Private Real Estate

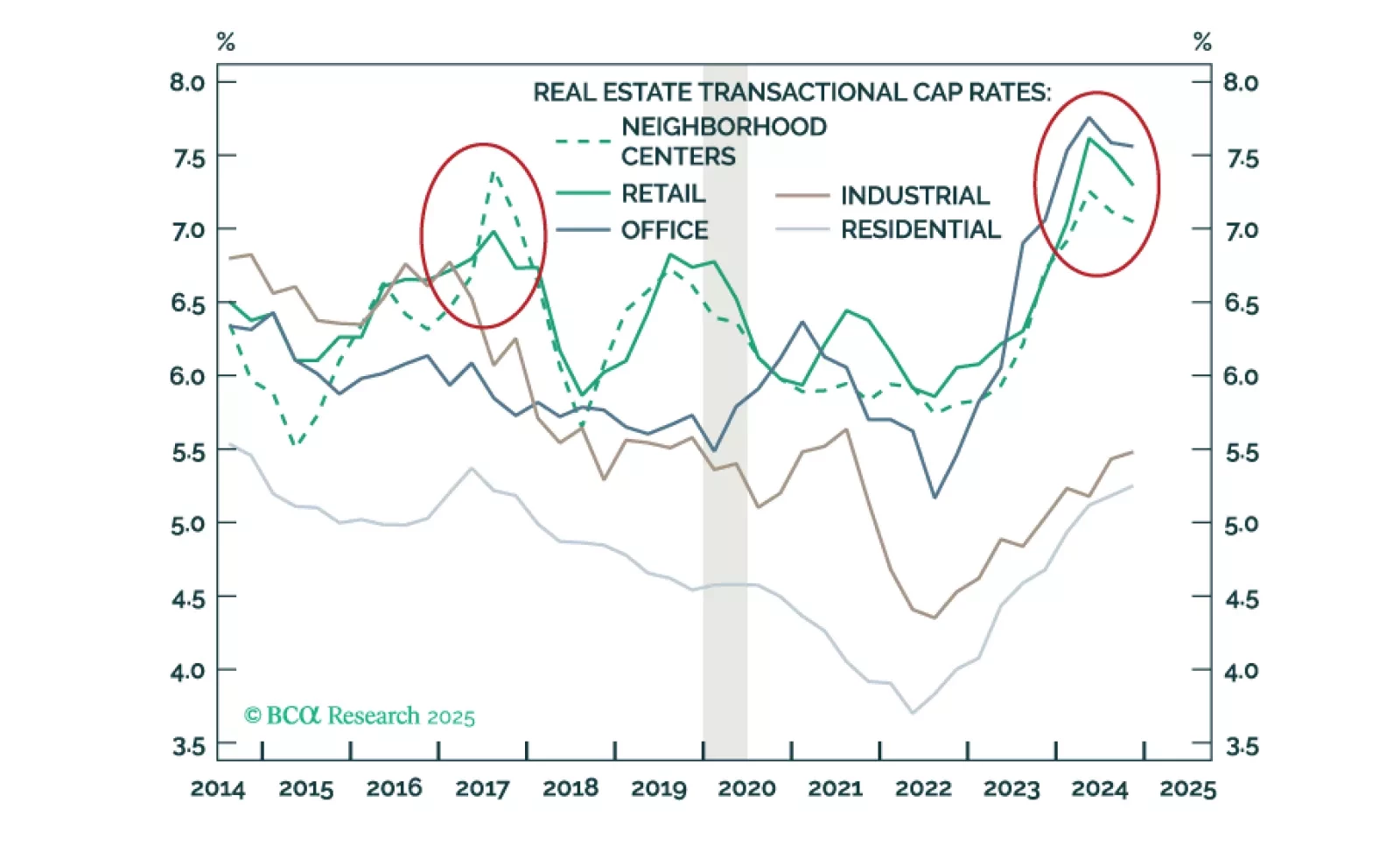

It is time to bet on brick-and-mortar again. The next time you step around your partner's Amazon package on your way to a physical store, consider this: Rock-bottom investor expectations, attractive initial fundamentals, and ongoing demographic shifts make Retail Real Estate a buy for the first time in a decade.

