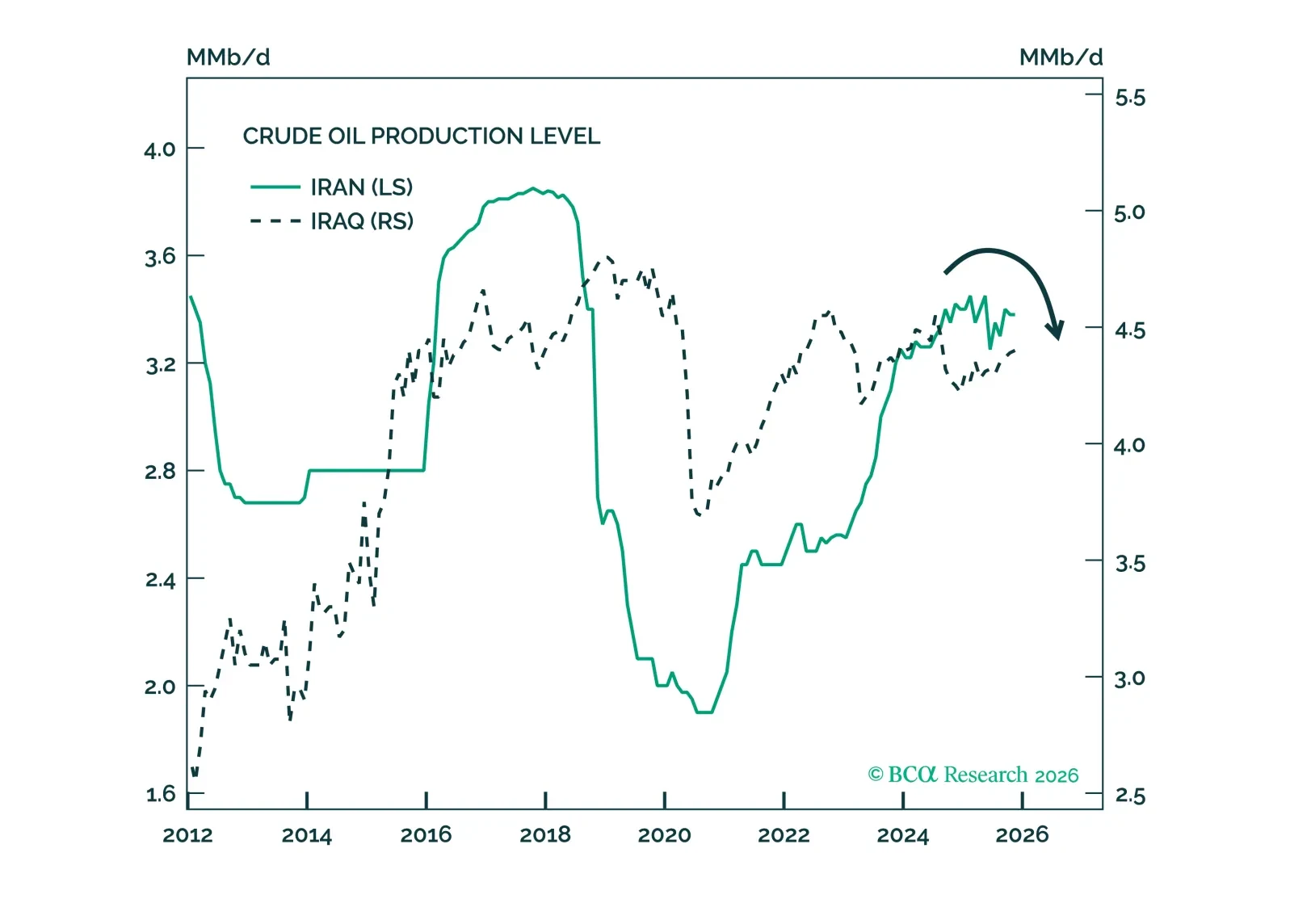

Oil

It is too soon to sell the rip in oil or buy the dip in stocks. Stick with risk-off trades for now.

