Private Equity

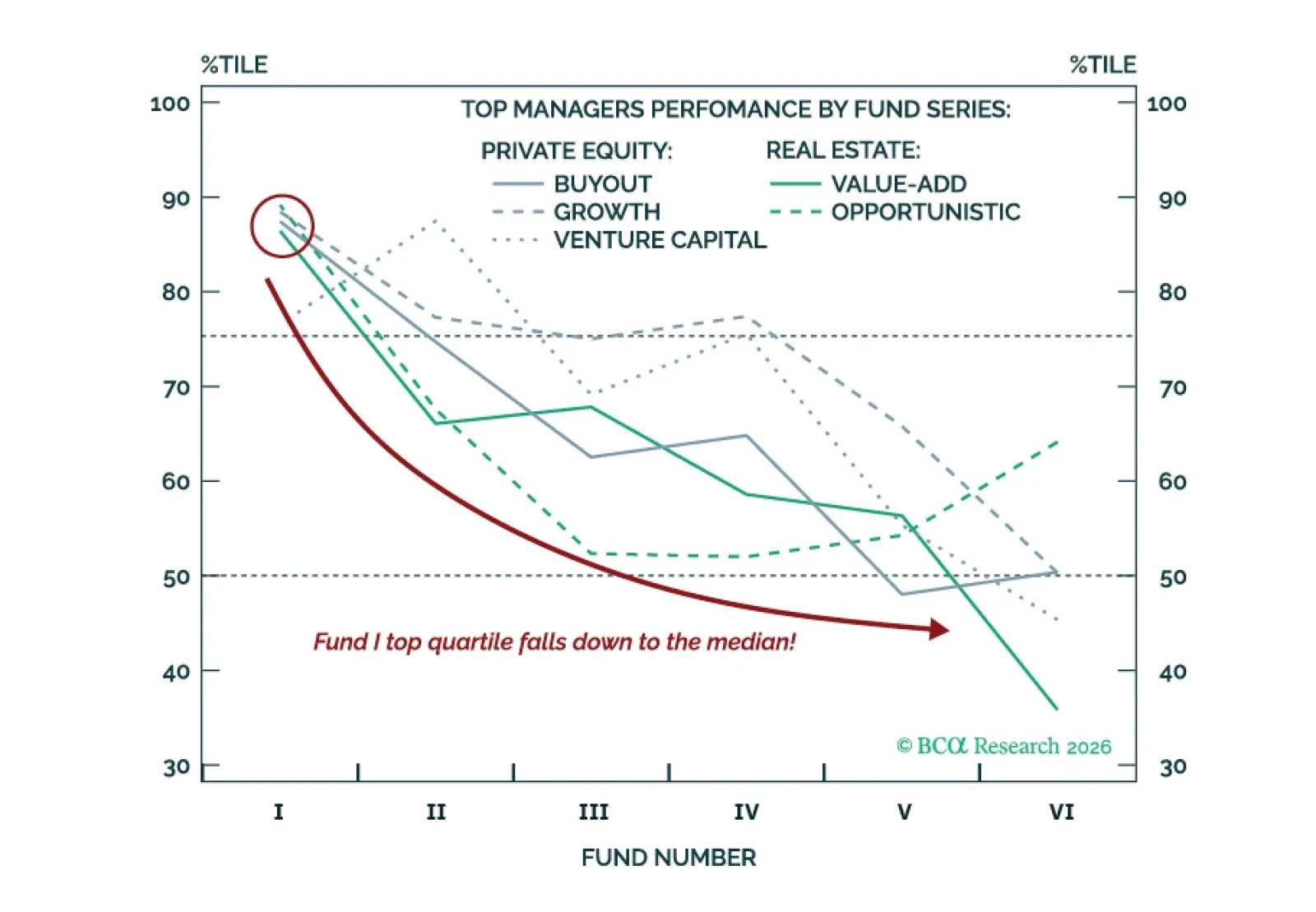

In Private Markets, yesterday’s winners often see outperformance fade. Top-quartile managers often regress toward the median as fund series mature. For investors evaluating the next Real Estate or Private Equity manager: Bias toward underweighting Funds V and beyond.

