Policy

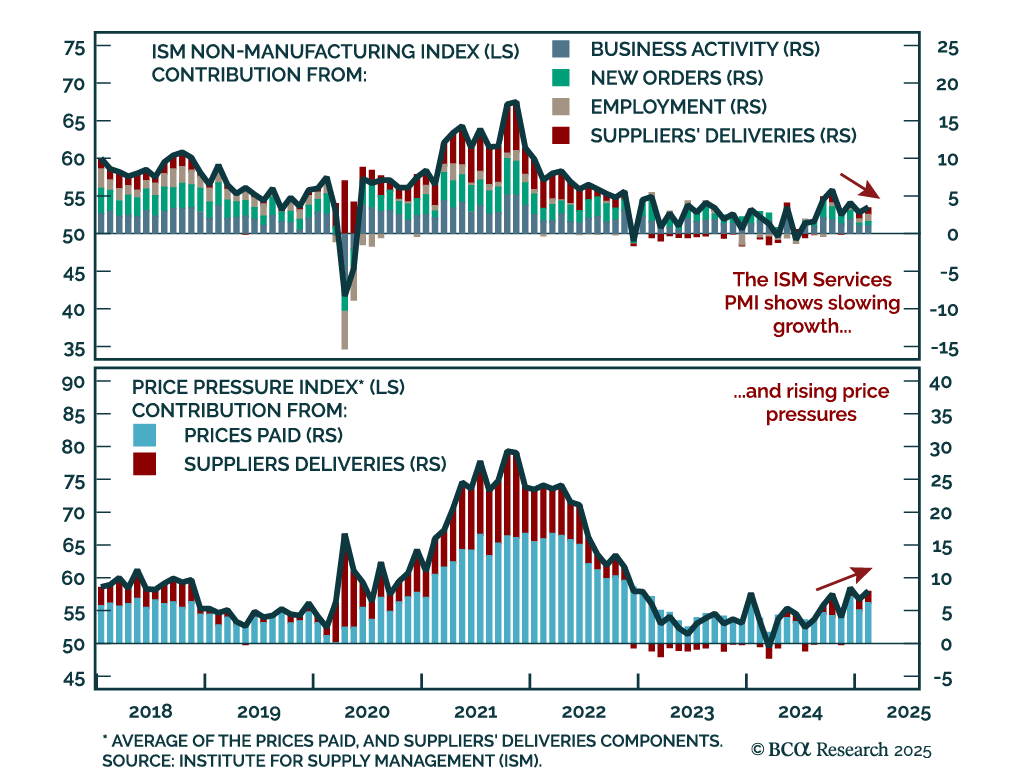

The February ISM Services beat estimates, rebounding to 53.5 from 52.8. All activity subcomponents increased, with new orders and employment ticking up. Price pressures however also increased, as prices paid went up and suppliers’ delivery times…

