Oil

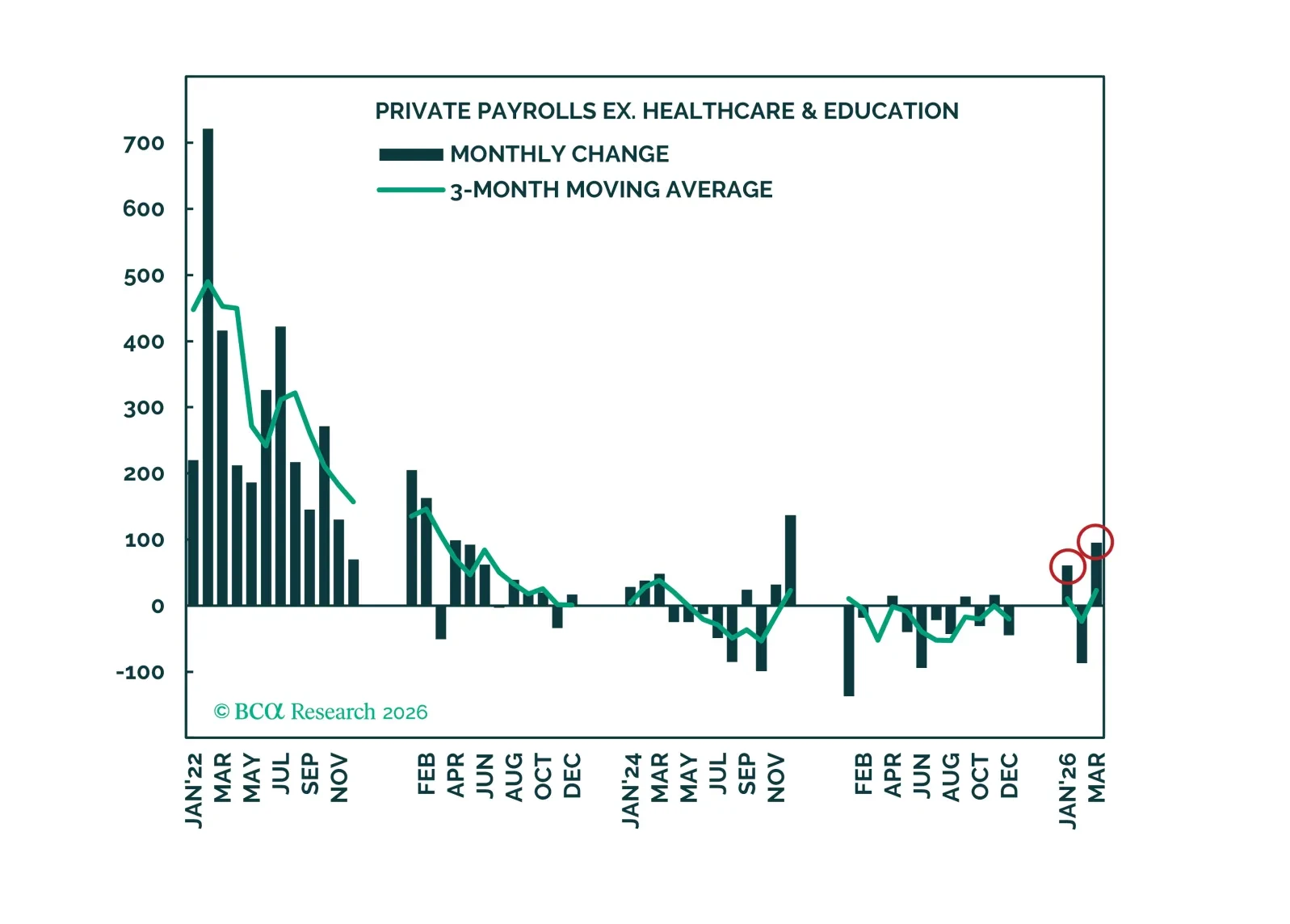

The labor market showed signs of reviving in the first three months of this year, but it is yet to be determined how consumers will react to the energy supply shock. We reiterate our benchmark asset allocation recommendations, but are skeptical that S&P 500 earnings growth will meet outsized expectations over the rest of 2026.

