Private Credit

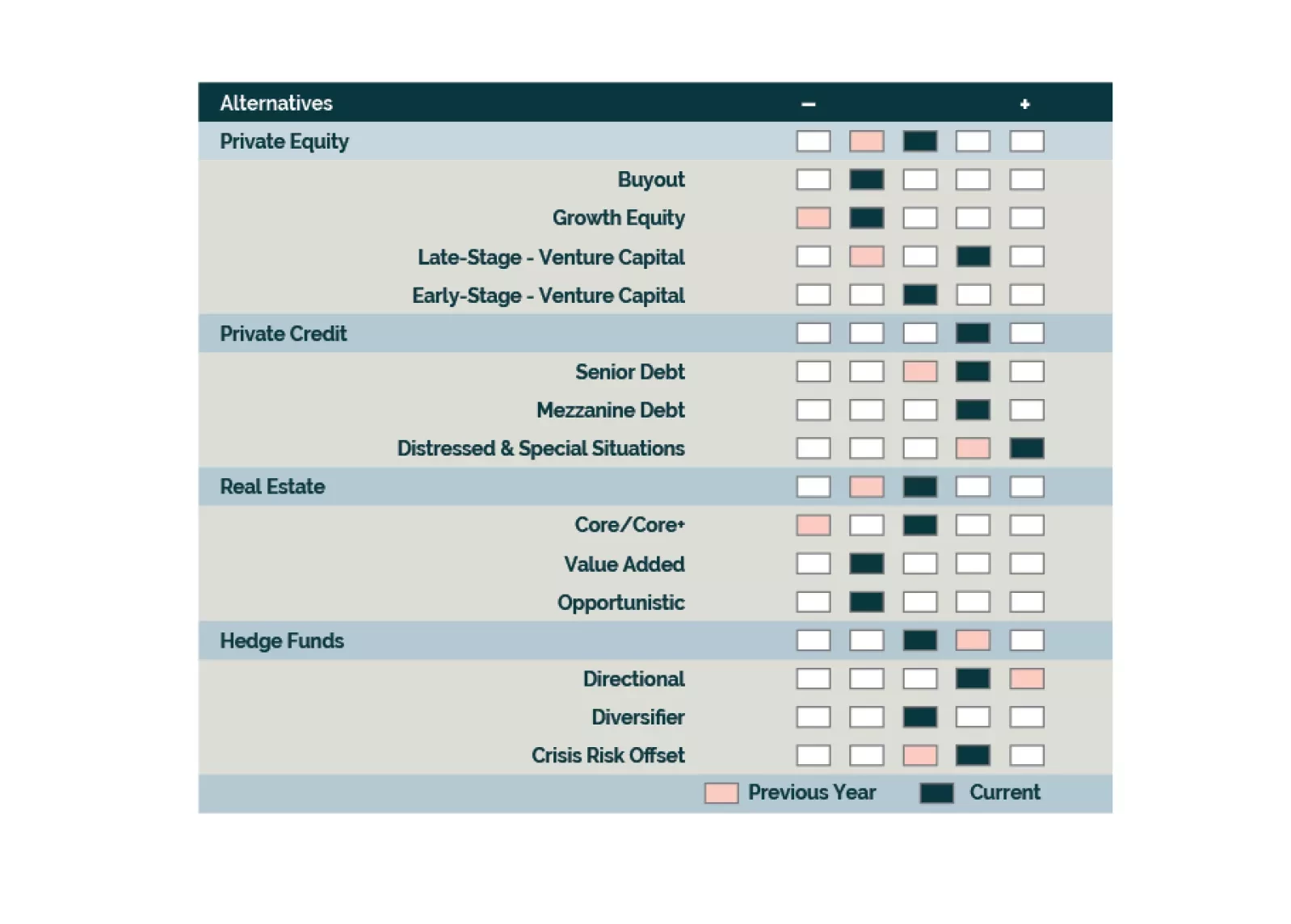

We are at a pivotal moment for Europe, supported by structural reforms and macro catalysts. While expanding credit markets and lower rates favor Private Equity over Private Credit, opportunities vary by segment. Large+ Buyouts are attractive as markets have priced in structural challenges. We downgrade Europe Private Credit, remain neutral on Europe Private Equity broadly but overweight Europe vs. North America in PE portfolios.

