Oil

In this Strategy Outlook, we present the major investment themes and views we see playing out for the rest of 2023 and beyond.

The attempted coup in Russia produced subdued short-covering rallies in oil, gas, and grains markets, as markets over time have observed that coups, rarely result in loss of production and exports. Markets await Putin’s next move. Unless and until a viable threat to the Putin government emerges, markets will continue pricing in fundamentals prevailing prior to Saturday’s attempted coup. We are keeping our base case brent and henry hub natgas price expectations unchanged.

We are strategically bullish on the outlook of the energy sector. Domestic and external political constraints asserted themselves, restraining the most negative impulse against this sector by the Biden administration. Go long energy versus cyclicals (ex-tech).

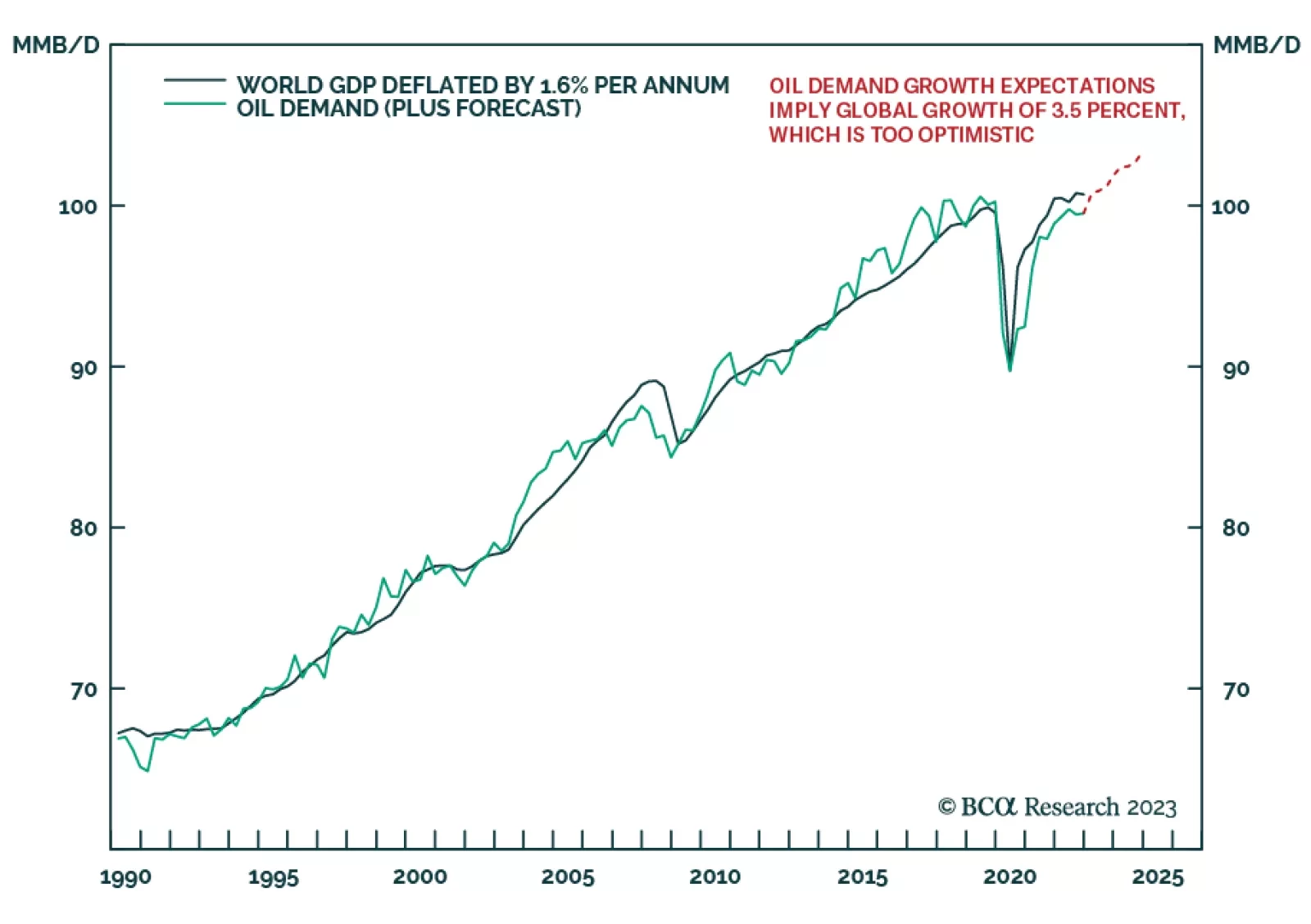

The normalization of oil storage markets in the Northern Hemisphere; strong demand, aided by China stimulus this year; and continued production discipline supports our view Brent prices likely have bottomed, and will move higher from here. We raised our 2023 Brent forecast $2/bbl to $92/bbl. Our forecast for next year is revised upward by $5/bbl to $120/bbl. Price risk remains to the upside, particularly if KSA exercises its option to extend production cuts of 1mm b/d.

Oil and metals reacted positively to the PBOC's 10 bp cut in the seven-day reverse repo rate, which will be part of the larger monetary and fiscal support needed to revive the economy. While deposit rates at state-owned banks have been reduced, additional rate cuts are expected. On the fiscal side, tax breaks and credit support are planned for the domestic EV market, while authorities are reportedly mulling further assistance for the property market.

In response to the first-ever federal indictment of a former President, investors should focus on the state of the economy and not on Trump’s legal trouble. They should also use the current market rally to stock up on protection, as a recession is still likely, albeit delayed.

What’s going on? The market-weighted stock market is up. But the equally-weighted stock market is not up. Neither is credit. Neither are industrial metal prices. Neither is the oil price, despite two waves of OPEC output cuts. We explain the dichotomy. Plus: European basic resources stocks can rebound, but Netherlands is likely to reverse.