Real Estate

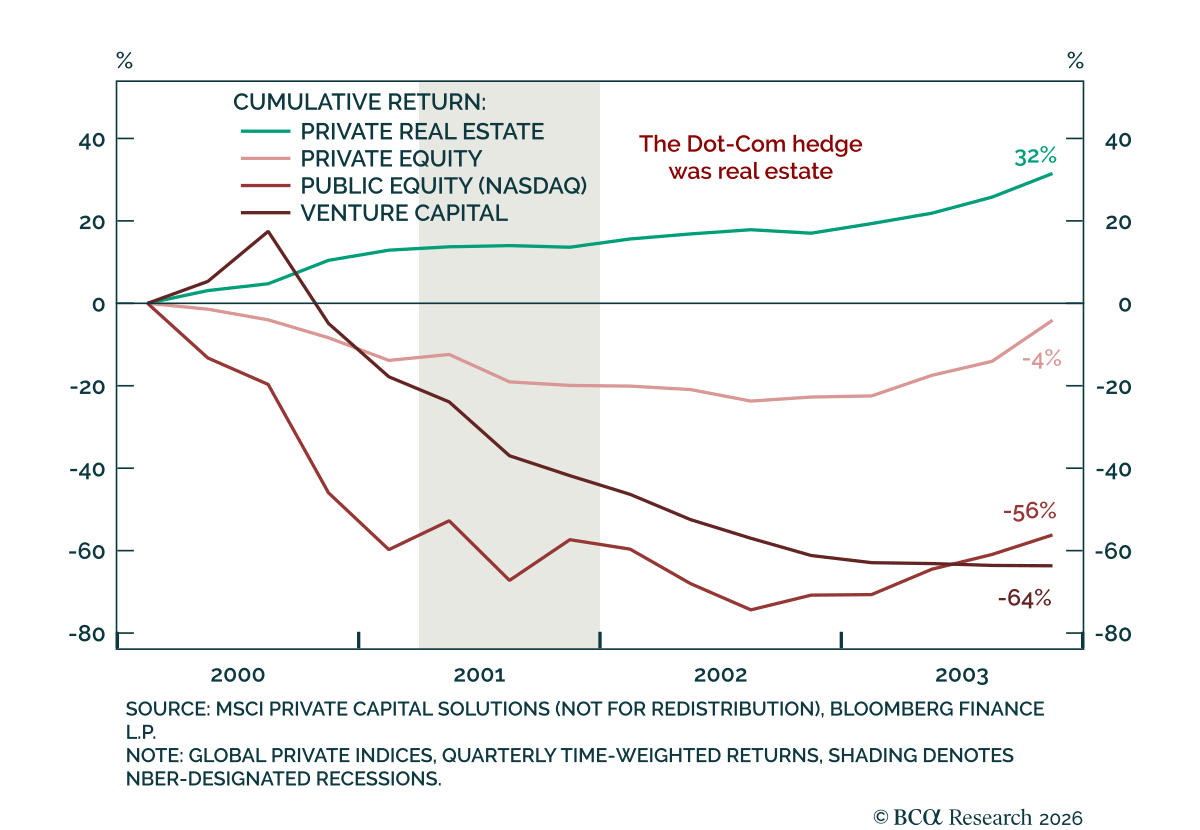

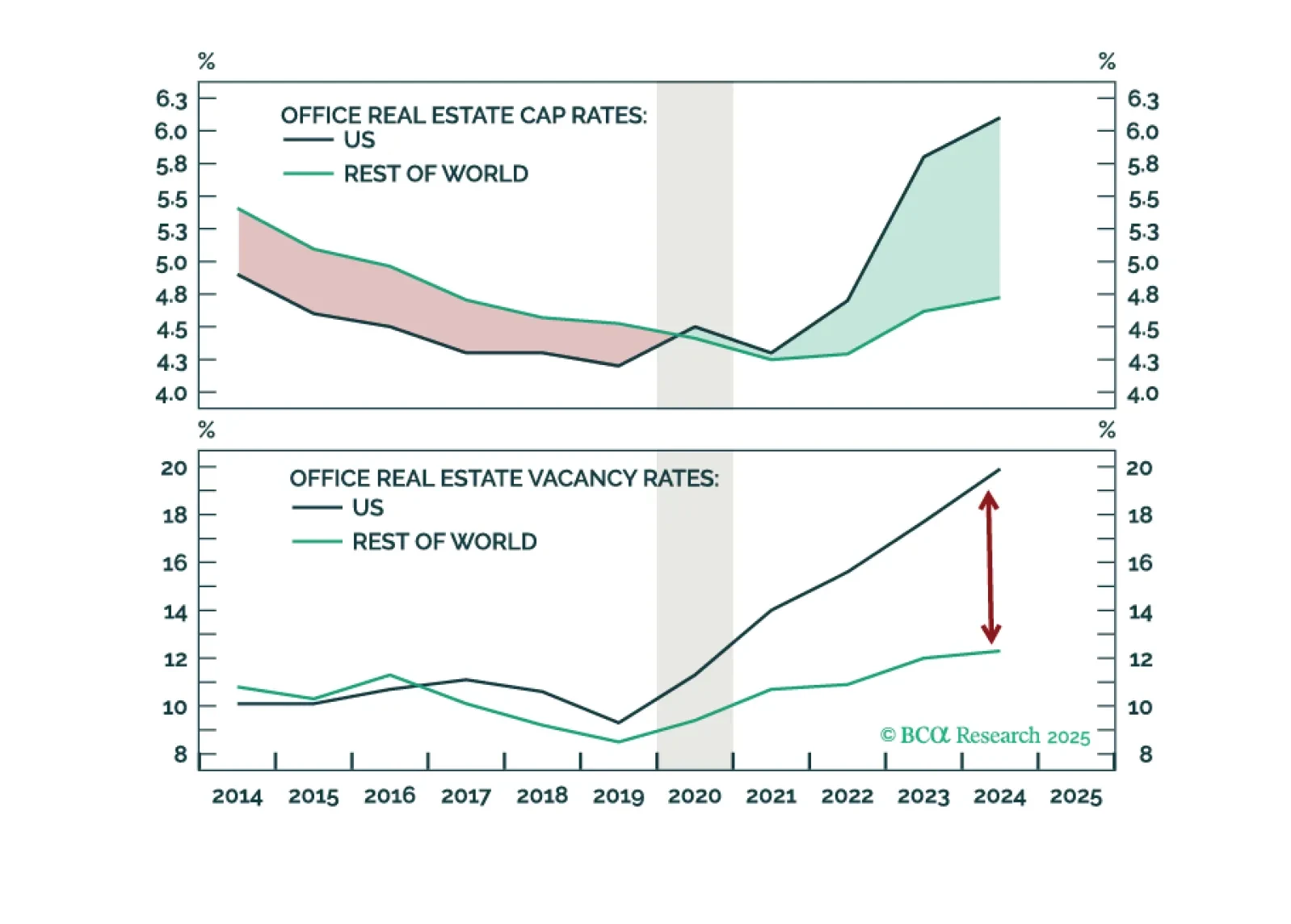

AI dominates markets, but concentration is risk. Real Estate is the diversifier. It outperformed during the Dot-Com bust and will do so again if the AI trade unwinds. Even Office, the sector arguably most exposed to AI disruption, will prove more resilient than bears expect.

