Oil

The odds of Russia cutting oil output will rise going into 4Q23, as Ukraine’s endgame increases pressure on it, and it actively seeks to undermine President Biden’s re-election. We reckon a 2mm b/d cut would push Brent above $140/bbl by December 2024. This would push inflation and inflation expectations higher and raise the odds of more Fed rate hikes. BCA Commodity & Energy Strategy will remain long the COMT and XOP ETFs. At tonight’s close, we will be getting long December 2024 $100/bbl Brent calls.

The US is not out of the woods when it comes to inflation, which means that it is too early to conclude that the Fed can stop raising rates. Any further increase in inflation risk would prompt us to turn more cautious on stocks.

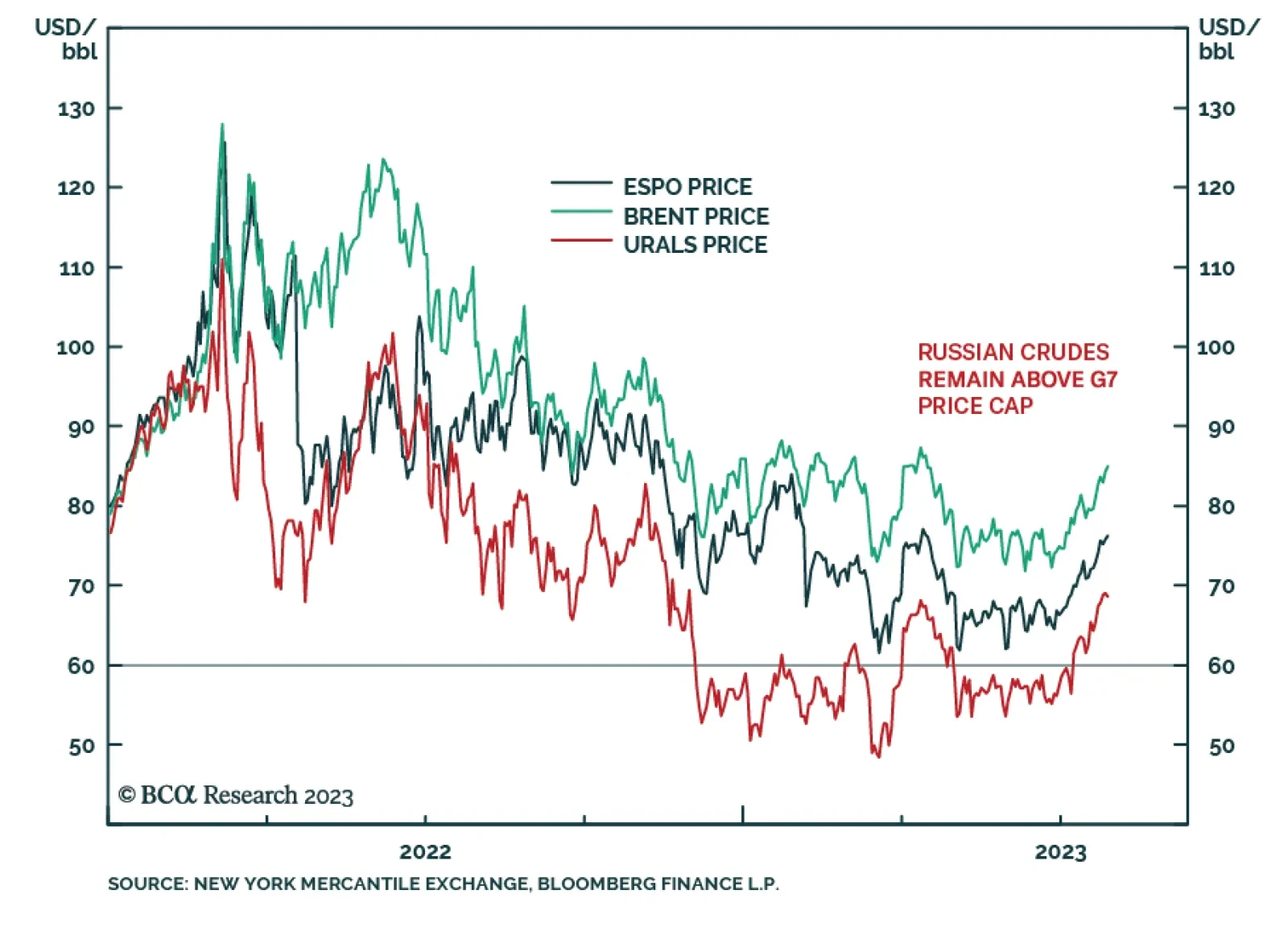

Global oil demand growth is tracking with our estimate of ~ 1.8mm b/d for this year. Supply discipline is being maintained by OPEC 2.0, where the core (KSA and the UAE) and Russia have reduced production by ~ 240k b/d yoy in 1H23. In addition, KSA extended its unilateral production cut of 1mm b/d from July into August. We expect inventory draws in 2H23 as supply stays below demand. Our Brent forecast remains unchanged at $92/bbl this year, and $120/bbl next year. We remain long the COMT and XOP ETFs.

