Oil & Gas Exploration & Production

Stay overweight US equities versus world, long US energy sector versus Middle East stocks, and long Canada and Mexico versus global-ex-US stocks.

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

Middle East conflict, extreme US policy uncertainty, Chinese economic slowdown, US-Russian proxy war, and Asian military conflicts do not create a stable investment backdrop for 2024. Our top five “black swan” risks may be highly improbable, but they stem from these underlying trends.

In this brief Insight we examine the expanding Middle East conflict and update the situation in the Taiwan Strait on the eve of elections. The Houthis are a distraction and China is not likely to invade Taiwan in the near term, but both situations support our overweight of US equities relative to global. Global growth is likely to slow while commodities are likely to see at least minor supply shocks.

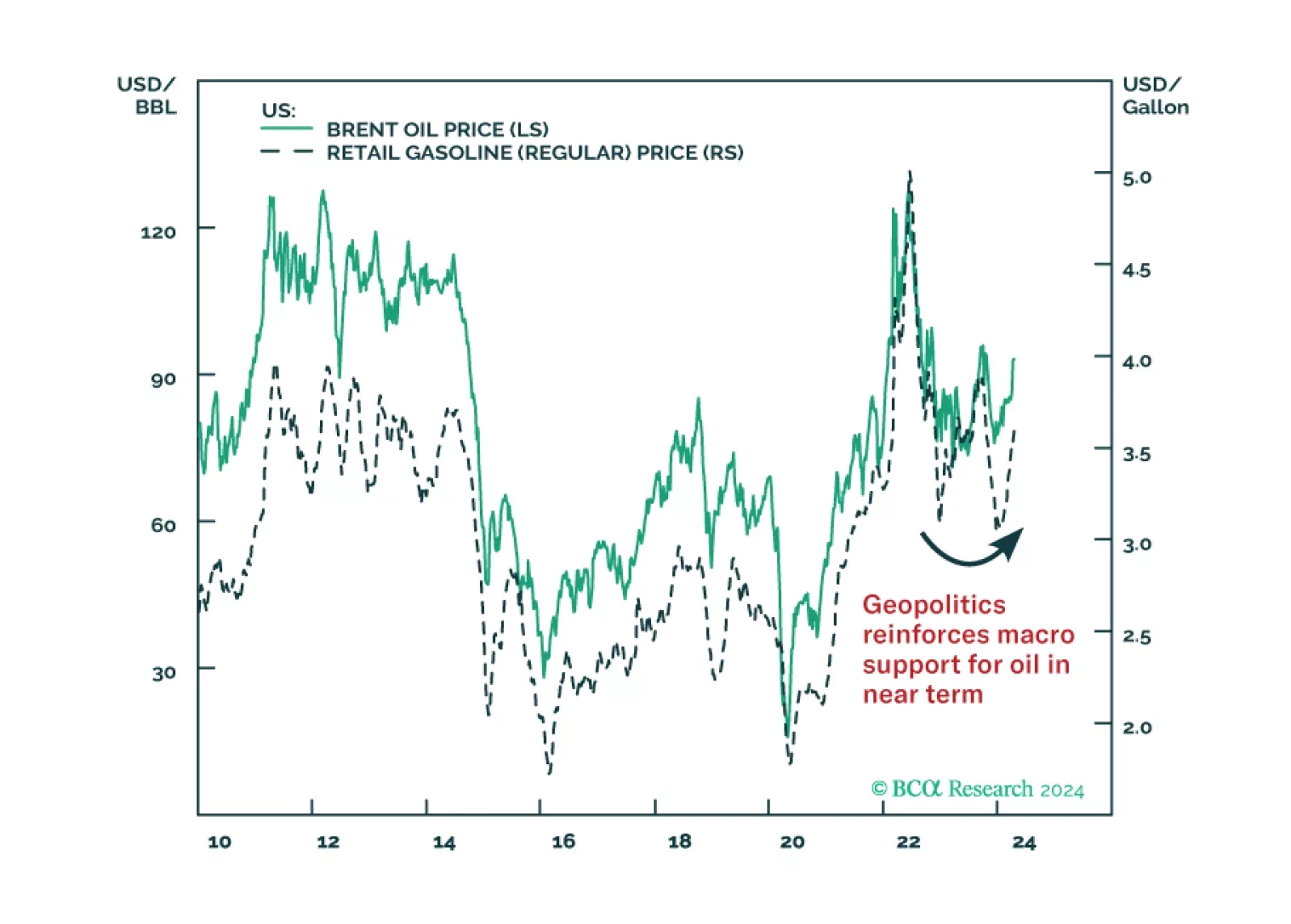

Oil prices will rise tactically due to supply risks. Recent developments indicate escalation of the conflict with Iran in the Middle East and confirm our expectation of energy supply disruptions and oil price spikes in the short run.

China’s oil demand growth will moderate to a still robust 4%-6% in the next six-to-nine months. We recommend that investors in China’s onshore and offshore stock indexes overweight energy producers.

The attempted coup in Russia produced subdued short-covering rallies in oil, gas, and grains markets, as markets over time have observed that coups, rarely result in loss of production and exports. Markets await Putin’s next move. Unless and until a viable threat to the Putin government emerges, markets will continue pricing in fundamentals prevailing prior to Saturday’s attempted coup. We are keeping our base case brent and henry hub natgas price expectations unchanged.

The OPEC 2.0 supply cuts announced over the weekend will be fundamentally bullish international crude oil prices. According to our model, brent will cross the USD 100/bbl mark by August this year. We believe the cohort is pre-emptively cutting oil supply in response to threats to their economic interest, including risks arising from the higher possibility of recession and rising market volatility following the banking crisis.