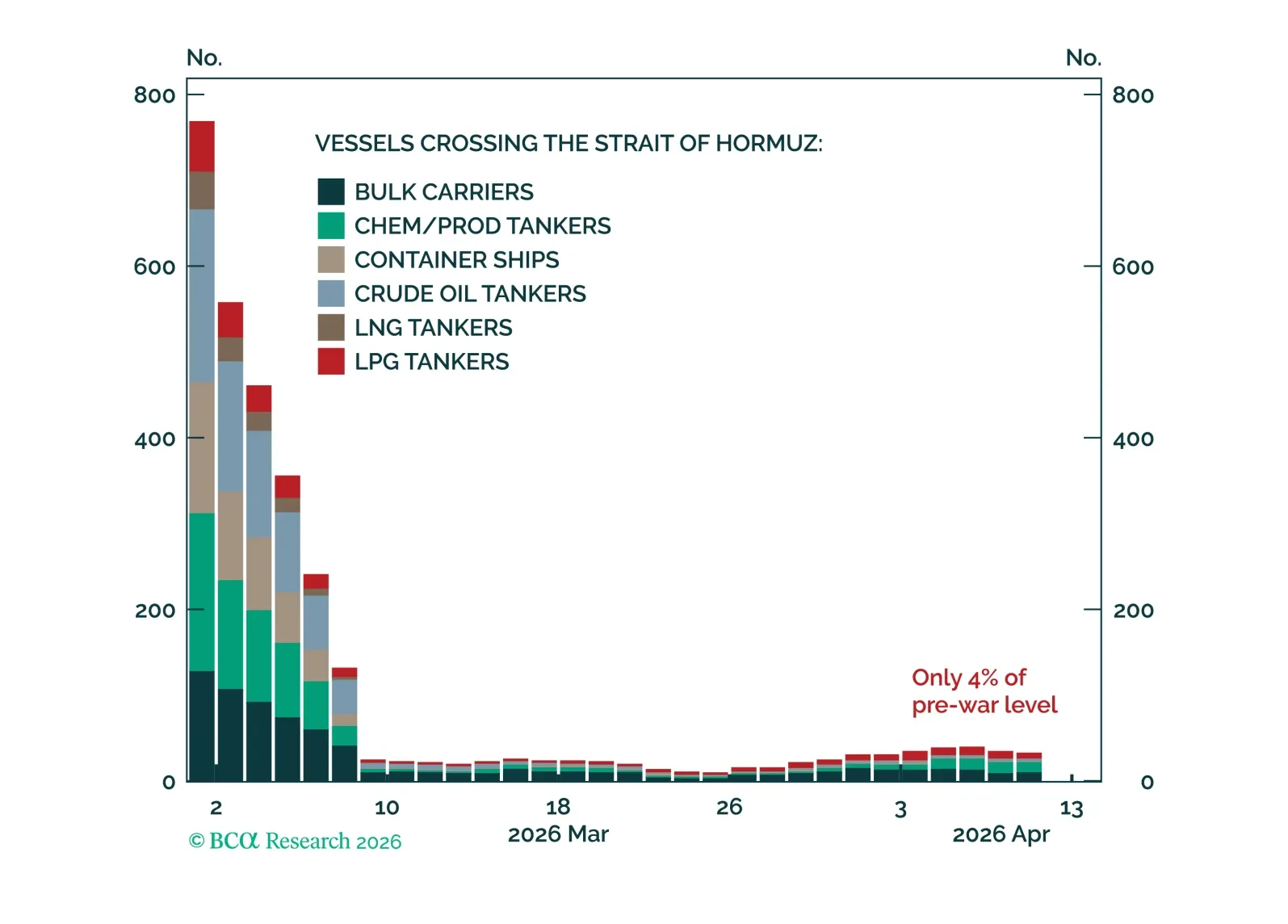

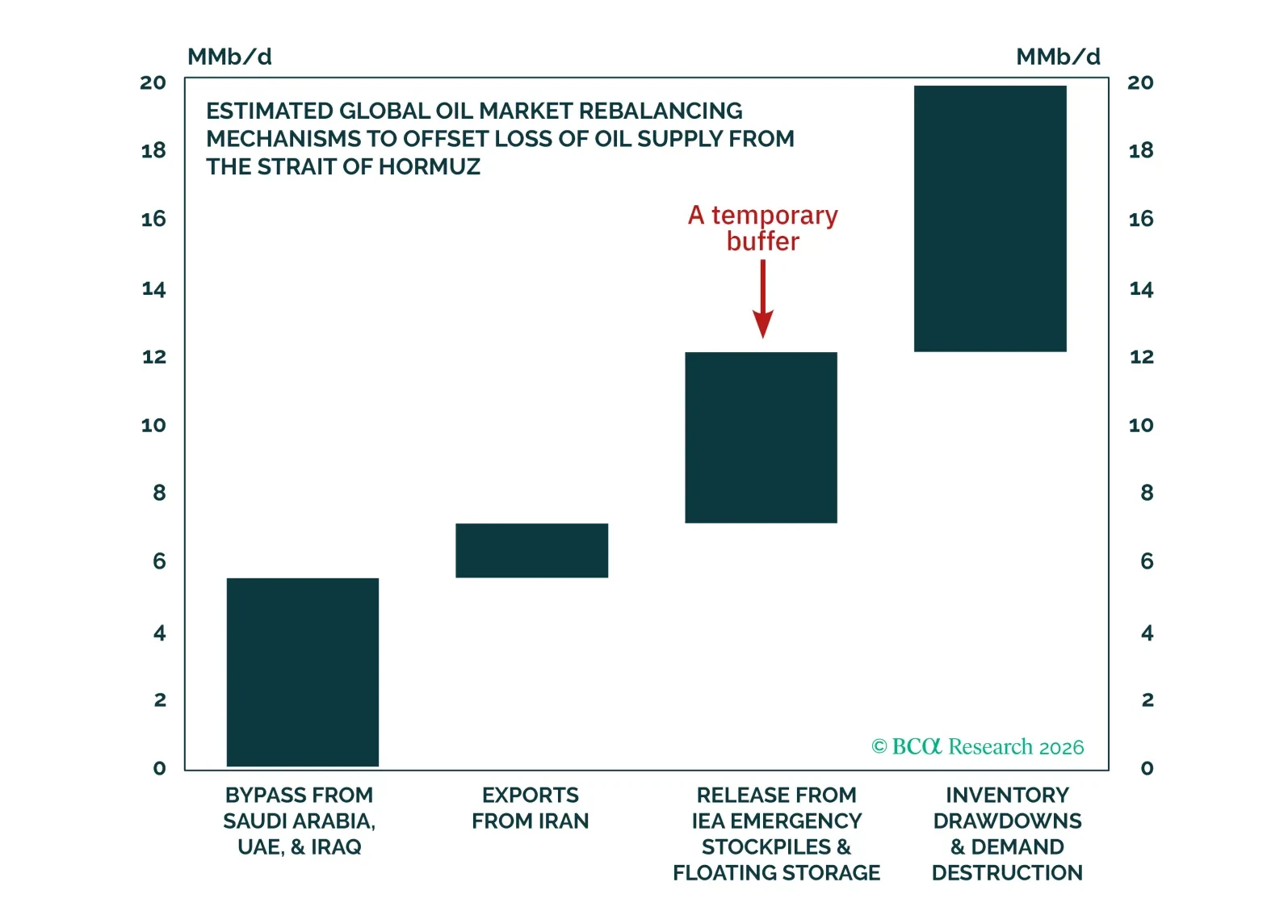

In this report, we deviate from our base case and instead assume that there is an immediate improvement in Hormuz traffic. This exercise allows us to explore how the global oil supply shortfall could eventually be offset if the right conditions are in place.

The relief rally in stocks can continue a while longer. However, much can still go wrong. As such, we are retaining a 12-month underweight to stocks but are moving to neutral on a short-term tactical horizon.

