Private Credit

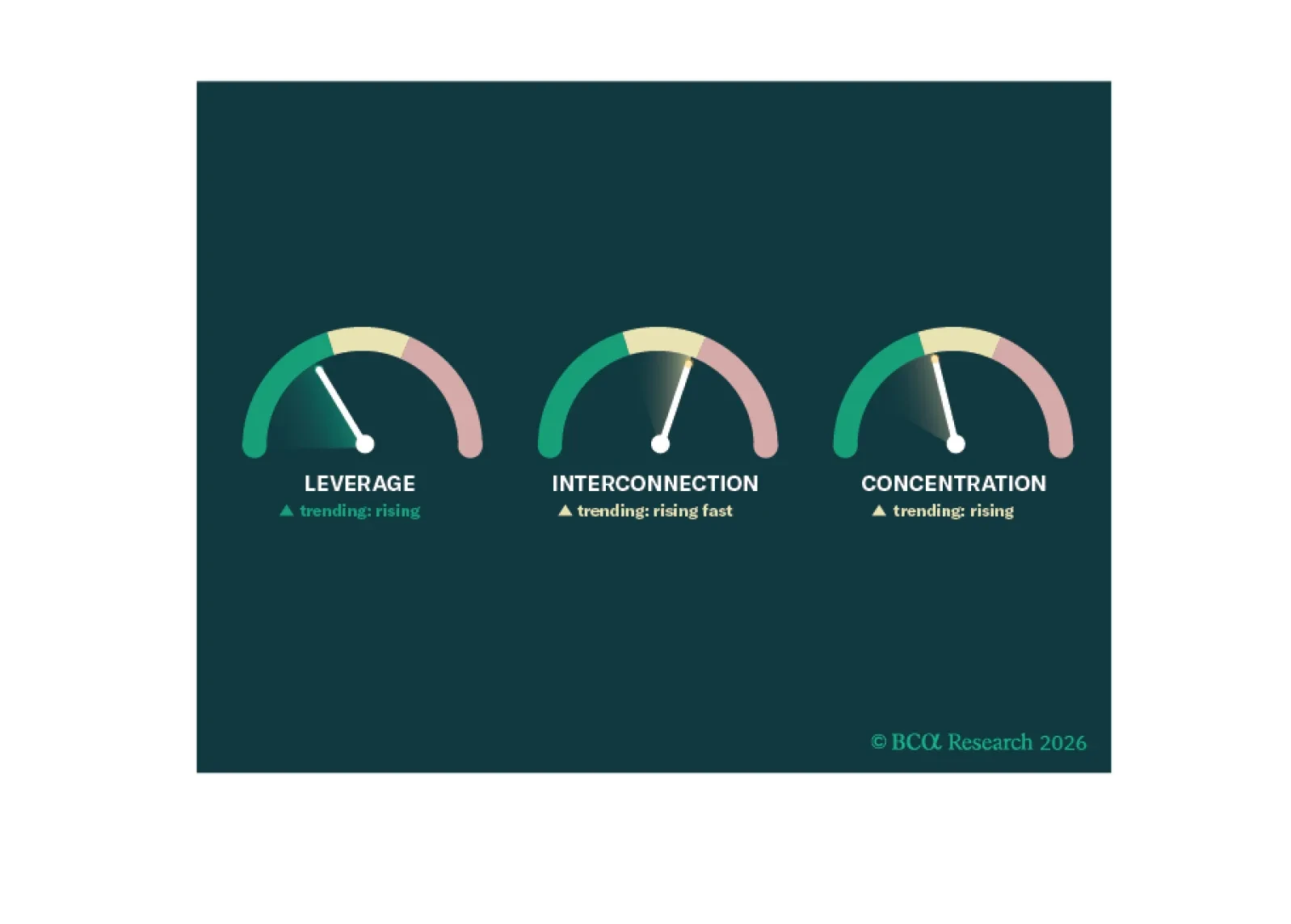

Today's concerns about Private Credit are overstated. We provide our three-criteria framework that investors can use to track Private Credit's doomsday risk. Systemic crises build over years and decades. In Private Credit, that build is happening now.

