Oil

Highlights Macro outlook: Global growth will continue to decelerate into early next year on the back of brewing EM stresses and an underwhelming policy response from China. Equities: Stay neutral for now, while underweighting EM relative to DM stocks. Within DM, overweight the U.S. in dollar terms. Bonds: Global bond yields may dip in the near term, but the longer-term path is firmly higher. Currencies: The dollar is working off overbought conditions, but will rebound into year-end. EM currencies will suffer the most. Commodities: Favor oil over industrial metals. Precious metals will also remain under pressure until the dollar peaks next year, before beginning a major bull run as inflation accelerates. Feature I. Economic Outlook The Fed Can Hike A Lot More If 2017 was the year of a synchronized global growth recovery, 2018 is turning out to be a year where desynchronization is once again the name of the game. The U.S. economy continues to fire on all cylinders, while much of the rest of the world is struggling to stay afloat. The divergence in economic outcomes has been mirrored in central bank policy. The Fed is now hiking rates once per quarter whereas most other major central banks are still sitting on their hands. How high can U.S. rates go? The answer is a lot higher than investors anticipate. Market participants currently expect the Fed funds rate to rise to 2.37% by the end of this year and 2.84% by the end of 2019. No rate hikes are priced in for 2020 and beyond. The Fed dots are somewhat higher than market expectations (Chart 1). The median dot rises to about 3.4% in 2020-21, but then falls back to 3% over the Fed's longer-run horizon. Both investors and the Fed have apparently bought into Larry Summers' secular stagnation thesis. They seem convinced that rates will not be able to rise above 3% without triggering a recession. While we have a lot of sympathy for Summers' thesis, it must be acknowledged that it is a theory about the long-term determinants of the neutral rate of interest. Over a shorter-term cyclical horizon, many factors can influence the neutral rate. Critically, as discussed last week, most of these factors are pushing it higher: Fiscal policy is extremely stimulative. The IMF estimates that the U.S. cyclically-adjusted budget deficit will reach 6.8% of GDP in 2019. In contrast, the euro area is projected to run a deficit of only 0.8% of GDP (Chart 2). The relatively more expansionary nature of U.S. fiscal policy is one key reason why the Fed can raise rates while the ECB cannot. Chart 1Markets Expect No Fed ##br##Hikes Beyond Next Year

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Chart 2Fiscal Policy Is More Expansionary ##br##In The U.S. Than In The Euro Area

Fiscal Policy Is More Expansionary In The U.S. Than In The Euro Area

Fiscal Policy Is More Expansionary In The U.S. Than In The Euro Area

Credit growth has picked up. After a prolonged deleveraging cycle, private-sector nonfinancial debt is increasing faster than GDP (Chart 3). The recent easing in The Conference Board's Leading Credit Index suggests that this trend will continue (Chart 4). Chart 3U.S. Private-Sector Nonfinancial Debt Is Rising At Close To Its Historic Trend

U.S. Private-Sector Nonfinancial Debt Is Rising At Close To Its Historic Trend

U.S. Private-Sector Nonfinancial Debt Is Rising At Close To Its Historic Trend

Chart 4U.S. Credit Growth Will Remain Strong

U.S. Credit Growth Will Remain Strong

U.S. Credit Growth Will Remain Strong

Wage growth is accelerating. Average hourly earnings surprised on the upside in August, with the year-over-year change rising to a cycle high of 2.9%. This followed a stronger reading in the Employment Cost Index in the second quarter. A simple correlation with the quits rate suggests that there is plenty of upside for wage growth (Chart 5). Faster wage growth will put more money into workers' pockets who will then spend it. The savings rate has scope to fall. The personal savings rate currently stands at 6.7%, more than two percentage points higher than what one would expect based on the current level of household net worth (Chart 6). If the savings rate were to fall by two points over the next two years, it would add 1.5% of GDP to aggregate demand. Chart 5The Quits Rate Is Signaling Upside For Wage Growth

The Quits Rate Is Signaling Upside For Wage Growth

The Quits Rate Is Signaling Upside For Wage Growth

Chart 6The Personal Savings Rate Has Room To Fall

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

A back-of-the-envelope calculation suggests that these cyclical factors will permit the Fed to raise rates to 5% by 2020, almost double what the market is discounting.1 An Absence Of Major Financial Imbalances Will Allow The Fed To Keep Raising Rates The past three recessions were all caused by financial market overheating rather than economic overheating. The 1991 recession was mainly the consequence of the Savings and Loan crisis, compounded by the spike in oil prices leading up to the Gulf War. The 2001 recession stemmed from the dotcom bust. The Great Recession was triggered by the housing bust. Today, it is difficult to point to any clear imbalances in the economy. True, housing activity has been weak for much of the year. However, unlike in 2006, the home vacancy rate stands near record-low levels (Chart 7). Tight supply will limit downside risks to both construction and home prices. On the demand side, low unemployment, high consumer confidence, and a rebound in the rate of new household formation should help the sector. Despite elevated home prices in some markets, the average monthly payment that homeowners must make to service their mortgage is quite low by historic standards (Chart 8). The quality of mortgage lending has also been very high over the past decade, which reduces the risk of a sudden credit crunch (Chart 9). Chart 7Low Housing Inventories Will Support Home Prices And Construction

Low Housing Inventories Will Support Home Prices And Construction

Low Housing Inventories Will Support Home Prices And Construction

Chart 8Housing Affordabiity Is Not Yet Stretched

Housing Affordabiity Is Not Yet Stretched

Housing Affordabiity Is Not Yet Stretched

Chart 9Mortgage Lenders Are Being Prudent

Mortgage Lenders Are Being Prudent

Mortgage Lenders Are Being Prudent

Unlike housing debt, there are more reasons to be concerned about corporate debt. The ratio of corporate debt-to-GDP has risen to record-high levels. So-called "covenant-lite" loans now make up the bulk of corporate leveraged loan issuance. While there is no doubt that the corporate debt market is the weakest link in the U.S. financial sector, some perspective is in order. U.S. corporate debt levels are quite low by global standards. Corporate debt in the euro area is more than 30 points higher as a percent of GDP than in the United States (Chart 10). Moreover, the interest coverage ratio - EBIT divided by interest expense - for U.S. corporates is still above its historic average (Chart 11). While this ratio will fall as interest rates rise, this will not happen very quickly. Most U.S. corporate debt is at fixed rates and average maturities have been rising. This reduces both rollover risk and the sensitivity of debt-servicing costs to higher short-term rates. An increasing share of U.S. corporate debt is held by non-leveraged investors. Bank loans account for only 18% of nonfinancial corporate sector debt, down from 40% in 1980 (Chart 12). This is important, because what makes a spike in corporate defaults so damaging is not the direct impact this has on the economy, but the second-round effects rising defaults have on financial sector stability. Chart 10U.S. Corporate Debt Not That High By Global Standards

U.S. Corporate Debt Not That High By Global Standards

U.S. Corporate Debt Not That High By Global Standards

Chart 11Interest Coverage Ratio Is Above Its Historic Average

Interest Coverage Ratio Is Above Its Historic Average

Interest Coverage Ratio Is Above Its Historic Average

Chart 12Banks Have Been Reducing Their Exposure To The Corporate Sector

Banks Have Been Reducing Their Exposure To The Corporate Sector

Banks Have Been Reducing Their Exposure To The Corporate Sector

In any case, we already had a dress rehearsal for what a corporate debt scare might look like. Credit spreads spiked in 2015. Default rates rose, but the knock-on effects to the financial system were minimal. This suggests that corporate America could handle a fair bit of monetary tightening without buckling under the pressure. The Fed And The Dollar If the Fed is able to raise rates substantially more than the market is discounting while most central banks cannot, the short-term interest rate spread between the U.S. and its trading partners is likely to widen. History suggests that this will produce a stronger dollar (Chart 13). Chart 13Historically, The Dollar Has Moved In Line With Interest Rate Differentials

Historically, The Dollar Has Moved In Line With Interest Rate Differentials

Historically, The Dollar Has Moved In Line With Interest Rate Differentials

Some have speculated that the Trump administration will intervene in the foreign-exchange market in order to drive down the value of the greenback. We doubt this will happen, but even if such interventions were to occur, they would not be successful. Presumably, currency interventions would take the form of purchases of foreign exchange, financed through the issuance of Treasurys. The purchase of foreign currency would release U.S. dollars into the financial system, but the sale of Treasury securities would suck those dollars back out of the system. The net result would be no change in the volume of U.S. dollars in circulation - what economists call a "sterilized" intervention. Both economic theory and years of history show that sterilized interventions do not have lasting effects on currency values. The Fed could, of course, provide funding for the Treasury's purchases of foreign exchange, leading to an increase in the monetary base. This would be tantamount to an unsterilized intervention. However, such a deliberate attempt to weaken the dollar by expanding the money supply would fly in the face of the Fed's efforts to cool growth by tightening financial conditions. We highly doubt the Fed's current leadership would go along with this. Emerging Markets In The Crosshairs The combination of rising U.S. rates and a stronger dollar is bad news for emerging markets. Eighty percent of EM foreign-currency debt is denominated in dollars. Outside of China, EM dollar debt is now back to late-1990s levels, both as a share of GDP and exports (Chart 14). The wave of EM local-currency debt issued in recent years only complicates matters. If EM central banks raise rates to defend their currencies, this could imperil economic growth and make it difficult for local-currency borrowers to pay back their loans. Rather than hiking rates, some EM central banks may simply choose to inflate away debt. Consider the case of Brazil. The fiscal deficit stands at nearly 8% of GDP and government debt has soared from 60% of GDP in 2013 to 84% of GDP at present (Chart 15). Ninety percent of Brazilian sovereign debt is denominated in reais. The Brazilian government won't default on its debt per se. However, if push comes to shove, Brazil's central bank can always step in to buy government bonds, effectively monetizing the fiscal deficit. This could cause the real to weaken much more than it already has. Chart 14EM Dollar Debt Is High

