Oil & Gas Exploration & Production

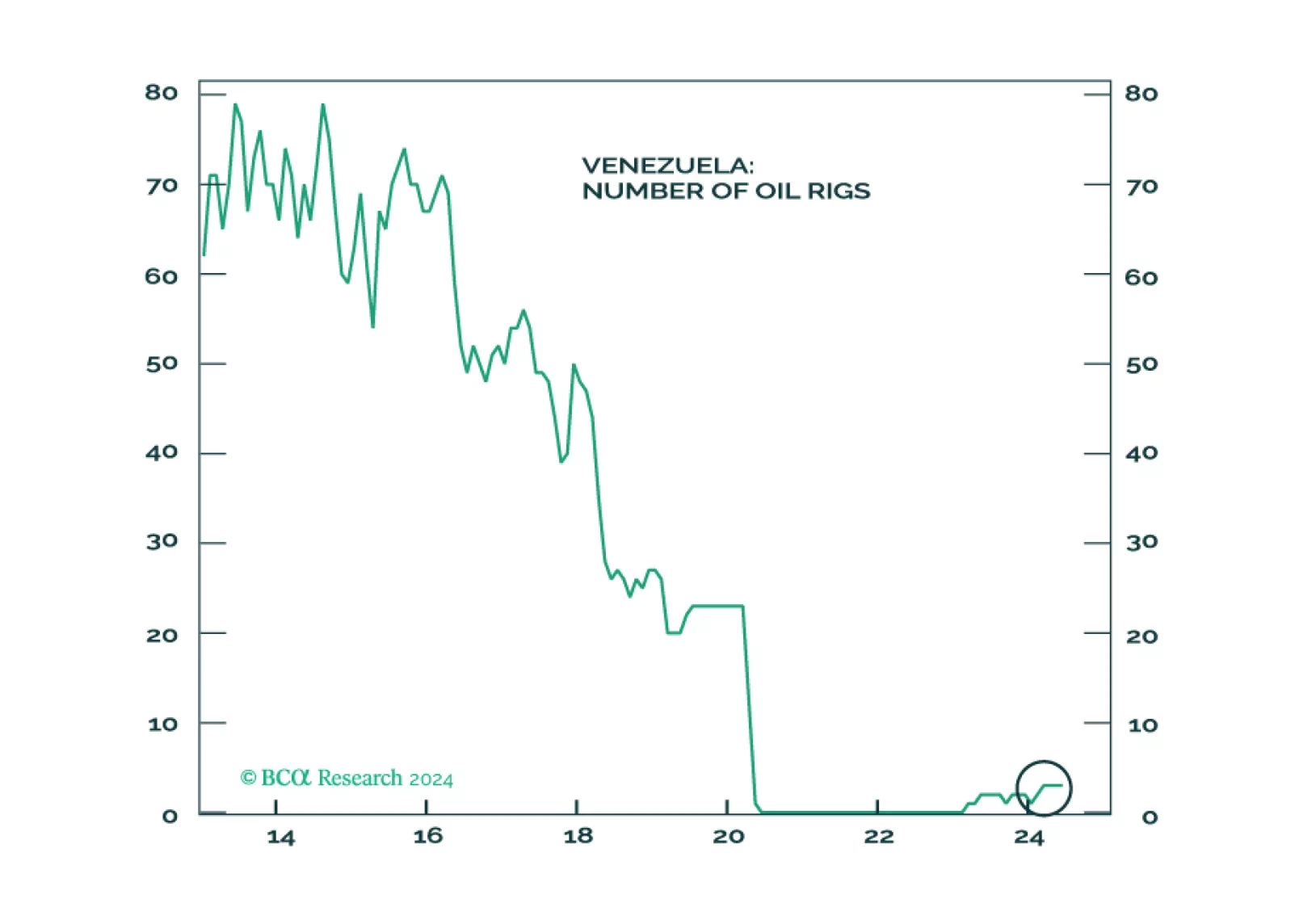

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

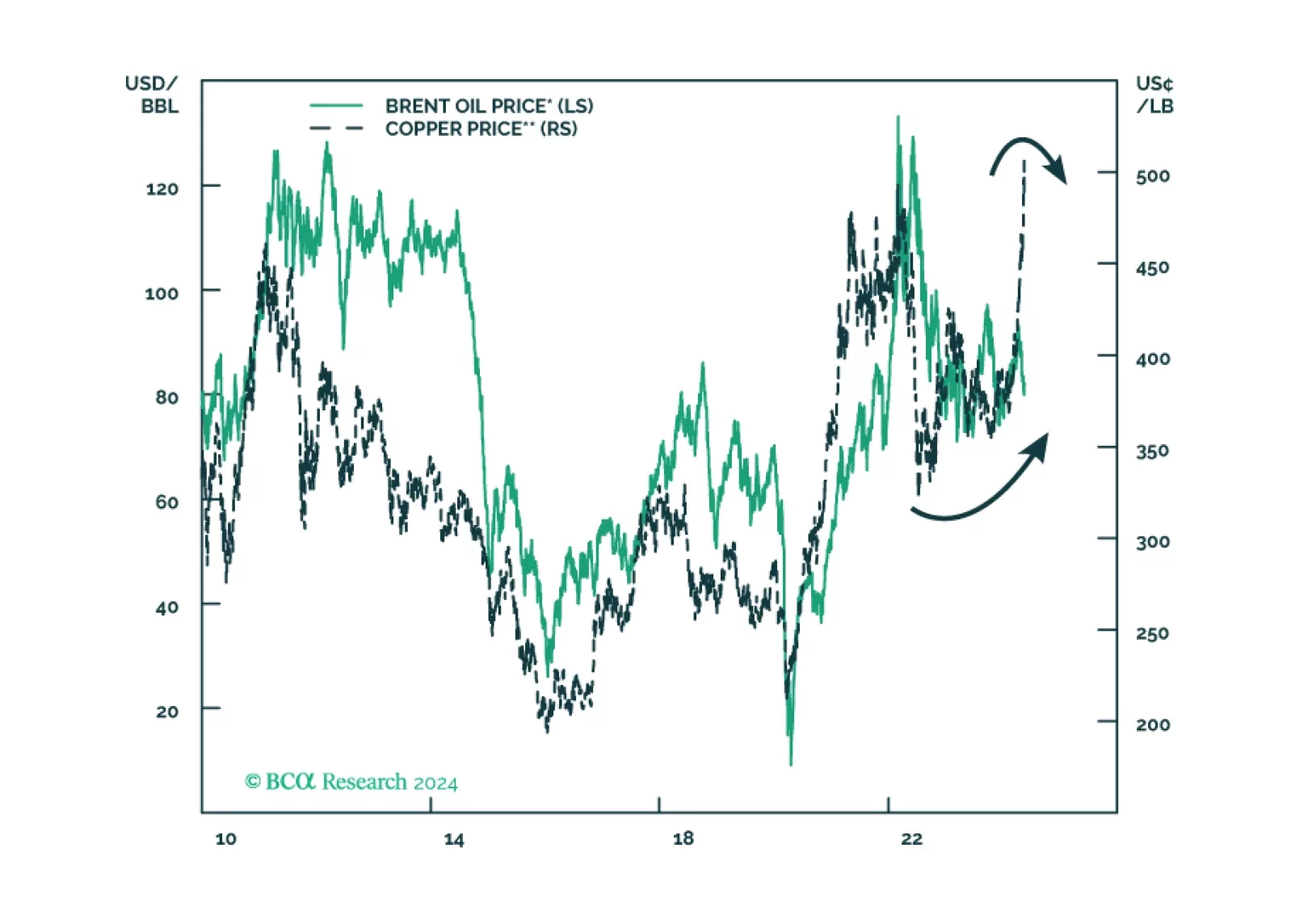

We close our overweights to Energy and Aerospace & Defense. The macroeconomic backdrop is deteriorating for Energy. As for A&D, the good news is already priced in.

