Private Markets

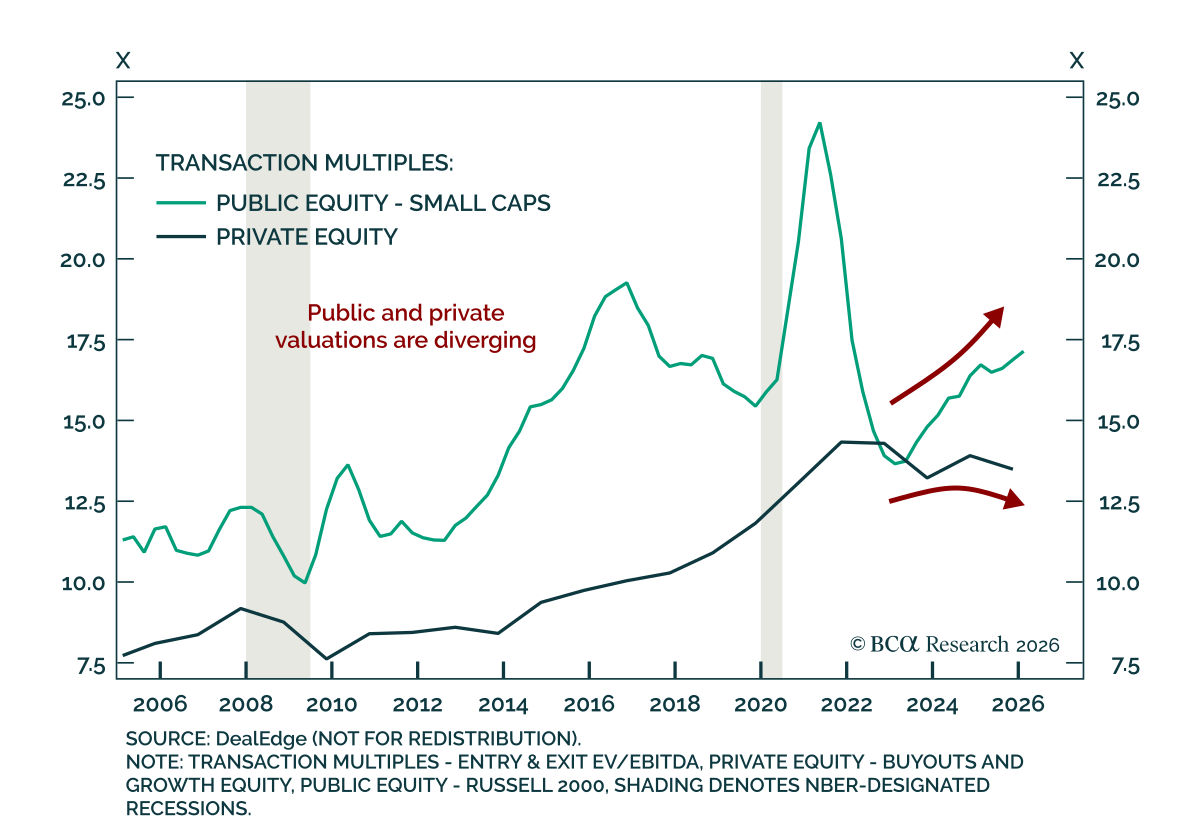

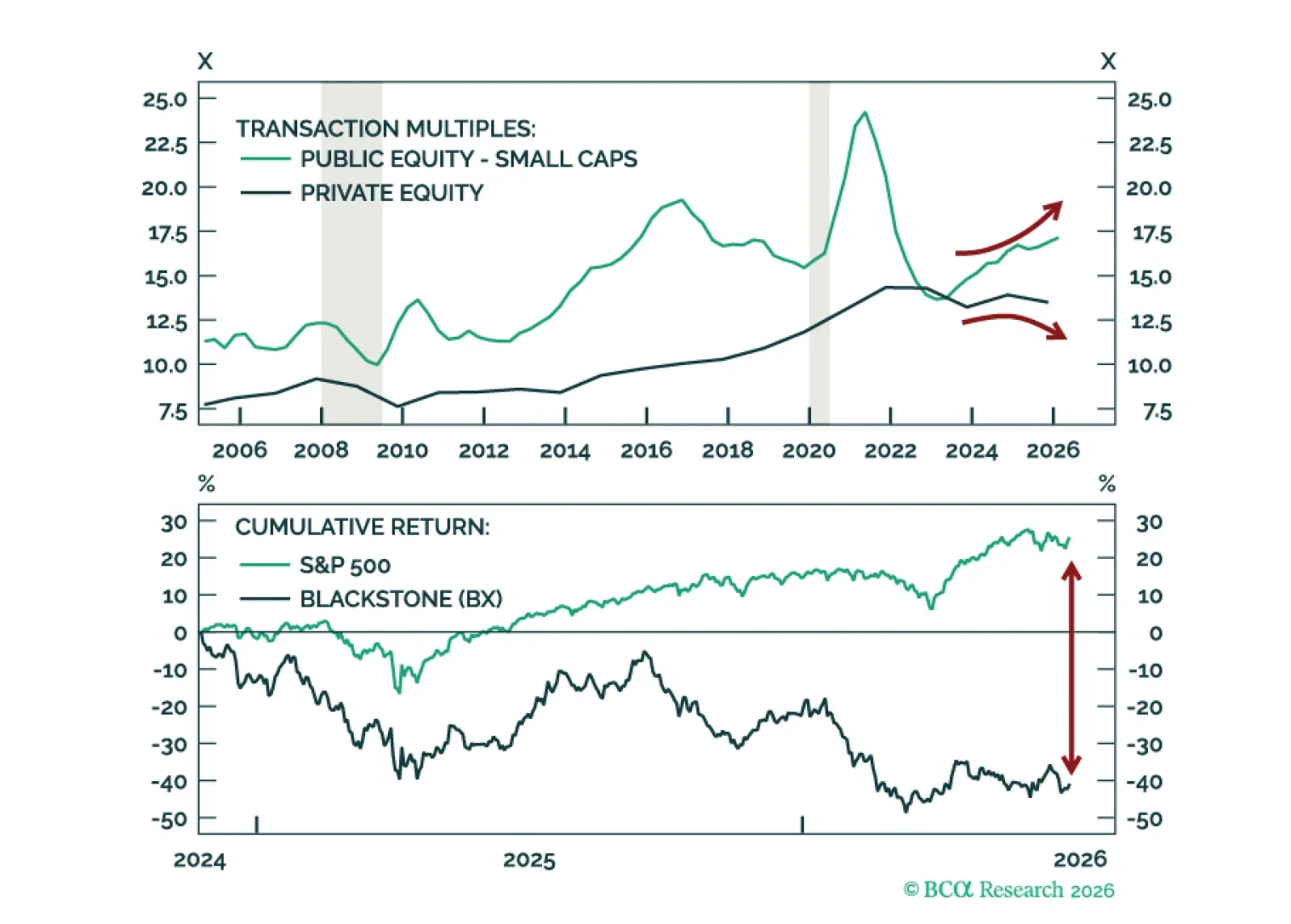

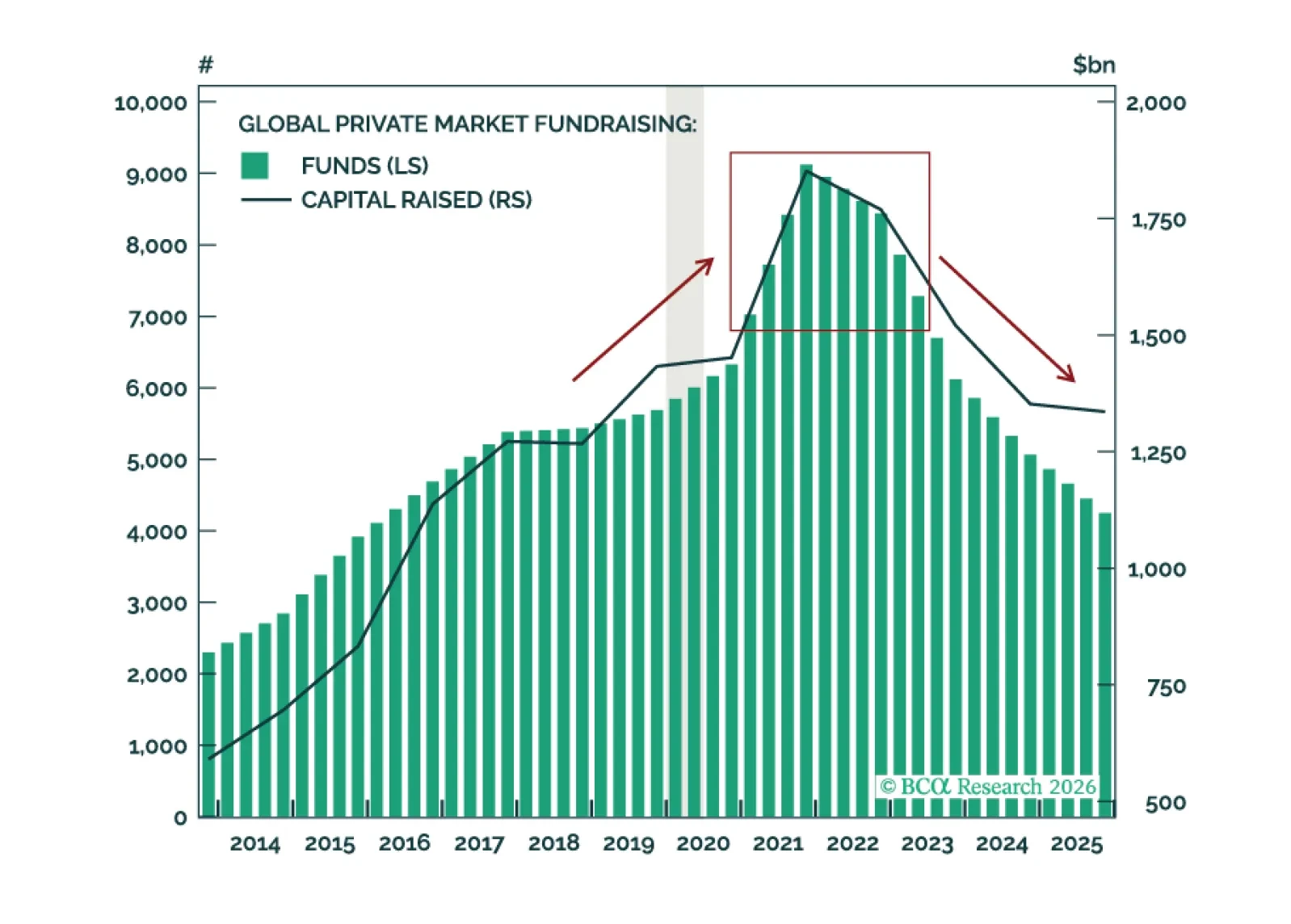

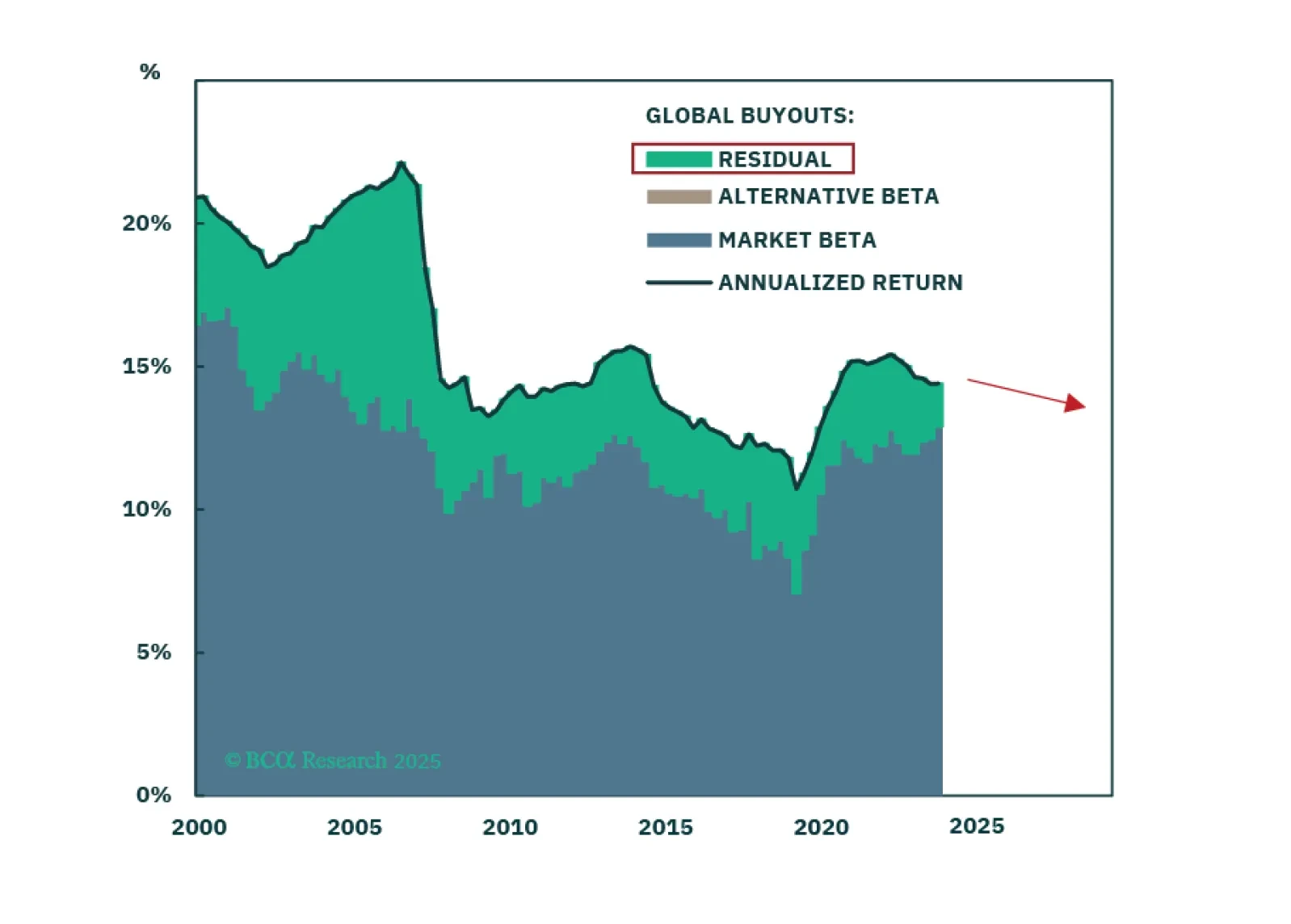

Beginning with this Quarterly report, The Global Asset Allocation and Private Markets teams are combining our quarterly outlooks into a single, unified framework, reflecting a more integrated approach to portfolio construction. In this joint outlook we upgrade Private Equity to overweight. Sentiment has soured, LPs are starved of distributions, flows have collapsed, valuations are trending lower, Secondaries are outperforming Primaries, and GP stocks are experiencing their worst underperformance on record. All signs of a durable bottom.

Investment risk in Private Markets differs from that in Public Markets. It unfolds over time, with today’s issues coming from yesterday’s investments. We explain why, and more importantly, why the next dollar now faces lower risk across both macro and fundamental drivers. Just do not expect a discussion about standard deviations.