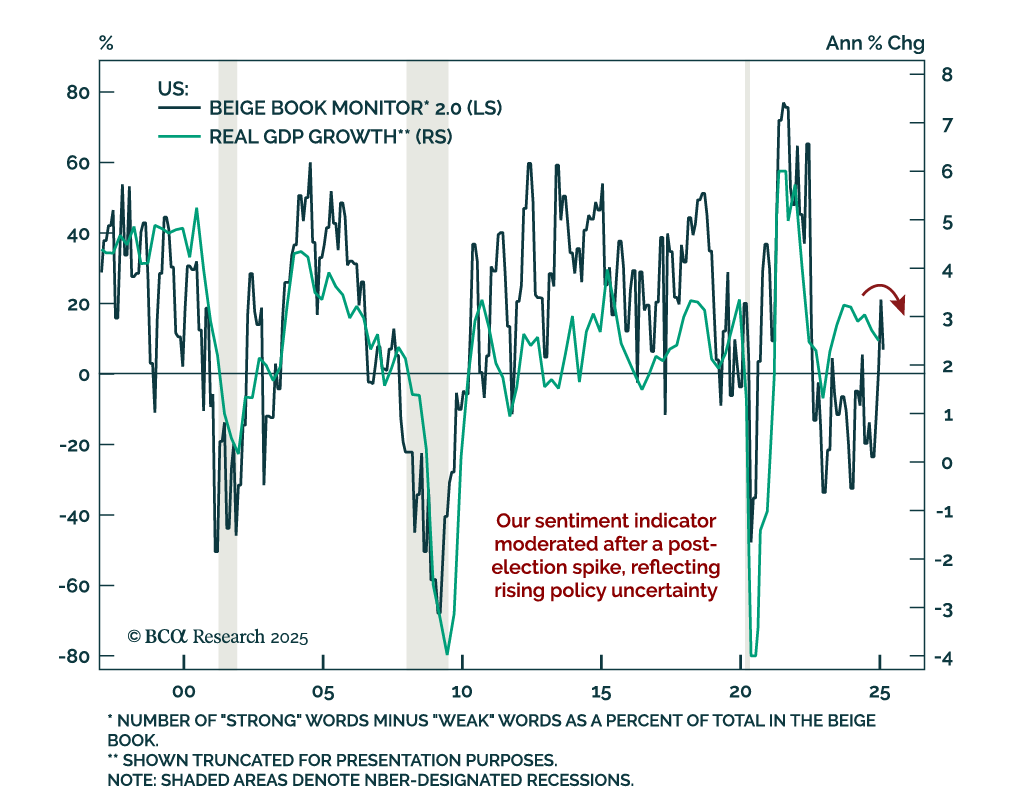

The Federal Reserve’s Beige Book shows a slowing economy, a moderating labor market, and rising price pressures. The latest Beige Book is in line with other sentiment indicators showing slower growth and decreased confidence following the post-election…

In light of President Trump’s address to Congress and the ebb-and-flow of tariff announcements, our Geopolitical strategists assessed the constraints on the administration’s disruptive agenda. Trump’s ability to implement his agenda is strongest in early…

Please join Doug Peta, Chief US Investment Strategist and co-author of The Bank Credit Analyst, for a Webcast on Wednesday, March 5 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET).

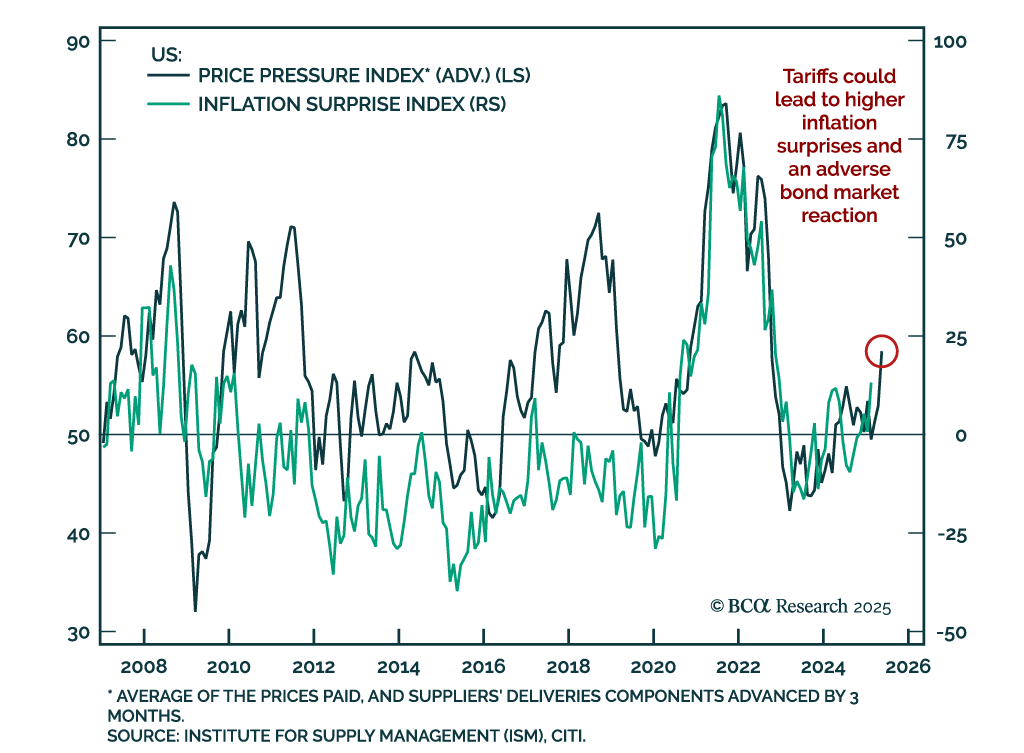

Leading US growth indicators have slowed, with economic surprises now in negative territory. However, Monday’s ISM Manufacturing showed that while activity is slowing due to tariffs uncertainty, supply-side price pressures are increasing. Our Price…