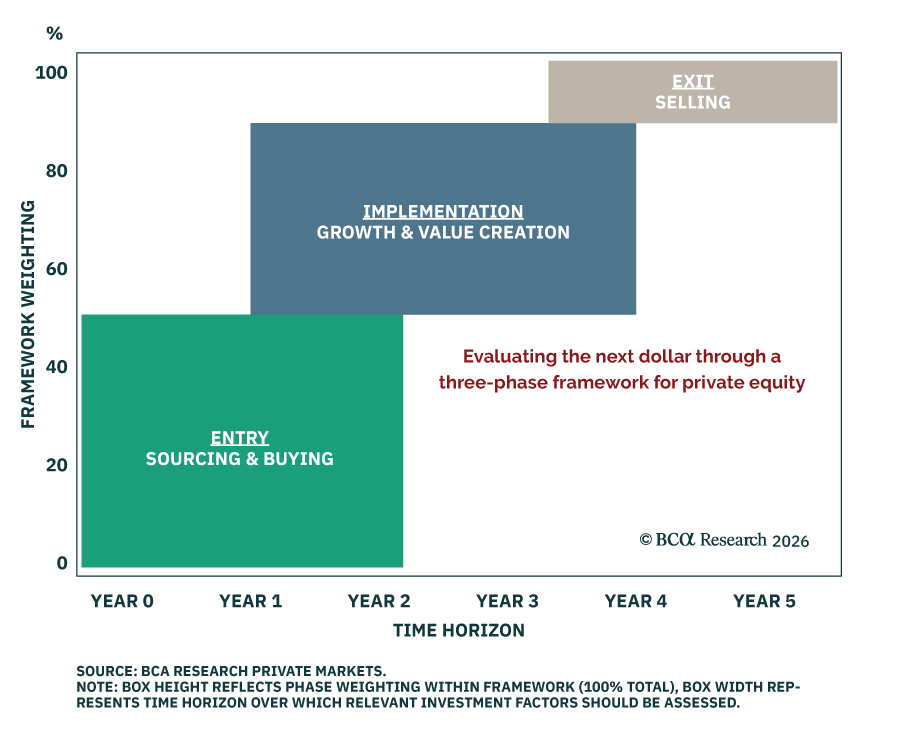

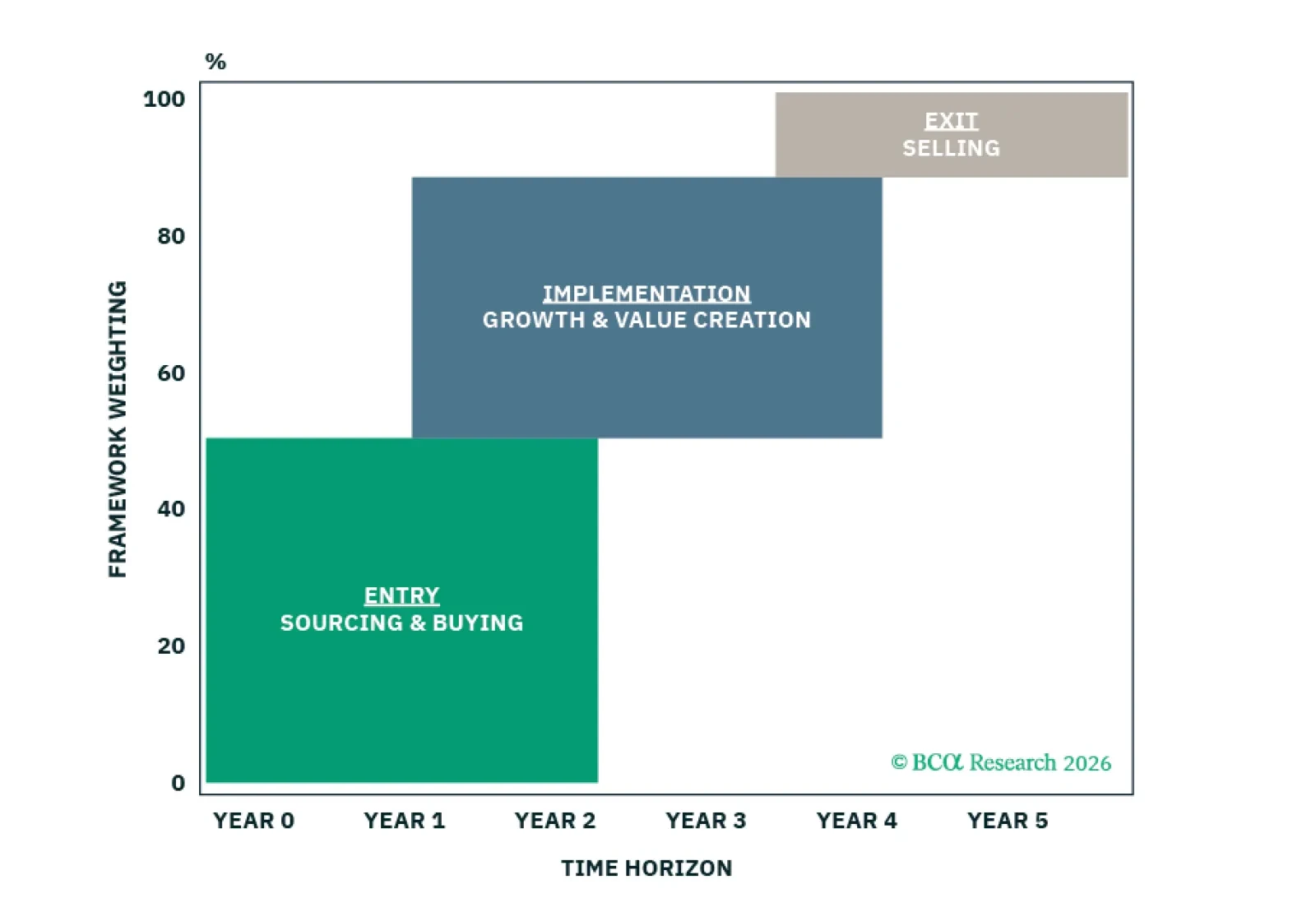

Private Equity fund vehicles may extend beyond 10 years, but the underlying assets that drive performance typically do not. We provide the framework for investors to capitalize on this reality.

M&A activity finally reaccelerated in Q4 2025—it’s just the start. Macro Hedge Funds have outperformed with top-decile performance from Discretionary Macro—but that’s towards the end. We move Macro from overweight to underweight and Event Driven from neutral to overweight.

Private Markets are entering a new phase as TPA and Evergreen funds expand. Shifts in access, implementation, and market leadership will have important implications for institutions, Wealth Management, and future Private Equity returns.