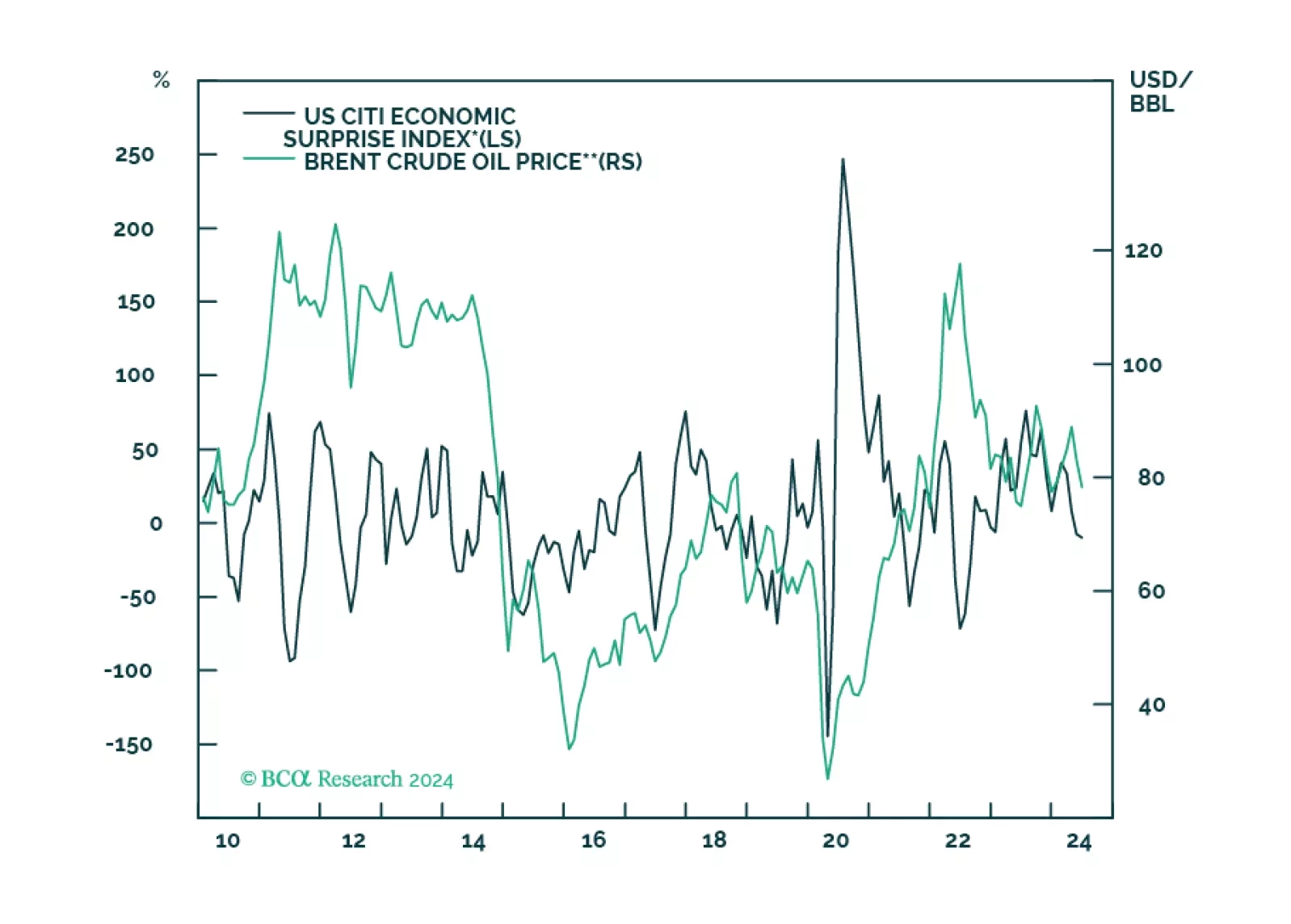

The death of the Iranian president reinforces our base case view of Middle Eastern instability and at least minor oil supply shocks. Rapid geopolitical developments in recent weeks are pointing to a new bout of global instability. The US is hobbled by its election. Conflicts with Russia, China, and Iran are all now escalating at the same time, at least marginally. Investors should reduce risk and shift to more defensive assets, markets, and sectors.