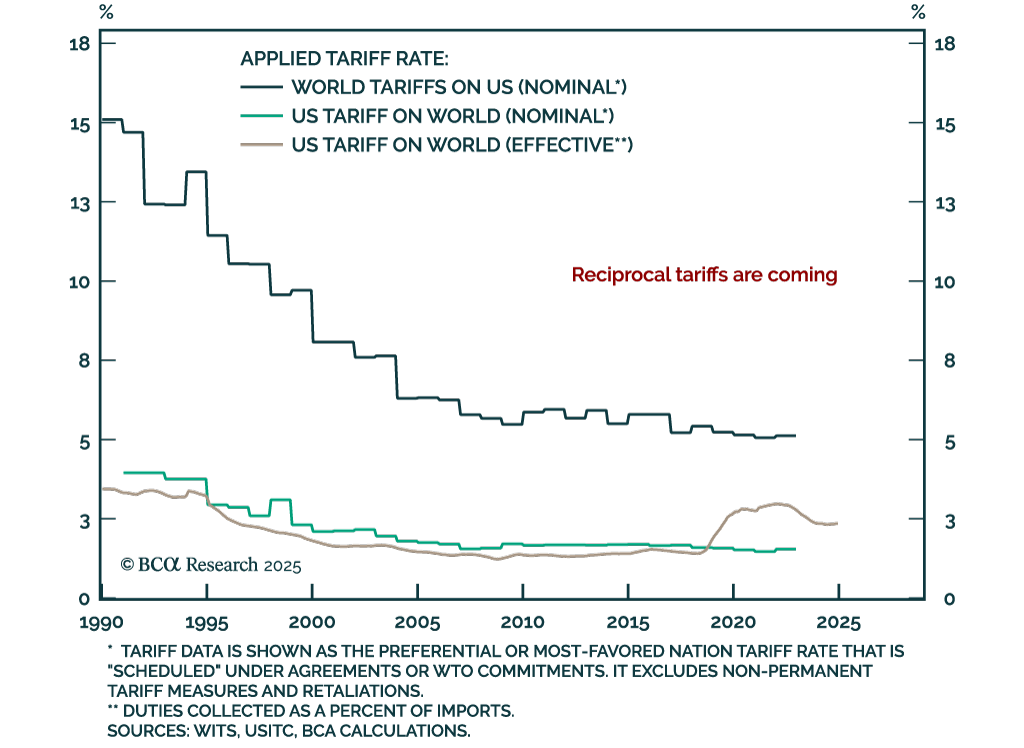

The Trump administration launched its biggest trade action on Tuesday, levying 25% tariffs on Canadian and Mexican goods, and an additional 10% to current tariffs on Chinese imports. Given its crucial role in US supply chains, Canadian energy only sees a 10%…

Trump will pull back from the trade war when stocks approach bear market territory. He will not withdraw from NATO. Favor European stocks on fiscal policy.

February flash inflation for the Eurozone was slightly hotter than expected but nonetheless declined, with both headline and core inflation falling 0.1% to 2.4% y/y and 2.6%, respectively. Services inflation also declined to 3.7% from 3.9%. While Europe…

Our Chart Of The Week comes from Juan Correa, from our Global Asset Allocation (GAA) strategy service. Juan highlights weakening US growth observed in the data lately. We have seen a few growth slowdown episodes since 2022. Why is this time…