EM Dollar Debt Is High

EM Dollar Debt Is High

Chart 15Brazil's Perilous Fiscal Position

Brazil's Perilous Fiscal Position

Brazil's Perilous Fiscal Position

Chinese Stimulus To The Rescue? When emerging markets last succumbed to pressure in 2015, China saved the day by stepping in with massive stimulus. Fiscal spending and credit growth accelerated to over 15% year-over-year. The government's actions boosted demand for all sorts of industrial commodities. The stimulus measures in 2015 followed an even greater wave of stimulus in 2009. While these stimulus measures invigorated China's economy and helped put a floor under global growth, they came at a price: China's debt-to-GDP ratio has swollen from 140% in 2008 to over 250% at present, which has endangered financial stability (Chart 16). Excess capacity has also increased. This can be seen in the dramatic rise in the capital-to-output ratio. It can also be seen in the fact that the rate of return on assets within the Chinese state-owned enterprise sector, which has been the main source of rising corporate leverage, has fallen below borrowing costs (Chart 17). Chart 16China: Debt And Capital Accumulation Went Hand In Hand

China: Debt And Capital Accumulation Went Hand In Hand

China: Debt And Capital Accumulation Went Hand In Hand

Chart 17China: Rate Of Return On Assets Below Borrowing Costs For SOEs

China: Rate Of Return On Assets Below Borrowing Costs For SOEs

China: Rate Of Return On Assets Below Borrowing Costs For SOEs

Chinese banks are being told that they must lend more money to support the economy, while ensuring that their loans do not turn sour. Unfortunately, that is becoming an impossible feat. The Chinese economy produces too much and spends too little. The result is excess savings, epitomized most clearly in a national savings rate of 46% (Chart 18). As a matter of arithmetic, national savings must be transformed either into domestic investment or exported abroad via a current account surplus. Now that the former strategy has run into diminishing returns, the Chinese authorities will need to concentrate on the latter. This will require a larger current account surplus which, in turn, will necessitate a relatively cheap currency. Above-average productivity growth has pushed up the fair value of China's real exchange rate over time. However, the currency still looks expensive relative to its long-term trend line (Chart 19). Pushing down the value of the yuan against the dollar will not be that difficult. Chart 20 shows that USD/CNY has moved broadly in line with the one-year swap spread between the U.S. and China. The spread was about 3% earlier this year. Today, it stands at only 0.6%. As the Fed continues to raise rates, the spread will narrow further, taking the yuan down with it. Chart 18China Saves A Lot

China Saves A Lot

China Saves A Lot

Chart 19The RMB Is Still Quite Strong

The RMB Is Still Quite Strong

The RMB Is Still Quite Strong

Chart 20USD/CNY Has Tracked China-U.S. Interest Rate Differentials

USD/CNY Has Tracked China-U.S. Interest Rate Differentials

USD/CNY Has Tracked China-U.S. Interest Rate Differentials

Unlike standard Chinese fiscal/credit easing, a stimulus strategy focused on weakening the yuan would hurt other emerging markets by undermining their competitiveness in relation to China. A weaker yuan would also make it more expensive for Chinese companies to import natural resources, thus putting downward pressure on commodity prices. The Euro Area: Back In The Slow Lane After putting in a strong performance in 2017, the economy in the euro area has struggled to maintain momentum this year. Growth is still above trend, but the overall tone of the data has been lackluster at best, with the risks to growth increasingly tilted to the downside. Weaker growth in China and other emerging markets certainly has not helped. However, much of the problem lies closer to home. Bank credit remains the lifeblood of the euro area economy. The 12-month credit impulse - defined as the change in credit growth from one 12-month period to the next - tends to track GDP growth (Chart 21).2 Euro area credit growth accelerated over the course of 2017, but has been broadly stable this year. As a result, the credit impulse has fallen, taking GDP growth down with it. It will be difficult for euro area GDP growth to increase unless credit growth starts rising again. So far, there is little sign that this is about to happen. According to the latest euro area bank lending survey, while banks continue to ease standards for business loans, they are doing so at a slower pace than in the past. A net 3% of banks eased lending standards in the second quarter, compared to 8% in the first quarter. Loan demand growth has been fairly stable. This suggests that loan growth will remain positive, but is unlikely to increase much from current levels. Worries about the health of European banks will further constrain credit growth. European banks in general, and Spanish banks in particular, have significant exposure to the most vulnerable emerging markets (Chart 22). Chart 21Euro Area Credit Growth Has Flatlined

Euro Area Credit Growth Has Flatlined

Euro Area Credit Growth Has Flatlined

Chart 22Spain Most Exposed To Vulnerable EMs

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Concerns about the ability of the Italian government to service its debt obligations will also restrain bank lending. Investors breathed a sigh of relief last month when the Italian government signaled a greater willingness to pare back next year's proposed budget deficit, in accordance with the dictates of the European Commission. Tensions remain, however, as evidenced by the fact that the ten-year spread between BTPs and German bunds is still 120 basis points higher than in April (Chart 23). The European political establishment is terrified of the rise in populism across the region and would love nothing more than to see Italy's populist parties implode. This means that any help from the ECB and the European Commission will only arrive once a full-fledged crisis is underway. Anyway, it is far from clear that a smaller budget deficit would actually translate into a lower government debt-to-GDP ratio. Like China, Italy also has a private sector that saves too much and spends too little. A shrinking population has reduced the need for firms to invest in new capacity. The prior government's pension cuts have also incentivized people to save more for their retirement. The result is a private sector savings-investment surplus that stood at 5% of GDP in 2017 compared to close to breakeven a decade ago (Chart 24). Chart 23Italian/Bund Spreads Signal Lingering Fiscal Strain

Italian/Bund Spreads Signal Lingering Fiscal Strain

Italian/Bund Spreads Signal Lingering Fiscal Strain

Chart 24Italy: Private Sector Saves Too Much And Spends Too Little

Italy: Private Sector Saves Too Much And Spends Too Little

Italy: Private Sector Saves Too Much And Spends Too Little

Unlike Germany, Italy cannot export its excess production because it does not have a hypercompetitive economy. Nor does it have the ability to devalue its currency to gain a quick competitiveness boost. This means that the Italian government has to absorb excess private-sector savings with its own dissavings - a fancy way of saying that it has to run a large budget deficit. This has effectively been Japan's strategy for over two decades. However, unlike Japan, Italy does not have a lender of last resort that can unconditionally buy government debt. This raises the risk that Italy's debt woes will resurface, either because the government abandons austerity measures, or because the lack of fiscal support causes nominal GDP to stagnate, making it all but impossible for the country to outgrow its debt burden. Receding Policy Puts The discussion above suggests that many of the "policy puts" that investors have relied on are in the process of having their strike price marked down to deeper out-of-the-money levels. Yes, the Fed will ease off on rate hikes if U.S. growth is at risk of stalling out completely. However, now that the labor market has reached full employment, the Fed will welcome modestly slower growth. Remember that there has never been a case in the post-war era where the three-month average of the unemployment rate has risen by more than a third of a percentage point without a recession taking place (Chart 25). The further the unemployment rate falls below NAIRU, the more difficult it will be for the Fed to achieve the proverbial soft landing. Chart 25Even A Small Uptick In The Unemployment Rate Is Bad News For The Business Cycle

Even A Small Uptick In The Unemployment Rate Is Bad News For The Business Cycle

Even A Small Uptick In The Unemployment Rate Is Bad News For The Business Cycle

Likewise, the "China stimulus put" - the presumption that most investors have that the Chinese authorities will launch a barrage of fiscal and credit easing at the first sign of slower growth - has become less reliable in light of the government's competing objectives namely reducing debt growth and excess capacity. The same goes for the "ECB put." Yes, the ECB will bail out Italy if the entire European project appears at risk. But spreads may need to blow out before the cavalry arrives. Meanwhile, just as the aforementioned policy puts are receding, new policy risks are rising to the fore, chief among them protectionism. We expect the trade war to heat up, with the Trump administration increasingly directing its ire at China. Trump's macroeconomic policies are completely at odds with his trade agenda. Fiscal stimulus will boost aggregate demand, which will suck in more imports. An overheated economy will prompt the Fed to raise rates more aggressively than it otherwise would, leading to a stronger dollar. All this will result in a wider trade deficit. What will Trump tell voters two years from now when he is campaigning in Michigan and Ohio about why the trade deficit has widened rather than narrowed under his watch? Will he blame himself or Beijing? No trophy for getting that answer right. II. Financial Markets Global Equities The combination of slower global growth, rising economic vulnerabilities outside the U.S., and a more challenging policy environment caused us to downgrade our view on global equities from overweight to neutral in June,3 while reiterating our preference for developed market equities relative to EM stocks. For now, we are comfortable with our bearish view towards emerging market stocks. While EM equities have cheapened, they are not yet at washed out levels (Chart 26). Bottom fishers still abound, as evidenced by the fact that the number of shares outstanding in the MSCI iShares Turkish ETF has almost tripled since early April (Chart 27). Chart 26EM Assets: Valuations Not Yet At Washed Out Levels