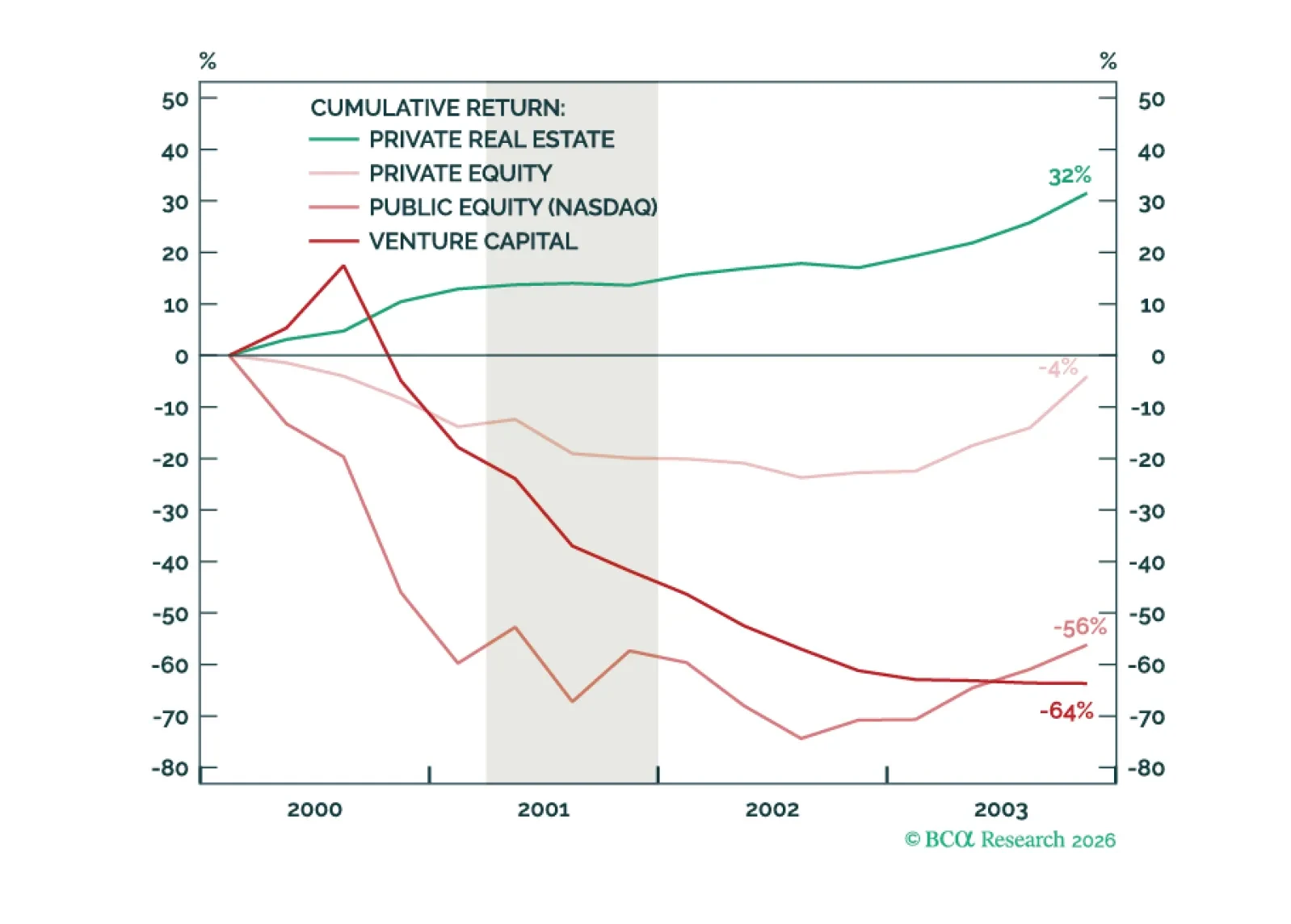

In Private Markets, yesterday’s winners often see outperformance fade. Top-quartile managers often regress toward the median as fund series mature. For investors evaluating the next Real Estate or Private Equity manager: Bias toward underweighting Funds V and beyond.

Private Credit, Software, Iran, Trump – important headlines, but the opportunity lies elsewhere. In this edition of the Public Versus Private series, we do things a little differently. We focus exclusively on US Sunbelt Multifamily, a perennial area of global investor interest. We favor Public REITs over Privates with valuations near a bottom.