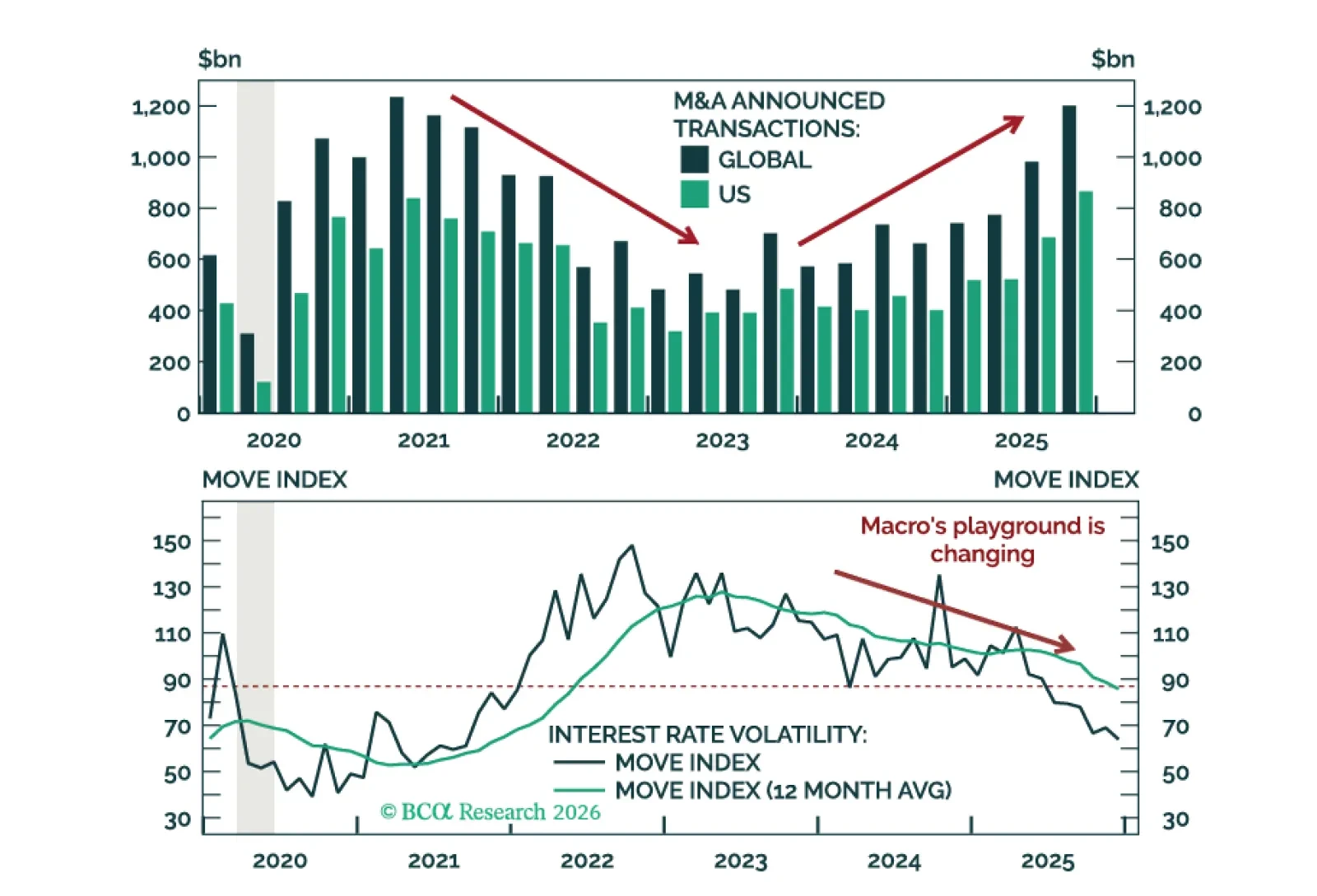

M&A activity finally reaccelerated in Q4 2025—it’s just the start. Macro Hedge Funds have outperformed with top-decile performance from Discretionary Macro—but that’s towards the end. We move Macro from overweight to underweight and Event Driven from neutral to overweight.