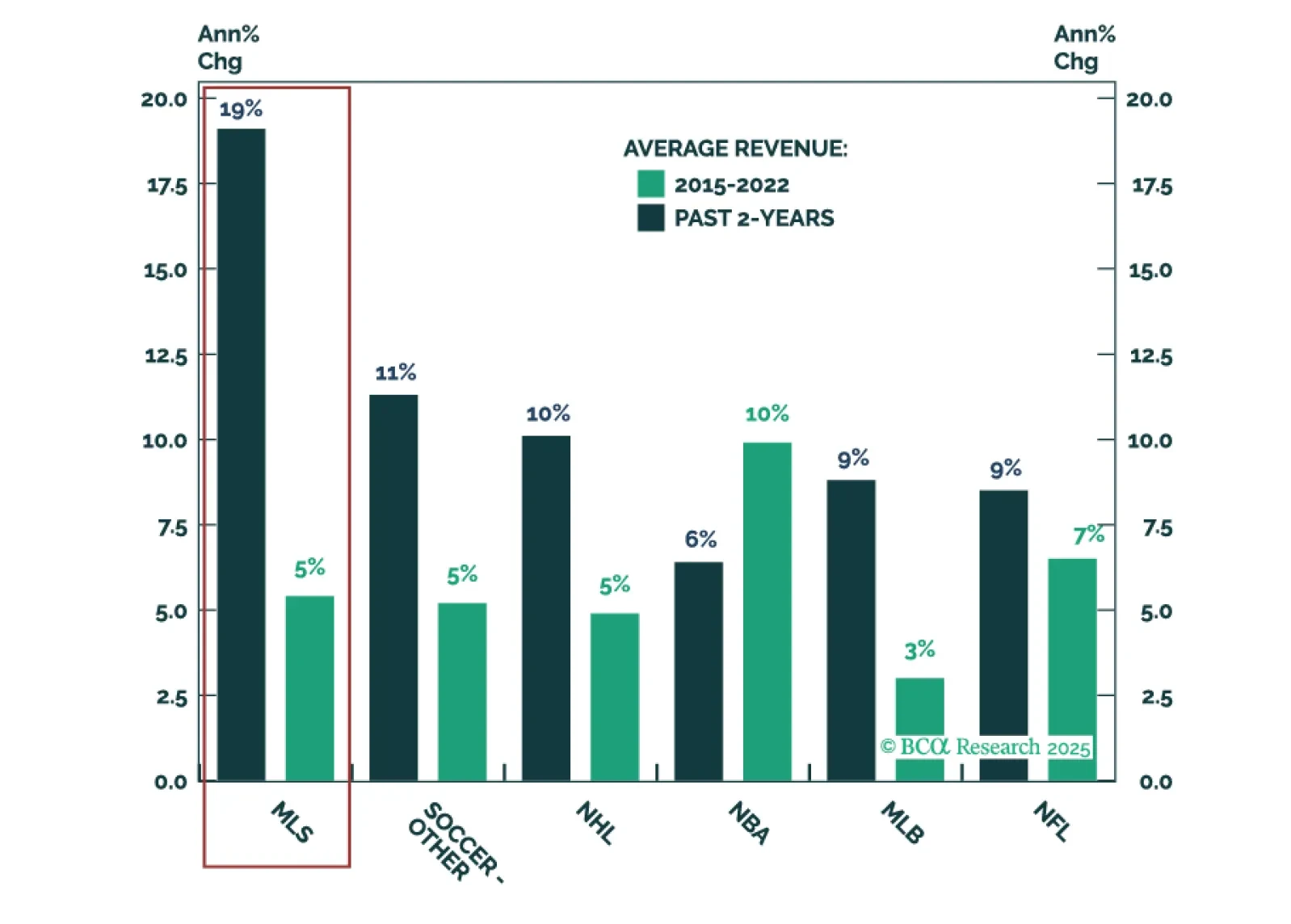

The NFL and NBA grab the headlines, but growth beats size. This report reveals the story behind Major League Soccer (MLS) growth. Valuations have jumped, yet plenty of upside remains—making the MLS relatively attractive compared to other US major leagues.

