Recession-Hard/Soft Landing

According to BCA Research’s Counterpoint service, job losers not on temporary layoff (‘bad’ unemployment) will need to rise further for the Fed to reach its 2 percent inflation target. Although prime-age participation has surged, the participation of older…

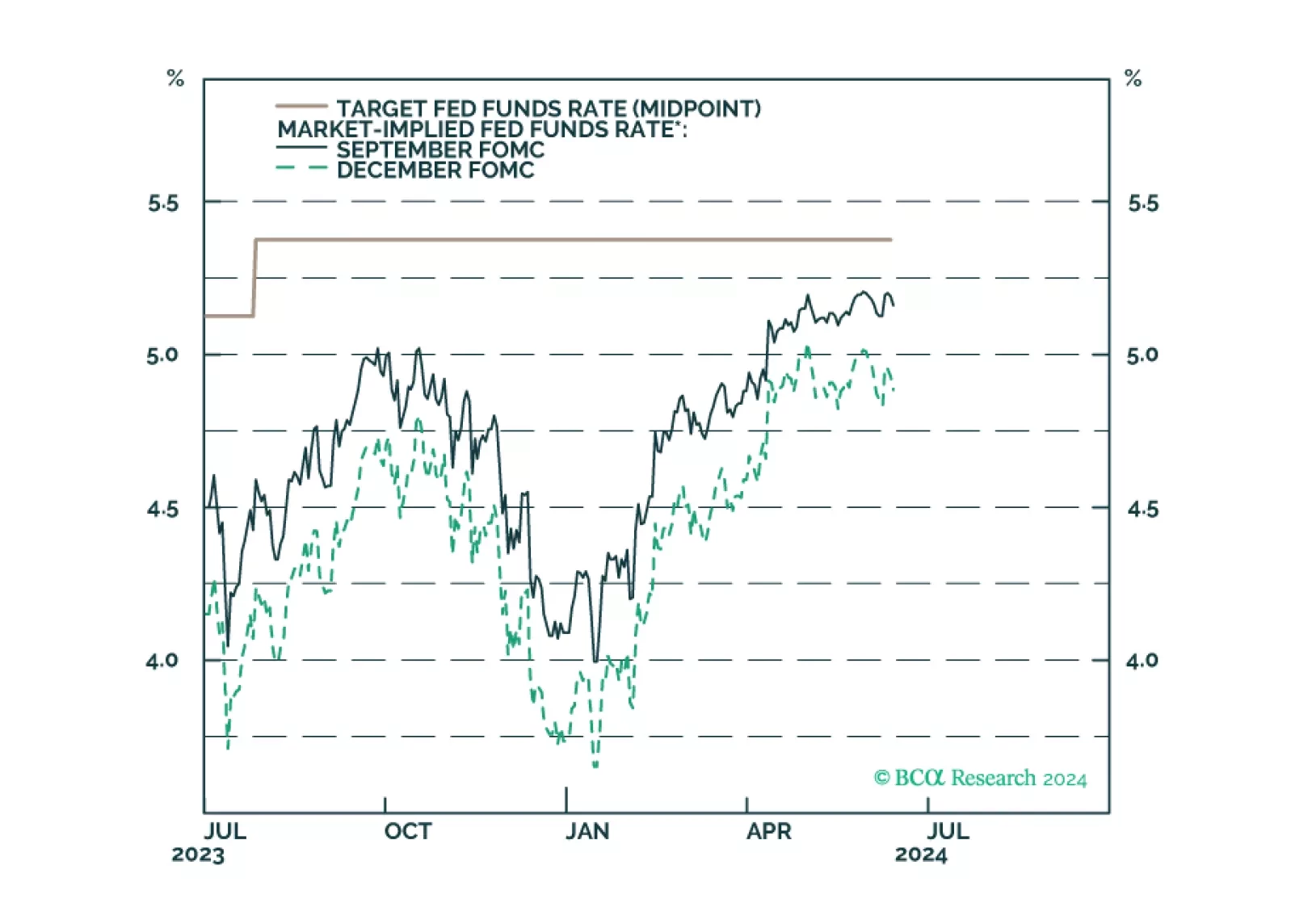

Our reaction to this morning’s CPI report and this afternoon’s FOMC meeting.