Everyone has opinions on Private Credit, but few have the data, and fewer have the objectivity. We give you both. In under 5 minutes, you will understand how we got here and, more importantly, how to allocate from here.

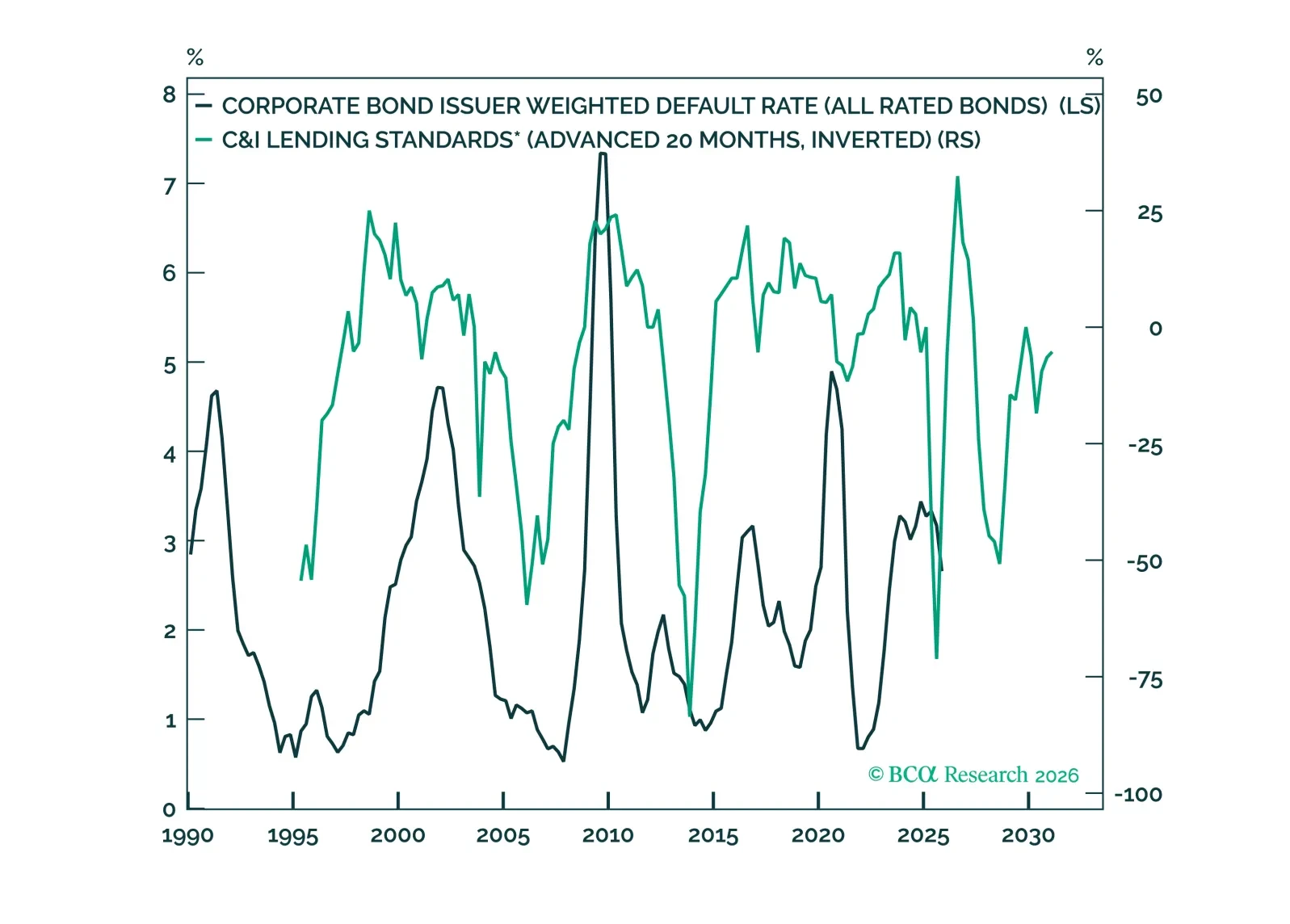

The turmoil in private credit is a wild card, but our traditional suite of credit cycle indicators does not point to an imminent spread-widening episode. We reiterate our benchmark weightings on Treasuries, investment-grade and high-yield corporate bonds.