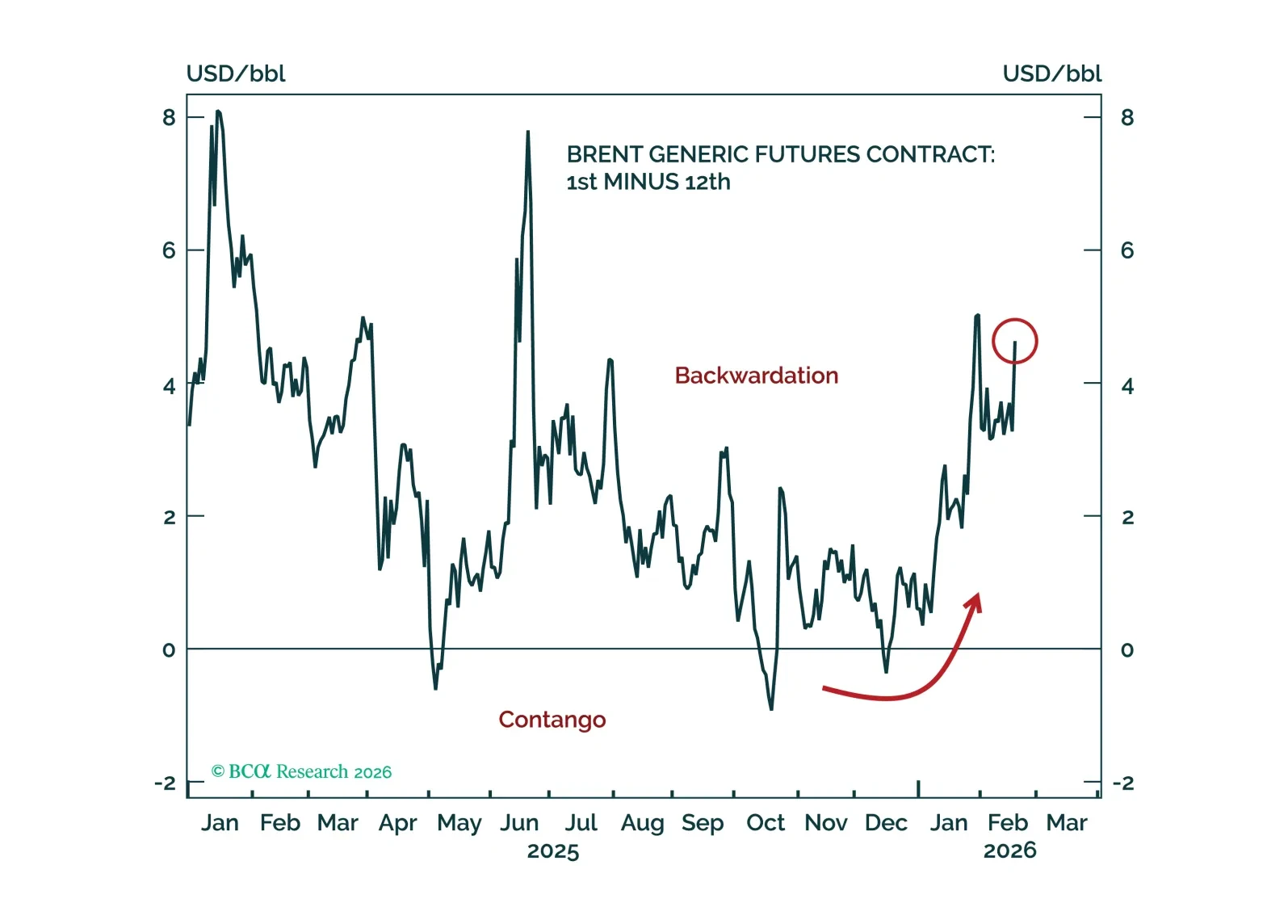

Middle East hostilities have triggered risk-off moves and pushed oil prices higher. Previous geopolitically driven oil price disruptions suggest that speed, persistence and equity market vulnerability relate to the degree of the market sell off. At the other end of the spectrum, energy stocks should benefit, but have already rallied significantly.

MacroQuant recommends a modest overweight position in equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has downgraded oil to neutral, and is bullish on copper and gold.

Oil price risks remain skewed to the upside over the near term as geopolitical risks continue to dominate.