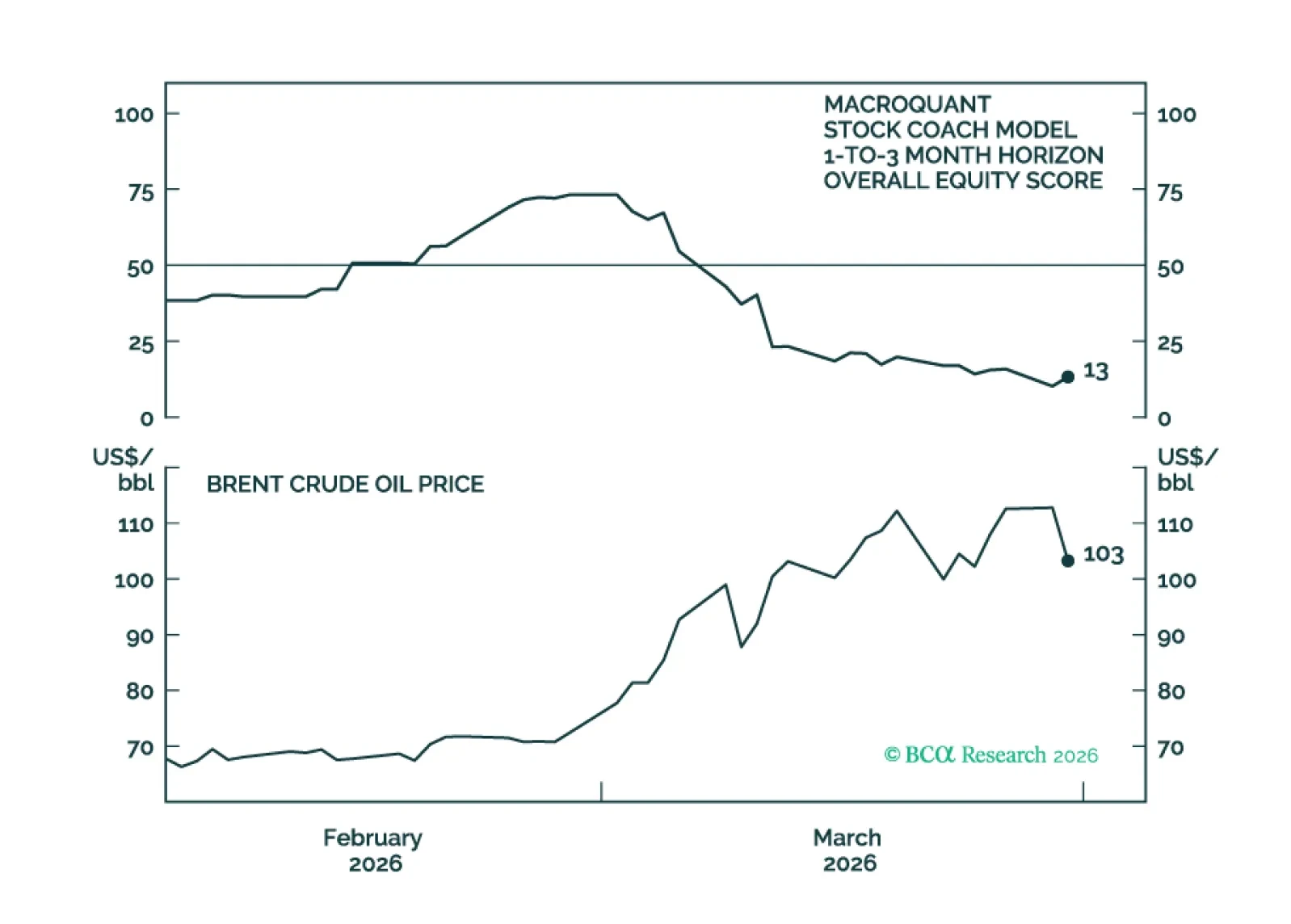

MacroQuant recommends a strong underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, has become neutral-to-slightly positive on the US dollar, has downgraded gold to neutral and copper to a strong underweight, and is bullish on oil.

