Oil

China’s oil demand growth will moderate to a still robust 4%-6% in the next six-to-nine months. We recommend that investors in China’s onshore and offshore stock indexes overweight energy producers.

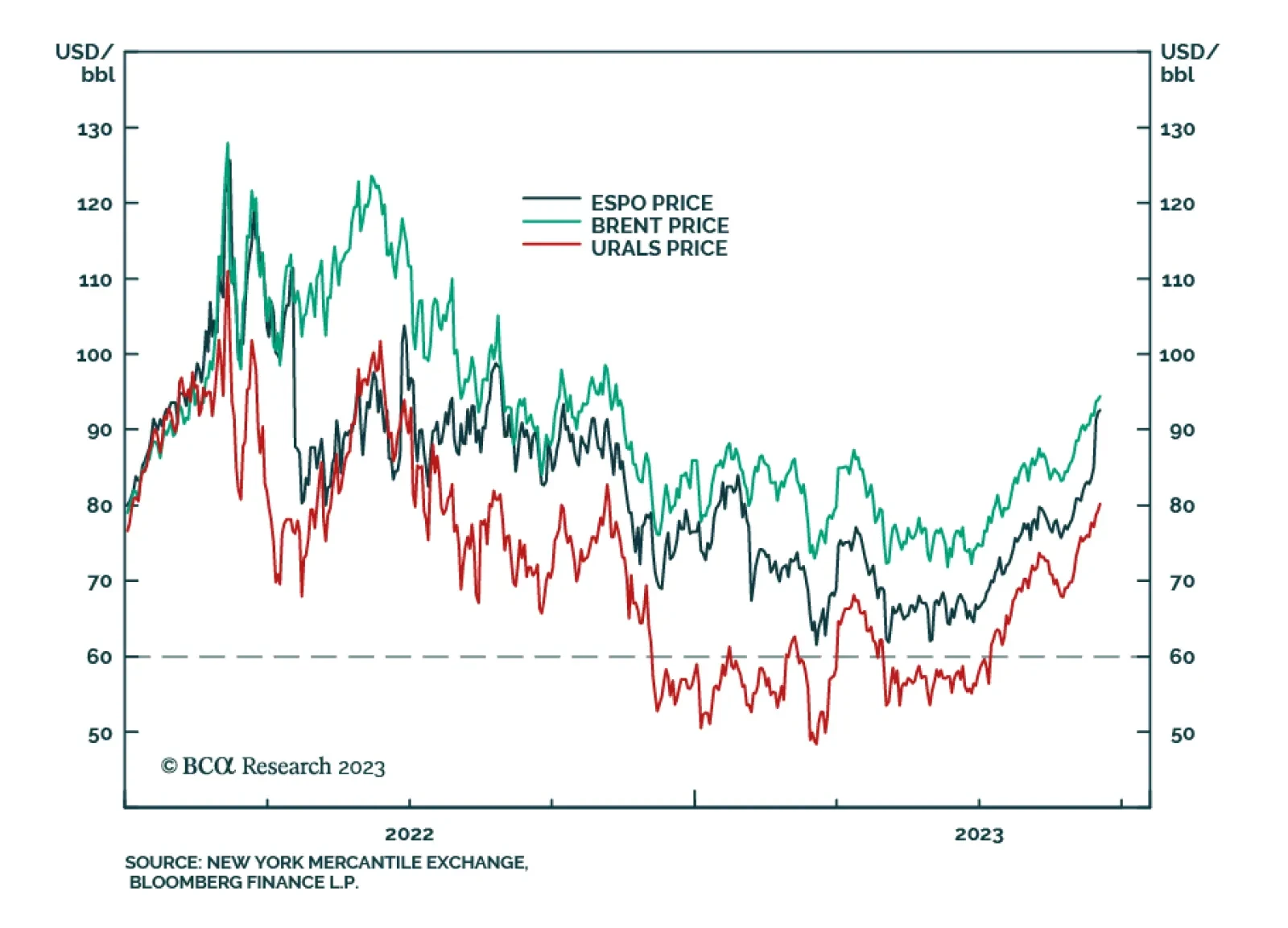

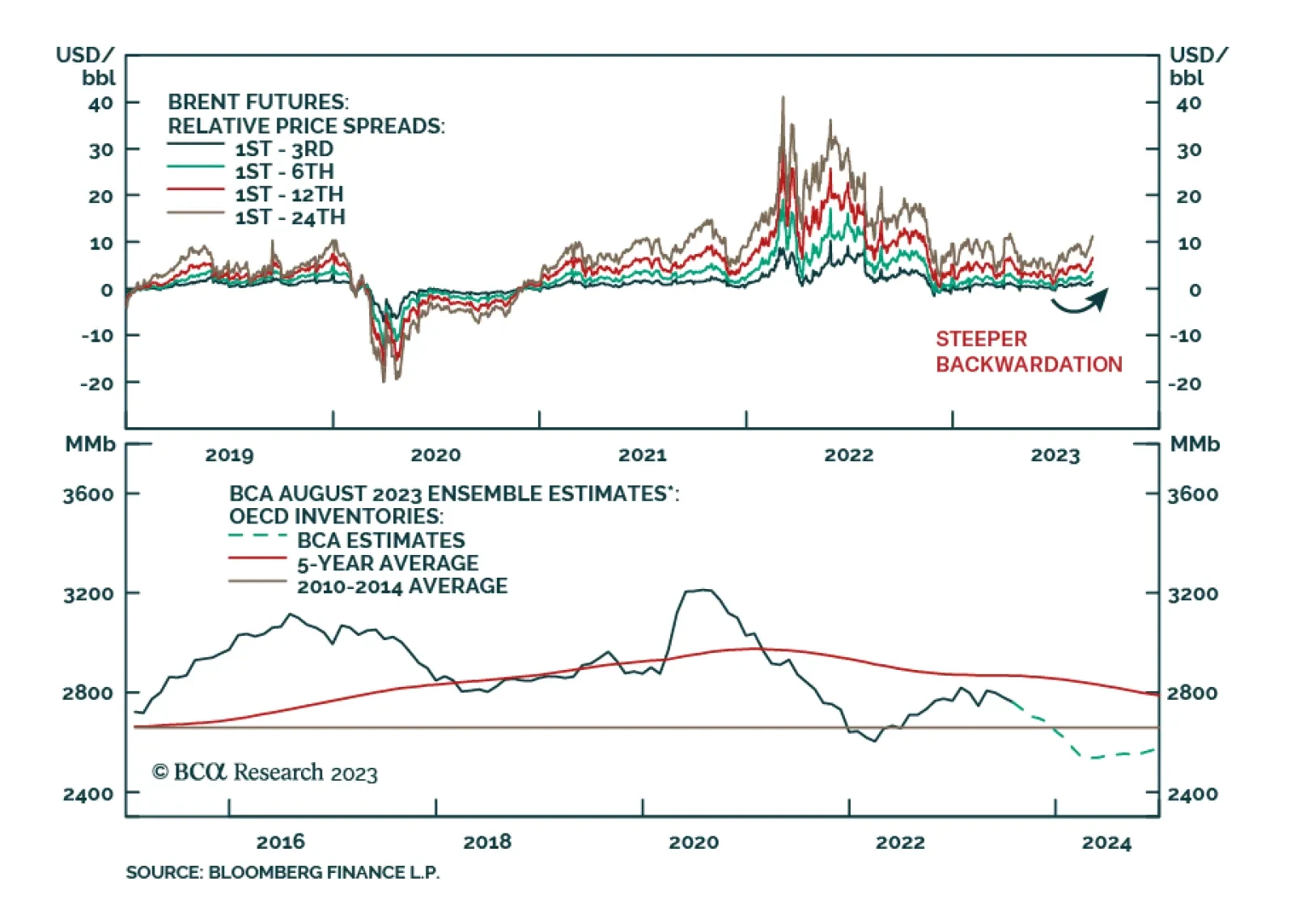

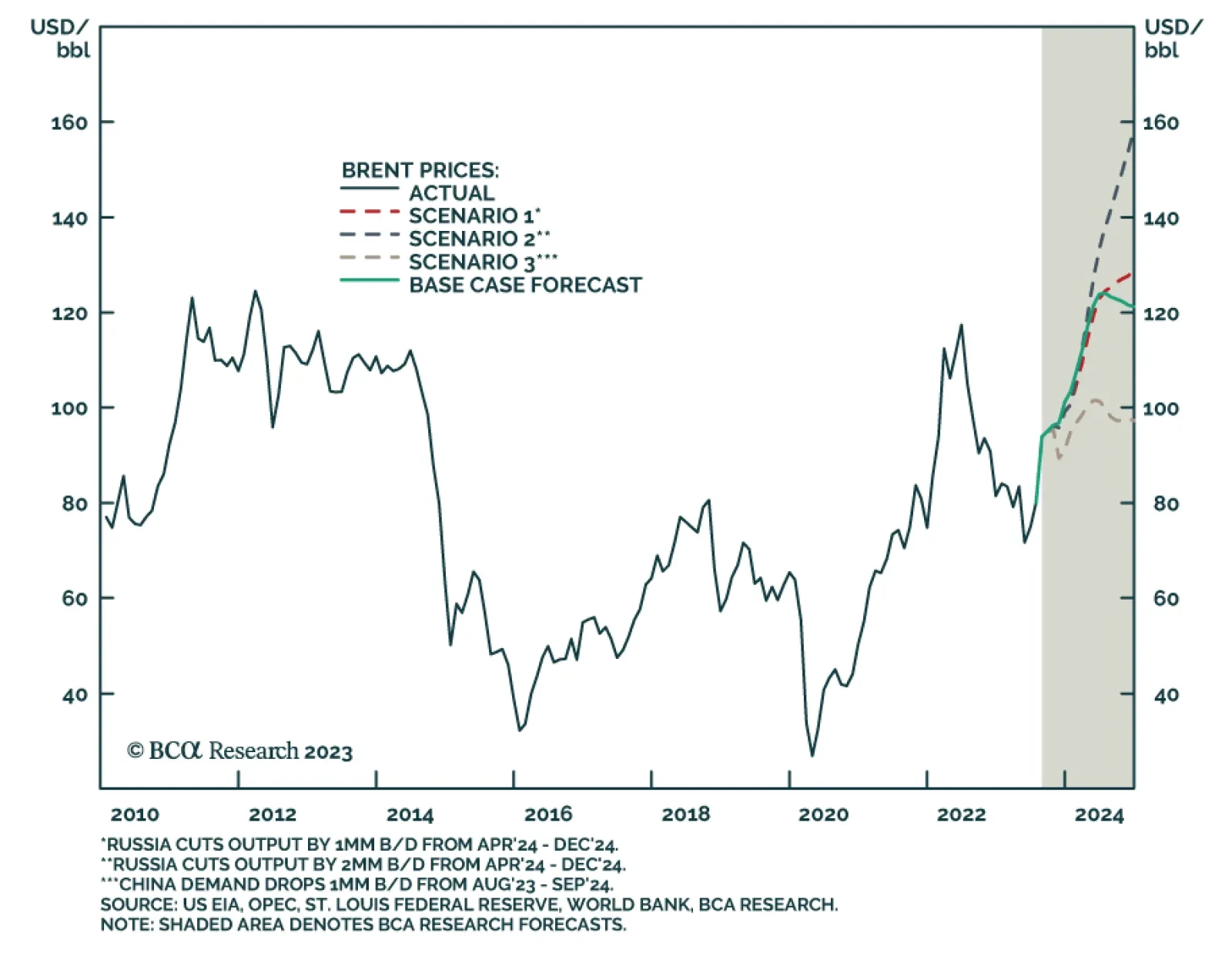

We continue to expect Brent crude to trade just above $101/bbl in 4Q23, and to average $118/bbl in 2024. Higher volatility looms. We expect Russia will cut oil production next year as part of a concerted effort to undermine Biden’s re-election. Oil-demand volatility is set to rise in response to divergent policy imperatives. We continue to favor equity exposure to oil and gas