Policy

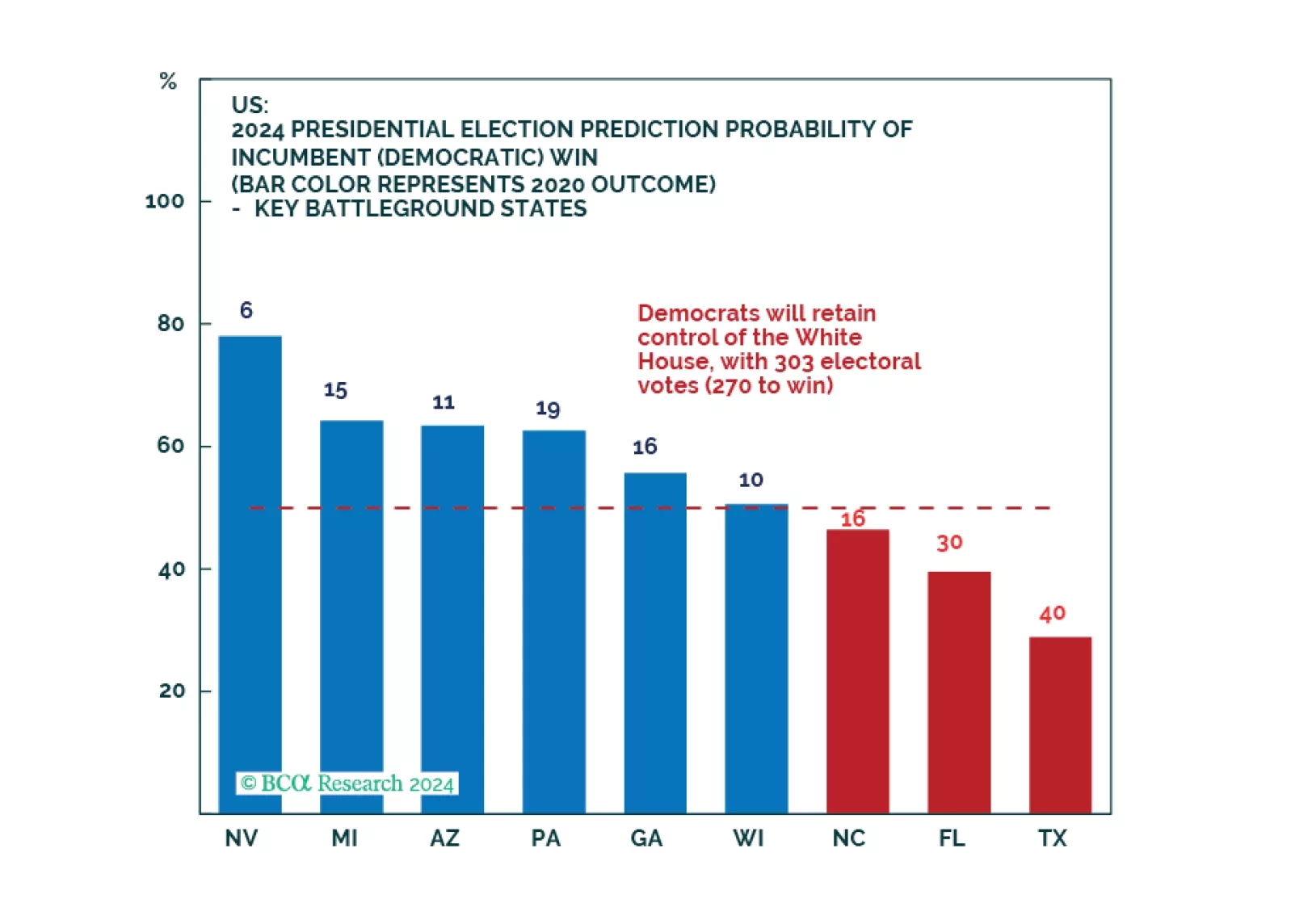

Democrats will not win a full sweep and implement drastic new tax hikes. However, our quant model still favors them to win the White House and just upgraded their odds. While we expect equity volatility around the election, investors do not need to worry about corporate tax hikes.

US nominal personal income growth accelerated from 0.2% m/m to 0.3% in July, faster-than-anticipated, whereas personal spending accelerated from 0.3% to 0.5%, in line with expectations. The savings rate edged lower from 3.1% to a 16-year-low of 2.9%. …

After surprising to the upside in July on higher energy costs, Eurozone CPI resumed its deceleration in August. Headline and core CPI declined from 2.6% y/y to 2.2% and from 2.9% to 2.8%, respectively. Energy prices contracted 0.3% y/y from July’s 1.2%…

Tokyo’s CPI is a timely leading indicator of nationwide price pressures. In August, the headline, core (ex-food) and the “core core” (ex-food and energy) measures all accelerated by larger-than-expected margins, reaching 2.6%, 2.4% and 1.6% y/y, respectively.…