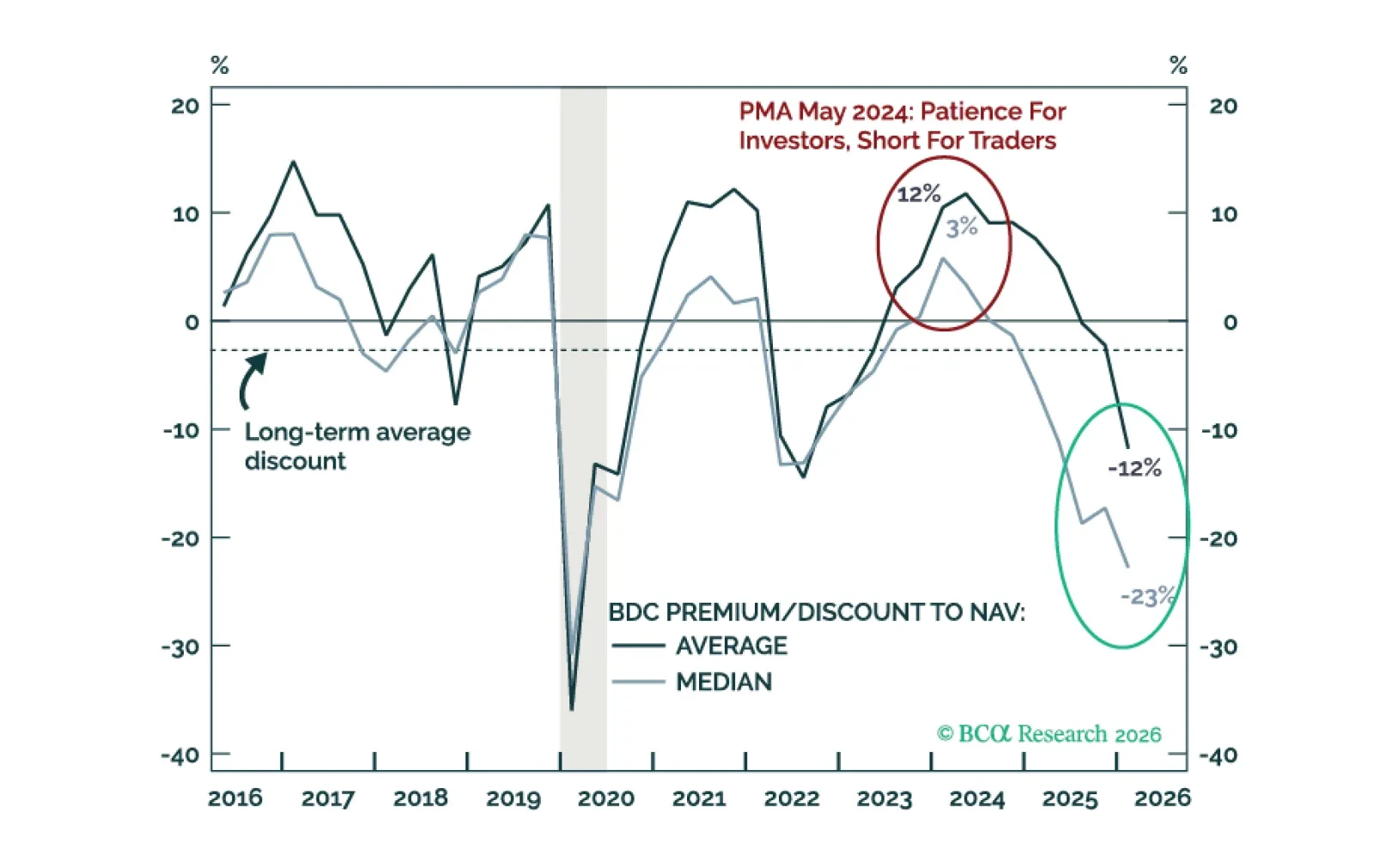

The 2026 next dollar playbook is about cross-asset relative-value investing. We move underweight Private Credit but not for reasons investors expect–BDCs are now longs. We shift to overweight Infrastructure and real assets more broadly–Publics included.