Nevertheless, we ultimately expect bearish fundamentals to reassert themselves over a six-to-12-month timeframe and drive oil prices lower.

Sell America? No. The GeoMacro trade is Buy RoW! Left-tail risks are easing because the US isn’t collapsing. That argues for less enthusiasm for safe havens, not selling US assets. The S&P 500 can perform while remaining underweight the US – it happened in 2025 and will happen again.

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

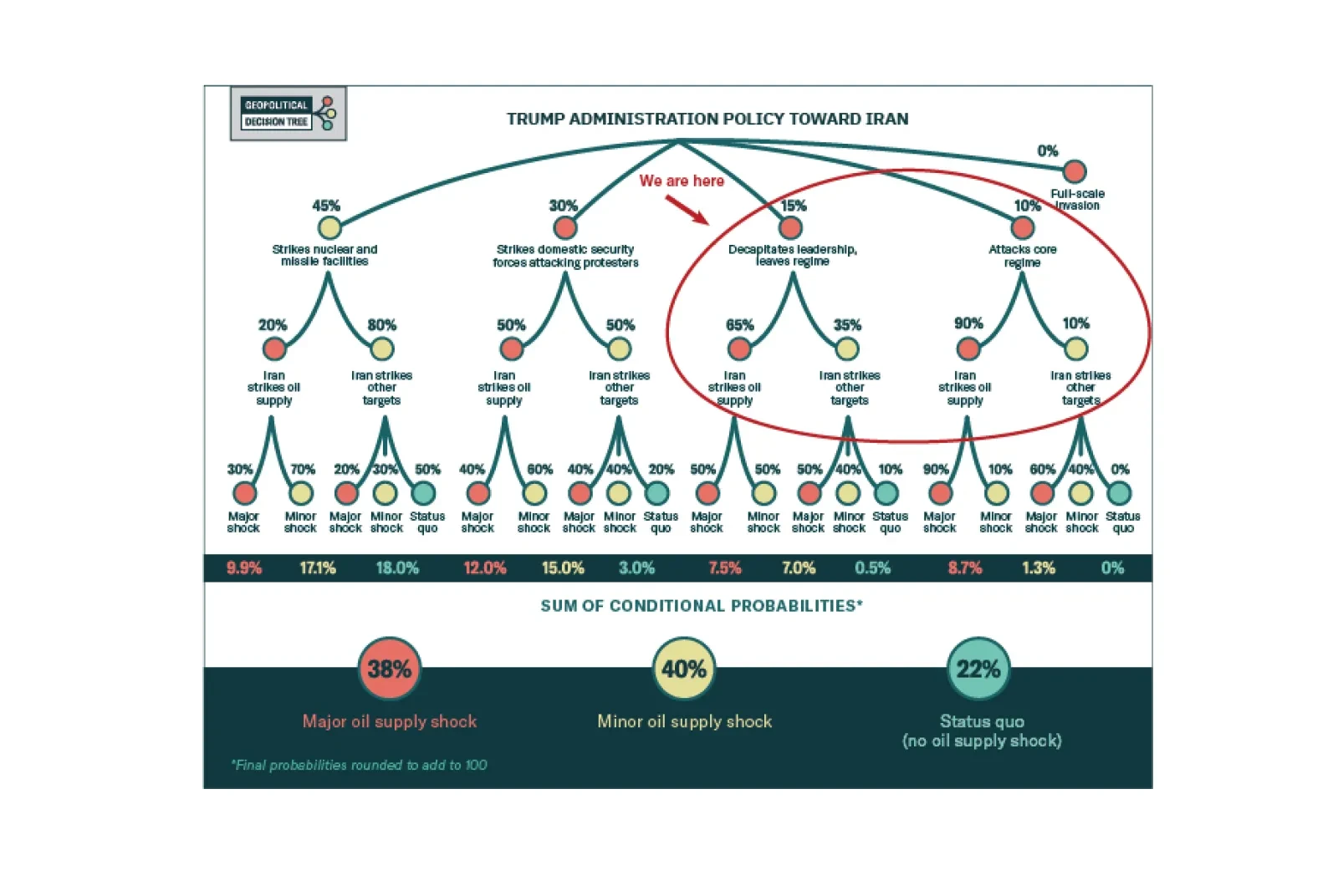

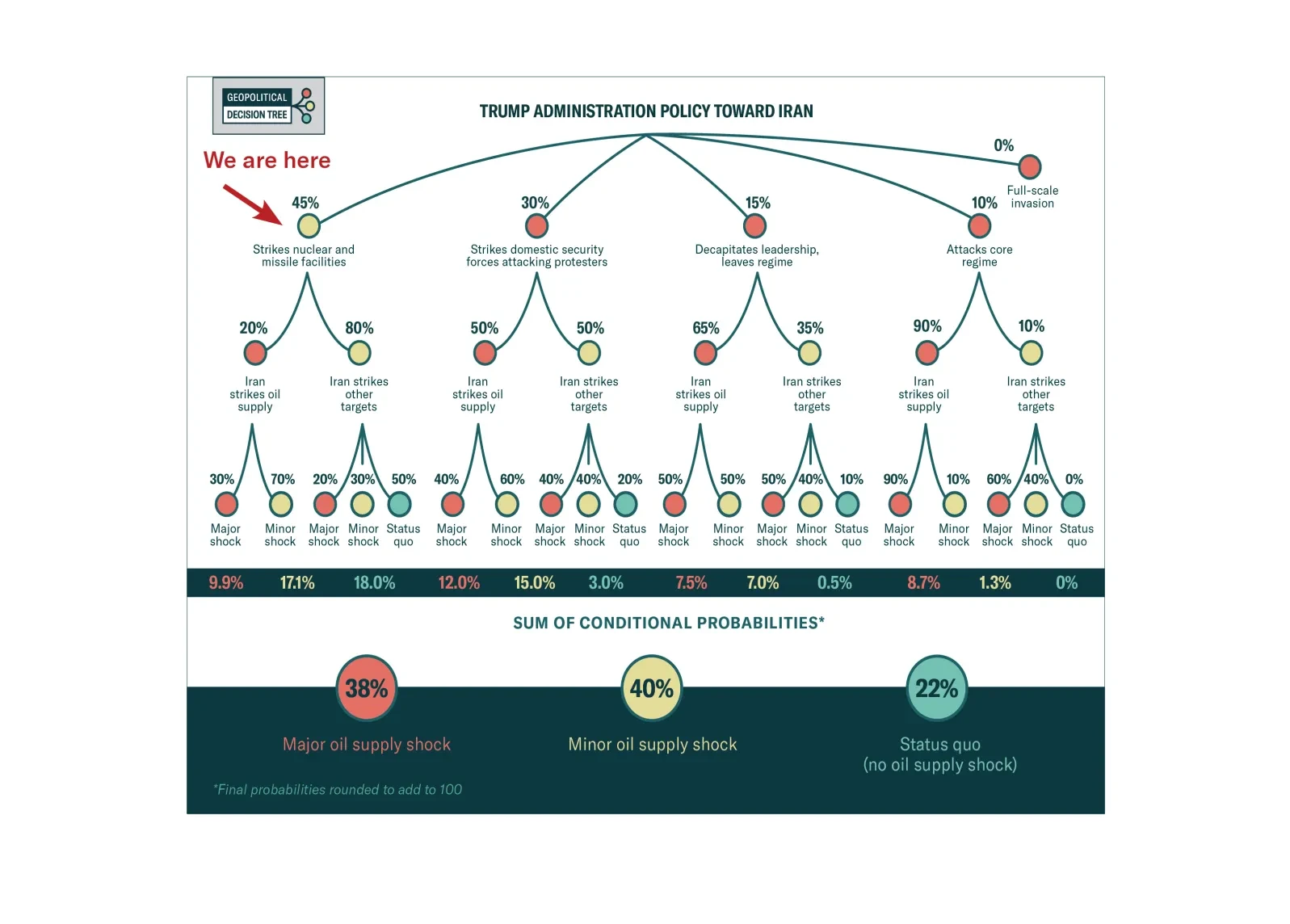

The US is likely to take significant military action in Iran, justifying our 40% risk of a major oil shock. Tactically go long Brent crude.

The risk to Iran's regime survival raises the probability of a massive global oil supply shock back to around 40%, where we put it last year.