EM Assets: Valuations Not Yet At Washed Out Levels

EM Assets: Valuations Not Yet At Washed Out Levels

Chart 27EM Bottom Fishers Still Abound

EM Bottom Fishers Still Abound

EM Bottom Fishers Still Abound

At some point - probably in the first half of next year - investors will liquidate their remaining bullish EM bets. At that point, EM stocks will rebound. European and Japanese equities should also start to outperform the U.S., given their more cyclical nature. As far as the absolute direction of the S&P 500 is concerned, the next few months could be challenging. U.S. stocks have been able to decouple from those in the rest of the world, but this state of affairs may not last. Recall that the S&P 500 fell by 22% peak-to-trough between July 20 and October 8, 1998, in what otherwise was a massive bull market. We do not know if there is another Long-Term Capital Management lurking around the corner, but if there is, a temporary selloff in U.S. stocks may be hard to avoid. Such a selloff would present a buying opportunity over a horizon of 12-to-18 months. If we are correct that cyclical forces have lifted the neutral rate of interest, it will take a while for monetary policy to reach restrictive territory. This means that both fiscal and monetary policy will stay accommodative at least for the next 18 months. As such, the S&P 500 may not peak until 2020. Appendix A - Chart I presents a stylized diagram of where we think global equities are going. It incapsulates three phases: 1) a challenging period over the next six months, driven by EM weakness; 2) a blow-off rally in equities starting in the middle of next year; 3) and finally, a recession-induced bear market beginning in late-2020. Appendix B also presents our valuation charts, which highlight that long-term return prospects are better outside the United States. Fixed Income After advocating for a long duration strategy for much of the post-crisis recovery, BCA declared "The End Of The 35-Year Bond Bull Market" on July 5, 2016, the very same day that the 10-year U.S. Treasury yield hit a record closing low of 1.37%. Cyclically and structurally, we continue to expect U.S. bond yields to rise more than the market is discounting. As noted above, the Fed is underestimating how high rates will need to go before they reach restrictive territory. This means that the Fed will end up behind the curve in normalizing monetary policy, causing the economy to overheat and inflation to rise above the Fed's comfort zone. Chart 28Bond Sentiment Is Extremely Bearish

Bond Sentiment Is Extremely Bearish

Bond Sentiment Is Extremely Bearish

Granted, the Fed is willing to tolerate a modest inflation overshoot. However, a core PCE reading above 2.3%, which is at the top end of the range of the Fed's own forecast, would prompt the Fed to expedite the pace of rate hikes. A bear flattening of the yield curve - a situation where long-term yields rise, but short-term rates go up even more - would be highly likely in that environment. Over a shorter-term horizon spanning the next six months, the outlook for yields is more benign. The combination of a stronger dollar, slower global growth, and flight-to-quality flows into the Treasury market from vulnerable emerging markets can cap yields. Add to this the fact that sentiment towards bonds is currently extremely bearish (Chart 28), and a temporary countertrend decline in yields becomes quite probable. Developed market bond yields in general are likely to follow the direction of U.S. yields, both on the upside and the downside, but in a more muted manner. Outside the periphery, euro area yields have less scope to fall in the near term given that they are already so low. European yields also have less room to rise once global growth bottoms next year because the neutral rate of interest is much lower in the euro area than in the United States. Ironically, a more dovish ECB would help reduce Italian bond yields, as higher inflation is critical for increasing Italian nominal GDP. Since labor market slack is still elevated in Italy, continued monetary stimulus would also lift wages in core Europe more than in Italy, helping to boost Italy's competitiveness relative to the rest of the euro area. Japanese yields have plenty of scope to rise over the long haul. An aging population is pushing more people into retirement, which will cause the national savings rate to fall further. A decline in the savings pool will increase the neutral rate of interest in Japan. Instead of raising the policy rate, the Japanese authorities will let the economy overheat, generating inflation in the process. This will cause the yield curve to steepen, particularly at the very long end (e.g., beyond 10 years) which is the part of the yield curve that is the least susceptible to the BoJ's yield curve control regime. We are positioned for this outcome through our short 20-year JGB/long 5-year JGB trade recommendation. Appendix A - Chart II shows our expectations for the major government bond markets over the coming years. Turning to credit markets, high-yield credit typically underperforms in the latter innings of business-cycle expansions, a period when the Fed is raising rates. Thus, while we do not think that U.S. corporate debt levels will be a major source of systemic financial risk for the broader economy, this is hardly a reason to be overweight spread-product. A more cautious stance towards credit outside the U.S. is also warranted. Currencies And Commodities The dollar is working off overbought conditions, but will rebound into year-end, as EM tensions intensify and hopes of a massive credit/fiscal-fueled Chinese stimulus package fizzle. EM currencies will weaken the most against the dollar over the next three-to-six months, but the euro and, to a lesser extent, the yen, will also come under pressure. Granted, the dollar is no longer a cheap currency, but if long-term interest rate differentials stay anywhere close to current levels, the greenback will remain well supported. Consider the dollar's value against the euro. Thirty-year U.S. Treasurys currently yield 3.20% while 30-year German bunds yield 1.12%, a difference of 208 basis points. Even if one allows for the fact that investors expect euro area inflation to be lower than in the U.S. over the next 30 years, EUR/USD would need to trade at a measly 82 cents today in order to compensate German bund holders for the inferior yield they will receive.4 We do not expect EUR/USD to get down to that level, but a descent into the $1.10-to-$1.12 range over the next six months is probable. Sterling will remain hostage to Brexit negotiations. It is impossible to know how talks will evolve, but our bias is to take a somewhat pound-positive view. The main reason is that support for Brexit has faded (Chart 29). Opinion polls suggest that if a referendum were held again, the "bremain" side would almost certainly prevail. Lacking public support for leaving the EU, it is unlikely that British negotiators could simply walk away from the table. This reduces the odds of a "hard Brexit" outcome. Indeed, a second referendum that leads to a "no-Brexit" verdict remains a distinct possibility. The combination of slower global growth and a resurgent dollar is likely to hurt commodity prices. Industrial metals are more vulnerable than oil. China consumes around half of all the copper, nickel, aluminum, zinc, and iron ore produced around the world (Chart 30). In contrast, China represents less than 15% of global oil demand. Chart 29When Bremorse Sets In

When Bremorse Sets In

When Bremorse Sets In

Chart 30China Is A More Dominant Consumer Of Metals Than Oil

China Is A More Dominant Consumer Of Metals Than Oil

China Is A More Dominant Consumer Of Metals Than Oil

The supply backdrop for oil is also more favorable than for metals. Not only are Saudi Arabia and Russia maintaining production discipline, but U.S. sanctions against Iran threaten to weigh on global crude supply. Further reduction in Venezuela's oil output, as well as potential disruptions to Libyan or Iraqi exports, could also boost oil prices. The superior outlook for oil over metals means we prefer the Canadian dollar relative to the Aussie dollar. While AUD/CAD has weakened in recent months, the Aussie dollar is still somewhat expensive against the loonie based on our long-term valuation model (Chart 31). We also see an increasing chance that Canada will negotiate a revamped trade deal with the U.S., as Trump focuses his attention more on China. Should this happen, it will remove the NAFTA break-up risk discount embedded in the Canadian dollar. Finally, a few words on precious metals. Precious metals typically struggle during periods when the dollar is appreciating (Chart 32). Consequently, we would not be eager buyers of gold or other precious metals until the dollar peaks, most likely around the middle of next year. As inflation starts to accelerate in late-2019 and in 2020, gold will finally move decisively higher. Chart 31Canadian Dollar Still Somewhat Cheap Versus The Aussie Dollar