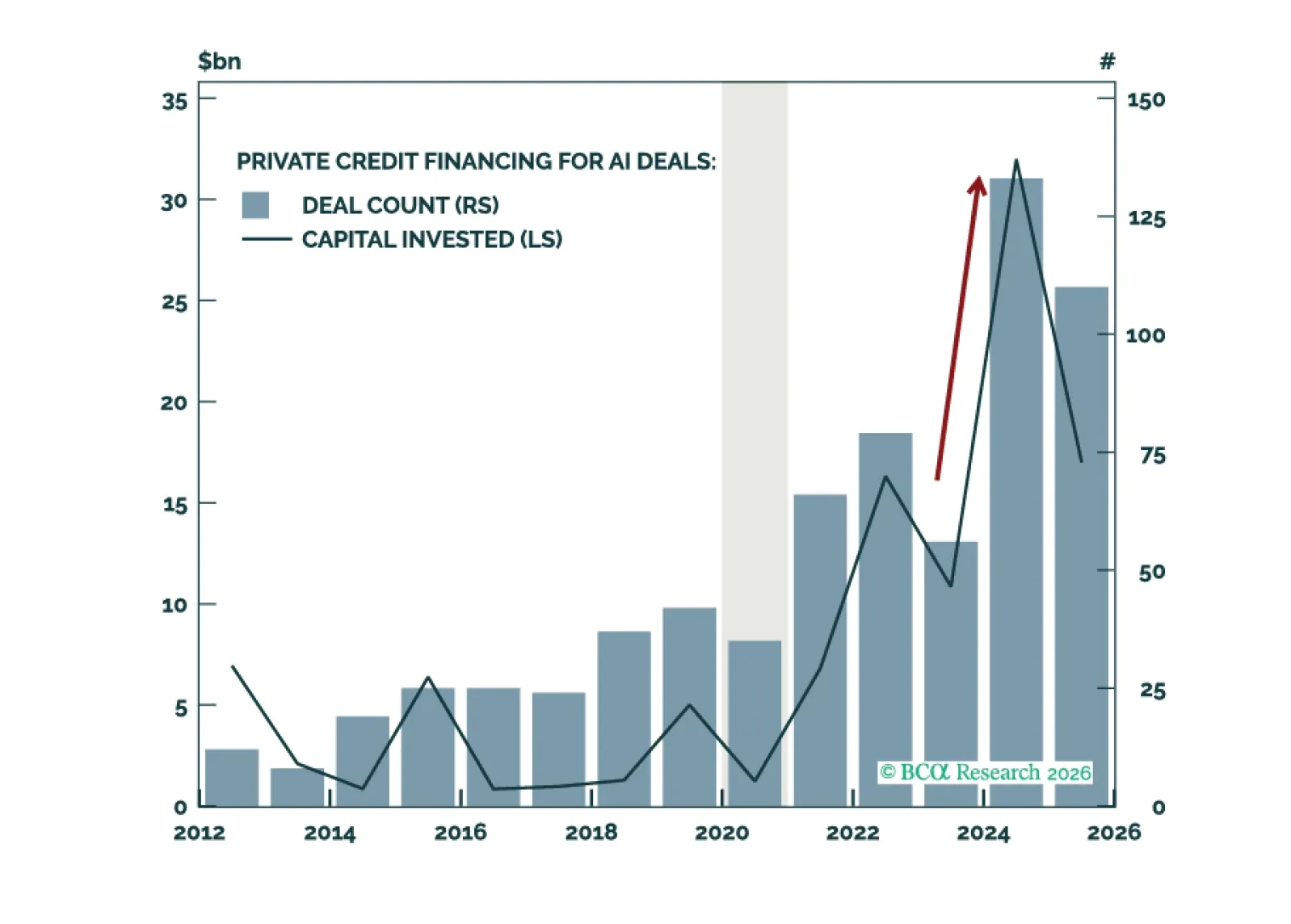

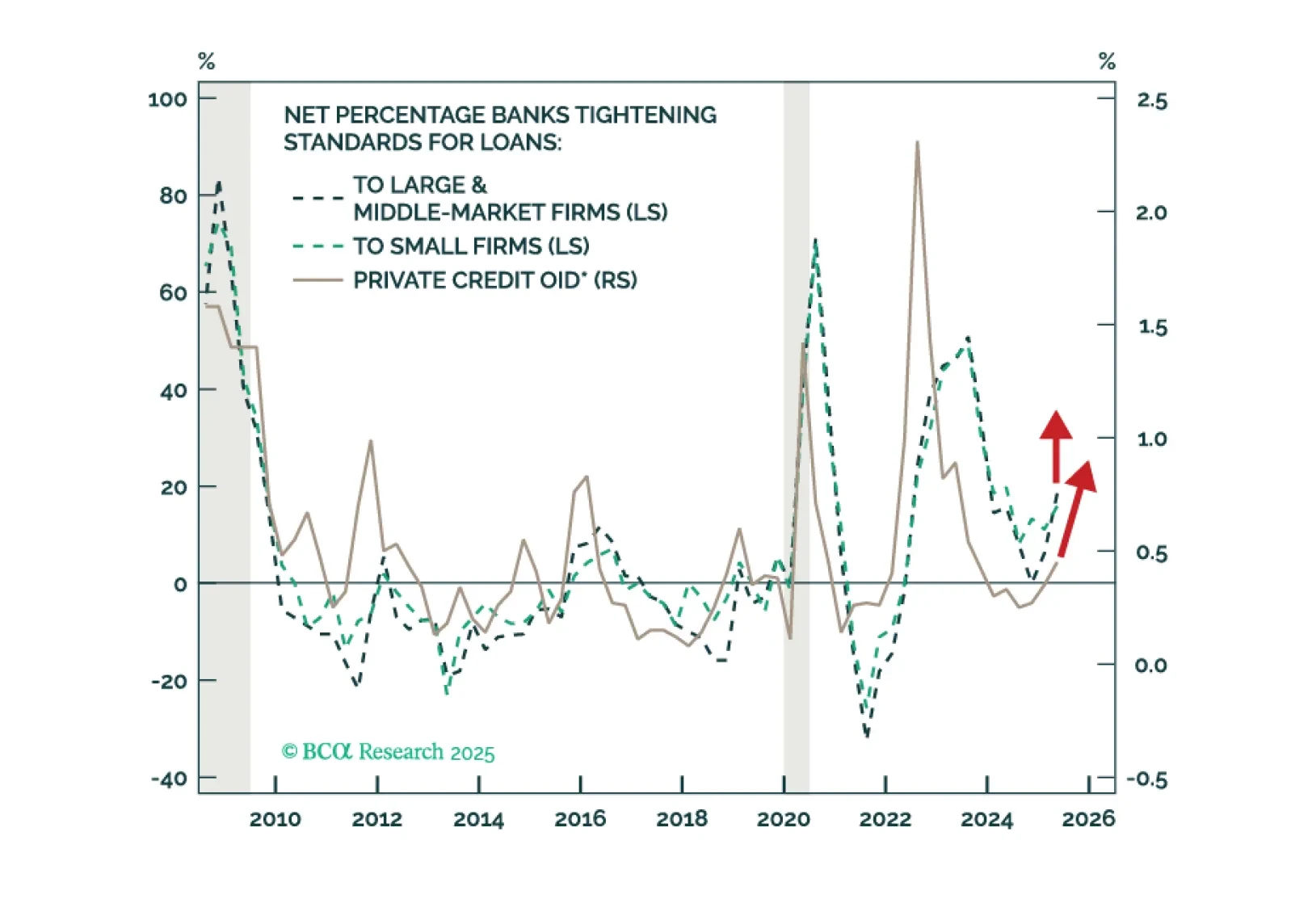

The AI trade has broadened beyond Public Markets, pulling Private Credit deeper into the ecosystem. Investors are right to understand their overlapping exposures between Public Equities, Venture Capital, Data Centers, and now Private Credit. However, risks from rising Venture Capital Debt and Asset-Based Lending are going unnoticed.