via the XOP ETF; direct exposure via the COMT ETF, and long Dec23 $100/bbl Brent calls. We are getting long Jan-Feb-Mar 2024 Brent futures vs. short the same months in 2025 expecting steeper backwardation as inventories draw and markets tighten.

China’s reopening faltered and now it is applying moderate stimulus. OPEC 2.0’s production discipline is getting results, with oil prices climbing. The Fed will not be able to deliver dovish surprises in Q4 2023. Investors should expect stock market and commodity volatility and prefer defensive positioning.

The geopolitical backdrop remains negative despite some marginally less negative news. China’s stimulus is not yet large or fast enough to prevent a market riot. Two of our preferred equity regions, ASEAN and Europe, are struggling to outperform. Investors should stay defensive overall.

We continue to expect China to deploy stronger fiscal and monetary stimulus to avoid prolonged deflation brought about by a liquidity trap and sub-zero growth. All the same, a lower-growth risk has been added to our ensemble forecast. We expect Brent to trade at $94/bbl in 2H23, and $120/bbl next year. WTI will trade $4 – $6/bbl lower.

The global economy will not enjoy an “immaculate disinflation” but will suffer a very maculate one due to China’s growth slowdown and restrictive monetary policy in the developed world. Investors should stay overweight low-beta assets.