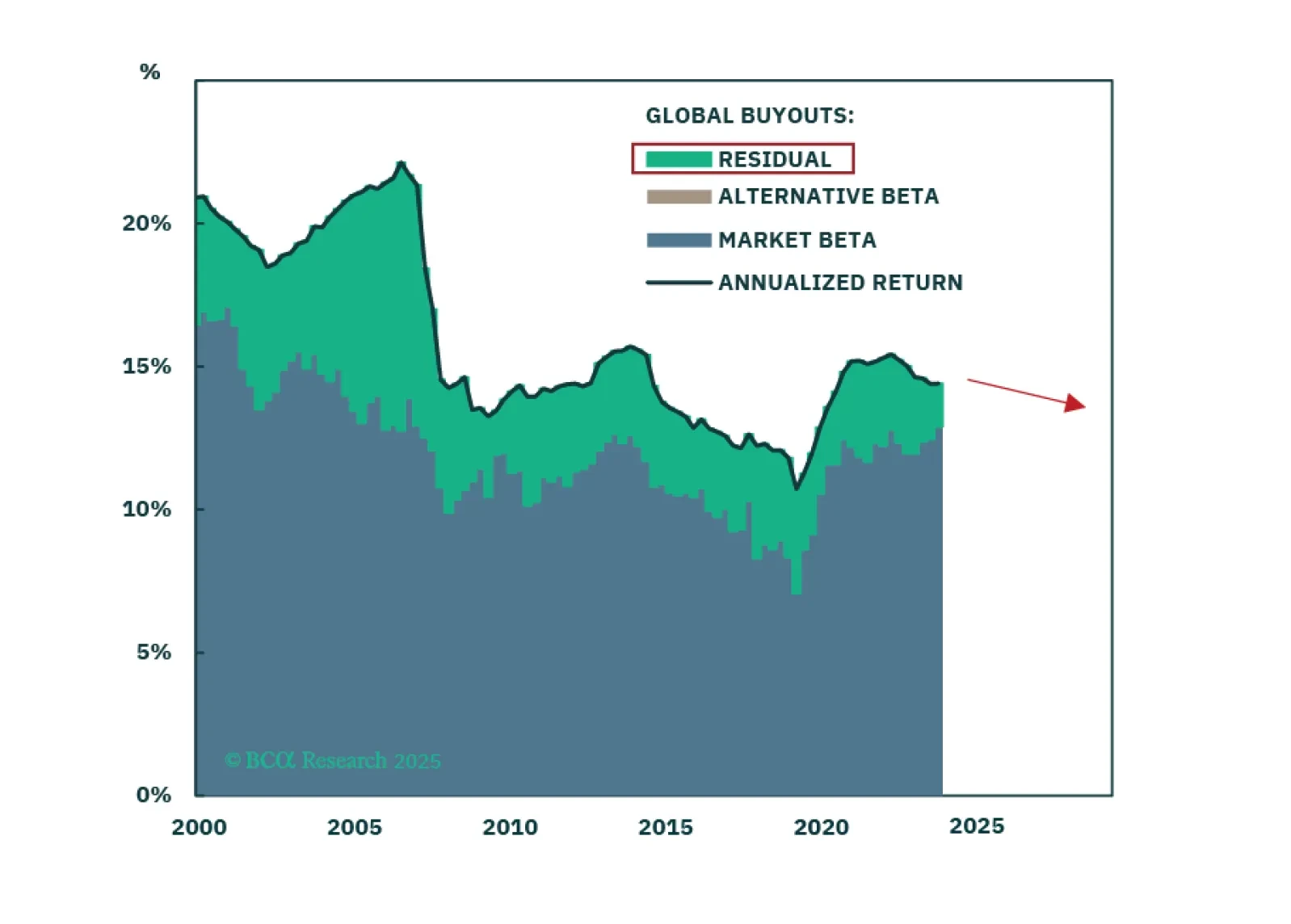

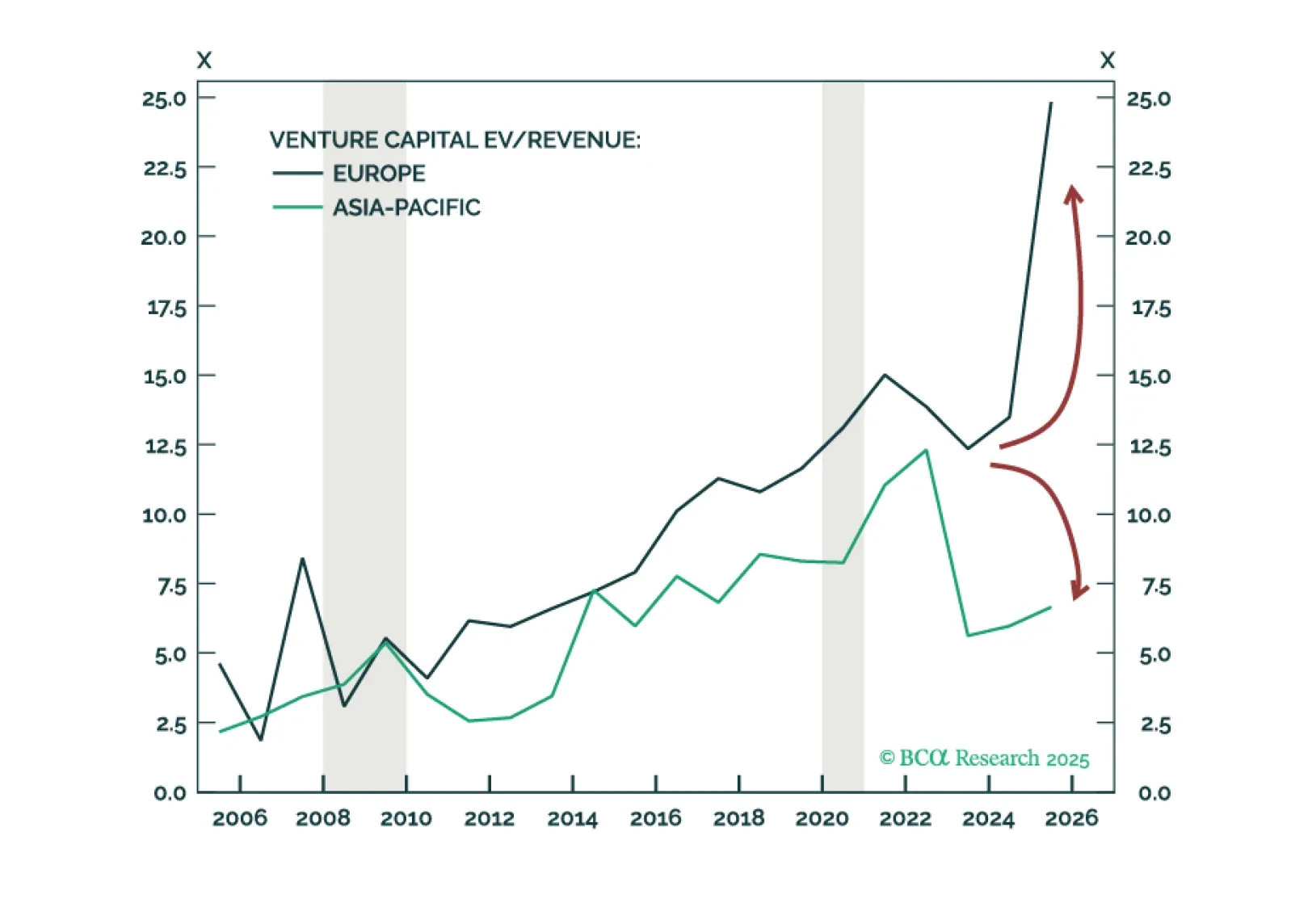

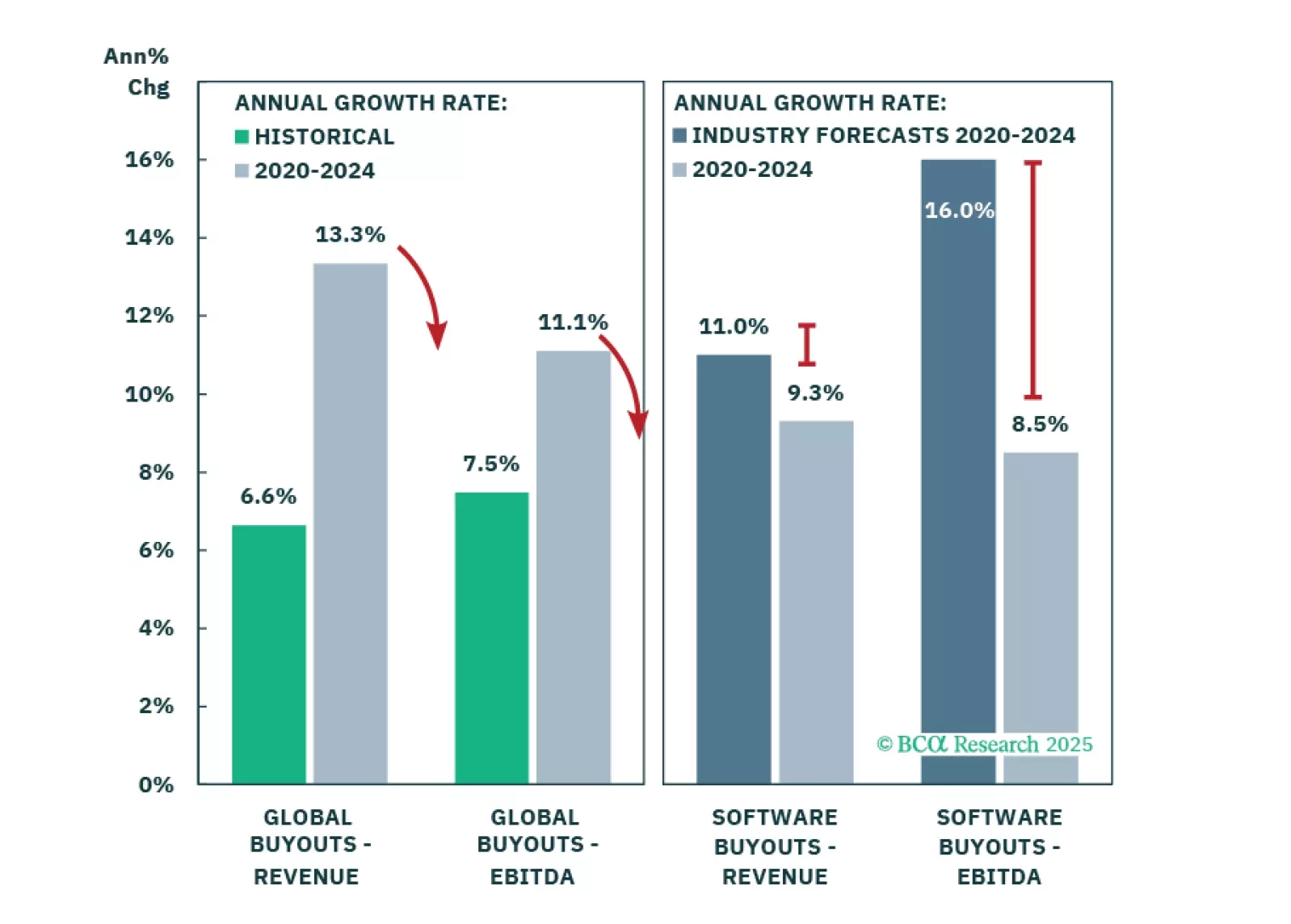

European euphoria is overdone. The most exceptional asset class in Europe is Infrastructure, but granular opportunities span other asset classes by sector and country. Venture Capital is a North America and Asia-Pacific play. We downgrade Private Credit, and upgrade Global Buyouts. Time to take profits on Long-Short Equity Hedge Funds.