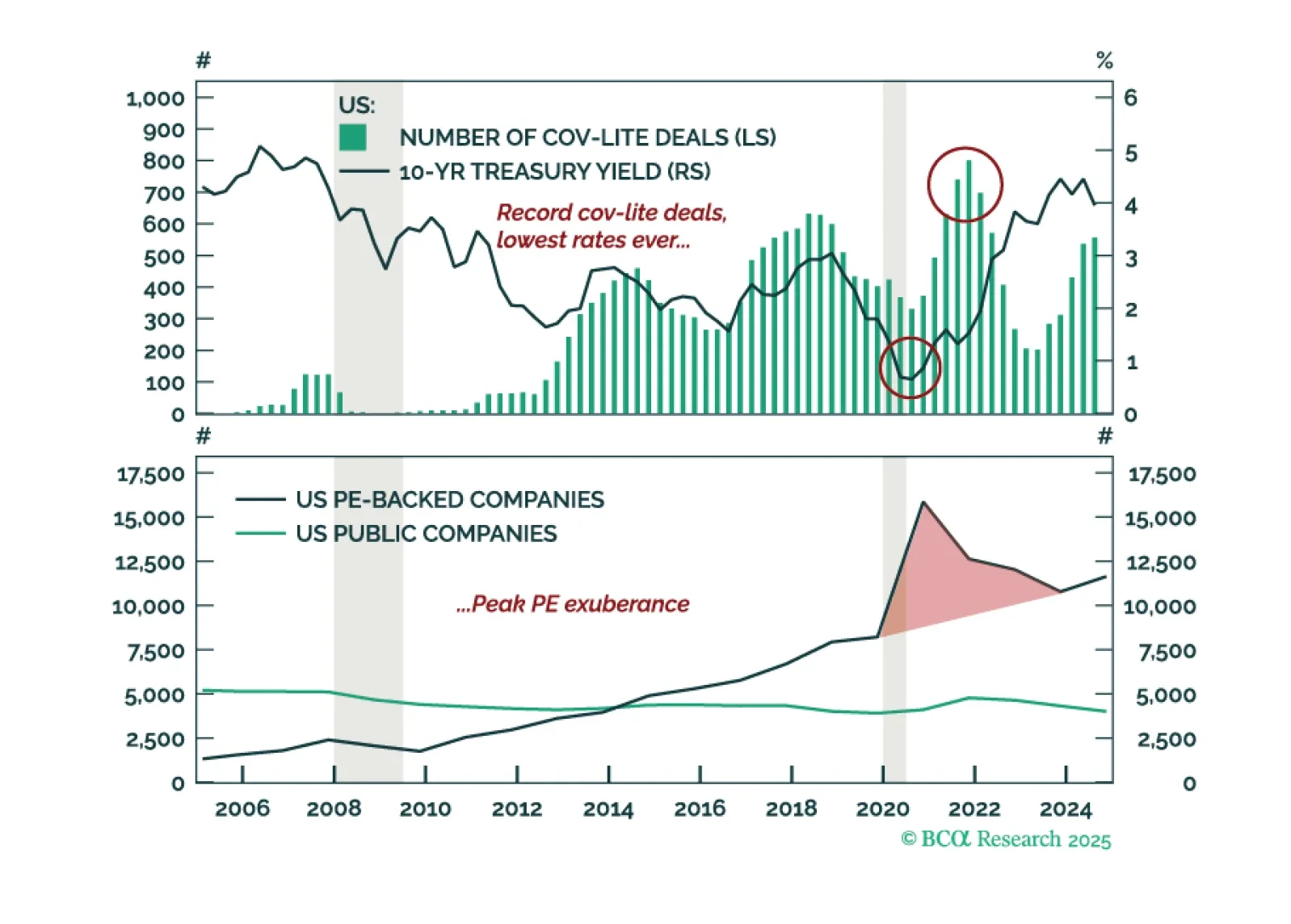

Private Credit outsiders are skeptical, insiders are believers—but are becoming nervous now. In the highlight of this Quarterly Report, we dig beneath the surface to uncover the buried bodies in Private AND Public Credit. The ghosts of 2020-2021 loan originations are catching up with investors.

Private Markets are entering a new phase as TPA and Evergreen funds expand. Shifts in access, implementation, and market leadership will have important implications for institutions, Wealth Management, and future Private Equity returns.