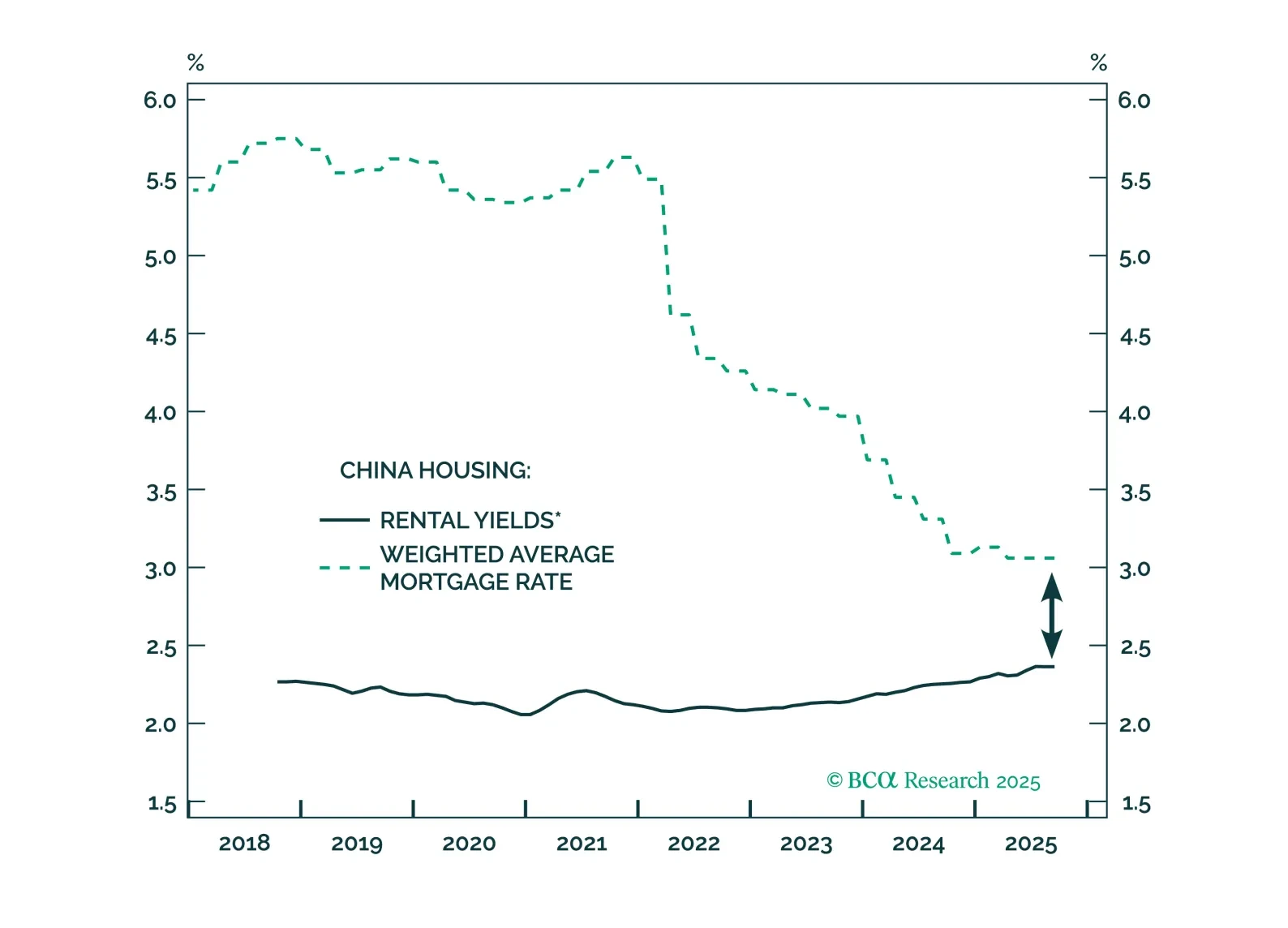

This report revisits China’s property market through both cyclical and structural lenses, assesses the likely policy responses, and evaluates their investment implications.