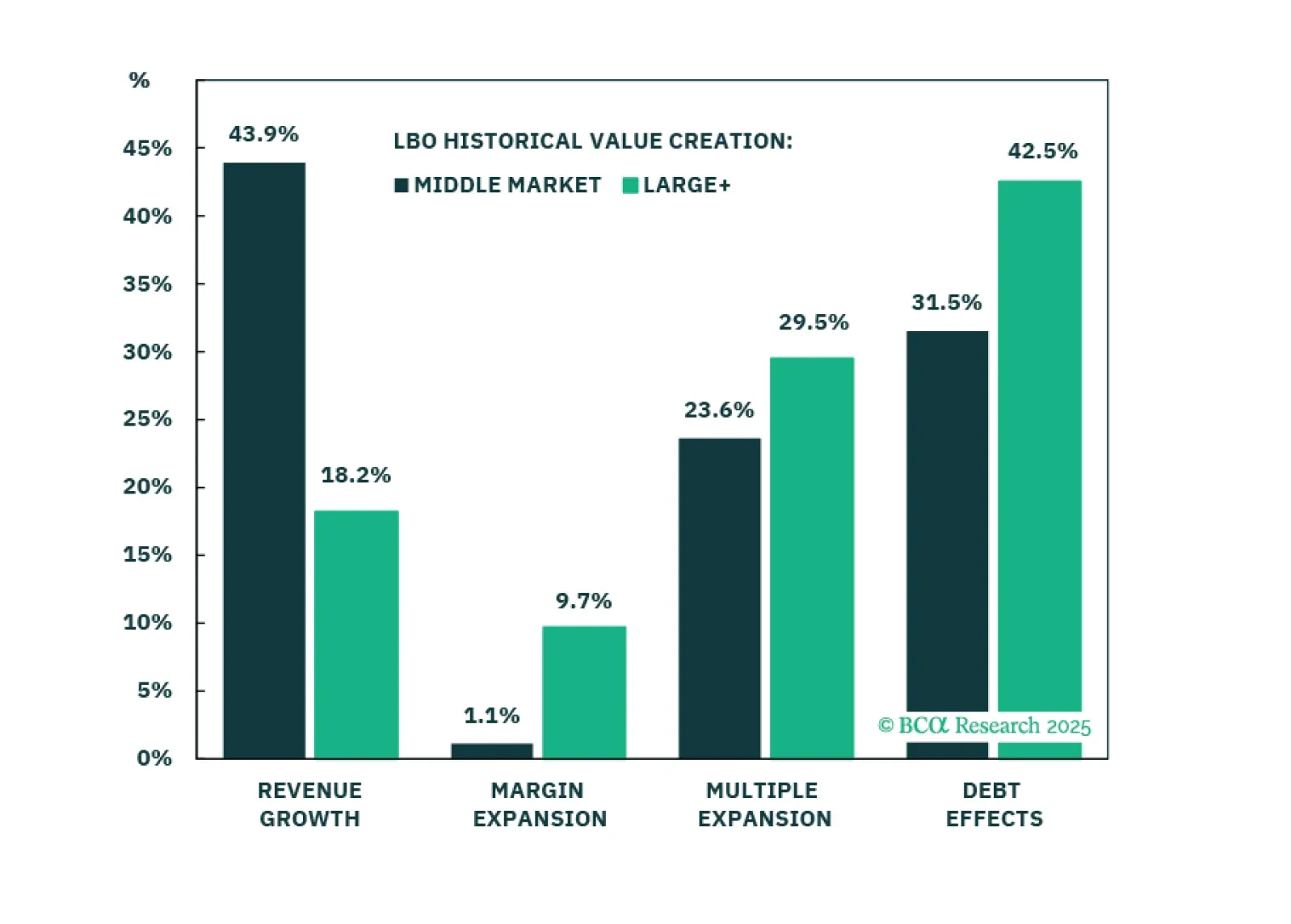

Return expectations have changed for Buyouts, but not equally for Large+ and Middle Market deals. While tariffs are dramatically reducing investor expectations, our return expectations are modestly increasing—with Large+ leading. In Part 2, we will tackle Private Credit.

Tariffs may trigger the recession, but the economy was already vulnerable from unsustainable growth and inflated expectations. Private Equity is most exposed, though this situation neither emerged suddenly nor will it unfold overnight. Our recommendations remain largely unchanged as market conditions increasingly align with our outlook.