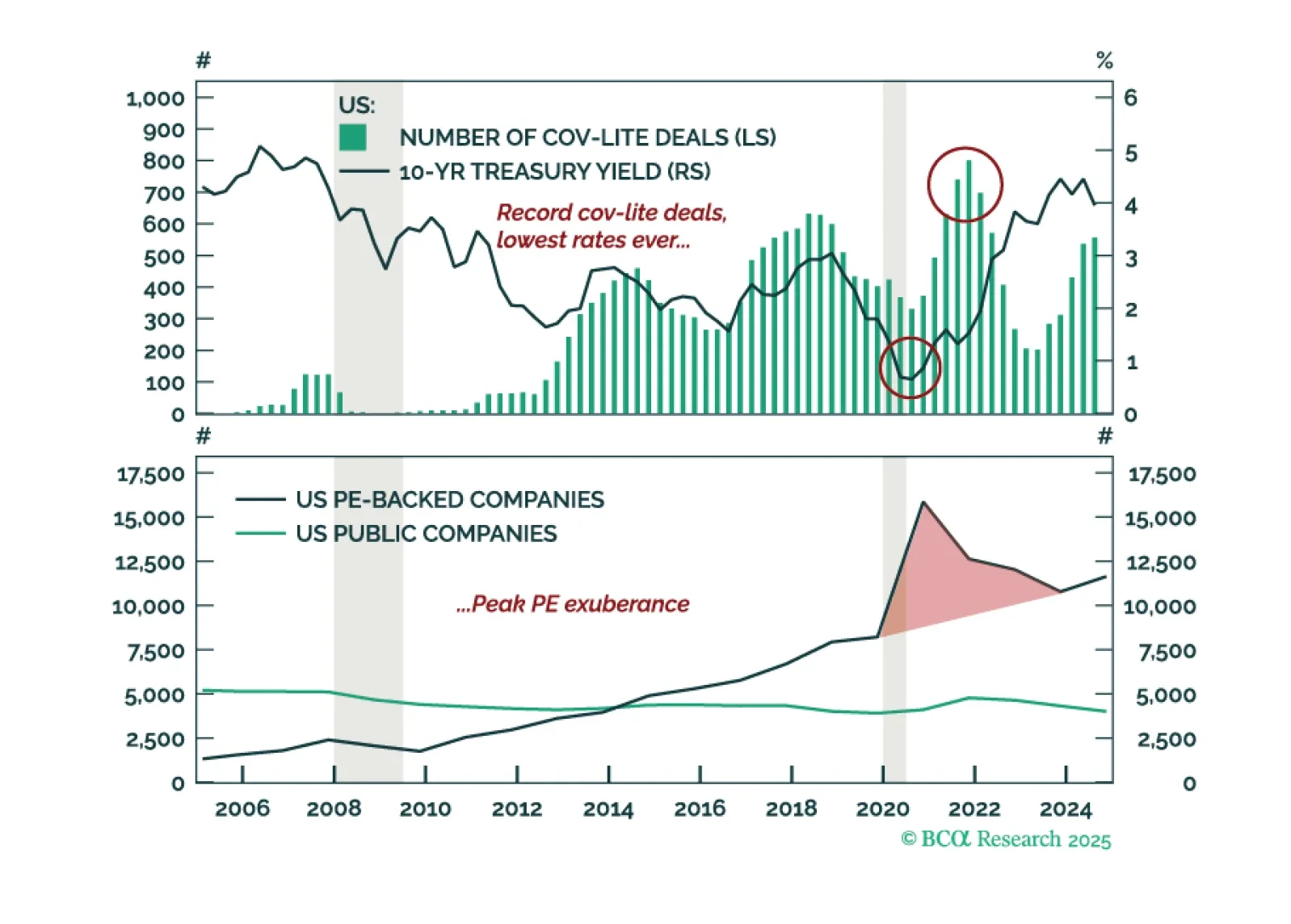

Private Credit outsiders are skeptical, insiders are believers—but are becoming nervous now. In the highlight of this Quarterly Report, we dig beneath the surface to uncover the buried bodies in Private AND Public Credit. The ghosts of 2020-2021 loan originations are catching up with investors.