US CPI inflation continued to ease in May. Headline CPI stagnated on a month-on-month basis (3.3% y/y) in May, down from April’s 0.3% m/m (3.4% y/y), and below expectations of a more muted rate of growth. Core CPI also slowed more than expected, rising…

The Bank of Japan exited negative interest rate policy in March, but subsequent softer-than-expected CPI inflation prints have complicated its path towards tightening. The central bank is widely expected to stay put when it meets this week. Governor Kazuo…

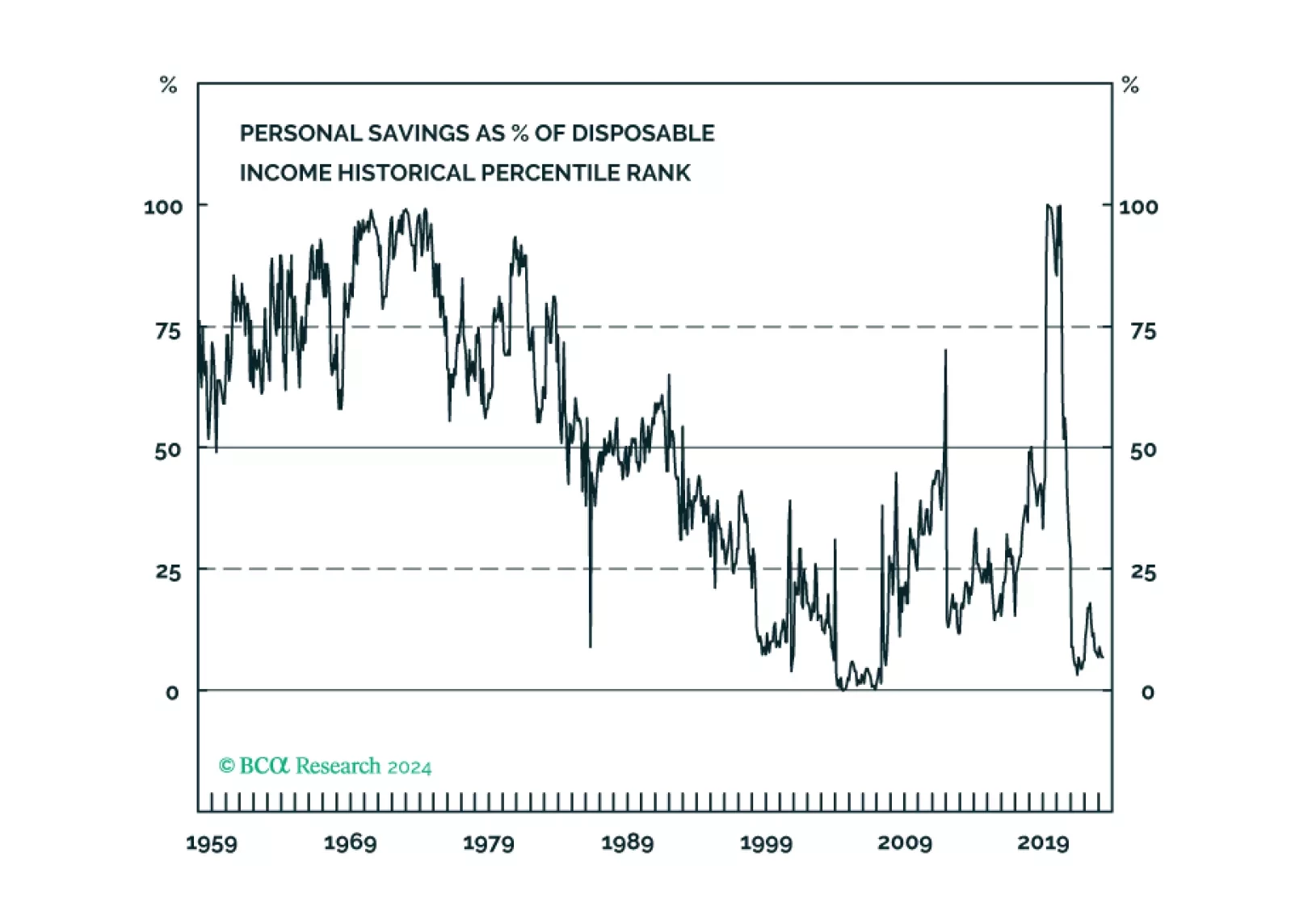

Total consumer credit rose by USD 6.4 billion in April (to USD 5,053 billion outstanding), from a USD 1.1 billion decrease in March (a large downward revision to the USD 6.3 billion rise initially reported) and significantly shy of expectations for a USD 10…