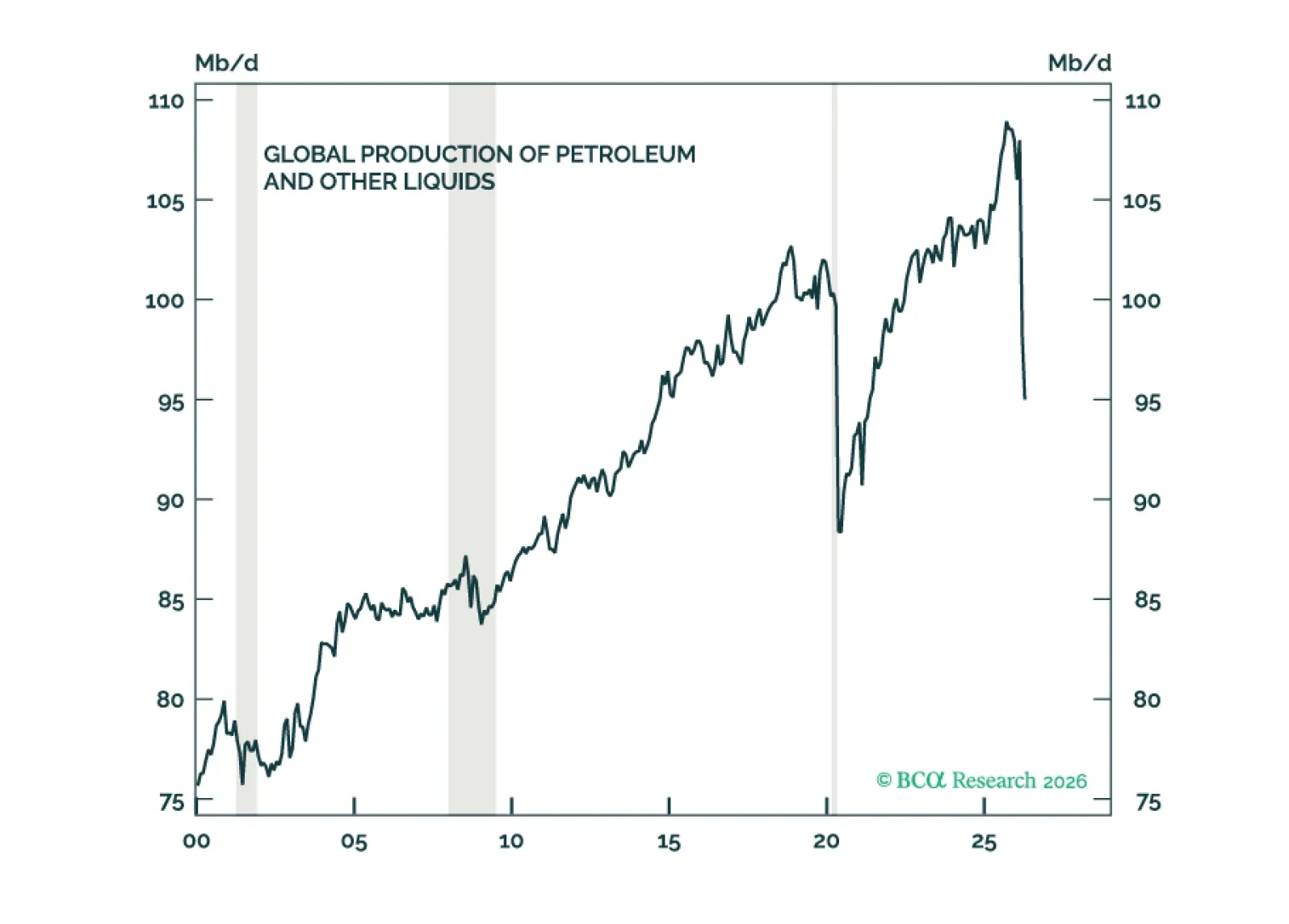

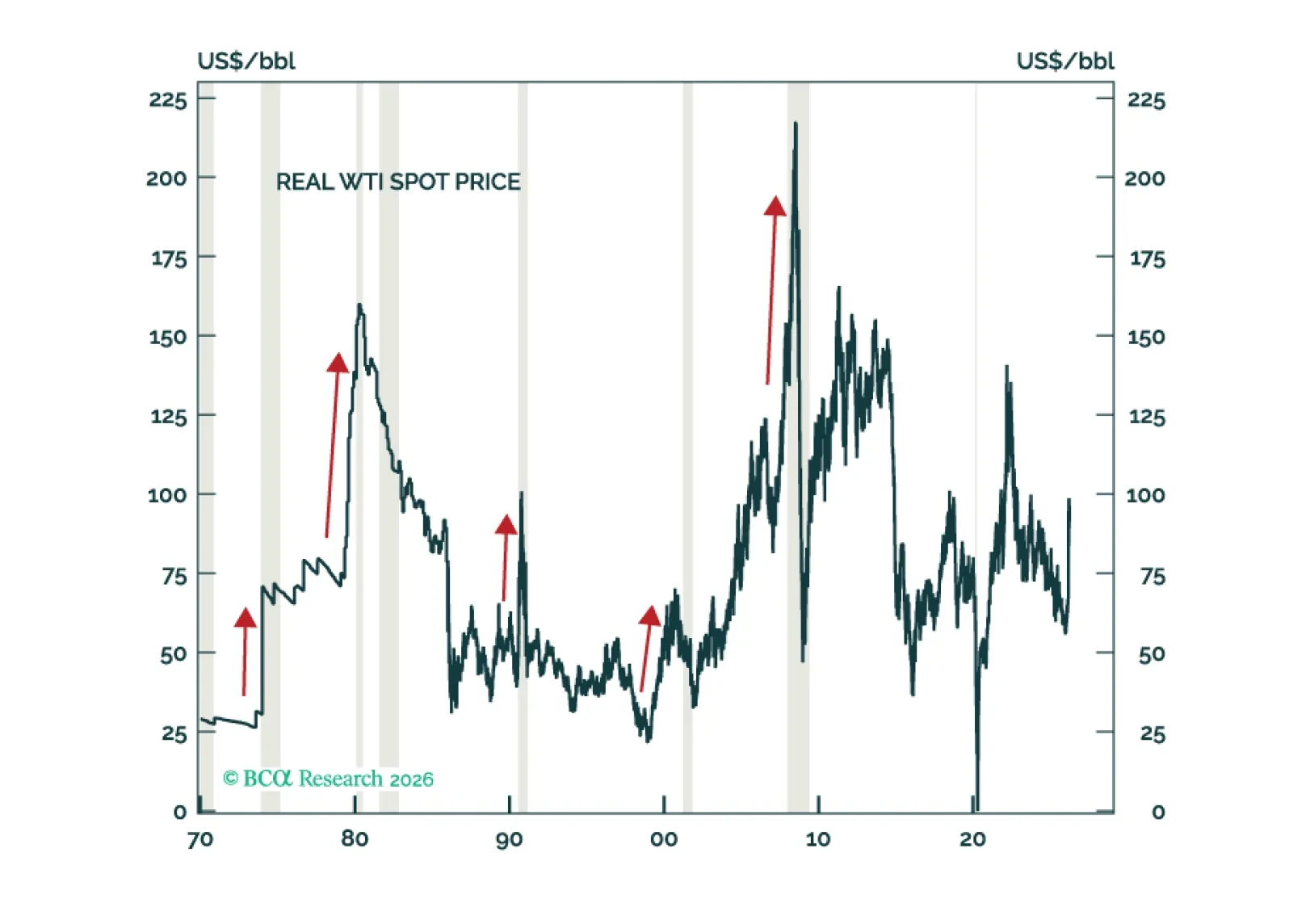

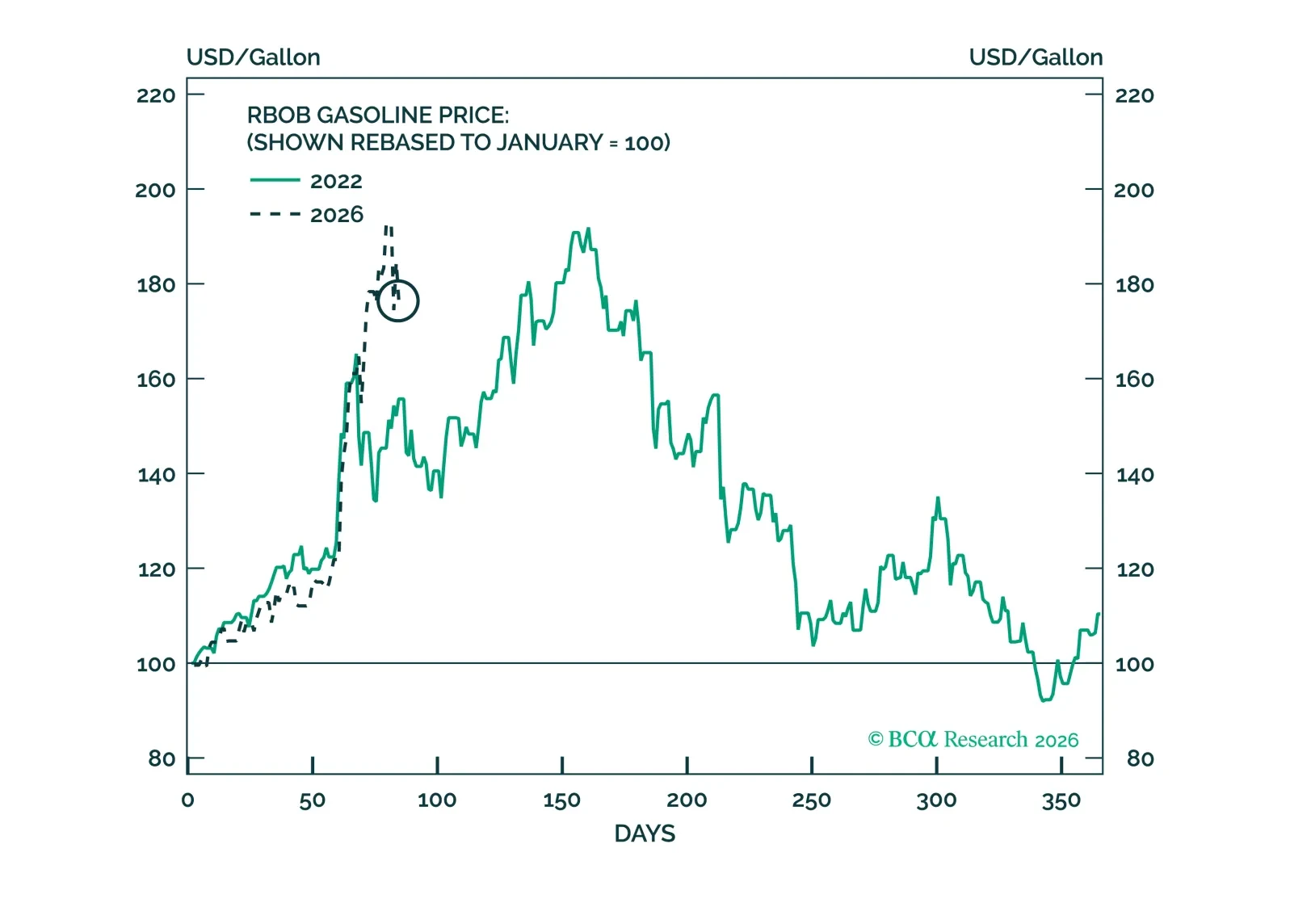

Over the past month, oil market participants have scrambled to fill the gap in global oil supply caused by the Strait of Hormuz’s closure. While these efforts have been impressive, the scale of the disruption means they are ultimately insufficient. Upside pressures will continue to dominate energy prices until transit through the Strait of Hormuz is restored.

One month into the Iranian conflict, we take stock of how markets have moved so far and how some of the big open questions might influence them going forward. A long opportunity may be developing at the long end of the Treasury curve.

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

In Section I, Doug argues that investors should maintain mildly defensive positioning while awaiting the restoration of normalized shipping flows through the Strait of Hormuz. In Section II, Jonathan examines the humanoid robot segment of the emerging physical AI landscape, concluding that humanoid robots are a potential but not yet imminent investment theme.