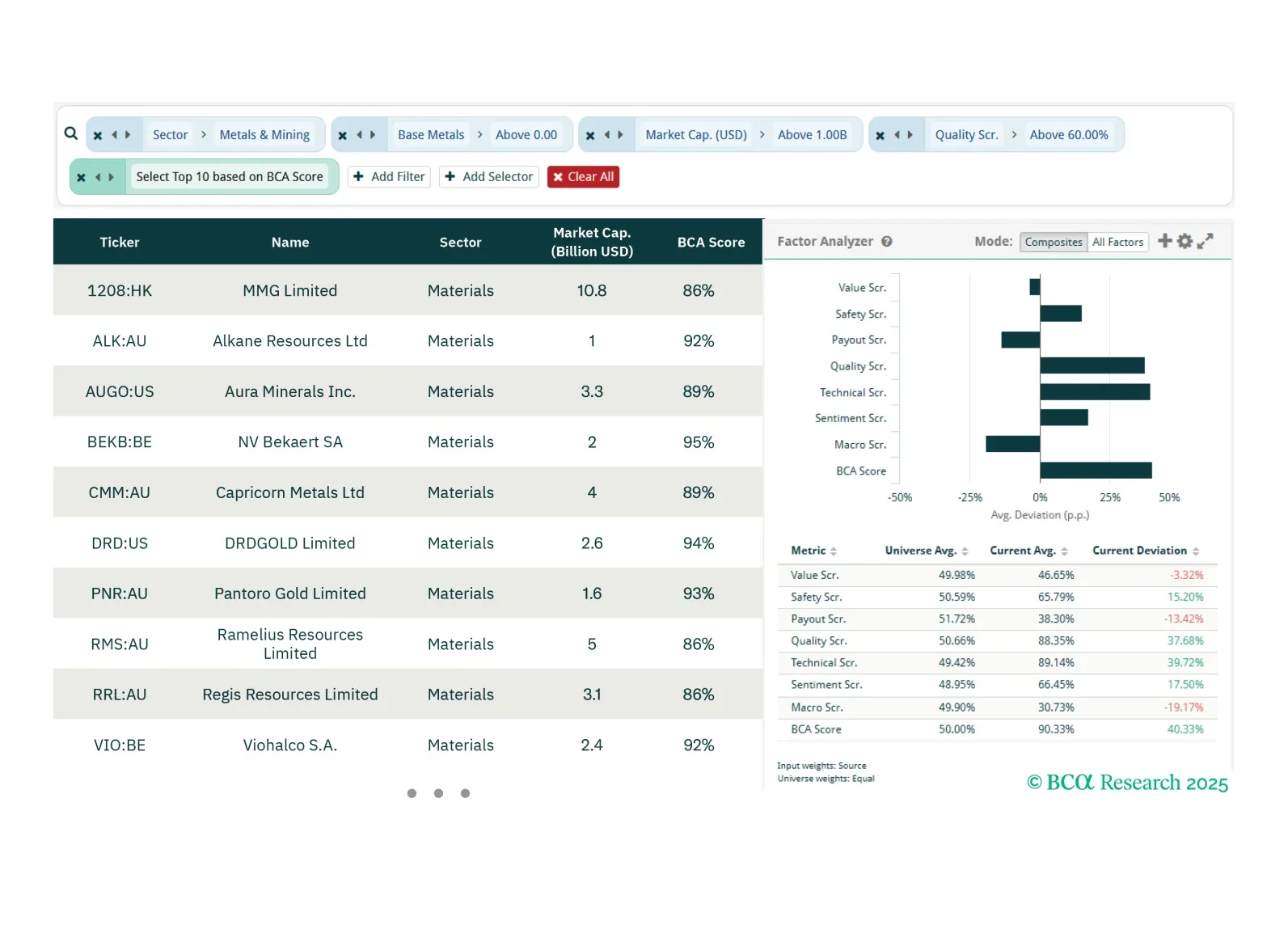

This week, our screeners explore ways to play a long-term bullish metals view, sub-sector REITS opportunities as well as Japanese Value stocks.