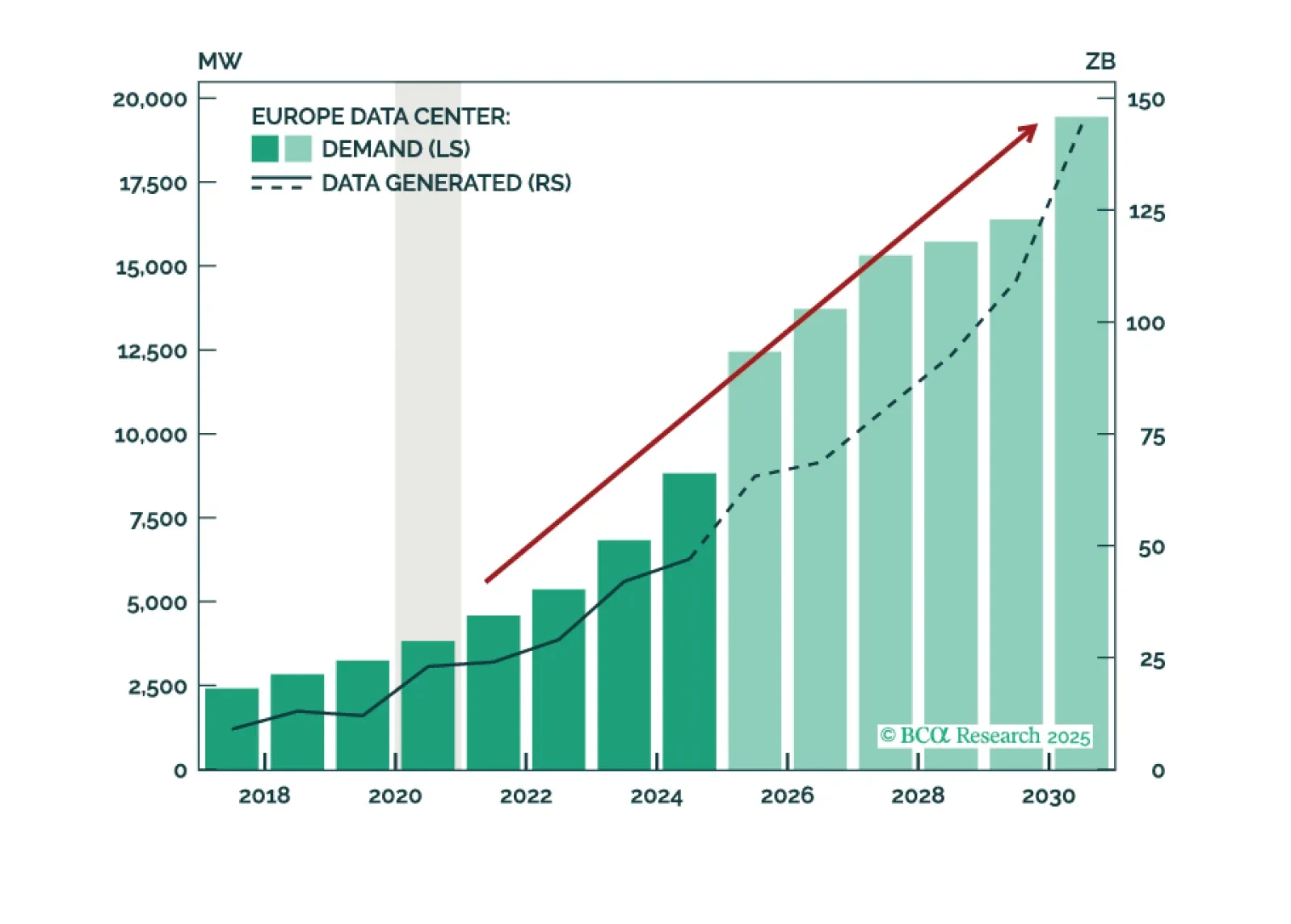

While the US is the pioneer, Europe will follow suit—more rapidly than expected. It is not a question of if GenAI will boom in Europe, but when. Europe’s Data Center growth is already strong today, but a US-style boom is just around the corner.

Private Credit return expectations edge lower. Middle Market Direct Lending remains attractive, rivaling Middle Market Buyouts.