Asset class expectations show mixed shifts from 2024, with Real Estate seeing substantial upgrades and Private Equity benefiting from Venture Capital improvements. Private Credit return expectations decline from 2024 but remain relatively attractive. Infrastructure shows varied dynamics across sub-strategies, with Value-Add offering strong return potential. Within Hedge Funds, Long-Short Equity shows higher tactical returns while Multi-Strategy leads strategic projections.

We are growing positive on Growth assets with recession expectations increasing our optimism on entry points. Equities are led by APAC Private Equity, North America Venture Capital, and Europe Buyouts. Our outlook continues to improve on CRE within the Inflation & Diversification bucket while we are underweight Multi-Strategy amongst Hedge Funds. We maintain an overweight to Senior Direct Lending for Income with a preference for North America.

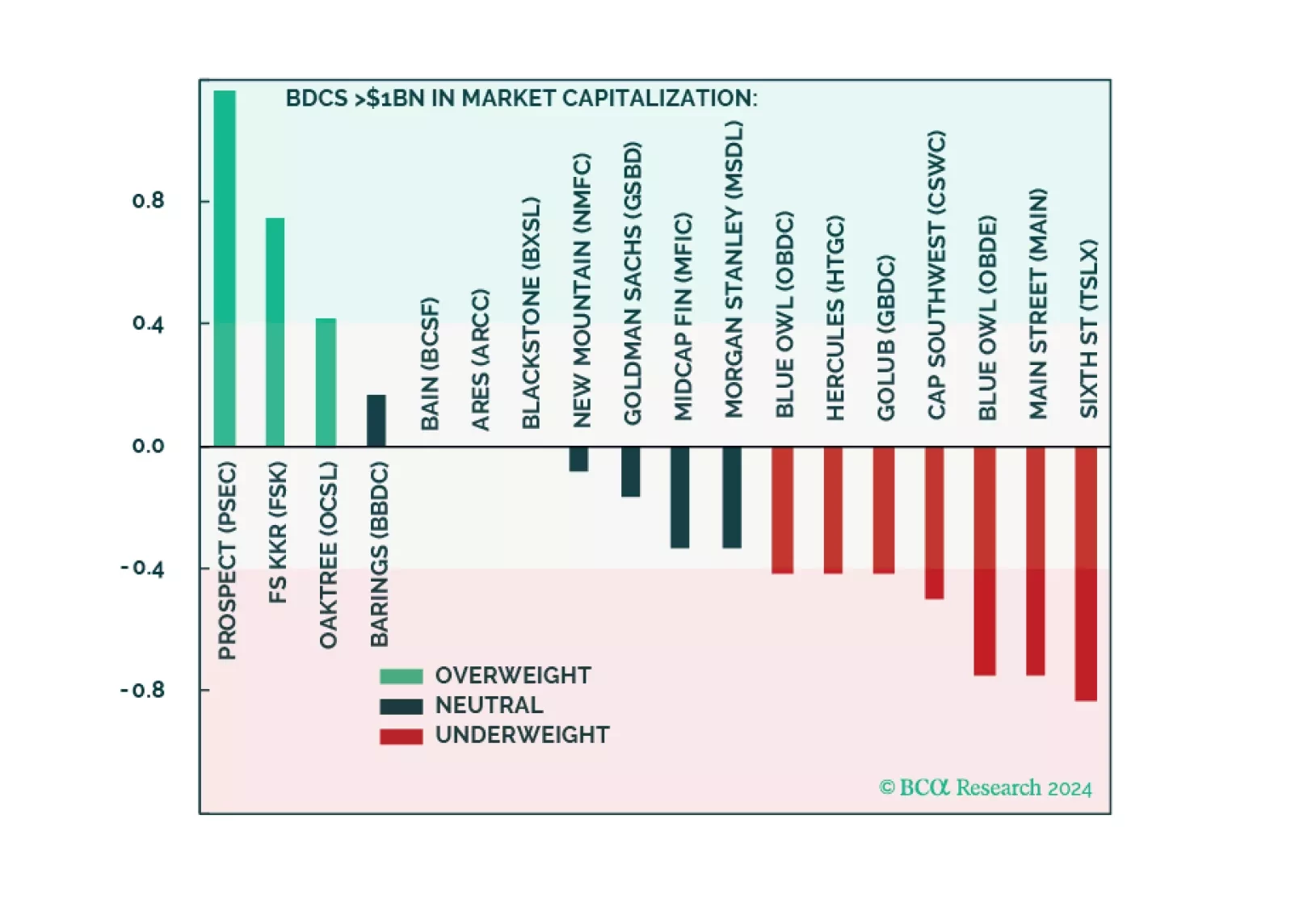

We are positive Private Credit but currently underweight Public BDCs. Today’s market pricing and sentiment in BDCs are excessively optimistic. Long-term investors should await a better entry point. Traders may find an attractive short. This report also peels back the Public BDC onion and presents over/underweights across individual BDCs via our filtering methodology.

Also included at the end of this report is an updated presentation titled 'Private Credit: Drivers Of The Boom And Understanding Risks On The Horizon,' recently presented at GII’s Private Credit Roundtable in Australia. It features updated charts and additional analysis.