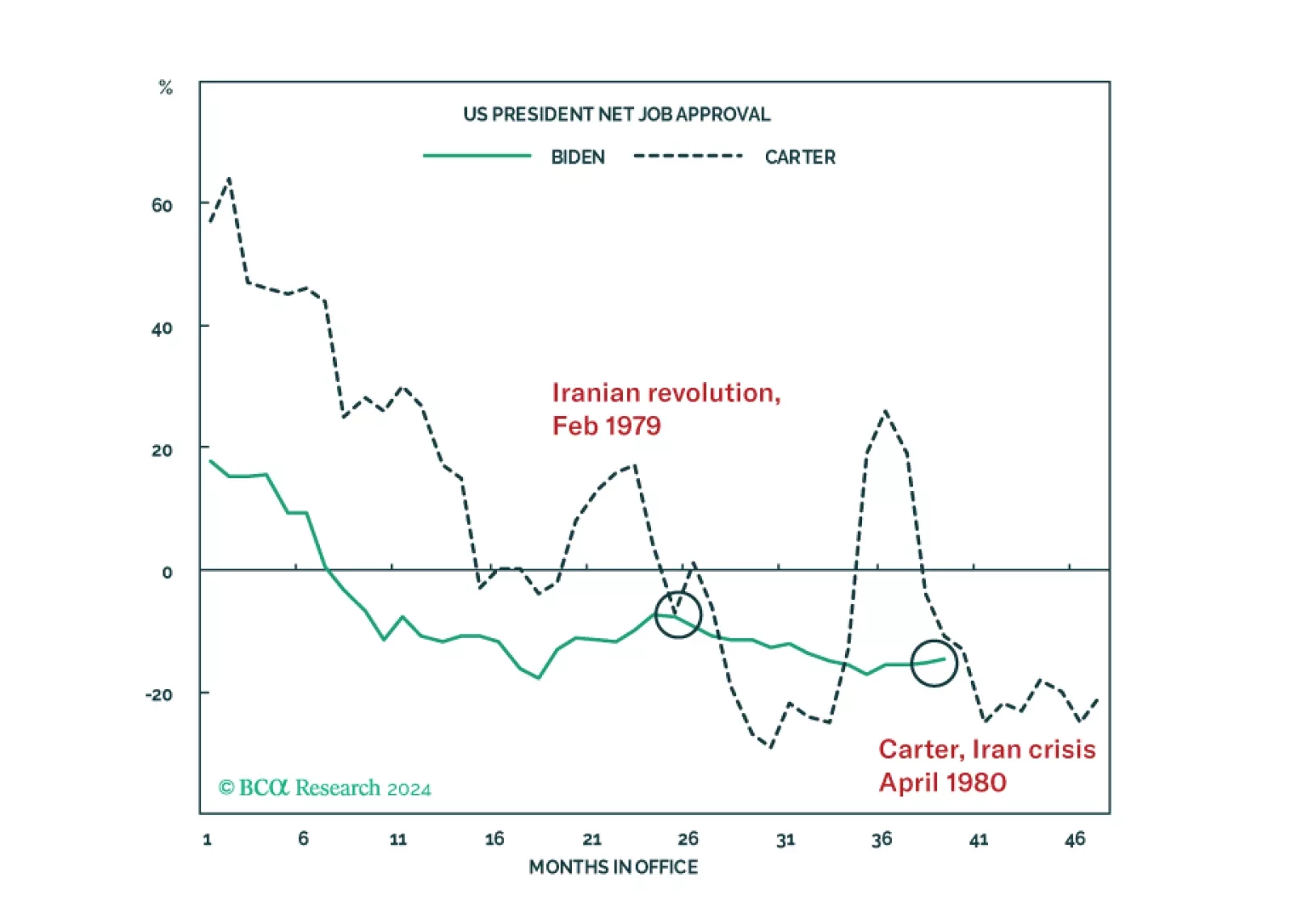

Our quant models suggest Democrats are still slightly favored for the White House. Our Senate model favors Republican control, though Montana and Ohio are the weak links that could deliver Democrats a de facto Senate majority in the event they keep the White House. But there are still six months before the vote. An oil shock from the Middle East or other negative economic news would force a major change to these models.