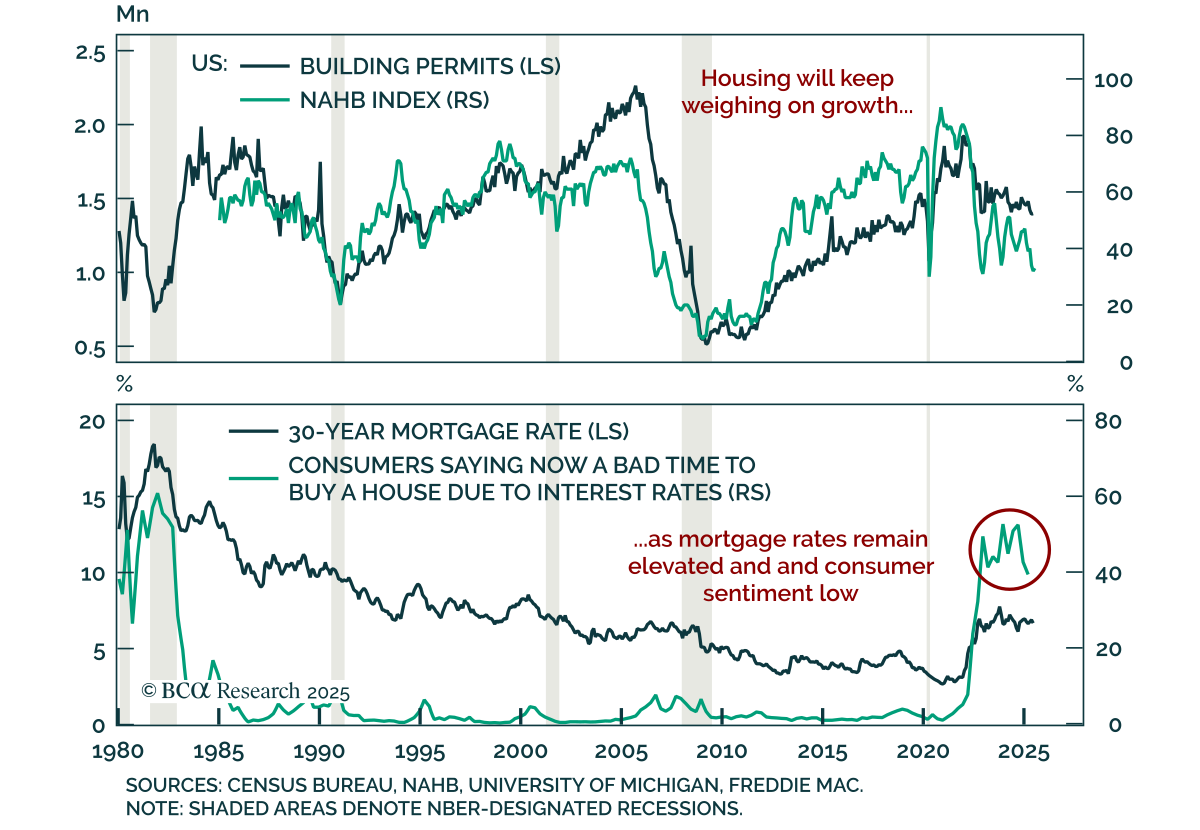

Real Estate performance is contingent upon the Fed rate-cutting cycle. Yet, we worry about a hawkish Fed surprise and are closing our overweight in the sector. We also recommend a granular approach to subsector selection.

Asset prices reflect expectations—but US Office Real Estate expectations are too pessimistic. We present the case for why strong fundamentals will drive performance, despite macro risks.

