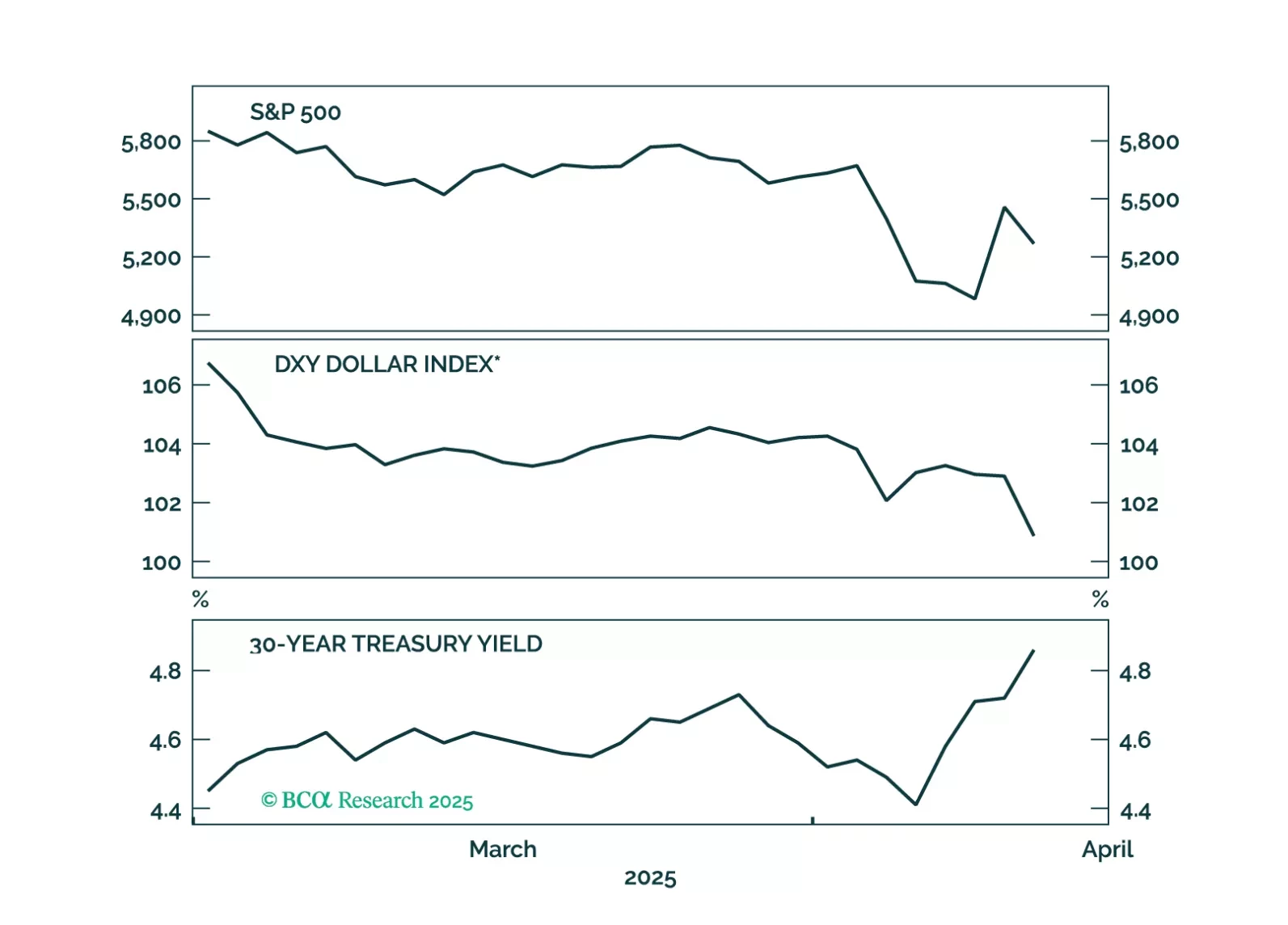

The combination of dollar weakness and rising US yields suggests global investors are questioning the safe-haven status of US Treasuries.