Venezuelan crude output is unlikely to alter the global oil market outlook for this year. However, US control of Venezuelan crude is a risk to Canadian oil sands producers and Canadian oil prices. Go long US oil refiners/short Canadian oil producers.

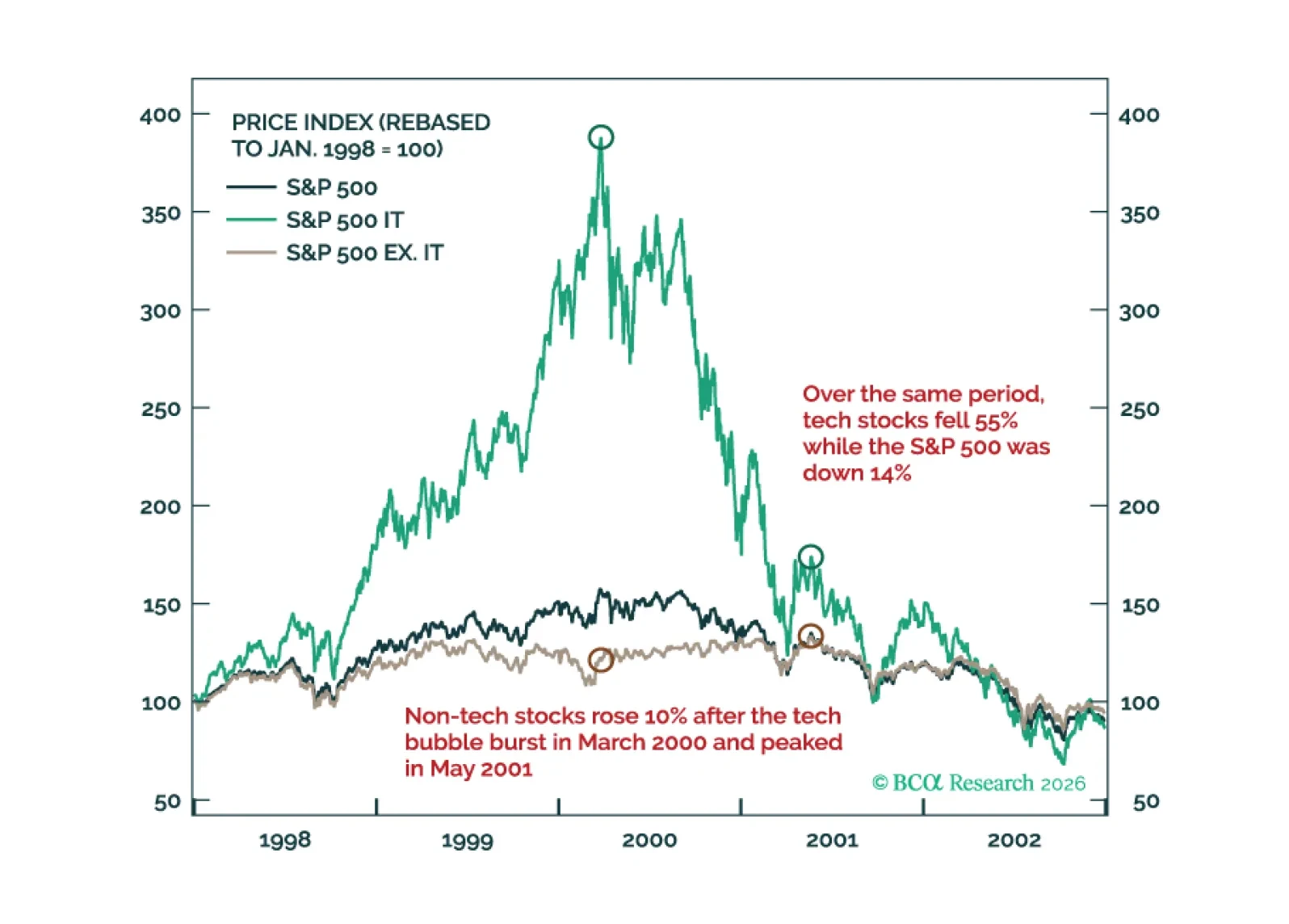

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.