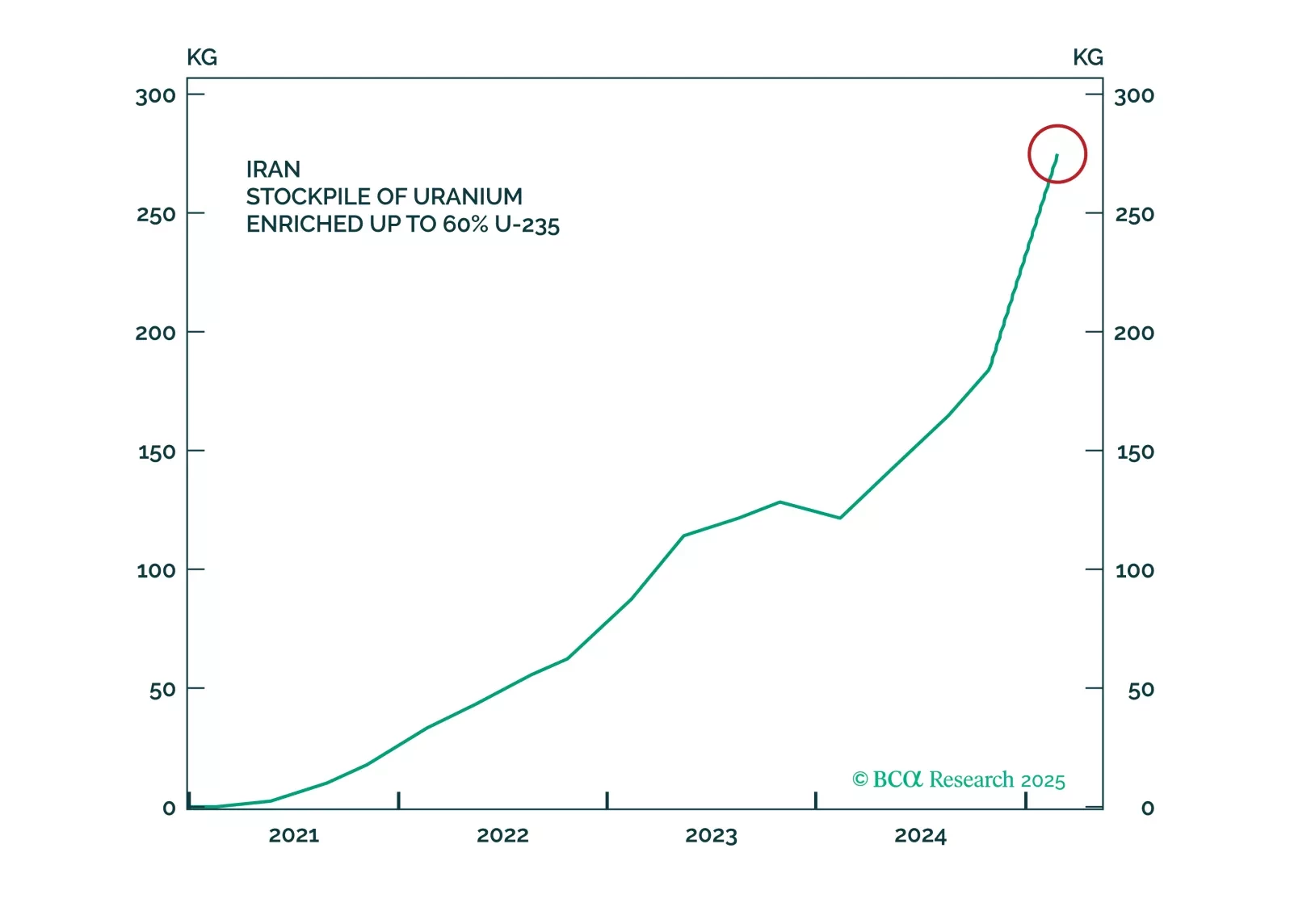

The tariffs on Canada and Mexico will come into effect as scheduled while the tariffs on China will be doubled. In the Middle East, Iranian response to any attack will threaten Middle Eastern oil supply. Meanwhile, Chinese fiscal support will surprise to the upside at the Two Sessions. But Trump's China policy will cause volatility. Now that the stock market is cracking, reinitiate defensive trades, such as long treasuries versus US stocks and long global defensives versus cyclicals.