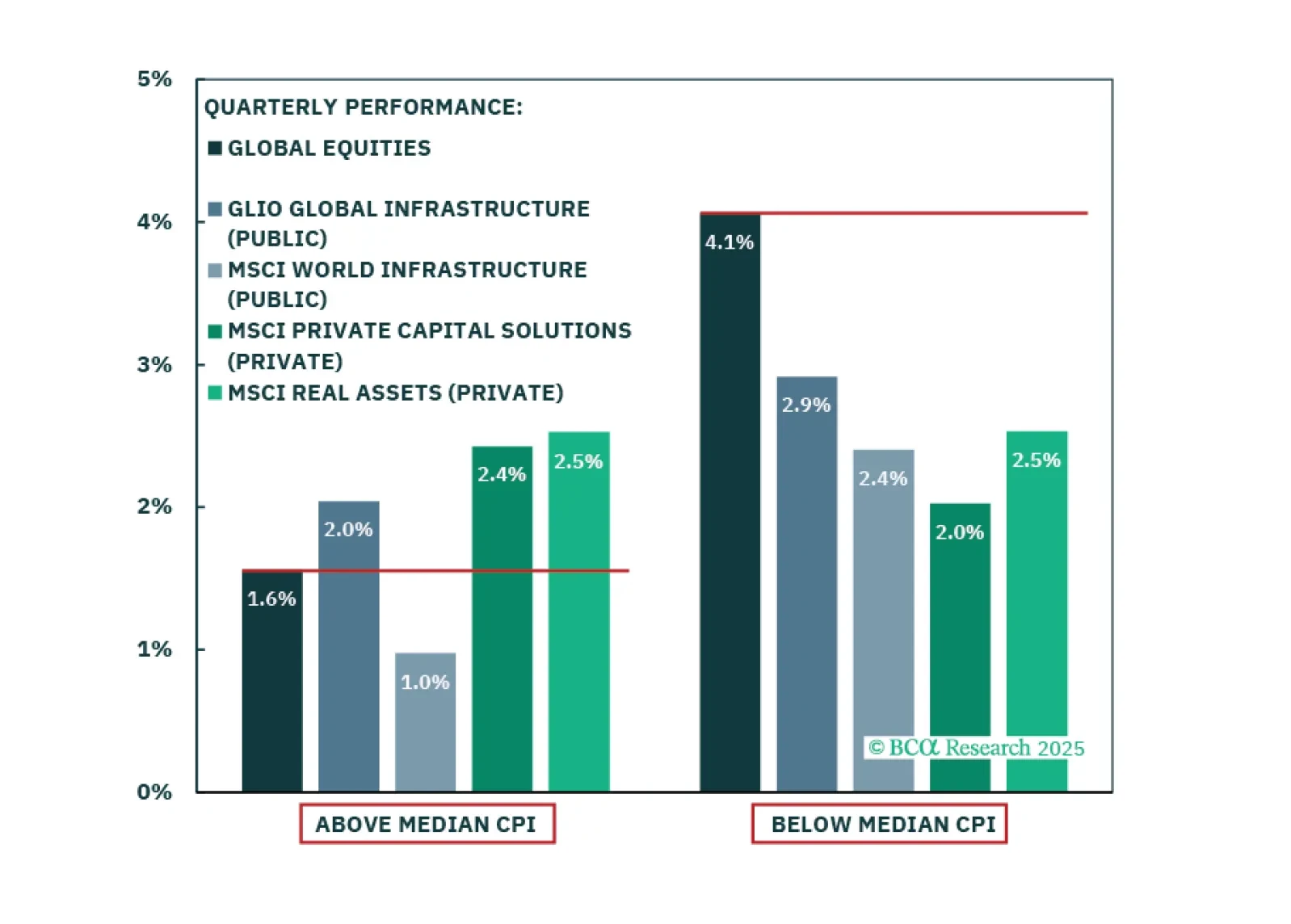

Private Infrastructure is superior to Public in both operational efficiency and inflation protection. However, current valuation spreads favor incremental Public deployment. Investors should consider a balanced approach between the two.