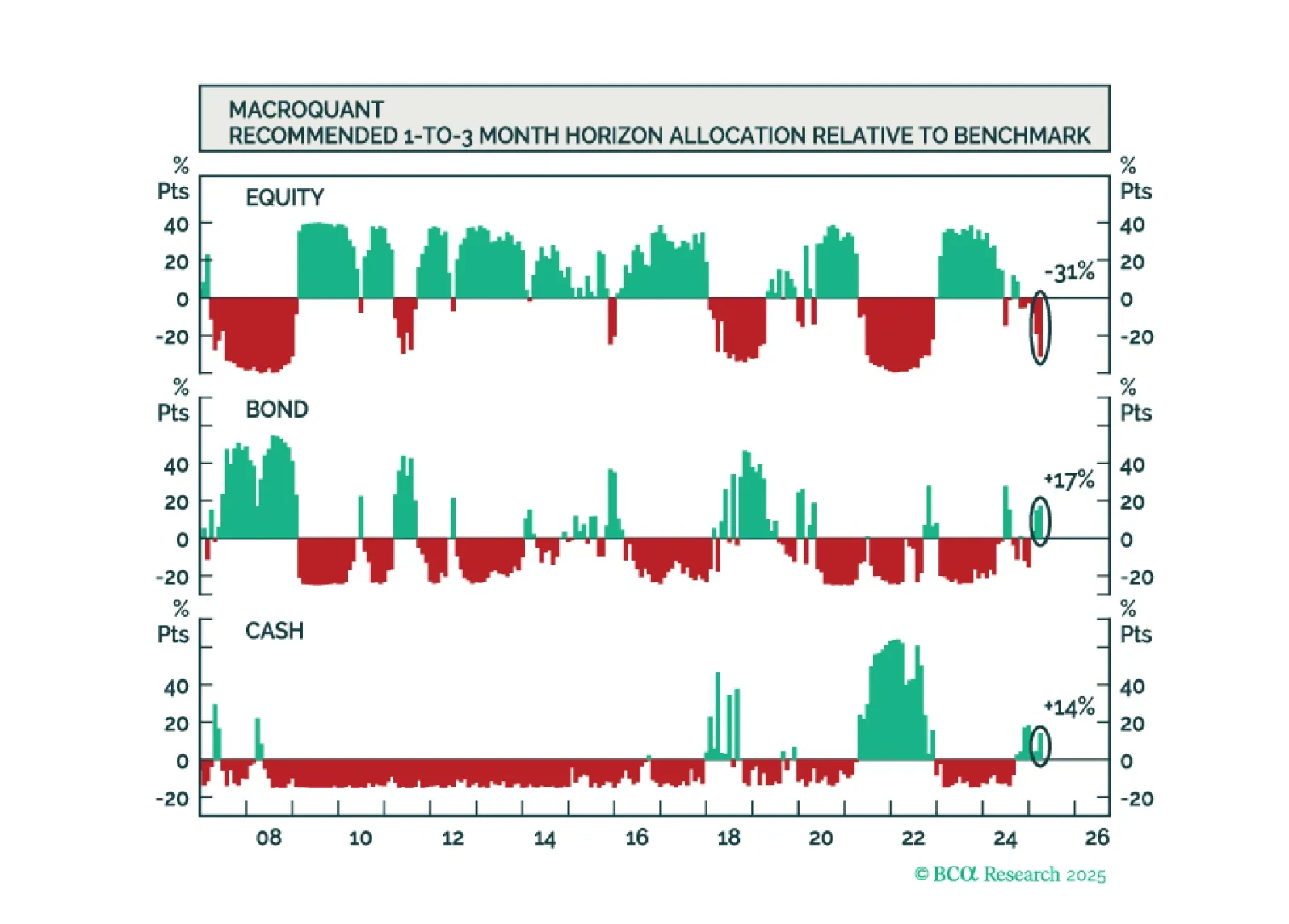

Our Portfolio Allocation Summary for April 2025.

