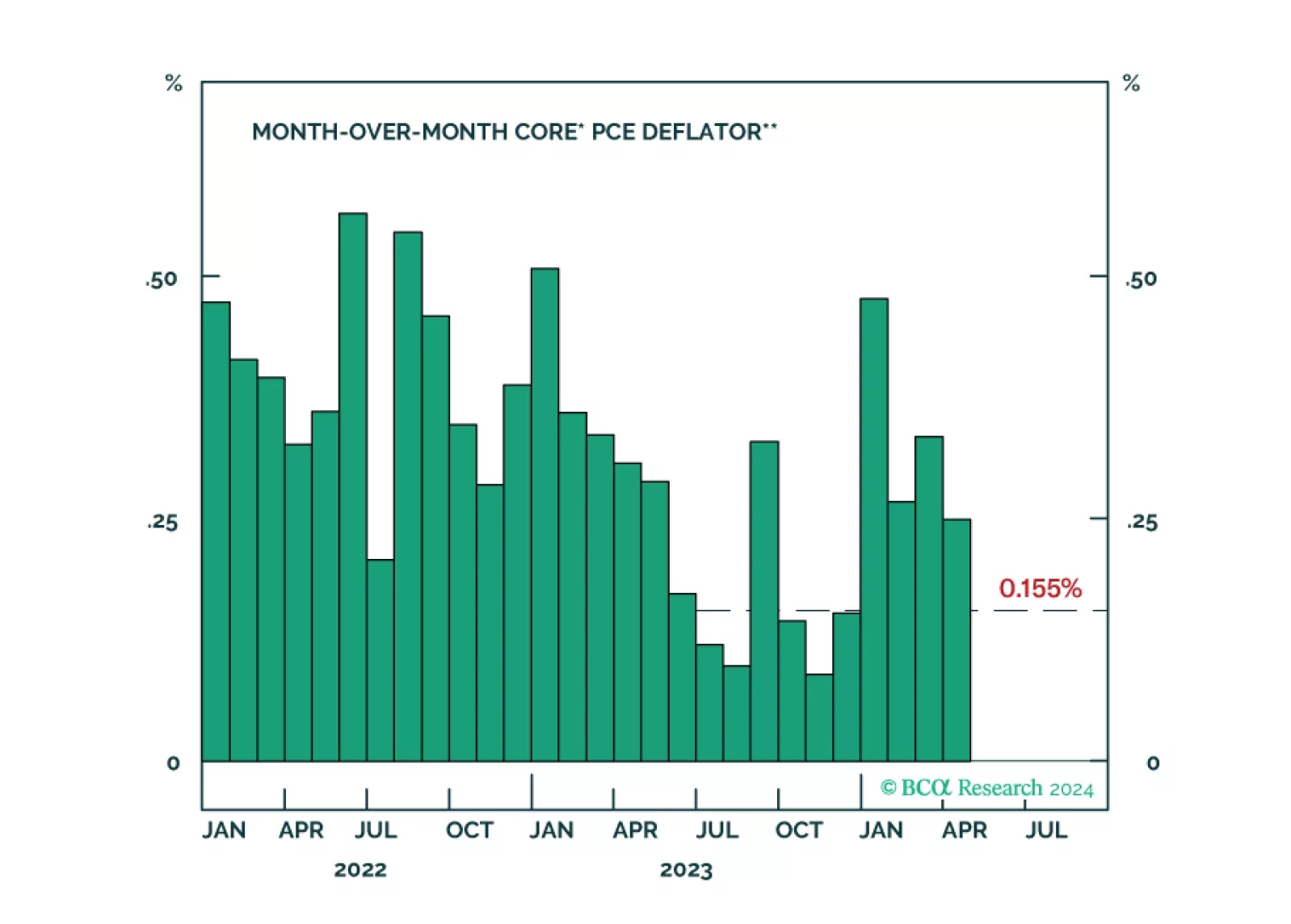

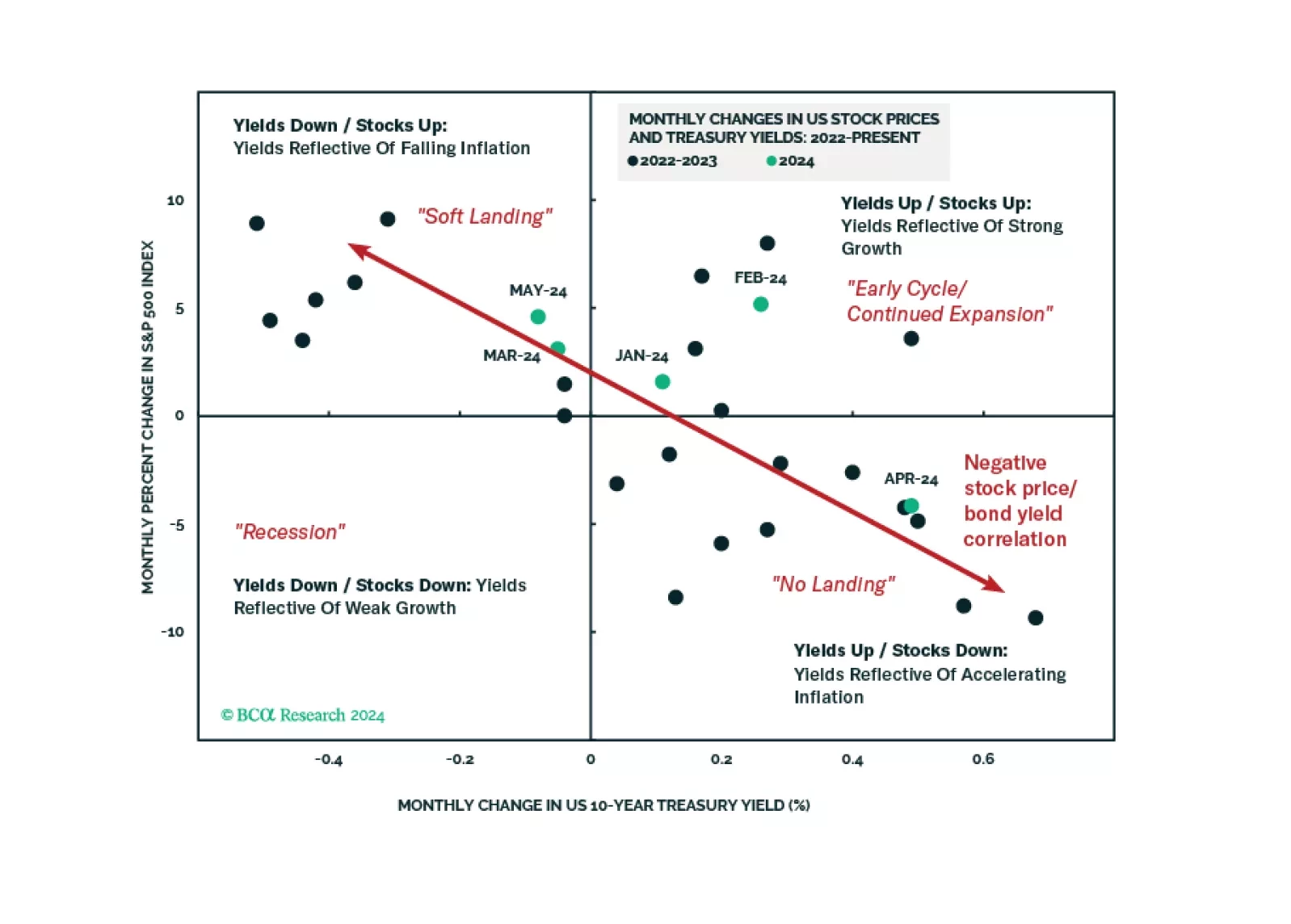

Recession-Hard/Soft Landing

Our Portfolio Allocation Summary for June 2024.