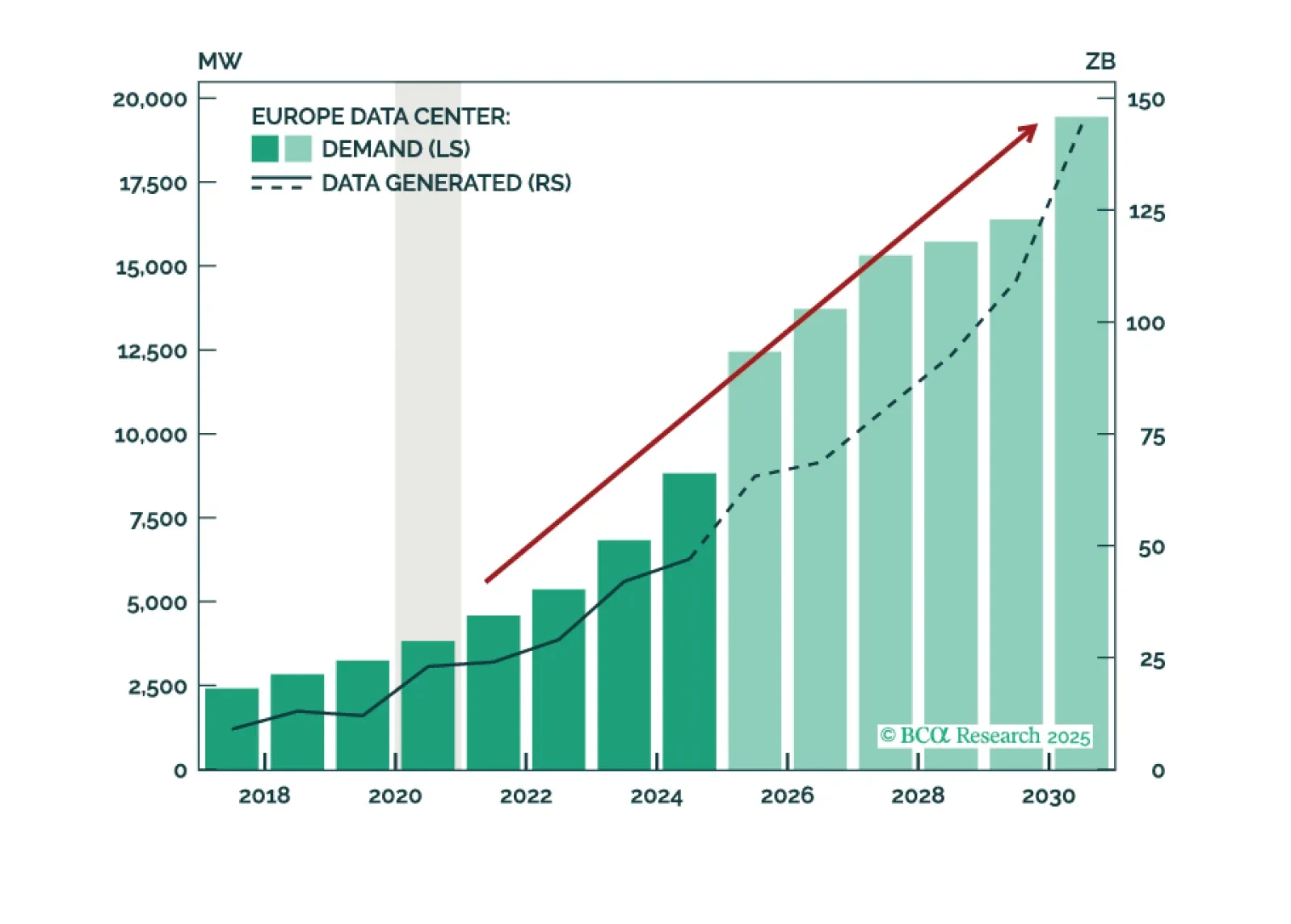

While the US is the pioneer, Europe will follow suit—more rapidly than expected. It is not a question of if GenAI will boom in Europe, but when. Europe’s Data Center growth is already strong today, but a US-style boom is just around the corner.