Canadian Dollar Still Somewhat Cheap Versus The Aussie Dollar

Canadian Dollar Still Somewhat Cheap Versus The Aussie Dollar

Chart 32Gold Won't Shine Until The Dollar Peaks

Gold Won't Shine Until The Dollar Peaks

Gold Won't Shine Until The Dollar Peaks

Appendix A - Chart III and Chart IV present an illustration of where the major currencies and commodities are heading. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com 1 Depending on which specification of the Taylor rule one uses, a one percent of GDP increase in aggregate demand will increase the neutral rate of interest by half a point (John Taylor's original specification) or by a full point (Janet Yellen's preferred specification). Fiscal policy is currently about 3% of GDP too stimulative compared to a baseline where government debt-to-GDP is stable over time. Assuming a fiscal multiplier of 0.5, fiscal policy is thus boosting aggregate demand by 1.5% of GDP. Nonfinancial private credit has increased by an average of 1.5 percentage points of GDP per year since 2016. Assuming that every additional one dollar of credit increases aggregate demand by 50 cents, the revival in credit growth is raising aggregate demand by 0.75% of GDP, compared to a baseline where credit-to-GDP is flat. The labor share of income has increased by 1.25% of GDP from its lows in 2015. Assuming that every one dollar shift in income from capital to labor boosts overall spending on net by 20 cents, this would have raised aggregate demand by 0.25% of GDP. Lastly, if the personal savings rate falls by two points over the next two years, this would raise aggregate demand by 1.5% of GDP. Taken together, these factors are boosting the neutral rate by anywhere from 2% (Taylor's specification) to 4% (Yellen's specification). This is obviously a lot, and easily overwhelms other factors such as a stronger dollar that may be weighing on the neutral rate. 2 Recall that GDP is a flow variable (how much production takes place every period), whereas credit is a stock variable (how much debt there is outstanding). By definition, a flow is a change in a stock. Thus, credit growth affects GDP and the change in credit growth affects GDP growth. Euro area private-sector credit growth accelerated from -2.6% in May 2014 to 3.1% in March 2017, but has been broadly flat ever since. Hence, the credit impulse has dropped. 3 Please see Global Investment Strategy Special Report, "Three Policy Puts Go Kaput: Downgrade Global Equities To Neutral," dated June 20, 2018. 4 For this calculation, we assume that the fair value for EUR/USD is 1.32, which is close to the IMF's Purchasing Power Parity (PPP) estimate. The annual inflation differential of 0.47% is based on 30-year CPI swaps. This implies that the fair value for EUR/USD will rise to 1.52 after 30 years. If one assumes that the euro reaches that level by then, the common currency would need to trade at 1.52/(1.0208)^30=0.82 today. Appendix A Appendix A Chart IMarket Outlook: Equities

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Appendix A Chart IIMarket Outlook: Bonds

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Appendix A Chart IIIMarket Outlook: Currencies

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Appendix A Chart IVMarket Outlook: Commodities

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Appendix B Appendix B Chart 1Long-Term Return Prospects Are Slightly Better Outside The U.S.

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Appendix B Chart 1Long-Term Return Prospects Are Slightly Better Outside The U.S.

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Appendix B Chart 1Long-Term Return Prospects Are Slightly Better Outside The U.S.

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Appendix B Chart 1Long-Term Return Prospects Are Slightly Better Outside The U.S.

2018 Q4 Strategy Outlook: Desynchronization Is Back

2018 Q4 Strategy Outlook: Desynchronization Is Back

Strategy & Market Trends Tactical Trades Strategic Recommendations Closed Trades

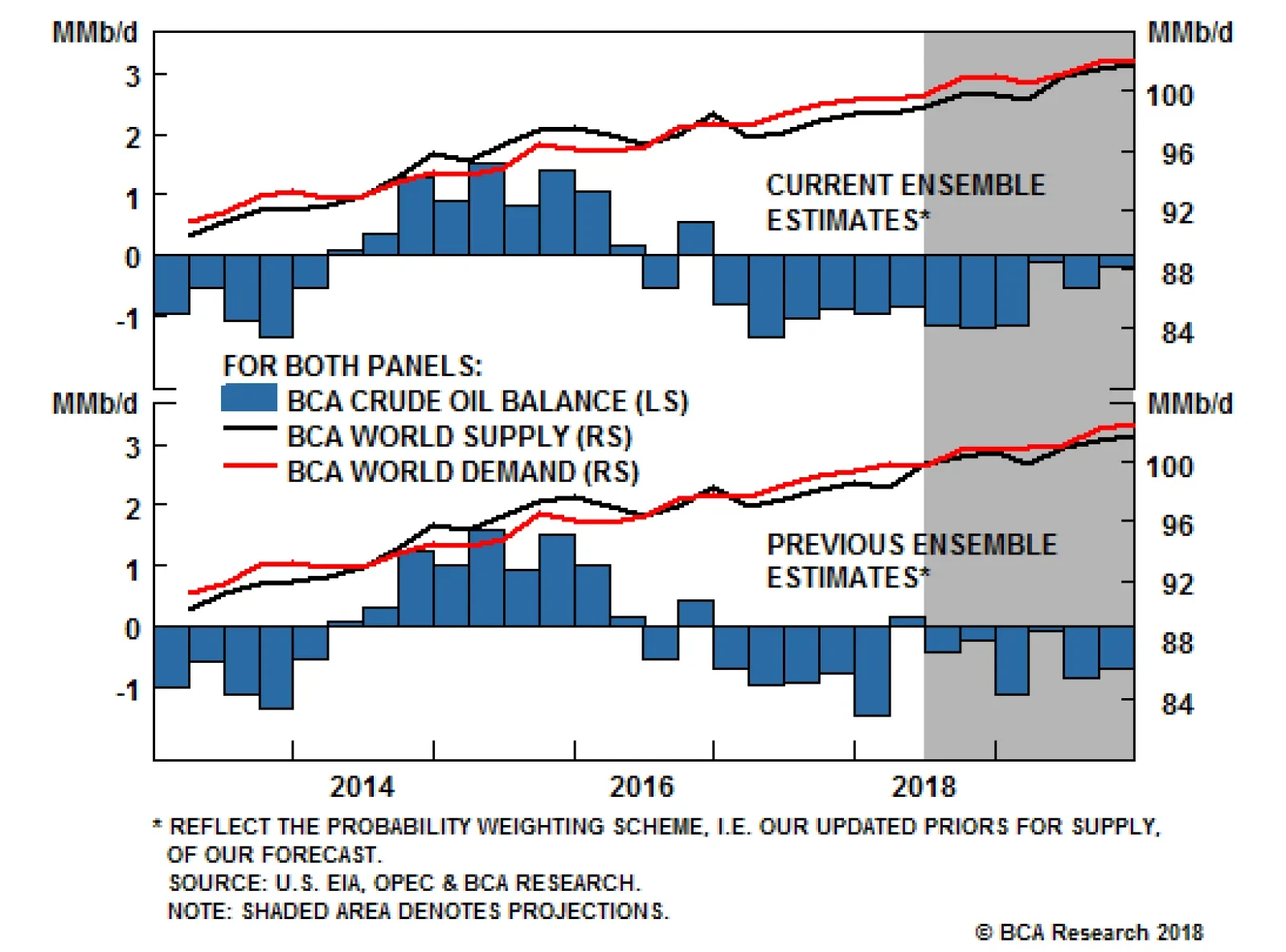

Highlights The risk of unplanned oil-production outages is rising. One or more such events will severely test OPEC 2.0's spare capacity in a supply-constrained market (Chart of the Week).1 As things now stand, OPEC 2.0 spare capacity - if it is available - and a likely U.S. SPR release of 500k b/d in 1Q19 will not cover expected production losses, if markets are hit with another unplanned outage from Libya or Iraq.2 Demand destruction via higher prices will have to balance markets. Oil markets are tightening (Chart 2). Falling supply and stable demand will produce a 1mm b/d physical deficit into 1H19, forcing continued OECD inventory draws (Chart 3). The dominant scenario in our forecast includes a supply shock arising from lost Iranian and Venezuelan exports, which triggers price-induced demand destruction. We raised the odds of Brent prices hitting $100/bbl by 1Q19, and our 2019 forecast to $95/bbl on the back of these factors. Unplanned outages would lift prices higher. Energy: Overweight. The long April, May and June 2019 Brent calls struck at $85/bbl vs short $90/bbl calls we recommended last week are up an average 33.8%, as of Tuesday's close. Base Metals: Neutral. Our foreign-exchange strategists expect the USD to correct further. This will be bullish for copper, which is up ~ 10% since Sept. 11. Precious Metals: Neutral. The USD correction will support gold in the short term. Technically, gold appears to be forming a pennant, which could be short-term bullish. Ags/Softs: Underweight. Corn prices are benefiting from strong exports, according to USDA data. Accumulated exports for the current crop year are up 27% vs last year in the week ending Sept. 13. Chart of the WeekUnplanned Oil-Production Outage Risks Up, OPEC 2.0's Spare Capacity Down

Risks From Unplanned Oil-Outage Rising; OPEC 2.0's Spare Capacity Is Suspect

Risks From Unplanned Oil-Outage Rising; OPEC 2.0's Spare Capacity Is Suspect

Chart 2Physical Oil Deficit Returns##BR##To Oil Market Next Year

Physical Oil Deficit Returns To Oil Market Next Year

Physical Oil Deficit Returns To Oil Market Next Year

Chart 3Fundamentals Support##BR##Strong Prices

Risks From Unplanned Oil-Outage Rising; OPEC 2.0's Spare Capacity Is Suspect

Risks From Unplanned Oil-Outage Rising; OPEC 2.0's Spare Capacity Is Suspect

Feature Oil markets are approaching a moment of truth. OPEC 2.0's spare capacity likely will be put to the test in 1Q19, as Iranian export volumes continue to fall, and other threats to production - Venezuelan losses, and increasing sectarian tension in Iraq and Libya - come to the fore. As the Chart of the Week demonstrates, spare capacity in the traditional OPEC states is low and falling: The U.S. EIA's most recent estimate of OPEC spare capacity is 1.7mm b/d this year and 1.3mm next year, well below the 2.3mm b/d average of 2008 - 2017. For its part, Russia - the other putative leader of OPEC 2.0 - likely only has ~ 200k b/d of spare capacity to ramp. On a relative basis, OPEC spare capacity is even more stretched: This year, the EIA expects it to average 1.7% of global demand. By next year, it is expected to fall to 1.3%, or ~ 1.3mm b/d. This will be lower than the spare capacity reported for 2008 (1.6%), when OPEC (mostly KSA) found itself struggling to meet surging EM demand, and well below the 2.6% average for 2008 - 2017. Spare capacity is very close to levels last seen in 2016, when low prices resulted in supply destruction. In the wake of the oil-price rout of 2014 - 16, capex collapsed as did maintenance spending needed to keep production steady y/y. This can be seen in the relentless decline in OPEC production ex GCC and the stagnation in other states unable to grow output (Chart 4 and Chart 5). Indeed, as prices hit their nadir in 1Q16, sovereign wealth funds (SWFs) in OPEC and non-OPEC states were being liquidated to cover gaping holes in producers' fiscal accounts. This partly explains the growing incidence of unplanned outages, and our contention OPEC spare-capacity claims are highly suspect (Chart of the Week). Chart 4OPEC 2.0's Core Producers Would Be Taxed to Replace Lost Exports