We go overweight Late-Stage Venture Capital and APAC Private Equity but remain underweight North America Buyouts. We maintain our neutral outlook towards Hedge Funds and are positive on Long-Short Equity, Event Driven, and CRO strategies. We are cooling towards Direct Lending strategies as competition and relative opportunities increase. CRE’s downturn continues to unfold; we are starting to be buyers.

Investors should be tactically tilting allocations towards Direct Lending, Distressed Debt, and Directional Hedge Fund strategies at the expense of Real Estate, Private Equity, and Diversifier Hedge Funds. Structural opportunities are emerging in Real Estate and Venture Capital.

We see challenges ahead for Global Buyout across geographies as valuations need further resetting. While we are concerned with capital controls and flight risk in Asia-Pacific Venture Capital, the upside potential from AI may be worth a look. The current entry point for Private Credit is opportune across North America and Europe with the distressed pipeline building. Real Estate does not look appealing with the macro and relative opportunity set driving our underweight. Hedge Funds have a favorable backdrop in the near-term, although prospects differ across Directional, Diversifier, and Crisis Risk Offset strategies.

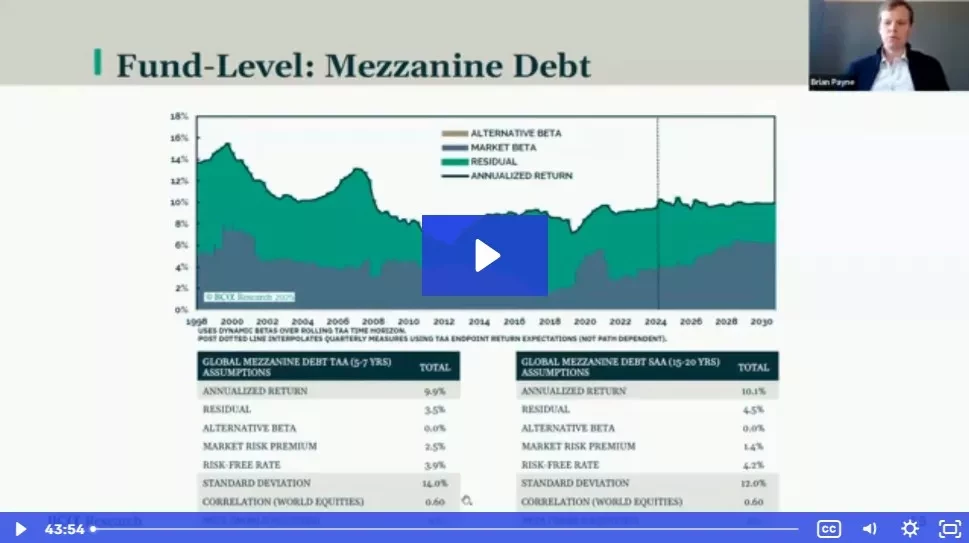

We are overweight Private Credit. Improvements in yield, negotiating leverage, and structuring upside are major tailwinds over the coming years. The business cycle provides an attractive backdrop for all Private Credit sub-asset classes. In this Special Report we examine Private Credit as a whole, but with more emphasis on the income-focused sub-categories of Senior and Mezzanine Debt.