Policy

In this report, we present the quarterly review of the Global Fixed Income Strategy Model Bond Portfolio. The portfolio remains positioned for slower global growth momentum over the next 6-12 months, favoring government bonds over corporate debt. The portfolio also favors government bonds in countries flirting with recession where policy rates are too high (core Europe & the UK).

The recent bear-steepening of the US Treasury curve has been driven by the combination of stronger-than-expected economic growth and stable Fed rate expectations. Historically, such periods do not last very long, and we see the current bear-steepening episode ending soon. We also highlight an opportunity in Agency MBS.

More equity volatility is coming in the short run. Trump’s nomination looks to be smooth, which marginally reduces the incumbent party advantage and increases policy uncertainty.

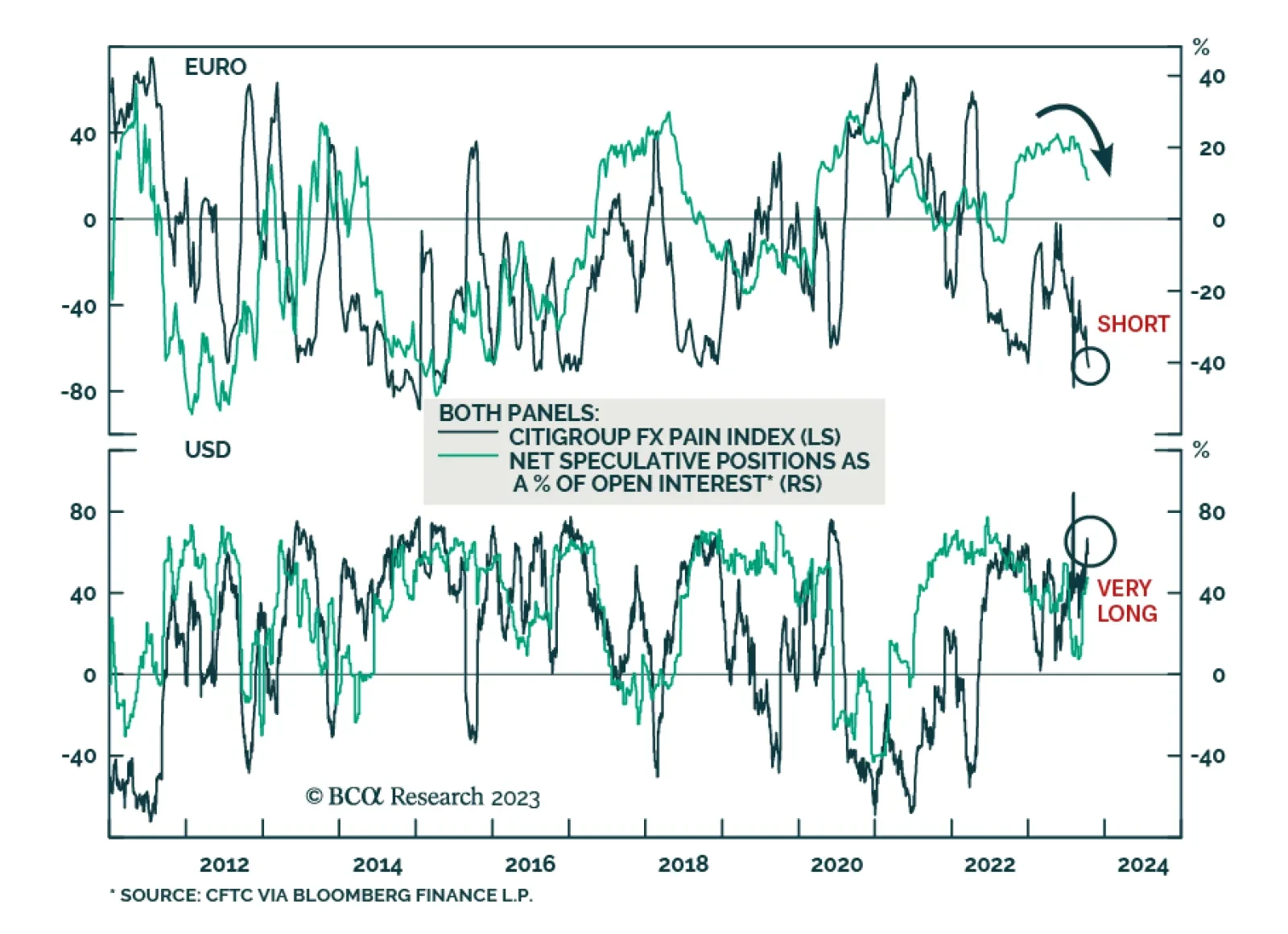

This week's Insight gauges the potential of a dollar breakout or breakdown and suggests a few trade ideas.