OPEC 2.0's Core Producers Would Be Taxed to Replace Lost Exports

OPEC 2.0's Core Producers Would Be Taxed to Replace Lost Exports

Chart 5Outside Of A Very Few Regions, Oil Production Has Struggled

Outside Of A Very Few Regions, Oil Production Has Struggled

Outside Of A Very Few Regions, Oil Production Has Struggled

U.S. Remains Adamant On Shutting Down Iran's Exports The Trump administration's goal is to reduce Iranian oil exports to zero via the sanctions it will impose beginning November 4 from ~ 2.5mm b/d back in April, when the U.S. sanctions were announced. However, as the EIA data indicates, achieving this goal would leave markets seriously short oil. Indeed, the Washington-based Center for International Strategic Studies (CSIS) noted in late August, "realistically, there is simply not enough readily available spare oil production capacity in the world to replace the loss of all Iranian barrels (some 2.4 mm b/d), coupled with the potential for further reductions in Venezuela, Libya, Nigeria, and elsewhere."3 Our modeling includes 1.25mm b/d of lost Iranian and Venezuelan exports, continued y/y losses in non-core OPEC (Chart 4), constrained U.S. production growth, and stagnate supply growth outside a handful of states able to lift their output (Chart 5). We do not believe OPEC 2.0 spare capacity is sufficient to cover these losses and one or two additional unplanned outages in Iraq or Libya, or anywhere for that matter. In addition, a 500k b/d release of U.S. SPR after the price goes above $90/bbl in 1Q19 will contain the supply shock we expect slightly, but will not completely reverse it. We have long believed KSA's ability to maintain production above 10.5mm b/d for an extended period is suspect, despite its claims it can ramp to its capacity of 12mm b/d.4 We are carrying KSA's current production at 10.4mm b/d in our balances estimates, roughly the level it self-reported to OPEC last month. To be clear, we are not saying KSA's production cannot be increased - perhaps to 10.7mm b/d - but we are dubious it can get to its claimed 12mm b/d capacity, or that it can sustain 10.7mm b/d indefinitely. It is important to note any short-term increase in OPEC 2.0's production will come out of spare capacity available to meet unplanned outages, or deeper-than-expected Venezuelan losses next year. Lastly, unplanned outages in a market already stretched by tighter supply will accelerate the rate of demand destruction via higher prices. This also would accelerate the arrival of a U.S. recession brought about by an oil-price shock, all else equal.5 Iran's Hand Is Strengthening You'd never know it from the declarations of President Trump and U.S. Treasury Secretary Steve Mnuchin - both of whom are adamant in their professed desire to see Iranian oil exports fall to zero - but the U.S. has been attempting to engage Iran in treaty discussions to limit the country's ballistic-missile capabilities and nuclear-development program.6 Not surprisingly, Iranian officials have shown no interest in such discussions. This is a remarkable turn of events, but not unexpected. At some point, it likely became apparent to the Trump administration the global oil markets are on a trajectory for significantly higher prices, as our analysis and forecasts indicate. It also likely is apparent to administration officials that oil prices - and gasoline prices, in particular, which matter most to U.S. voters - will be surging just as the 2020 presidential campaign gets underway next summer. Along with our colleague Marko Papic, who runs BCA's Geopolitical Strategy, we believe that, from a game-theoretic perspective, the approach from the U.S. actually strengthens Iran's hand. Given its history with the previous round of sanctions, and the economic hardships they imposed, the government in Iran likely believes it can ride out 12 to 18 months of renewed sanctions. It is not unrealistic to entertain the possibility Iranian politicians take the bet that sharply higher gasoline prices in the U.S. by 2H19 will give Democrats in U.S. presidential and congressional races - which kick off next summer - a powerful issue with which to campaign against President Trump and the GOP. Bottom Line: There is a non-trivial chance that OPEC 2.0 spare capacity will prove insufficient to cover the losses in Iranian and Venezuelan exports we foresee in the very near term. Should this prove to be the case, the odds that Brent crude oil prices exceed our $95/bbl forecast for next year are high. We believe Iran's political hand could be strengthened, if it rebuffs overtures by the Trump administration to negotiate a treaty to replace the executive agreement with former U.S. president Obama that limited its nuclear program. We recommended getting long Brent call spreads last week to position for the higher prices we are forecasting for next year. Specifically, we recommended getting long April, May and June 2019 Brent calls struck at $85/bbl vs short $90/bbl calls. As of Tuesday's close, these positions were up 33.8% on average vs their opening levels last Thursday. Robert P. Ryan, Senior Vice President Commodity & Energy Strategy rryan@bcaresearch.com Hugo Bélanger, Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com 1 Please see "Upside Risks Dominate BCA's Oil Price Forecast," published by BCA Research's Commodity & Energy Strategy October 26, 2017, and "OPEC 2.0 Scrambles To Reassure Markets," published June 28, 2018. Both are available at ces.bcaresearch.com. 2 OPEC 2.0 is the name we coined for the oil-producer coalition led by the Kingdom of Saudi Arabia (KSA) and Russia, which was formed in November 2016, following the price collapse brought on by OPEC's market-share war launched in November 2014. Please see last week's Commodity & Energy Strategy lead article, "Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl." It is available at ces.bcaresearch.com. In that article we note that, in addition to the highly visible export losses in Iran due to U.S. sanctions and continued deterioration in Venezuelan production, the EIA reduced its estimate of U.S. production growth by 201k b/d in 2019, and the IEA reduced its estimate of Brazilian output this year by 260k b/d. 3 Please see "Whither the Oil Market? Headlines and Tariffs and Bears, Oh My..." published by csis.org August 29, 2018. We are closely following a just-proposed workaround to U.S. sanctions on Iranian oil exports made by the High Representative of the EU, Federica Mogherini, at the UN General Assembly meeting in New York on Tuesday. Ms. Mogherini proposed setting up a special-purpose vehicle that would allow importers in the EU, China and Russia to continue purchasing Iranian oil crude. The SPV would transact in euros, yuan, and roubles, so as to avoid processing transactions through the Society for Worldwide Interbank Financial Telecommunication SWIFT system in Brussels. The SWIFT system is dominated by USD transactions, and the U.S. Treasury has high visibility into transactions made using the system, given USD-denominated transaction like oil purchases and sales must ultimately be cleared through a U.S. bank or intermediary. Iran already takes yuan for its oil, and this mechanism would allow it to purchase goods and services denominated in these currencies. If technical details of the proposed system can be worked out, the SPV could facilitate increased Iranian exports under the U.S. sanctions regime. This would cause us to lower our estimate of lost exports from that country from our baseline assumption of 1.25mm b/d. Please see "Why India Will Struggle to Join Iran's Sanctions Busters," published by bloomberg.com on September 26, 2018. 4 We are not the only ones dubious of KSA's ability to ramp production. Please see "Can Saudi Arabia pump much more oil," published by reuters.com July 1, 2018. 5 In our House view, a recession in the U.S. does not arrive until 2H20. We have argued an oil-supply shock, particularly during a Fed tightening cycle, typically presages a recession in the 6 - 18 months following the shock. Please see Commodity & Energy Strategy lead article, "Odds of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl." It is available at ces.bcaresearch.com. 6 Please see "U.S. seeking to negotiate a treaty with Iran," published September 19, 2018, by reuters.com. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table

Risks From Unplanned Oil-Outage Rising; OPEC 2.0's Spare Capacity Is Suspect

Risks From Unplanned Oil-Outage Rising; OPEC 2.0's Spare Capacity Is Suspect

Trades Closed in 2018 Summary of Trades Closed in 2017

Risks From Unplanned Oil-Outage Rising; OPEC 2.0's Spare Capacity Is Suspect

Risks From Unplanned Oil-Outage Rising; OPEC 2.0's Spare Capacity Is Suspect

Since 2017, the factor model used by our commodity strategists to forecast oil prices shows that brent prices have been supported by two drivers that are simultaneously pushing price estimates higher: First, strong compliance of OPEC 2.0 members to the…

With the loss of Iranian exports occurring faster and sooner than expected, and Venezuela remaining on the brink of collapse, senior energy officials from the U.S., Russia, Saudi Arabia are going to great lengths to reassure their domestic consumers…

