Policy

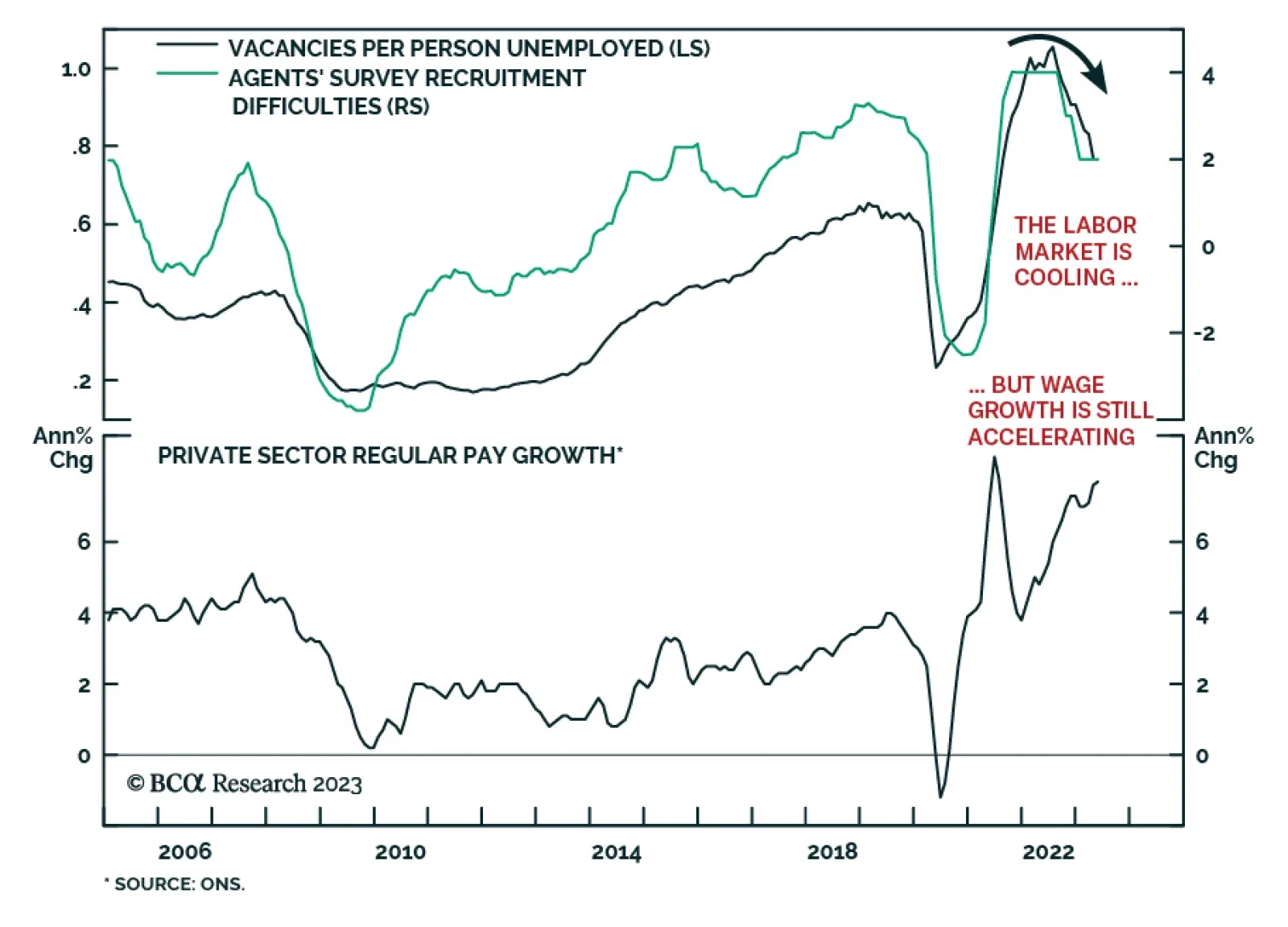

Time is running out on the Bank of England’s tightening cycle. UK economic growth is flirting with recession, unemployment is rising, house prices are contracting and inflation is decelerating. Markets are overestimating the eventual bottom in UK inflation, and thus are also underestimating how much the Bank of England will eventually cut rates in the next easing cycle, which could begin as soon as H1/2024. The backdrop is turning increasingly positive for Gilts on a medium-term basis, while the overbought pound is due for a breather.

Some thoughts on this week’s bear-steepening of the Treasury curve and this morning’s employment report.

In this insight, we assess the prospect of the Swiss franc over the next six months.

The Supreme Court is a generator of certainty rather than uncertainty for US markets. In the event of a constitutional crisis, a court intervention will likely reduce volatility.