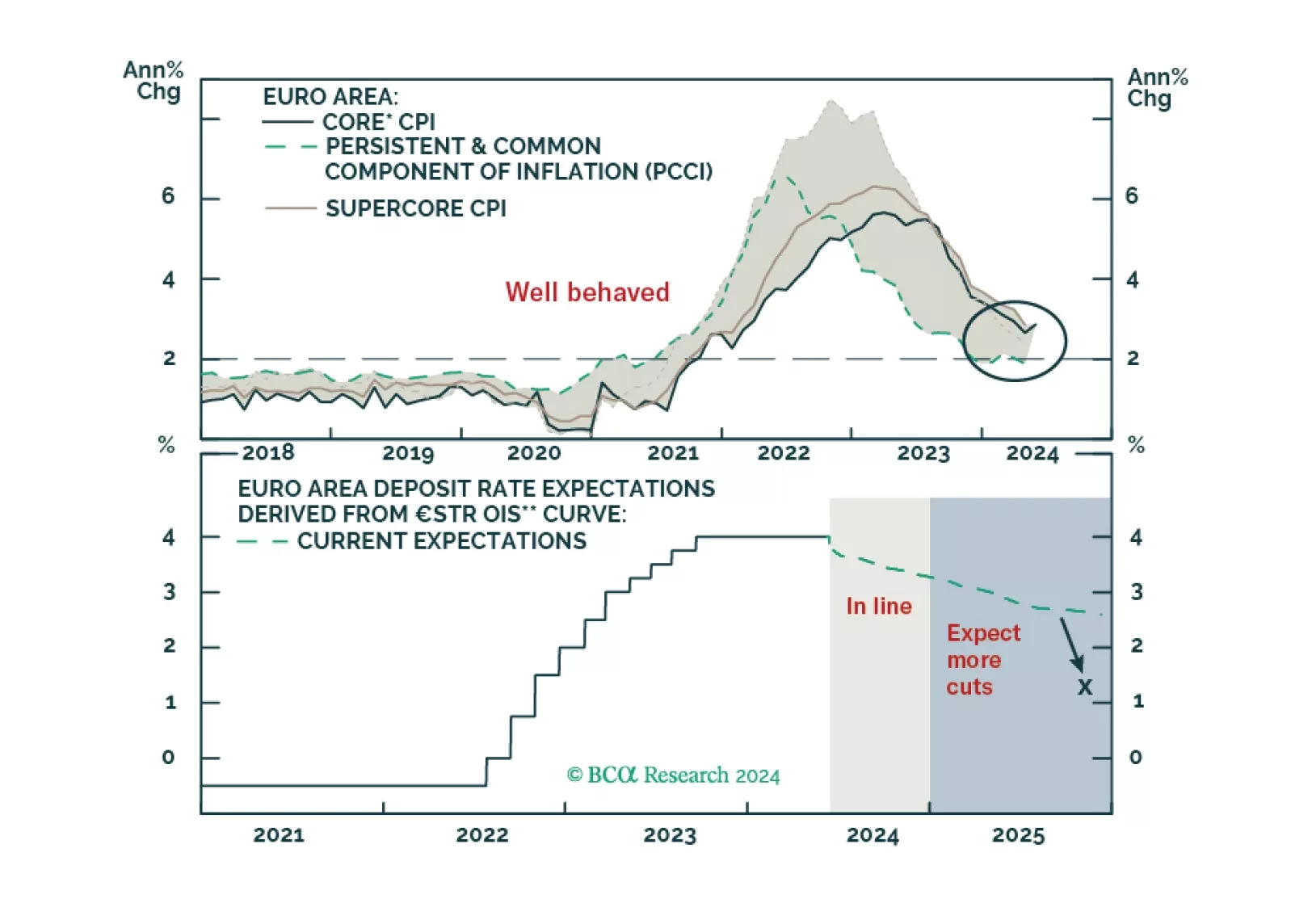

The ECB is now firmly in easing mode, even if it refuses to pre-commit to a specific rate path. What does this data dependency mean for the euro and European yields?

Although the comprehensive economic surprise indexes continued weakening in May, the metrics in our equity downgrade checklist haven’t softened enough to check more boxes now. While we continue to expect the US economy will enter a recession before year end, it is not yet certain and we remain tactically neutral.

US nonfarm payrolls grew by 272 thousand in May, accelerating from 165 thousand in April, and swamping expectations of 180 thousand. Average hourly earnings increased by 4.1% y/y from an upwardly revised 4.0%. However, the unemployment rate unexpectedly…

China’s exports in USD terms surged 7.6% y/y in May, from 1.5% in April, surpassing expectations of a 5.7% gain. However, base effects largely overstate the strength of Chinese exports given that they contracted by 8% y/y in May 2023. Subsequent declines…

Global growth expectations for 2024 have been revised higher. Investors now forecasts 2024 GDP growth to clock in at 3%, up from 2.6% at the beginning of this year. A 1.1% upward revision in US growth expectations since January is driving the increased…