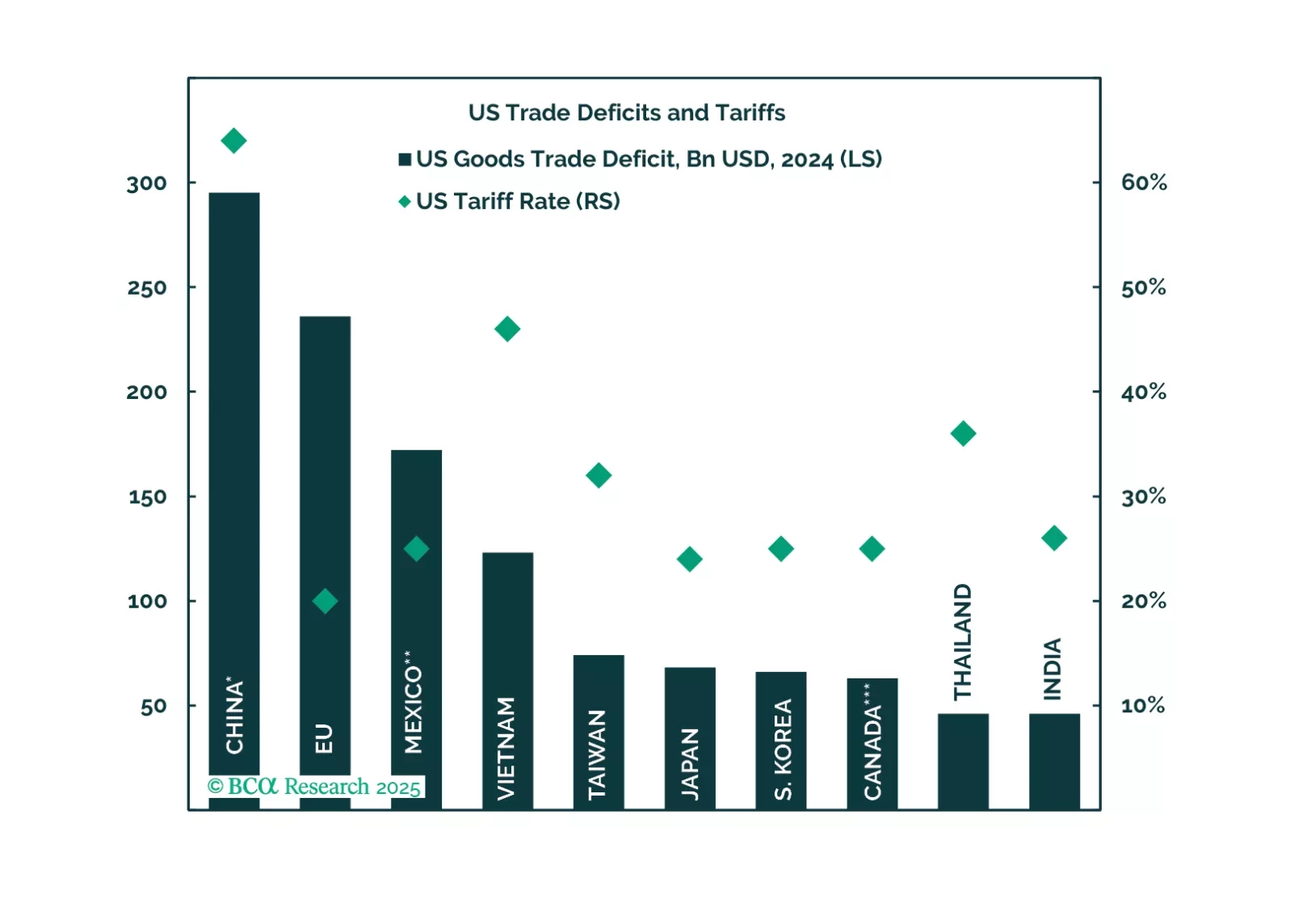

President Trump imposed tariffs on the world in his first 100 days, as we expected. Tariffs may have catalyzed a recession in the US, given the weakness in consumer sentiment and demand. Trump will soon backpedal and grant exemptions to countries that are negotiating, which he will showcase as proofs of his successful trade policy. While he may backpedal on his tariffs on other countries, China is not likely to receive the same treatment due to the US-China strategic competition.

The stimulus measures driving the post-COVID expansion were beginning to wane after five years and pointing the economy in the direction of an organically occurring recession. Now that DOGE and the multi-front trade war have sped up the timetable, we reiterate our risk-off recommendations.

The March employment report showed strong job growth, but the labor market remains in a fragile state and the demand shock from tariffs could be the catalyst that tips it over the edge into recession.

Trump's Tariff D-Day brings a negative surprise to financial markets already anxious over a declining US cyclical economy. Investors should sell risky assets, increase safe havens, and overweight US assets in the near term.