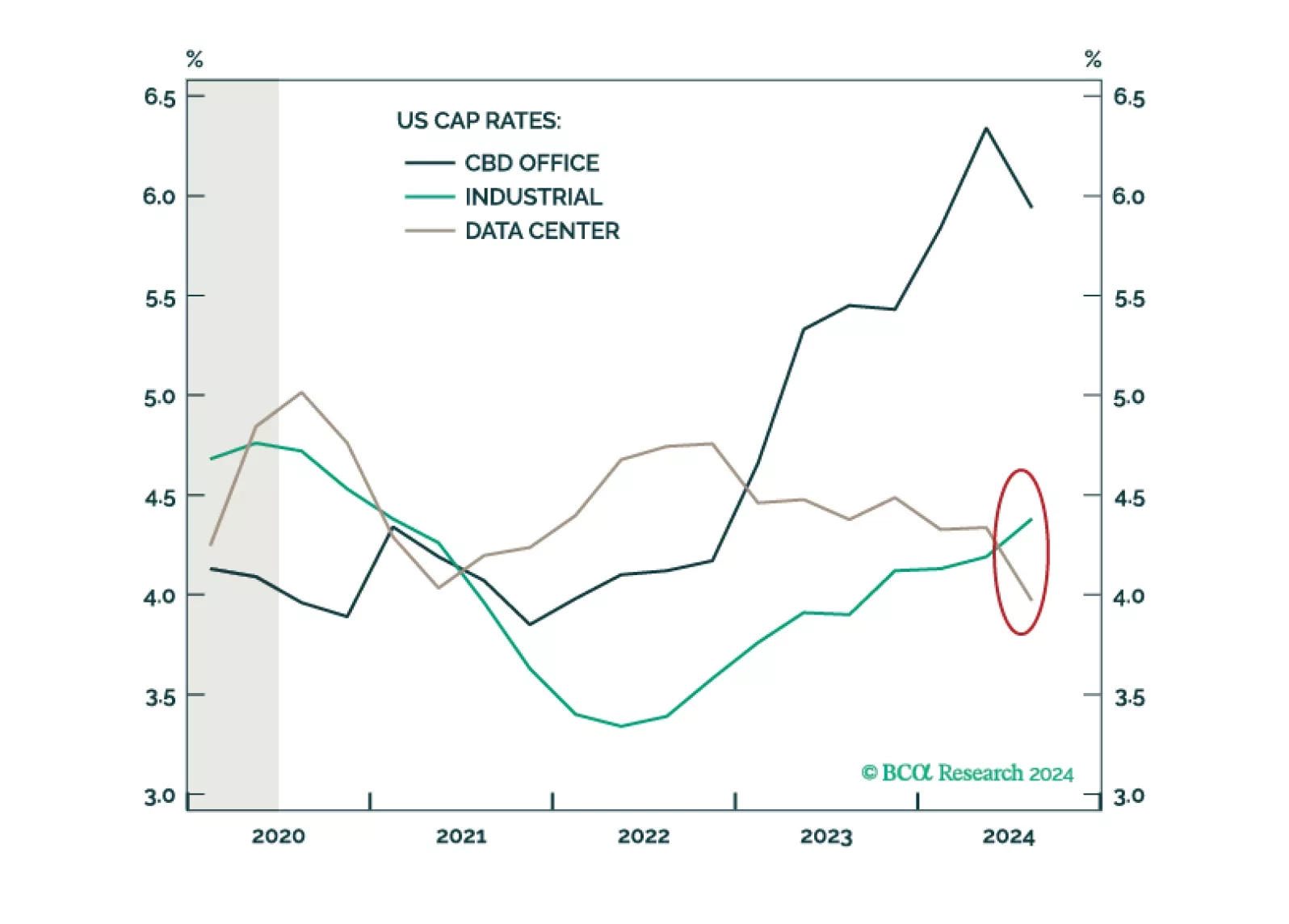

While AI deployment creates compelling investment opportunities, hyperscale facilities are not the only path forward. Investors should consider Office conversions into colocation Data Centers as the next dollar opportunity.