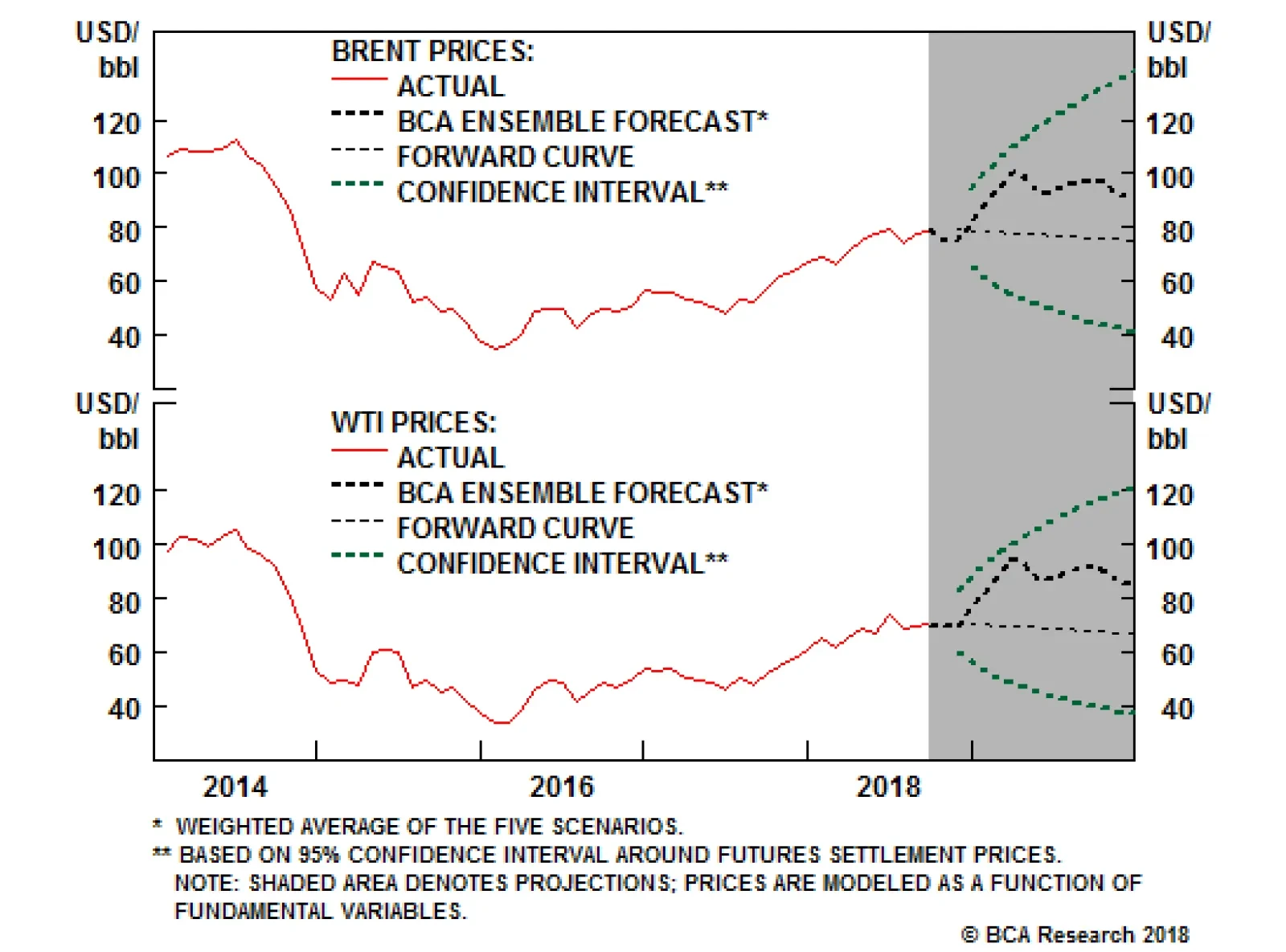

Highlights Recent estimates by ship trackers put the loss of Iranian exports at close to 1mm b/d as of mid-September vs April levels. This loss is higher (and sooner) than our previous baseline expectation, and prompts us to raise our estimate of lost Iranian oil exports to 1.25mm b/d by November, when U.S. sanctions kick in. Venezuela still is close to collapse, but may avoid a complete meltdown with Chinese companies stepping in to safeguard the $50 billion loaned to the country's oil industry.1 We expect production to fall below 1mm b/d next year - to less than half its end-2016 level. With Fed policy likely to continue tightening into 2019 as oil prices surge, the odds of an equity bear market and recession arriving in 2H19 - vs our 2H20 House view - also increase. Our dominant scenario now includes a supply shock and higher prices in 1Q19, which is followed by a U.S. SPR release and price-induced demand destruction (Chart of the Week). As a result, we are raising the odds of Brent prices reaching or exceeding $100/bbl by as early as 1Q19, and lifting our 2019 forecast to $95/bbl. Energy: Overweight. U.S. refining capacity utilization remains close to 19-year highs. At 97.1% of operable capacity, it is within a whisker of the four-week-moving-average highs of 97.3% recorded in August, driven by strong product demand ex U.S. Base Metals: Neutral. The U.S. Treasury granted permission to Rusal's existing customers to continue signing new contracts with the aluminum producer. The announcement stopped short of a full removal of sanctions, which are set to come into effect on October 23. Precious Metals: Neutral. The strong trade-weighted USD continues to hold gold prices on either side of $1,200/oz. We remain long as a portfolio hedge. Ags/Softs: Underweight. The USDA's Crop Production report forecasts record yields for corn and soybeans - 181.3 and 52.8 bushels/acre, respectively - which continues to weigh on prices. The bean harvest is expected to be a record. Feature Chart of the WeekBCA Ensemble Forecast Lifts Brent To $95/bbl, As Market Tightens

BCA Ensemble Forecast Lifts Brent To $95/bbl, As Market Tightens

BCA Ensemble Forecast Lifts Brent To $95/bbl, As Market Tightens

With the loss of Iranian exports occurring faster and sooner than expected, and Venezuela remaining on the brink of collapse, senior energy officials from the U.S., Russia and the Kingdom of Saudi Arabia (KSA) are going to great lengths to reassure their domestic consumers everything - particularly on the supply side - is under control. We are inclined to believe their comfort level re global oil supply is inversely proportional to the amount of reassurance they provide their domestic audiences. The more they meet and talk - particularly to the media - the more concerned they are. And right now, they're pretty concerned. Rick Perry, the U.S. Energy Secretary, held a presser in Moscow following his meeting with Alexander Novak, Russia's Energy Minister, saying the U.S., KSA and Russia can lift output over the next 18 months to compensate for the loss of exports from Iran, Venezuela, and other unplanned outages.2 That might be true, but the market's already tightening far faster and far sooner than many analysts expected. Covering a supply shortfall in 18 months does nothing for the market over the next few months, particularly with demand remaining robust (Chart 2) and OECD inventories falling (Chart 3). Since 2017, our factor model shows Brent prices have been supported by two factors acting simultaneously together: Chart 2Fundamentals Support Strong Prices

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Chart 3Inventory Draws Will Accelerate

Inventory Draws Will Accelerate

Inventory Draws Will Accelerate

Strong compliance of OPEC 2.0 members to the coalition's production-cutting agreement, which reduced the OPEC Supply-and-Inventory factor's role, and The pickup in global oil demand, particularly in EM economies, which pushed our Global Demand factor up. These effects were partly counterbalanced by the rise in our non-OPEC Supply factor - driven by strong growth in U.S. shale-oil output - which became the largest negative contributor to price movements. Global demand's been strengthening since the end of 1H17 on the back of stellar EM income growth. This remains the fundamental backdrop to global oil for now. While our base case remains relatively supportive for oil prices, we are raising the odds of a price spike resulting from a supply shock as early as 1Q19 on the back of larger- and faster-than-expected Iranian export losses, and continued declines in Venezuelan production. Should this occur, we believe it would trigger a U.S. SPR release, and produce demand destruction at a rate that could be faster than historical experience would suggest (Table 1). This further tightens balances, and leads us to raise our 2019 forecast for Brent crude oil to $95/bbl on average, up from $80/bbl last month, with WTI trading $6/bbl below that (Chart 4). This forecast is highly conditional, given our assumptions re supply-side variables, a U.S. SPR release, and demand destruction estimates. Table 1BCA Global Oil Supply - Demand Balances (MMb/d) (Base Case Balances)

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Chart 4BCA's Oil Balances Tighter

BCA's Oil Balances Tighter

BCA's Oil Balances Tighter

Oil Balances Tighten As Supply Contracts In our monthly balances update, we are incorporating a sharply accelerated loss of Iranian export barrels to the market, which already is evident. Bloomberg this week reported its tanker-tracking service registered a decline in Iranian exports of close to 1mm b/d between April, when sanctions were announced, and mid-September.3 At this rate, the assessment by Platts Analytics last week that as much as 1.4mm b/d of Iranian exports could be lost by the time U.S. sanctions kick in November 4 appears more likely.4 However, to be conservative, we are building in a loss of 1.25mm b/d in our balances, and have it developing over the July - November period in increments of 250k b/d, instead of the November - February interval we assumed in last month's balances. We will monitor this situation and revise our estimates as new information arrives. Also on the supply side, we are assuming the U.S. SPR releases 500k b/d starting a month after Brent prices go over $90/bbl in March 2019. This is in line with the SPR's enabling legislation, which limits drawdowns to 30mm b/d over a 60-day period, after the President authorizes such action to meet a severe energy supply interruption. Lastly, we continue to carry supply constraints arising from the lack of sufficient take-away capacity to get all of the crude produced in the Permian Basin to refining markets in our models. To wit: We continue to expect 1.2mm b/d of supply growth from the U.S. shales, driven largely by Permian production, vs an earlier expectation of 1.4mm b/d of growth. We expect the Permian to be de-bottlenecked by 4Q19. We expect the Big 3 producers Secretary Perry expects to fill supply gaps in 18 months - the U.S., Russia, and KSA - to produce 10.83mm, 11.4mm and 10.4mm b/d in 2H18, and 11.79mm, 11.43mm and 10.4mm b/d next year, respectively. They will get some help from OPEC's Gulf Arab producers - i.e., the core OPEC producers (Chart 5) - but, supply will continue to fall/stagnate in most of the rest of the world, particularly in offshore producers (Chart 6). Chart 5While Core OPEC Can Increase Supply...