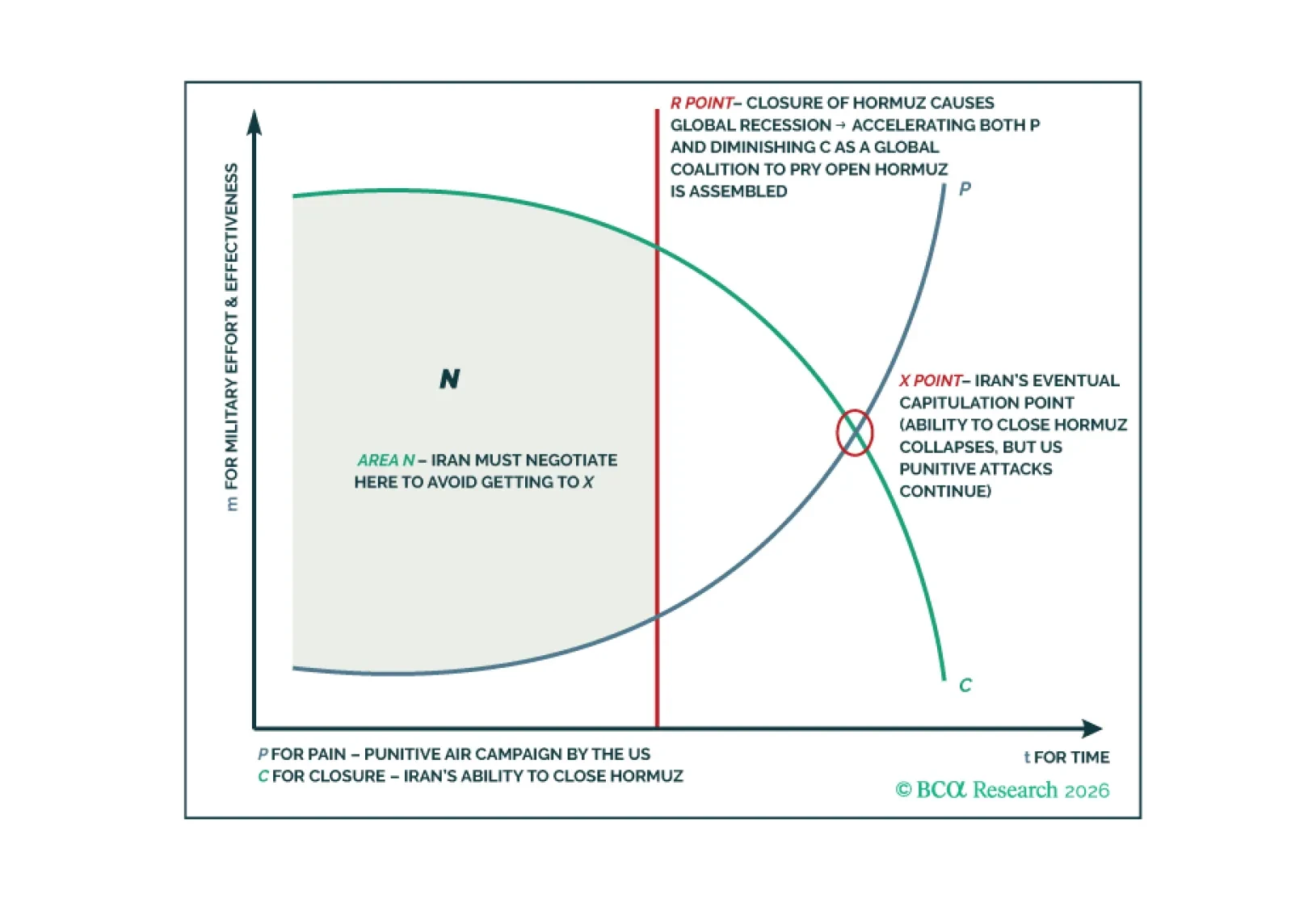

The Iran war may not deescalate in the near term, and if it does, it will likely reescalate later this year, suggesting investors should take a cyclically defensive outlook.