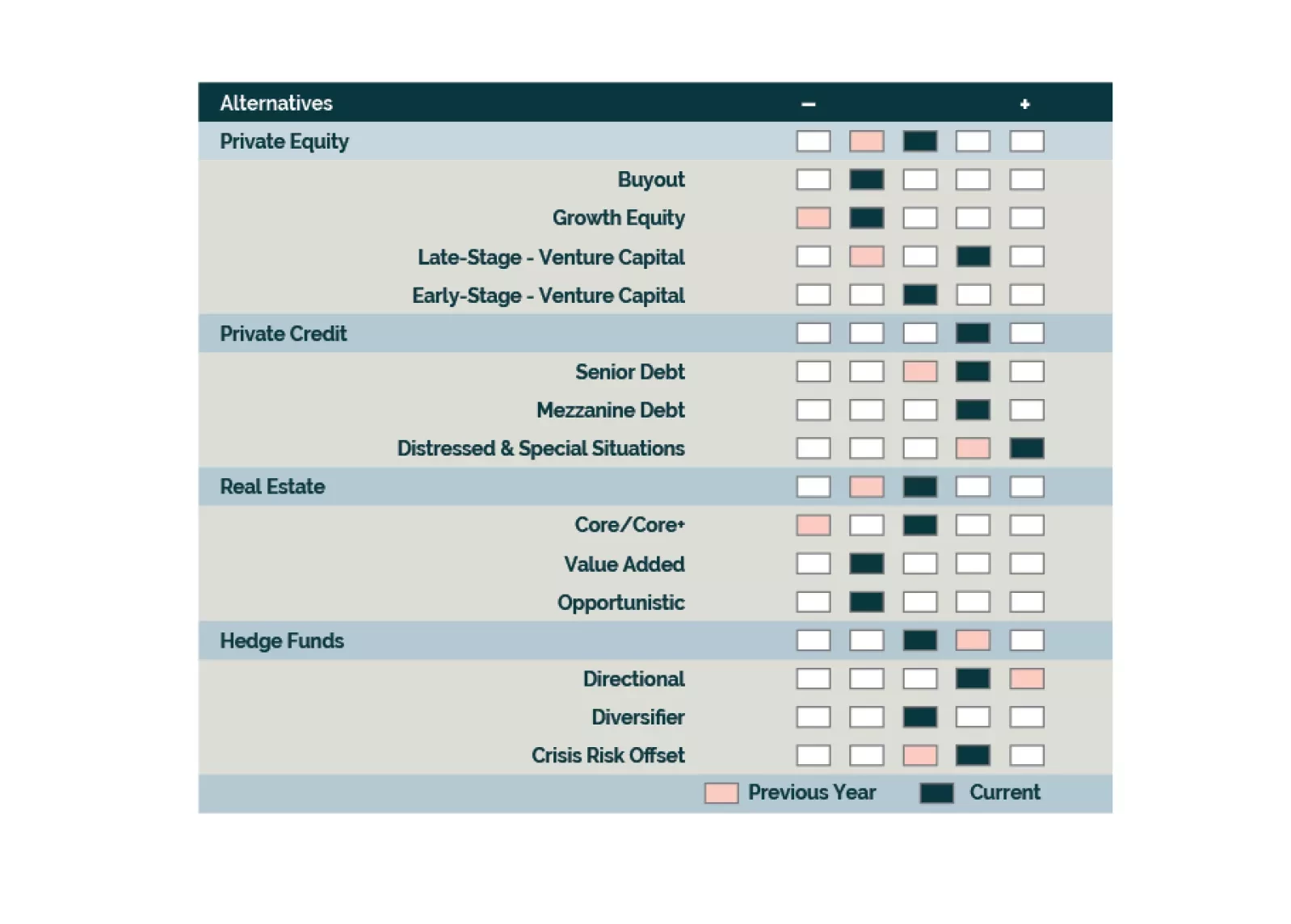

Asset class expectations show mixed shifts from 2024, with Real Estate seeing substantial upgrades and Private Equity benefiting from Venture Capital improvements. Private Credit return expectations decline from 2024 but remain relatively attractive. Infrastructure shows varied dynamics across sub-strategies, with Value-Add offering strong return potential. Within Hedge Funds, Long-Short Equity shows higher tactical returns while Multi-Strategy leads strategic projections.