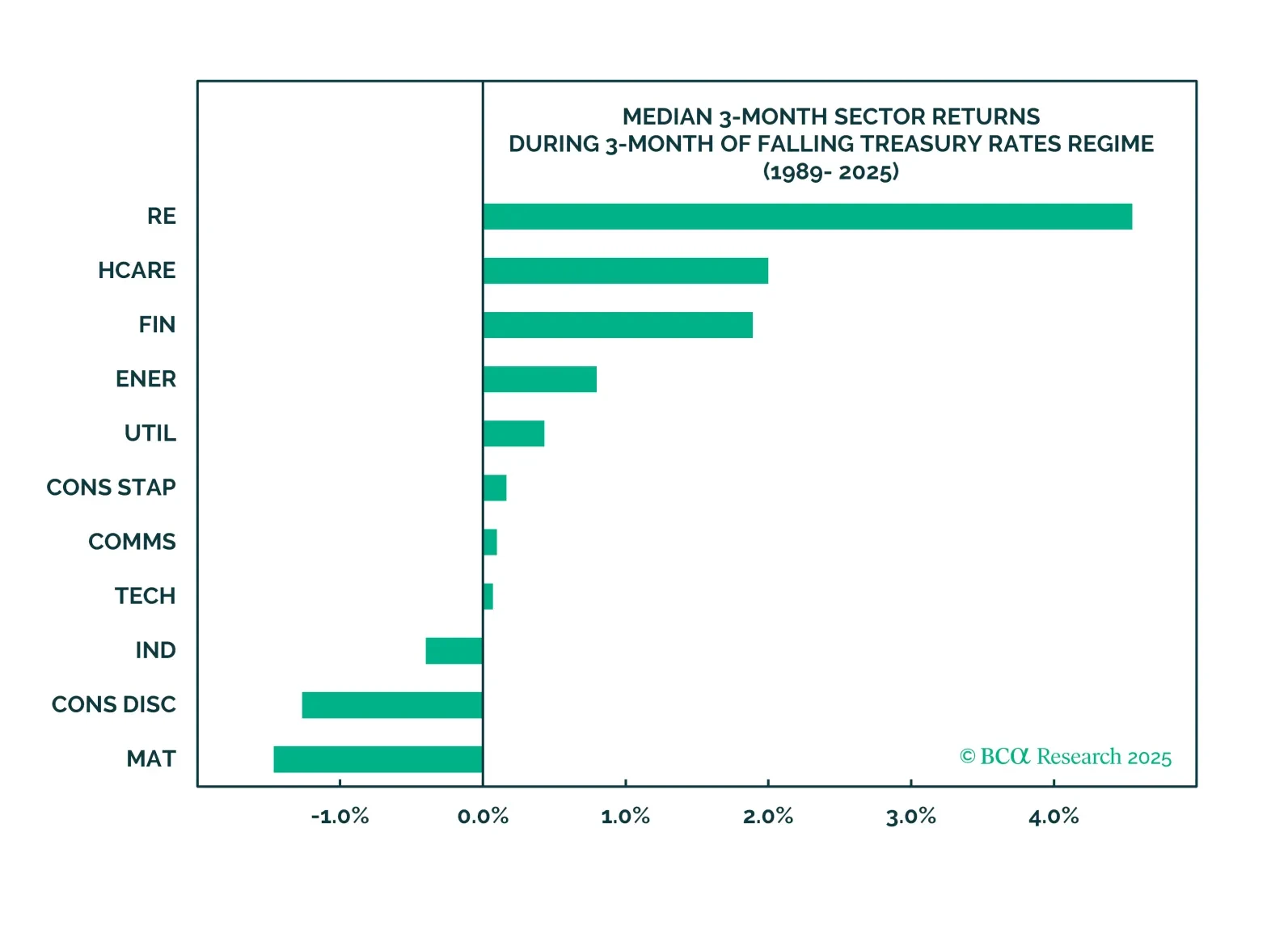

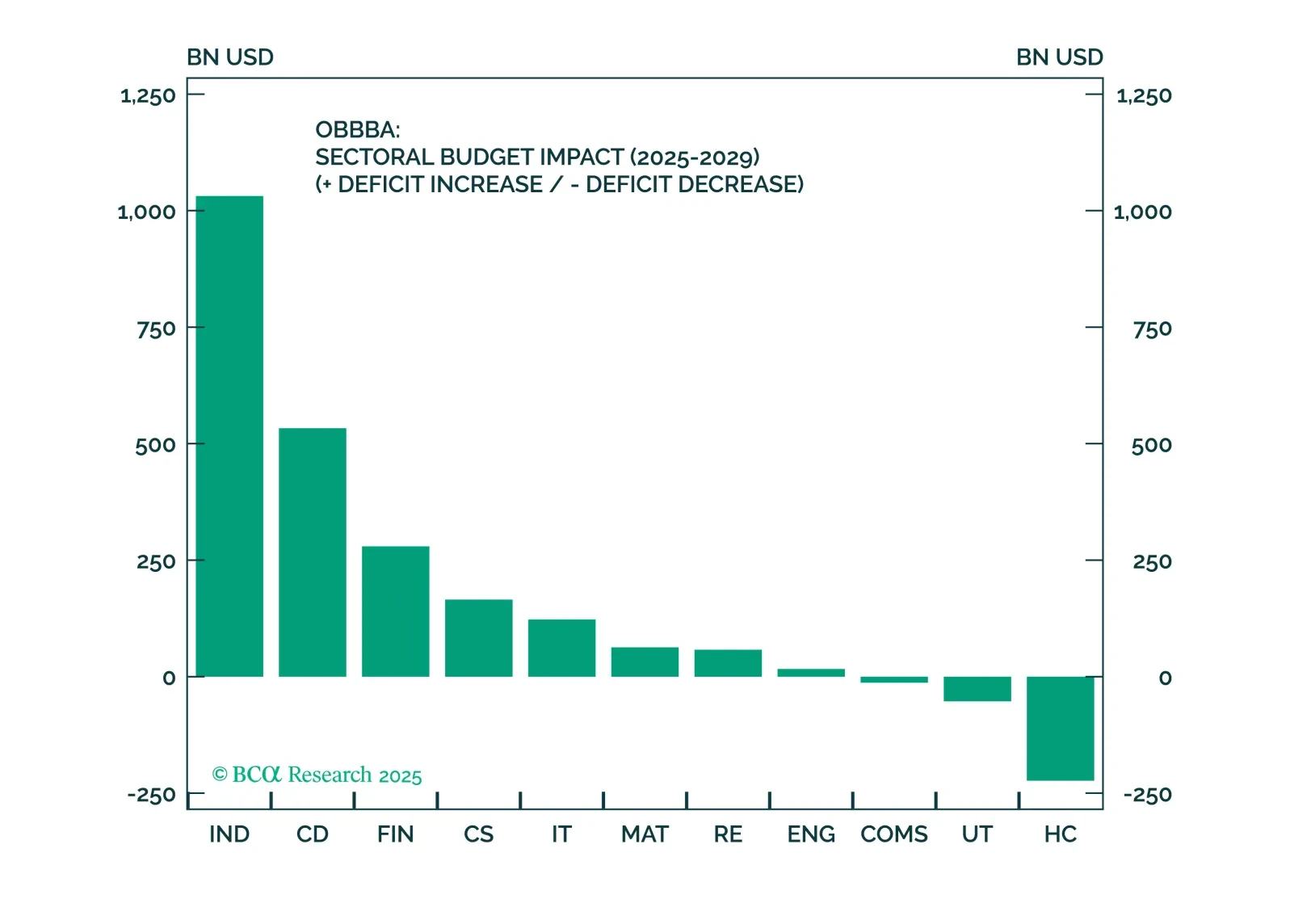

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.