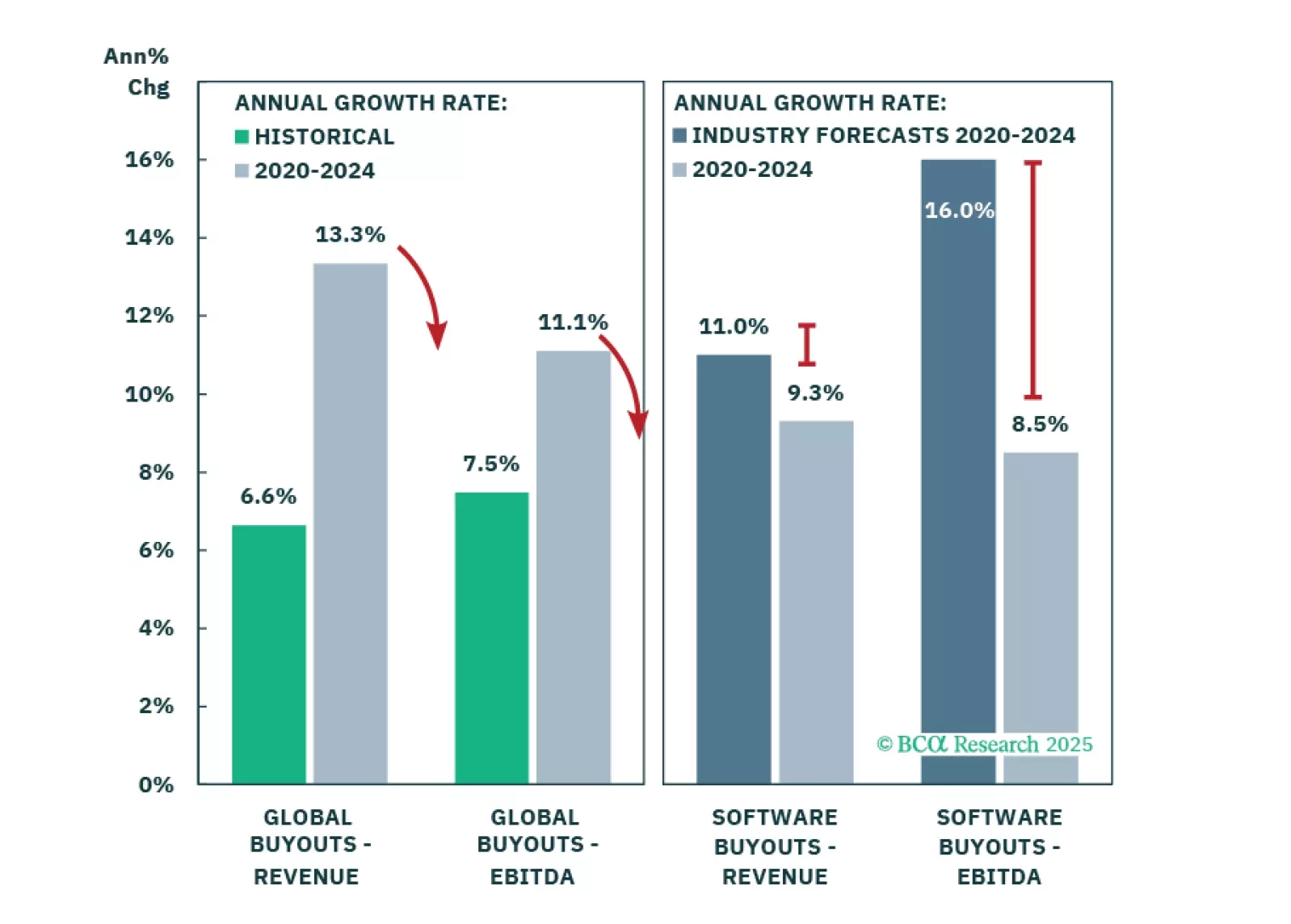

Tariffs may trigger the recession, but the economy was already vulnerable from unsustainable growth and inflated expectations. Private Equity is most exposed, though this situation neither emerged suddenly nor will it unfold overnight. Our recommendations remain largely unchanged as market conditions increasingly align with our outlook.