While Core OPEC Can Increase Supply...

While Core OPEC Can Increase Supply...

Chart 6... 'The Other Guys' Output Stagnates

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

We also note the EIA and IEA have lowered their supply-growth estimates this month. The EIA this month reduced expected U.S. crude production growth by 210k b/d in 2019, and the IEA lowered its estimate of offshore production growth in Brazil from 260k b/d to just 30k b/d this year. These are non-trivial adjustments in a market that was tight prior to the downgrade in supply growth. Still, there are significant marginal disagreements on the supply side among the major data supporters (the EIA, IEA and OPEC), which can be seen in Table 2. Table 2Comparison Of Major Balances Estimates

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Demand Destruction Likely As Prices Spike In 1Q19 We expect the rate of growth in EM incomes and trade - a proxy for income - to slow slightly this year vs 2017, on the back of a strengthening USD. This will reduce the rate of growth in EM imports and the rate of growth in EM commodity demand, at the margin. However, y/y growth in EM incomes is expected to remain positive over the next 12 months in our baseline scenario, which will keep the level of commodity demand - particularly for oil and industrial metals - robust. This will drive global demand growth of ~ 1.6mm b/d this year, roughly unchanged from last month. Higher prices risk slowing next year's growth. This is where it gets tricky. An oil-supply shock occurring when global demand is strong most likely will produce a price spike, as we've been arguing for the past several weeks.5 This price spike, coupled with continued monetary-policy tightening by the Fed, raises the likelihood of demand destruction globally. Higher oil prices and a stronger USD act as a double-whammy on EM oil demand. The problem we have now is gauging the elasticity of oil demand, particularly in EM. Oil markets are fundamentally different now than at any point in the modern era - roughly beginning in the early 1960s with the ascendance of OPEC - because many big oil-importing EM economies removed or relaxed subsidies following the prices collapse of 2014 - 2016. Prominent among these states are China and India. OPEC states also took advantage of the price collapse to relax or remove subsidies, e.g., KSA.6 The price shock we anticipate, therefore, will be the first in the modern era in which EM consumers - the principal driver of oil demand in the world, accounting for roughly 70% of the demand growth we expect - are exposed directly to higher prices. How quickly they will respond to higher prices is unknown. For this reason, we're introducing what we consider a reasonable first approximation of how EM demand might respond to higher prices and a stronger USD into the scenarios we include in our ensemble forecast (Chart 7). As a first approximation - subject to at least monthly adjustment, as more data become available - we are modeling a 100k b/d loss of demand for every $10/bbl increase in crude oil prices.7 We will continue to iterate on this as new information becomes available. Chart 7Ensemble Scenarios Reflect New Risks

Ensemble Scenarios Reflect New Risks

Ensemble Scenarios Reflect New Risks

Bottom Line: We've raised the odds of a supply shock in the oil markets that takes Brent prices to or through $100/bbl by 1Q19. Should this occur, we expect it will be met by a U.S. SPR release of 500k b/d a month after prices breach $90/bbl. This price spike will set off a round of demand destruction, which we expect will be quicker than history would suggest, given many large EM oil-consuming states have relaxed or eliminated fuel subsidies, leaving their consumers exposed to the price shock. This will be exacerbated by a stronger USD going forward, as the Fed likely looks through the price spike and continues with its policy-rate normalization. In this scenario, a U.S. recession could arrive in 2H19 vs our House view of 2H20 or later. In addition, we would expect an equity bear market to ensue sooner than presently anticipated. We recommend using Brent call spreads to express the view consistent with our research. At tonight's close, we will go long April, May and June 2019 calls struck at $85/bbl and short $90/bbl calls. Robert P. Ryan, Senior Vice President Commodity & Energy Strategy rryan@bcaresearch.com Hugo Bélanger, Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com 1 Please see "Venezuela hands China more oil presence, but no mention of new funds," published by reuters.com September 14, 2018. 2 U.S. Energy Secretary Rick Perry made this claim at a press conference after meeting with Russian Energy Minister Alexander Novak last Friday. Please see "Big Three oil states can offset fall in Iran supplies: Perry," published by reuters.com September 14, 2018. 3 Please see "Saudi Arabia Is Comfortable With Brent Oil Above $80," published by bloomberg.com September 18, 2018. 4 Please see "OPEC crude oil production rises to 32.89 mil b/d in Aug as cuts unwind: Platts survey" published by SP Platts Global September 6, 2018. 5 Please see "Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge," published by BCA Research's Commodity & Energy Strategy Weekly Report on September 13, 2018. It is available at ces.bcaresearch.com. For a discussion of the effect of a stronger USD on global oil demand, please see "Trade, Dollars, Oil & Metals ... Assessing Downside Risk," published by the Commodity & Energy Strategy August 23, 2018. 6 Please see the Special Focus in the World Bank's January 2018 Global Economic Prospects entitled "With The Benefit of Hindsight: The Impact of the 2014 - 16 Oil Price Collapse," beginning on p. 49. 7 In this simulation, we employ an iterative one-step-ahead forecasting methodology that reduces demand by 100k b/d for every $10/bbl increase in prices. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Trades Closed in 2017 Summary of Trades Closed in 2018

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Odds Of Oil-Price Spike In 1H19 Rise; 2019 Brent Forecast Lifted $15 To $95/bbl

Highlights Oil markets and U.S. monetary policy are tightening coincidentally. This confluence of events in the past typically presages an equity correction and recession in the U.S. in the following 6 to 18 months (Chart of the Week). EM economies also could weaken as Fed policy collides with the oil-price spike we expect in the wake of a supply shock. In spite of continuing pressure from the Fed's policy-rate normalization policy, we continue to favor gold as a portfolio hedge (see below). Energy: Overweight. Russia's energy minister Alexander Novak expressed his determination to cooperate with OPEC to evolve the current production cut and emphasized his willingness to maintain a stable market, as reported by Platts on Tuesday.1 Base Metals: Neutral. Alcoa workers at Western Australian alumina and bauxite facilities voted to extend a strike initiated on August 8. Precious Metals: Neutral. The odds of sharply higher oil prices colliding with rising U.S. interest rates are increasing as the year winds down. Gold will outperform equities in this environment. Ags/Softs: Underweight. Brazilian farmers are lobbying Chinese consumers and Argentine suppliers to establish a futures contract tailored for delivery of soybeans from Latin America to China.2 Feature Oil markets continue to tighten, as the now fully discounted loss of ~ 2mm b/d of Iranian and Venezuelan exports is compounded by additional supply-side concerns in Iraq and Libya, and razor-thin OPEC spare capacity. Global demand remains robust. Against this backdrop, it is hardly surprising the energy ministers of the Kingdom of Saudi Arabia (KSA) and Russia are huddling with the U.S. Energy Secretary this week to discuss oil markets in separate meetings on opposite sides of the globe.3 The risk an oil-supply shock collides with tightening monetary conditions in the U.S. is rising, as the Fed continues its rates-normalization policy. This potent confluence of risks, which could push Brent prices above $120/bbl, raises the odds of a sharp correction in U.S. equities (Chart of the Week). It also could pull the recession we expect in 2020 into 2019. This is a risk assessment, not our baseline scenario. While the odds of an oil-price spike accompanied by higher interest rates are increasing, we are not changing our view of oil or gold markets: We expect Brent crude to average $70/bbl in 2H18 and $80/bbl in 2019. We also remain long gold as a portfolio hedge against higher inflation this year and next, and expect the Fed to stay the course on its rates-normalization policy.4 Chart of the WeekOil Price Spikes + Rising U.S. Interest Rates Typically Presage S&P 500 Sell-Off