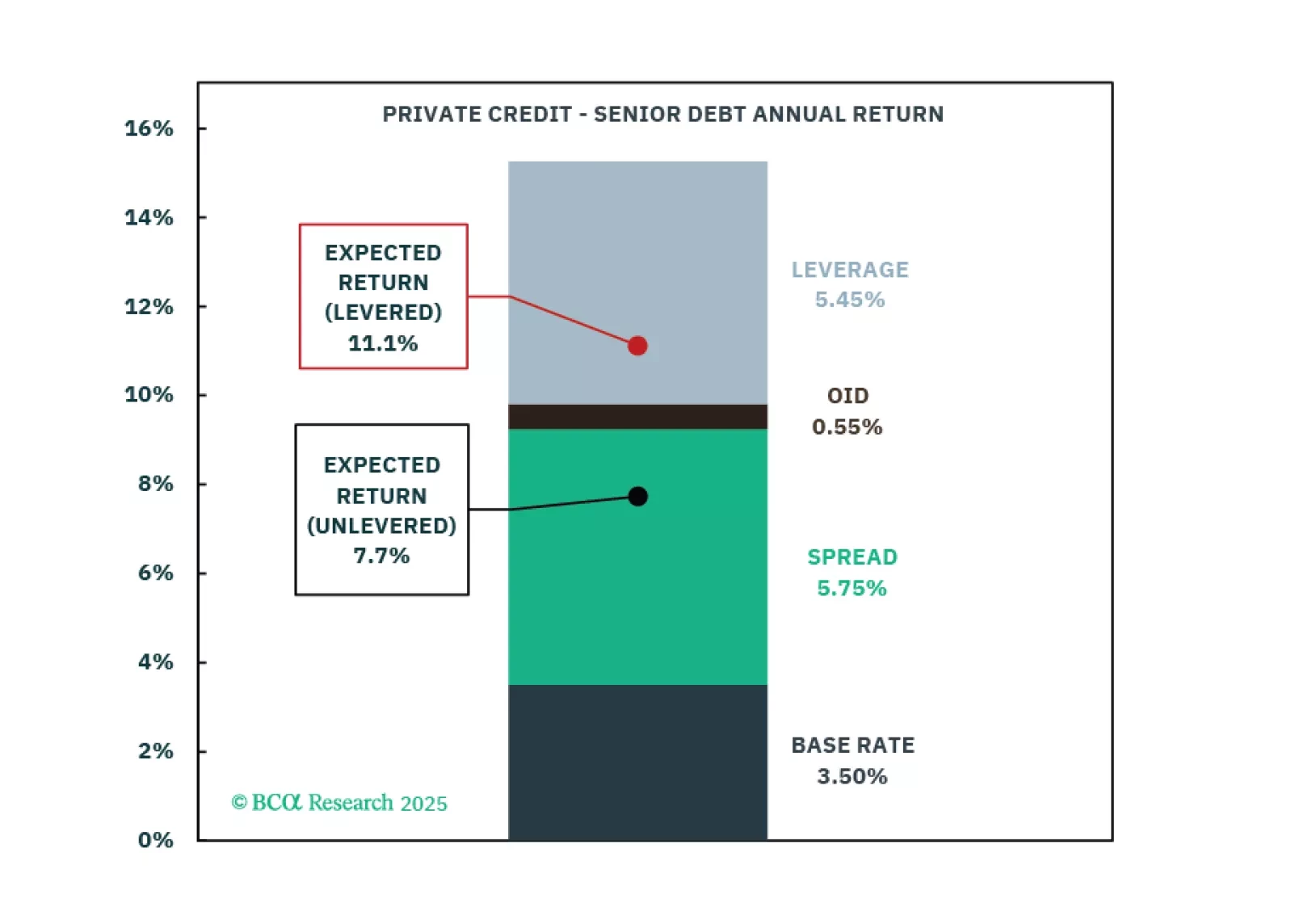

We are growing positive on Growth assets with recession expectations increasing our optimism on entry points. Equities are led by APAC Private Equity, North America Venture Capital, and Europe Buyouts. Our outlook continues to improve on CRE within the Inflation & Diversification bucket while we are underweight Multi-Strategy amongst Hedge Funds. We maintain an overweight to Senior Direct Lending for Income with a preference for North America.

