Oil

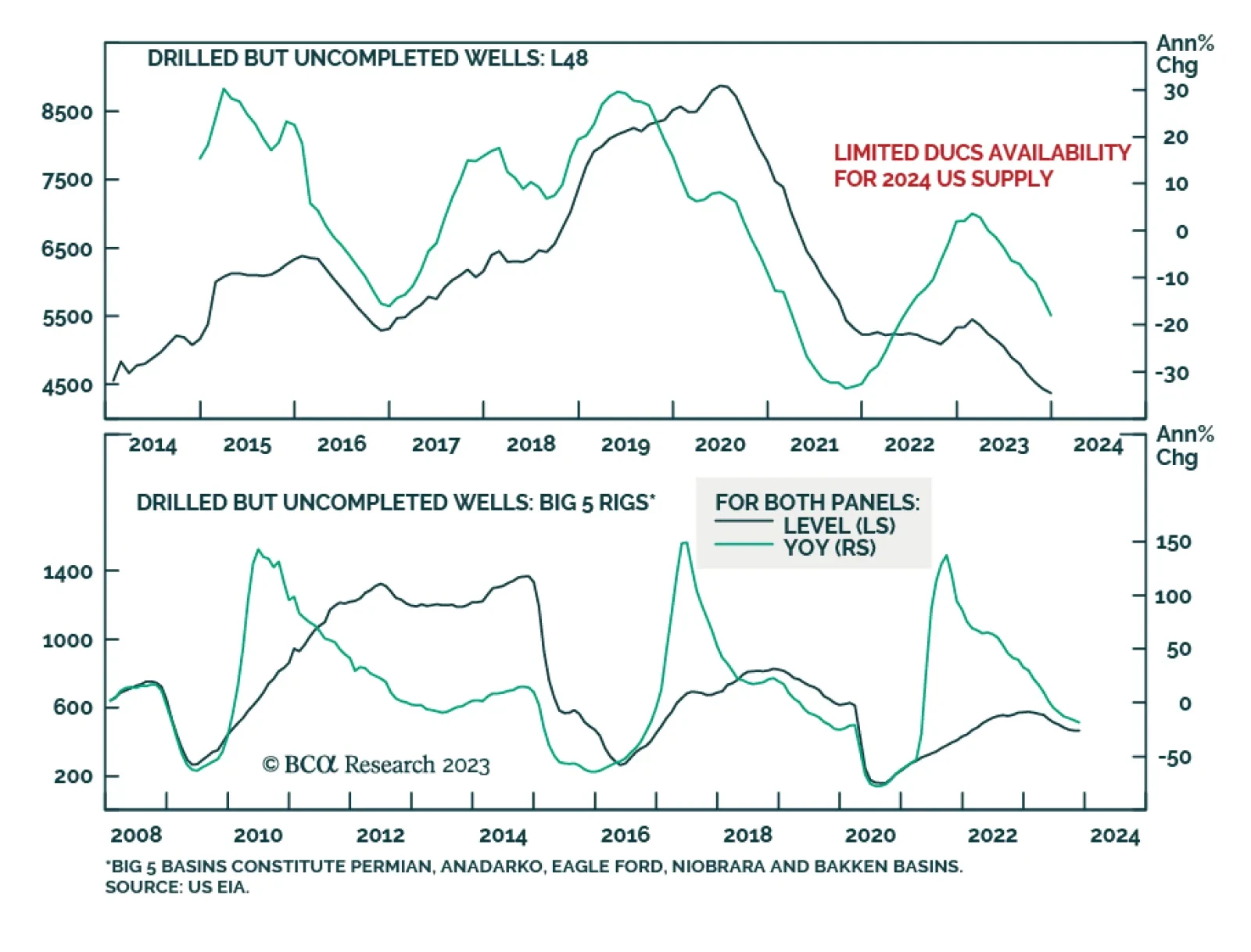

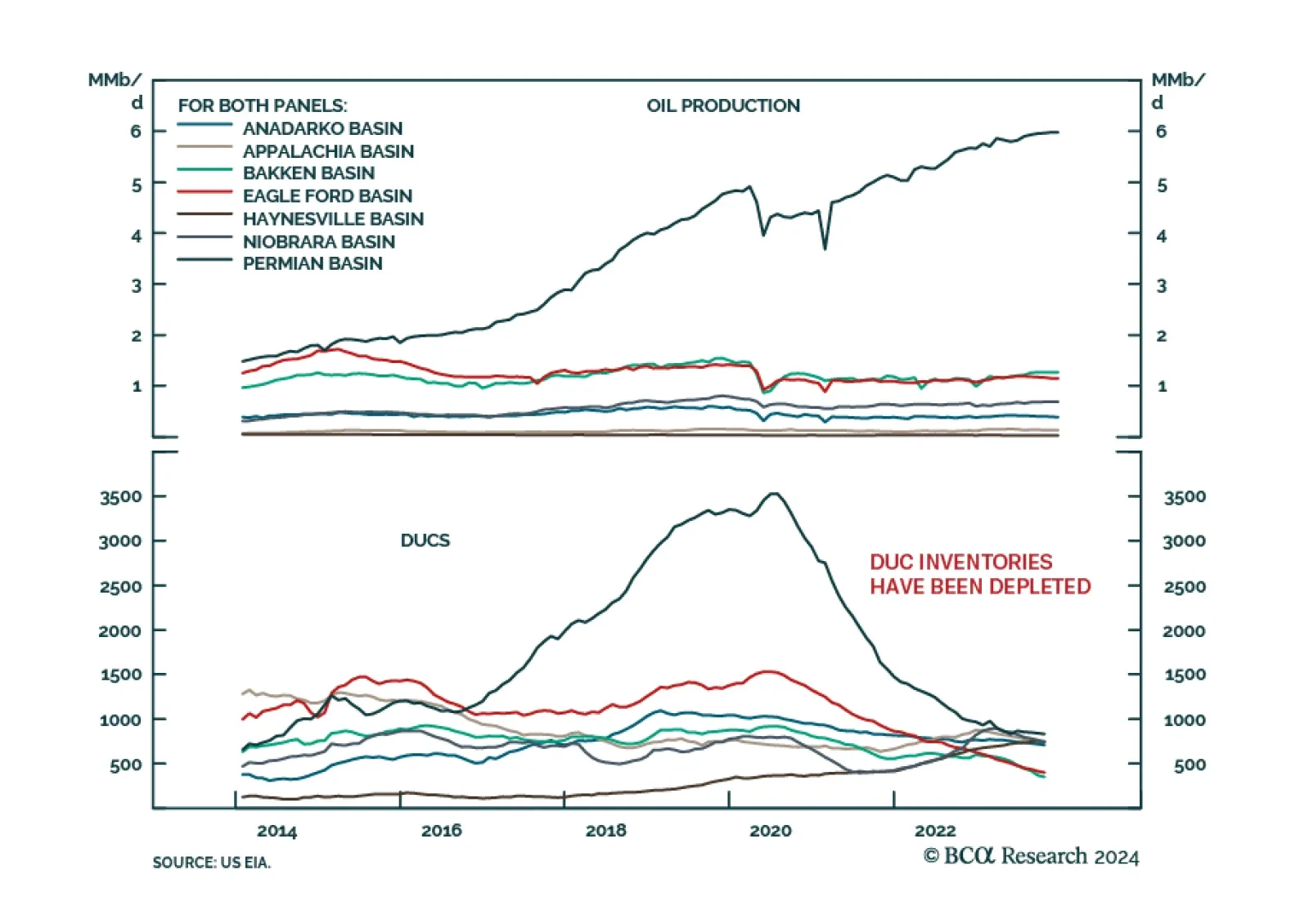

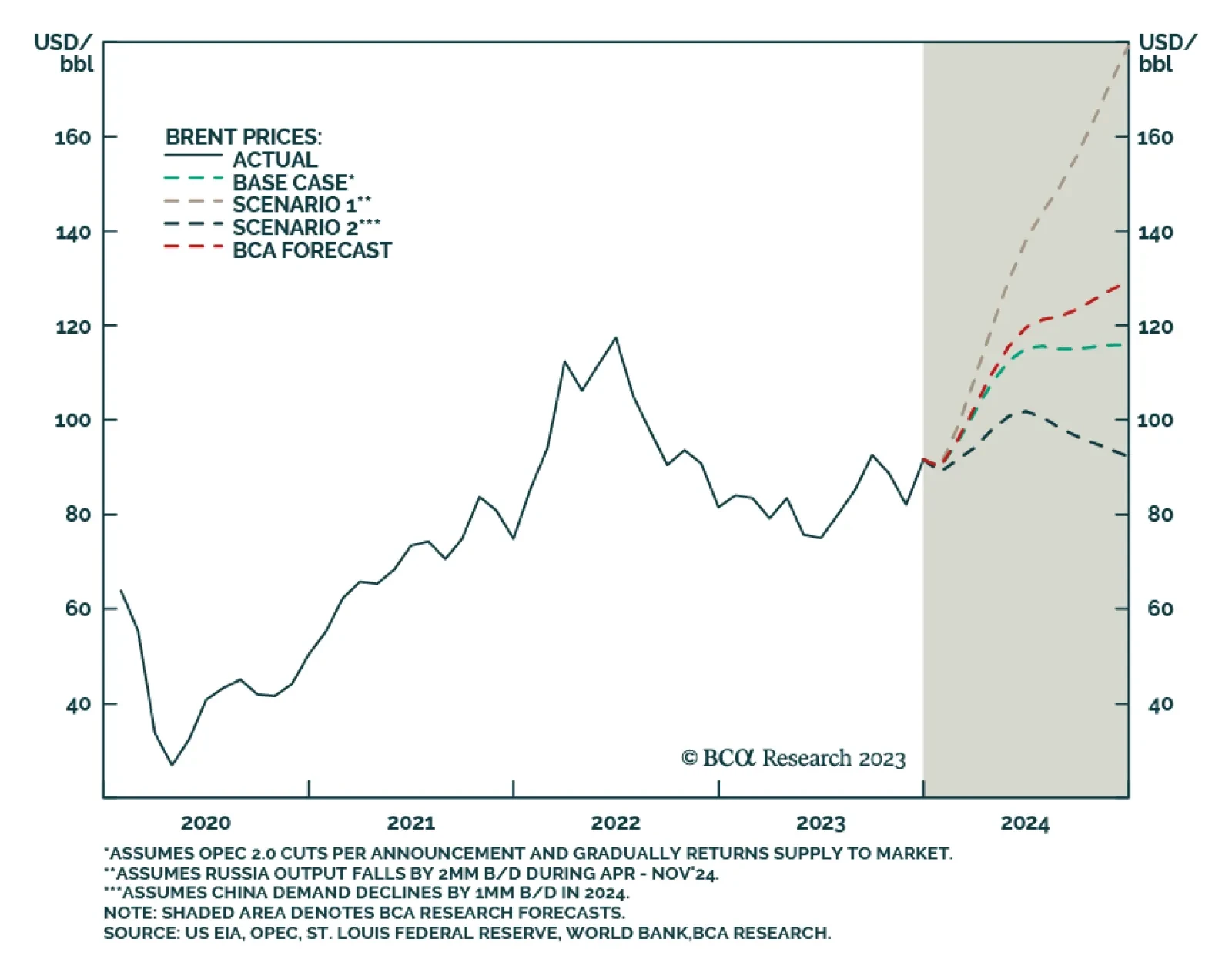

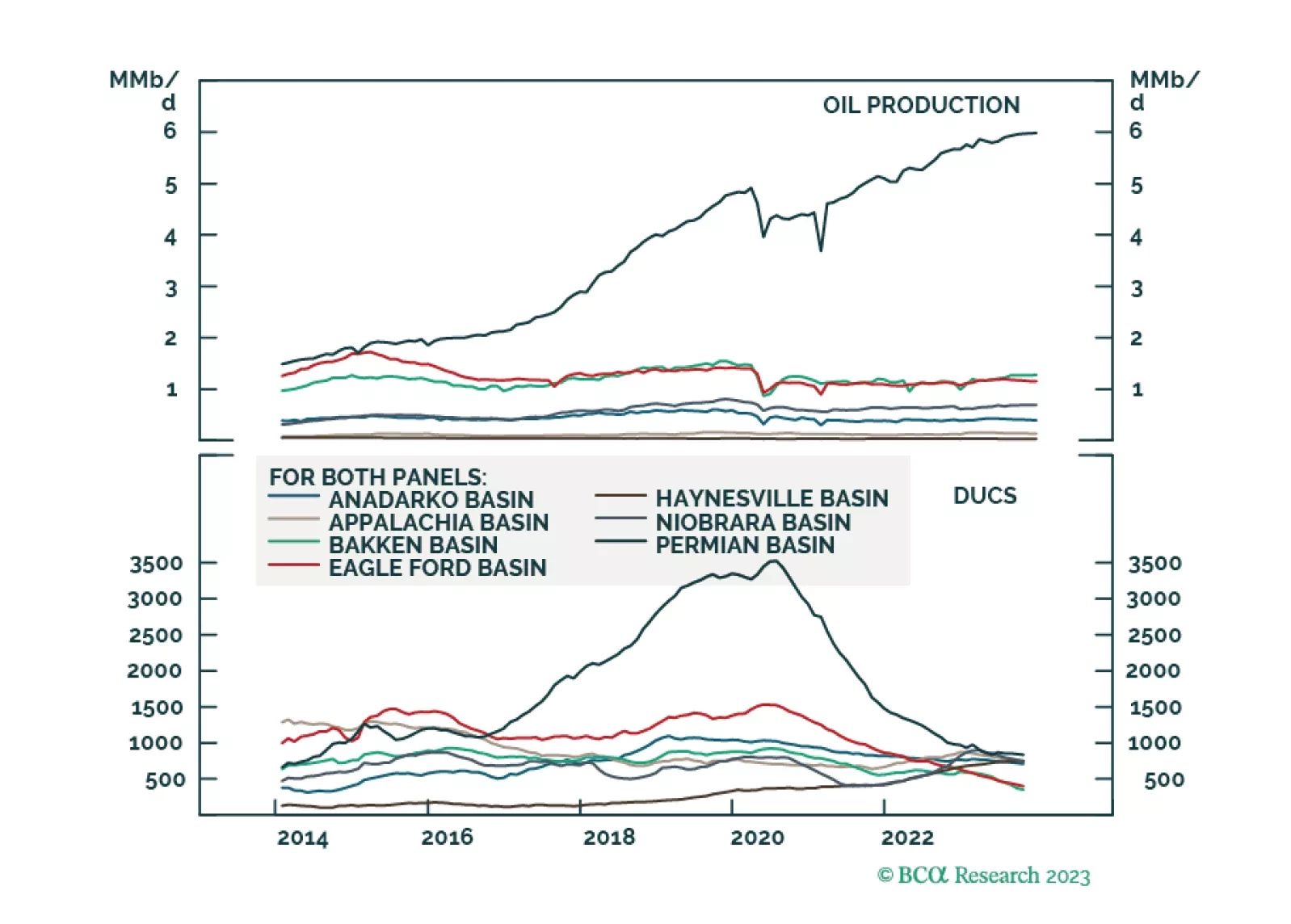

The risk markets will be surprised by another 1mm b/d increase in crude oil supplies this year or next from the US is low, given the depletion of the unfinished-well inventory that drove shale output higher. Demand remains strong, although growth will slow. Higher non-OPEC 2.0 production, slowing demand growth, lower upside risk and the carryforward of elevated 2023 inventories take our 2024-25 Brent forecasts to $95/bbl and $105/bbl, respectively.

In this brief Insight we examine the expanding Middle East conflict and update the situation in the Taiwan Strait on the eve of elections. The Houthis are a distraction and China is not likely to invade Taiwan in the near term, but both situations support our overweight of US equities relative to global. Global growth is likely to slow while commodities are likely to see at least minor supply shocks.

The market’s pricing of a soft landing means that geopolitical risks are becoming more, not less, relevant in 2024. US domestic divisions will invite challenges as foreign powers rightly fear that US policy will turn more hawkish after the election.