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

That said, gold will remain one of the best indicators of how markets assess the Fed's willingness to lean into its rates policy: If prices weaken further, it will signal markets are pricing in continued tightness in U.S. monetary policy. Any weakness resulting from this expectation will be an opportunity to get long (or longer) gold as a portfolio hedge, particularly if oil markets tighten as we expect. Energy Ministers Meet As Oil Markets Tighten KSA's minister, Khalid al-Falih, and U.S. Energy Secretary Rick Perry met in Washington this past Monday, and Perry is due to travel to Moscow for a scheduled visit today. The increasing likelihood of 2mm b/d of exports being lost to U.S. sanctions against Iran later this year, and the imminent collapse of Venezuela, provides the context for these meetings. Platts Analytics estimates as much as 1.4mm b/d of Iranian exports could be lost to the market by the time U.S. sanctions against that country kick in in November. In our base case, we expect a loss of 1mm b/d, which keeps the global market in a physical deficit next year (Chart 2). Total OPEC production in August is estimated by Platts at 32.9mm b/d, a 10-month high, with output in Iraq surging to 4.7mm b/d and to 940k b/d in Libya.5 That Iraqi and Libyan production surge is increasingly at risk, however. In addition to the fully discounted Iranian and Venezuelan risk, we expect American, Saudi and Russian ministers also will discuss the growing risk to Iraq's and Libya's production, and its implications for global supply.6 Civil unrest in these states raises the risk of additional unplanned outages over the near term just as output is recovering.7 Concerns over razor-thin OPEC spare capacity - equal to ~ 1.5% to 2.0% of global demand - and continued strong global consumption likely number among their concerns, as well. In our view, these factors strongly suggest the oil market is setting up for a supply shock that could lift prices above $120/bbl (Chart 3). Chart 2Physical Deficits Could Widen

Physical Deficits Could Widen

Physical Deficits Could Widen

Chart 3High-Price Scenarios Becoming More Likely

High-Price Scenarios Becoming More Likely

High-Price Scenarios Becoming More Likely

Fed Policy Could Collide With Oil Price Spike With the U.S. economy at or very near full capacity, unemployment below 4%, and inflation and inflation expectations ticking higher, we believe the Fed will remain focused on its rates-normalization policy. This increases the risk an oil-supply shock collides with tightening monetary conditions in the U.S. is rising. If the Fed looks through the oil-price spike we expect in the next 6 to 12 months - treating it as a transitory event - its rates-normalization policy will become problematic for the U.S. and global economies. Such a reading by the Fed would be a policy error, in our estimation. As shown in the Chart of the Week, an oil-supply shock accompanied by continued Fed tightening raises the risk of a sharp correction in U.S. equity markets, and perhaps could trigger a bear market. In addition, the recession we expect later in 2020 could be pulled into 2019. As shown in Table 1, 10 out of the 11 recessions in the U.S. since 1945 were preceded by spikes in oil prices. Not every rise in oil prices was accompanied by a recession. In other words, recessions in the U.S. are usually preceded by spikes in oil prices, but not all spikes in oil prices are followed by recessions. This is important, as it implies that forecasting a recession based solely on rises in oil prices can sometimes misfire. Table 1History Of Oil Supply Shocks

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

On the other hand, an oil-price shock combined with a rate-tightening cycle presents a more reliable recession signal. In fact, since 1970, every time the Fed-funds rate rose by more than ~200bps and oil prices rose by more than 50%, the U.S. business cycle peaked in the following 6-18 months.8 EM Growth Threatened, As Well As the Fed proceeds with its policy-rate normalization, the broad trade-weighted USD (USD TWIB) will strengthen. A sharp increase in oil prices accompanied by continued strength in the USD TWIB will redound to the detriment of EM economies, reducing demand for commodities generally, as the local currency costs of all USD-denominated goods increases. The confluence of these factors - should they materialize - would reduce EM income growth - perhaps even cause a contraction - and would produce a medium-term deflationary impulse, along with a rush to U.S. treasuries and other safe-haven assets. This would lower U.S. interest rates, all else equal, forcing the Fed to put its rates-normalization policy on hold, and possibly reverse it.9 Favor Gold, If Oil Spikes And Rates Rise In sum, the U.S. economy is at or very near full capacity, which will keep the Fed focused on its rates-normalization process. This will likely cause the Fed to treat the oil-price spike we expect on the back of a supply-side shock over the next 6 - 12 months as transitory. The Fed won't view it as a true inflationary threat, and will continue with its rates policy, as its core inflation gauge - the U.S. PCEPI ex food and energy - continues to move higher. Over the short run, this would look like U.S. real rates are falling, boosting the appeal of gold. However, the oil-price spike plus a maintained bias by the Fed to continue raising policy rates will lift the USD TWIB, even as oil prices remain high. This will be a double-whammy to EM economies - the absolute price of oil in USD will rise significantly, even as a stronger USD raises the cost of all other dollar-denominated goods and services. This will reduce disposable income and lower aggregate demand in EM economies. Should the Fed misread the oil-price spike in a rising interest-rate environment, we believe holding gold in a diversified portfolio continues to make sense. Gold outperforms in rising inflation environments, and when demand for safe-havens increases. In addition, gold outperforms equities in periods of declining stock markets (Chart 4). This convexity on the upside and downside is one of gold's strongest attributes. Bottom Line: Given the continued pressure on gold from the Fed's rates-normalization policy, the yellow metal will remain an inexpensive portfolio hedge. Gold prices are currently below or close to their long-term average when expressed in terms of the S&P 500 or oil units (Chart 5). Hence, diverting limited amount from equity to gold is recommended on a risk-adjusted basis. Chart 4Gold V. S&P 500

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

Chart 5Gold Is Relatively Cheap

Gold Is Relatively Cheap

Gold Is Relatively Cheap

Robert P. Ryan, Senior Vice President Commodity & Energy Strategy rryan@bcaresearch.com Hugo Bélanger, Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com 1 Please see "Russian energy minister Novak sees broader OPEC, Russia, allies cooperation charter 'expedient' from Jan 1, 2019" published by SP Platts Global on September 11, 2018. 2 Please see "Brazil Farmers Vie For Soy Contract During U.S. - China Trade War," published by reuters.com on September 10, 2018. 3 Please see "U.S. and Saudi energy ministers to meet in Washington: DOE," and "Russia's Novak to meet with U.S. counterpart Perry, discuss oil markets," both published by reuters.com on September 10, 2018. 4 Our view is aligned with BCA's U.S. Bond Strategy, which can be found in "The Powell Doctrine Emerges" published September 4, 2018. It is available at usbs.bcaresearch.com. 5 Please see "OPEC crude oil production rises to 32.89 mil b/d in Aug as cuts unwind: Platts survey" published by SP Platts Global September 6, 2018. Noteworthy in the Platts analysis is the KSA increase to 10.5mm b/d. NB: We will be updating our balances next week. See also "U.S. warns Iran it will respond to attacks by Tehran allies in Iraq" published by reuters.com on September 11, 2018. 6 Rising secular tensions in Iraq - particularly vis-à-vis Iran's role in that state - could threaten production and exports there, as we discussed in the Special Report we published last week, in concert with BCA's Geopolitical Strategy. Please see "Iraq: The Fulcrum Of Middle East Geopolitics And Global Oil Supply" published September 5, 2018, and "Iraq Is The Prize In U.S. - Iran Sanctions Conflict" published June 7, 2018. Both are available at ces.bcaresearch.com. 7 Civil order in Libya is collapsing. The Islamic State is increasing the tempo of its operations in and around Libya; forces loyal to the late dictator late Muammar Qaddafi staged a mass escape from a Tripoli prison earlier this month; and local militia are threatening to extend the Libyan unrest into neighboring states. Please see "Libya's Haftar threatens to 'spread war' to Algeria" reported by Arab News September 11, 2018; "Masked gunmen attack Libyan oil corporation HQ in Tripoli," published by The Guardian September 10, 2018; and "Hundreds escape in jailbreak near Libyan capital" published by The National in the UAE September 3, 2018. 8 These effects are not constant or fixed. Each period has its own specificities implying a range around the rate hike and oil-prices spike necessary to disrupt the economy. 9 Please see BCA Commodity & Energy Strategy Weekly Report, "Trade, Dollars, Oil & Metals ... Assessing Downside Risk" published August 23, 2018, available at ces.bcaresearch.com. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

Trades Closed in 2018 Summary of Trades Closed in 2017

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

Oil-Supply Shock, Rising U.S. Rates Favor Gold As A Portfolio Hedge

Highlights The U.S. midterm elections are far less investment-relevant than consensus holds; Trump will increase the pressure on China and Iran regardless of the likely negative election results for the GOP; The Iranian sanctions, civil conflict in Iraq, and other oil supply issues are the real geopolitical risk; Despite the tentative good news on Brexit, political uncertainty in the U.K. makes now a bad time to buy the pound; Go long Brent crude / short S&P 500; long U.S. energy / tech equities; long JPY / short GBP. Feature The U.S. political cycle begins in earnest after Labor Day. Understandably, we have noticed an uptick in client interest, with a steady stream of questions and conference call requests about U.S. politics. Generally, our forecast remains unchanged since our April net assessment of the upcoming midterm election.1 Democrats have a slightly better than 60% probability of winning the House of Representatives, with a solid 45% probability of taking the Senate, and rising. The latter is astounding, given that the "math" of the Senate rotation is against the Democrats. Our bias toward a Democratic victory is based on current polling (Chart 1) and President Trump's woeful approval rating (Chart 2). There are a lot of other moving parts, however, and we will update them next week in detail. Chart 1GOP Trails In Polls, But It Is Still Close

GOP Trails In Polls, But It Is Still Close

GOP Trails In Polls, But It Is Still Close

Chart 2Trump's Approval Rating Lines The GOP Up For Steep Losses

Fade The Midterms, Not Iraq Or Brexit

Fade The Midterms, Not Iraq Or Brexit