Chinese onshore and offshore bank stocks have outperformed their respective broad markets by 26% and 24% since October. Despite deteriorating return on assets, return on equity and net interest margins, investors have sought out their high dividend yields and…

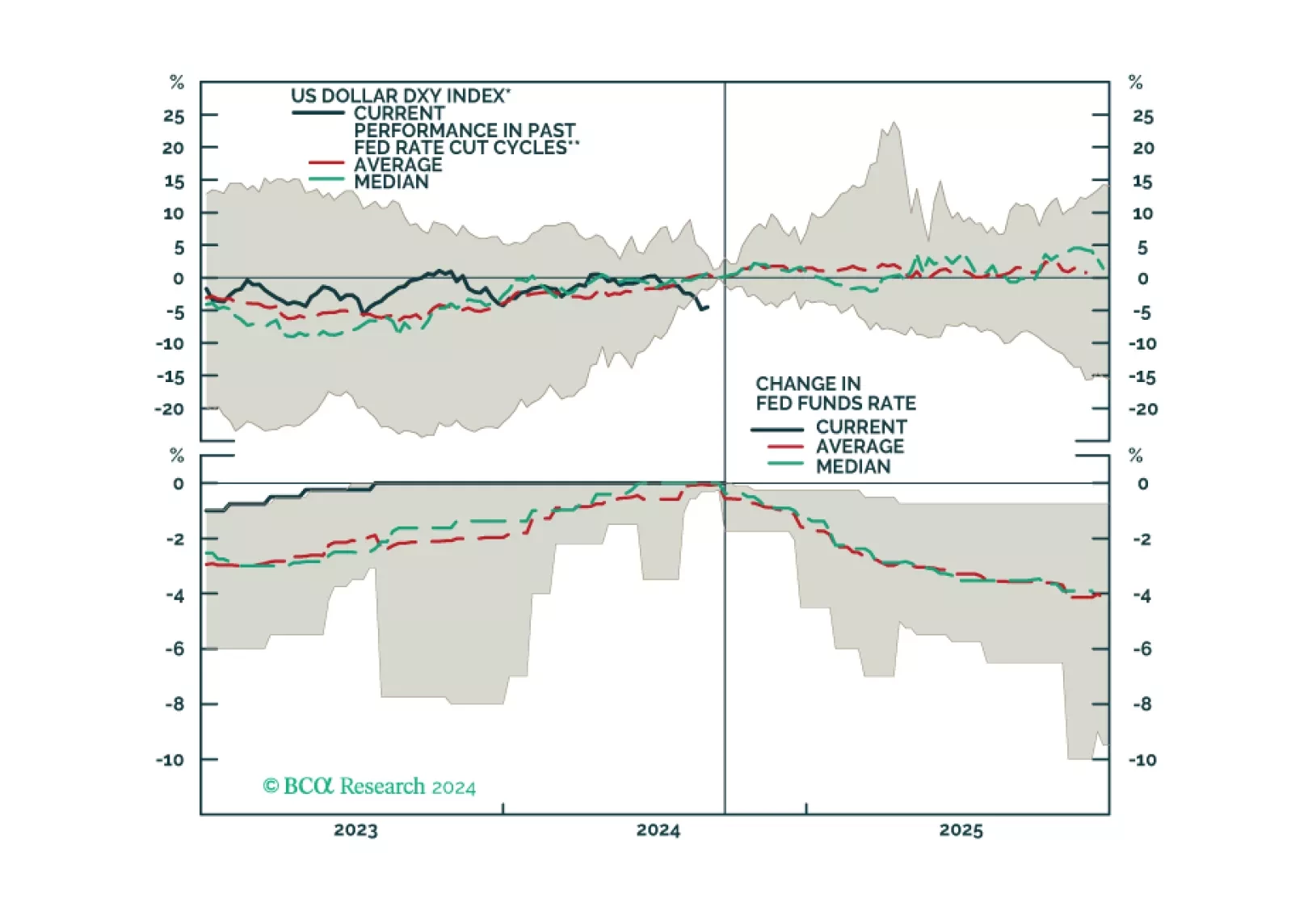

This Insight looks at potential dollar moves in the next six-to-twelve months.

China has notably diversified its export markets over the past two decades, reducing its dependence on the US and other DM economies and strengthening trade ties with EM nations. Since 2000, shipments to the US have halved (from 30% to 16% of total…

According to BCA Research’s Counterpoint Strategy service, the post-pandemic US economy has inverted from its usual ‘demand-constrained’ state to a highly unusual ‘supply-constrained’ state. This inversion is still a ways from normalizing, with labor demand…

Last week, economists polled by Bloomberg revised their consensus 2024 US GDP forecasts upwards, from 2.3% to 2.5%. Government spending and private investment were both revised 0.3 ppts higher to 3.0% and 3.9%, respectively, while consumption growth forecasts…