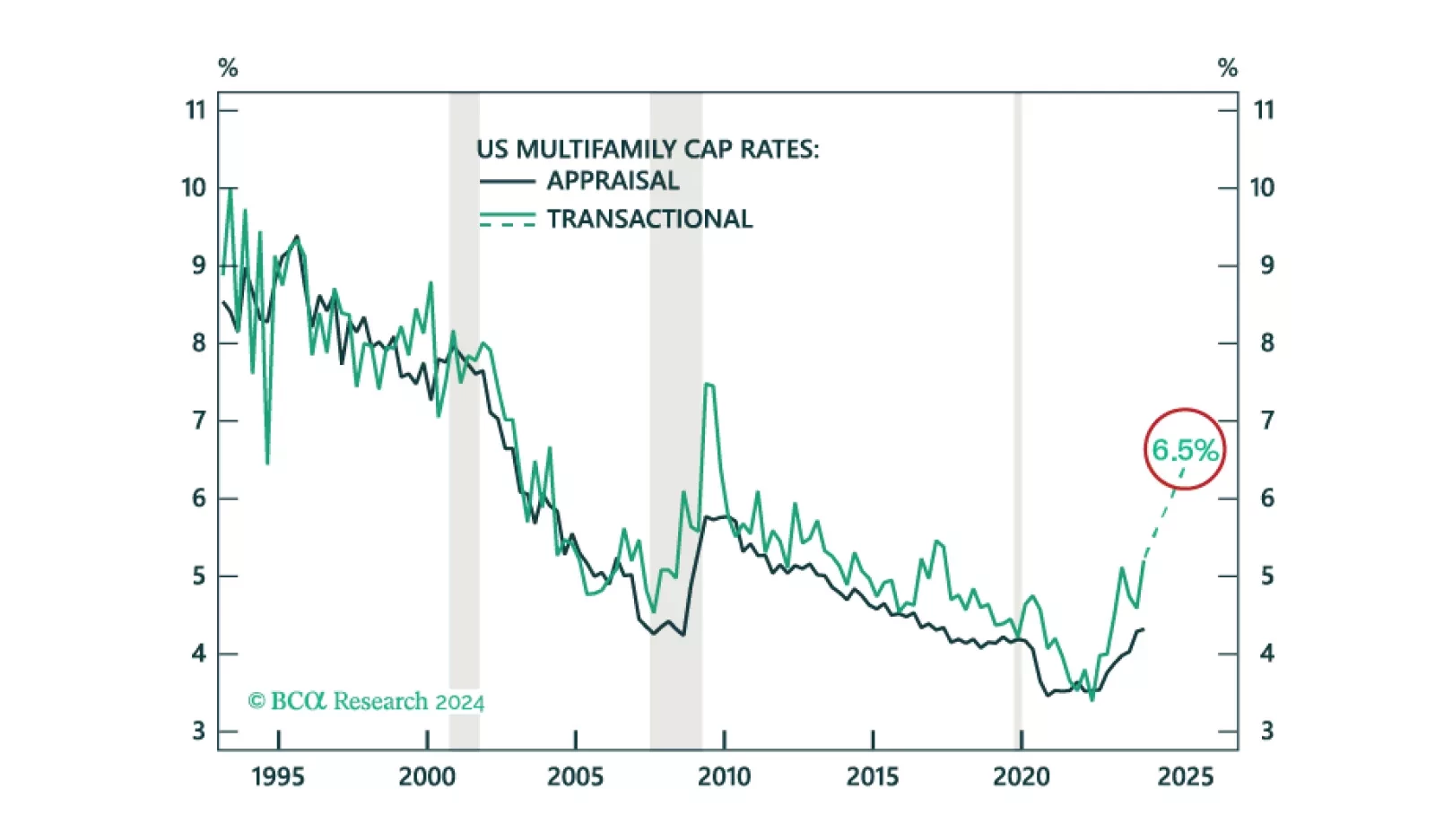

We project US Multifamily cap rates to increase from 5.2% to 6.5%. While we find an unfavorable risk-adjusted return on the asset, especially relative to other opportunities in CRE, cap rates are moving closer to peak.

We go overweight Late-Stage Venture Capital and APAC Private Equity but remain underweight North America Buyouts. We maintain our neutral outlook towards Hedge Funds and are positive on Long-Short Equity, Event Driven, and CRO strategies. We are cooling towards Direct Lending strategies as competition and relative opportunities increase. CRE’s downturn continues to unfold; we are starting to be buyers.

Investors should be tactically tilting allocations towards Direct Lending, Distressed Debt, and Directional Hedge Fund strategies at the expense of Real Estate, Private Equity, and Diversifier Hedge Funds. Structural opportunities are emerging in Real Estate and Venture Capital.

We see challenges ahead for Global Buyout across geographies as valuations need further resetting. While we are concerned with capital controls and flight risk in Asia-Pacific Venture Capital, the upside potential from AI may be worth a look. The current entry point for Private Credit is opportune across North America and Europe with the distressed pipeline building. Real Estate does not look appealing with the macro and relative opportunity set driving our underweight. Hedge Funds have a favorable backdrop in the near-term, although prospects differ across Directional, Diversifier, and Crisis Risk Offset strategies.

We see a more positive backdrop for credit providers, with bilateral and structuring features as tailwinds for Private Credit. While there may be potential green shoots in some areas of Private Equity, current valuations are not attractive. We prefer Directional Hedge Funds over Diversifier and Risk Mitigation strategies. Real Estate has been an effective hedge against inflation, but now historically low cap rates are a headwind.