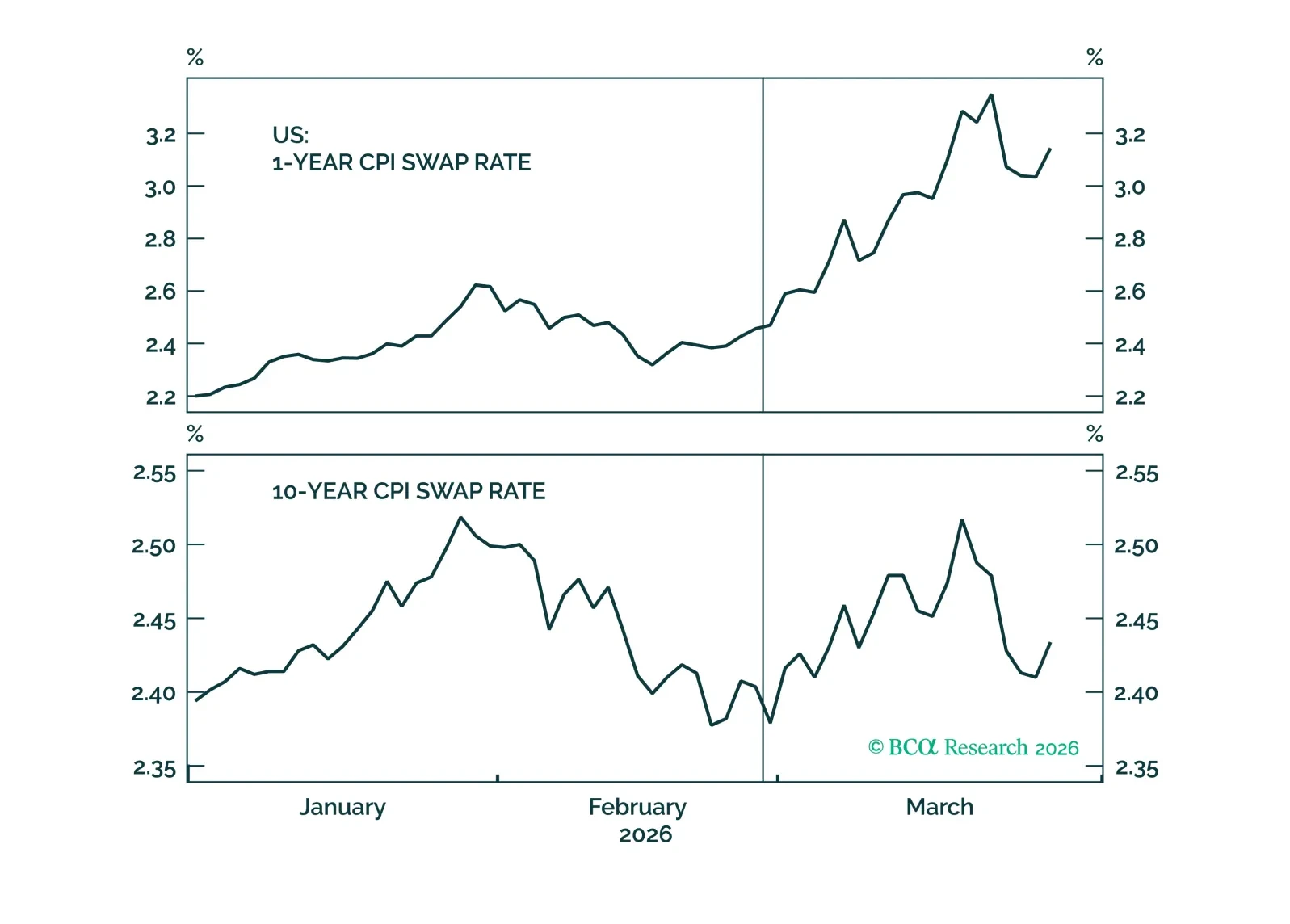

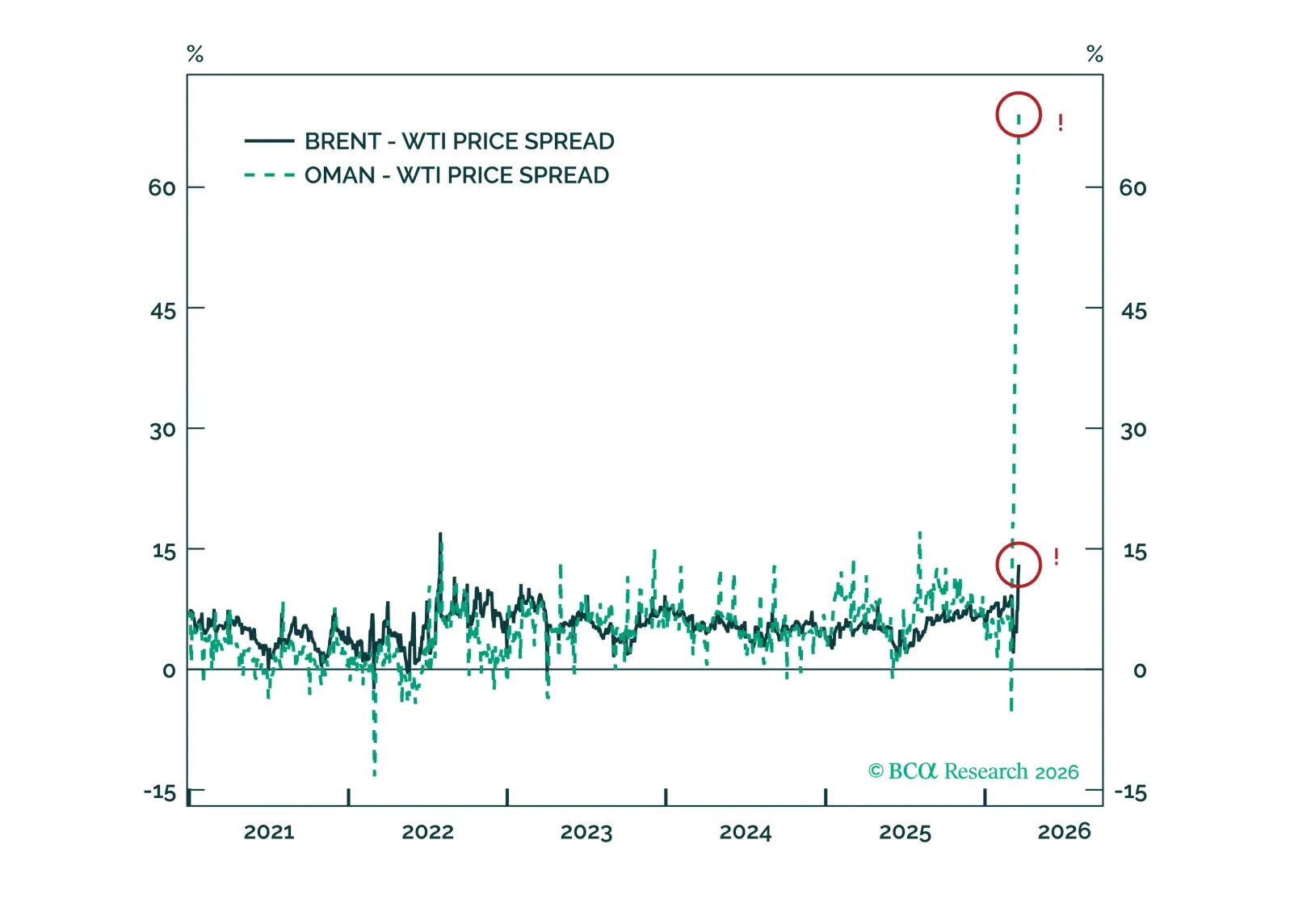

WTI is relatively calm amid the current conflict in the Middle East. Markets are too complacent on US crude relative to other international benchmarks.