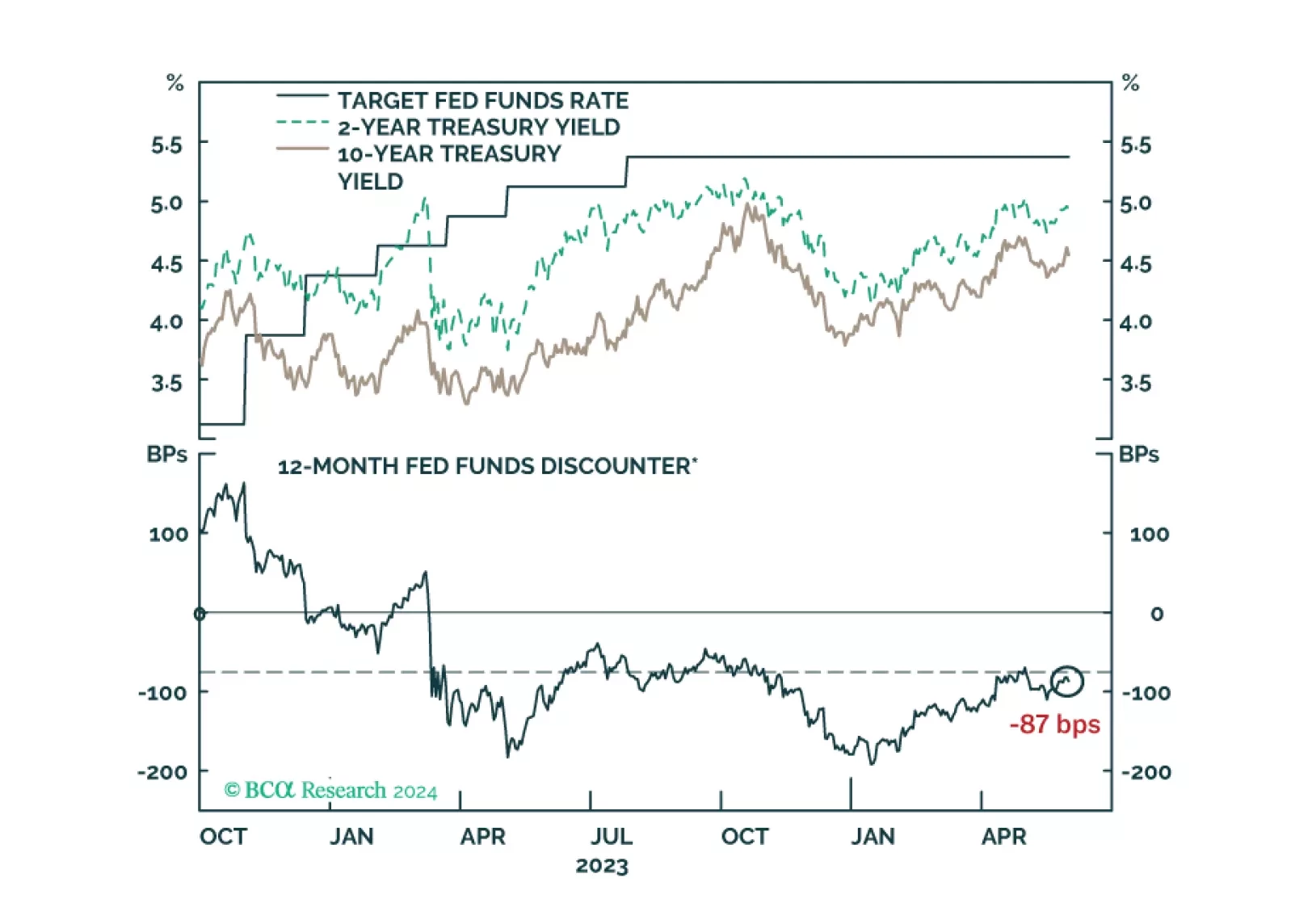

We comment on whether Treasury market valuation is sufficiently attractive to get long bonds and consider some of the common arguments for why yields may yet make new highs.

In Section I, we argue that global investors have been lulled into a false sense of security concerning the resiliency of the US economy. Tight monetary policy means that something must change for a recession to be avoided, and developed market rates cuts will likely be too modest and come too late to save the day. Nimble investors or those highly sensitive to tracking error should not be underweight stocks over the coming 3-6 months. Over a 6-12 month time horizon, we continue to recommend that investors remain underweight global equities versus US$-hedged long-maturity developed market government bonds. Section II is a guest report written by Martin Barnes, BCA’s former Chief Economist. Martin revisits the idea of the Debt Supercycle and discusses how its true end may emerge in response to a fiscal crisis in the US over the coming few years.