Falling inflation enables central banks to pause rate hikes, which is good news. But time goes on. Restrictive monetary policy, Chinese debt-deflation, energy supply shocks, US and global policy uncertainty, and extreme geopolitical risks will undermine hopes of a soft landing and beautiful disinflation.

Positive economic surprises have delayed the onset of recession in the United States. But tighter monetary and fiscal policy, slowing global growth, and a looming rebound in policy uncertainty and geopolitical risk suggest that investors should buy insurance while it is cheap.

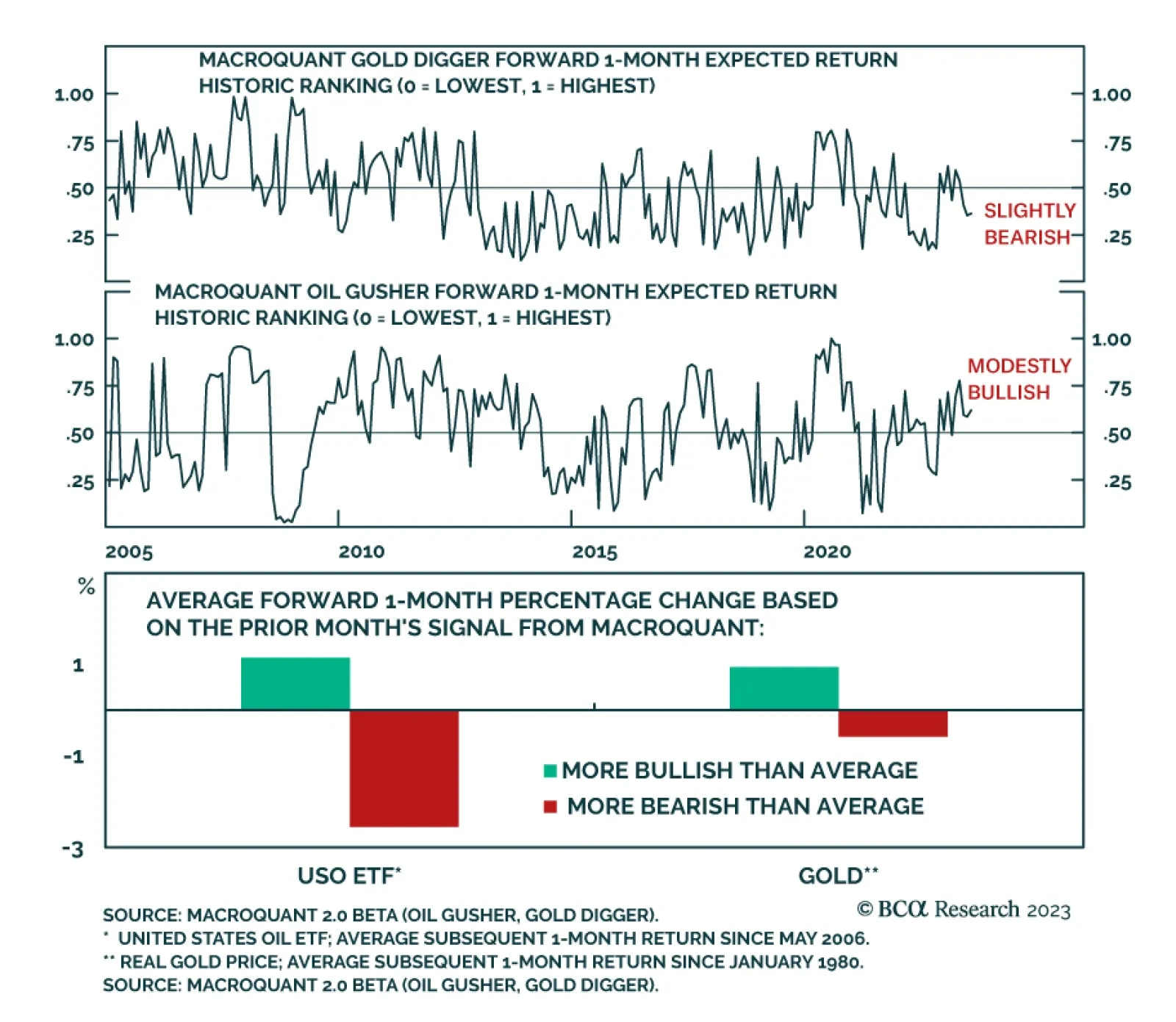

Markets continue to be tossed to and fro by central-bank policy, and risks of higher commodity prices. These are due to fiscal stimulus and exogenous weather and war-related risk, which could send food and energy prices higher this winter. We remain long gold outright, energy and metals producers via the XOP, XME and PICK ETFs, direct commodity exposure via the COMT ETF, and futures exposure to backwardation in copper (long 4Q23 copper futures vs. short 4Q24 copper futures).

We build a four-stage business cycle framework based on economic growth and capacity utilization, and then analyze historical returns for most major asset allocation decisions for each stage. Given that we are in the early recession stage (negative growth coupled and an overheated economy), our framework recommends a defensive positioning across all asset classes.