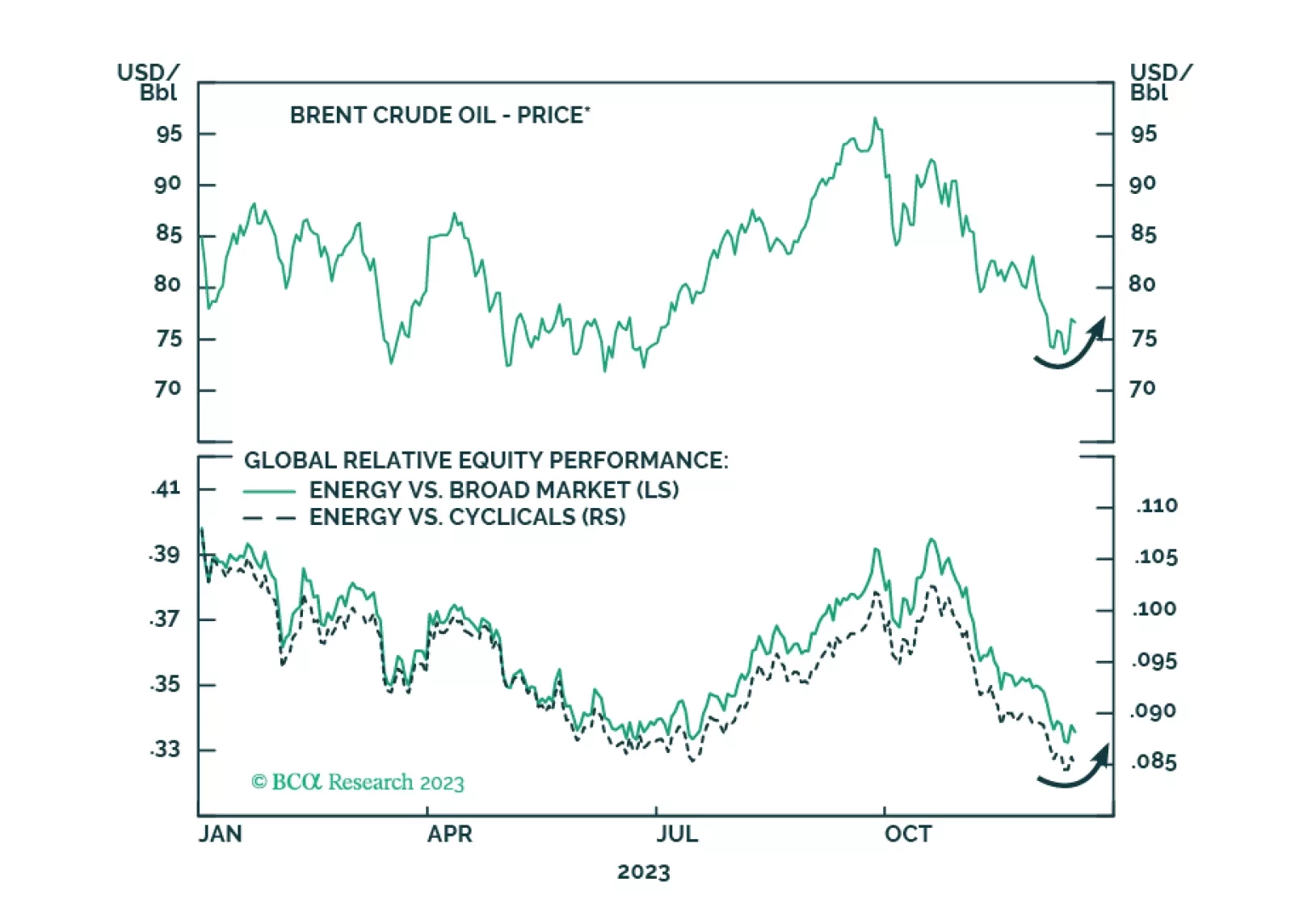

Oil prices will rise tactically due to supply risks. Recent developments indicate escalation of the conflict with Iran in the Middle East and confirm our expectation of energy supply disruptions and oil price spikes in the short run.

Political economy dominates fundamentals going into 2024, as states prepare for war and de-risk supply chains. Asynchronous global growth will elevate commodity-price volatility. We expect oil to trade above $100/bbl in 2024 and continue to favor equity exposure to oil-and-gas producers. Given weak capex, we also favor metals miners and refiners. We remain long the Gold, the XME and COMT ETFs We were stopped out of our XOP ETF with a 12.5% gain; we will re-establish it at tonight’s close.

Global Investment Strategy predicted the surge of inflation in 2021/22 and the immaculate disinflation of 2023. Now their unique framework is predicting a recession in the second half of 2024.