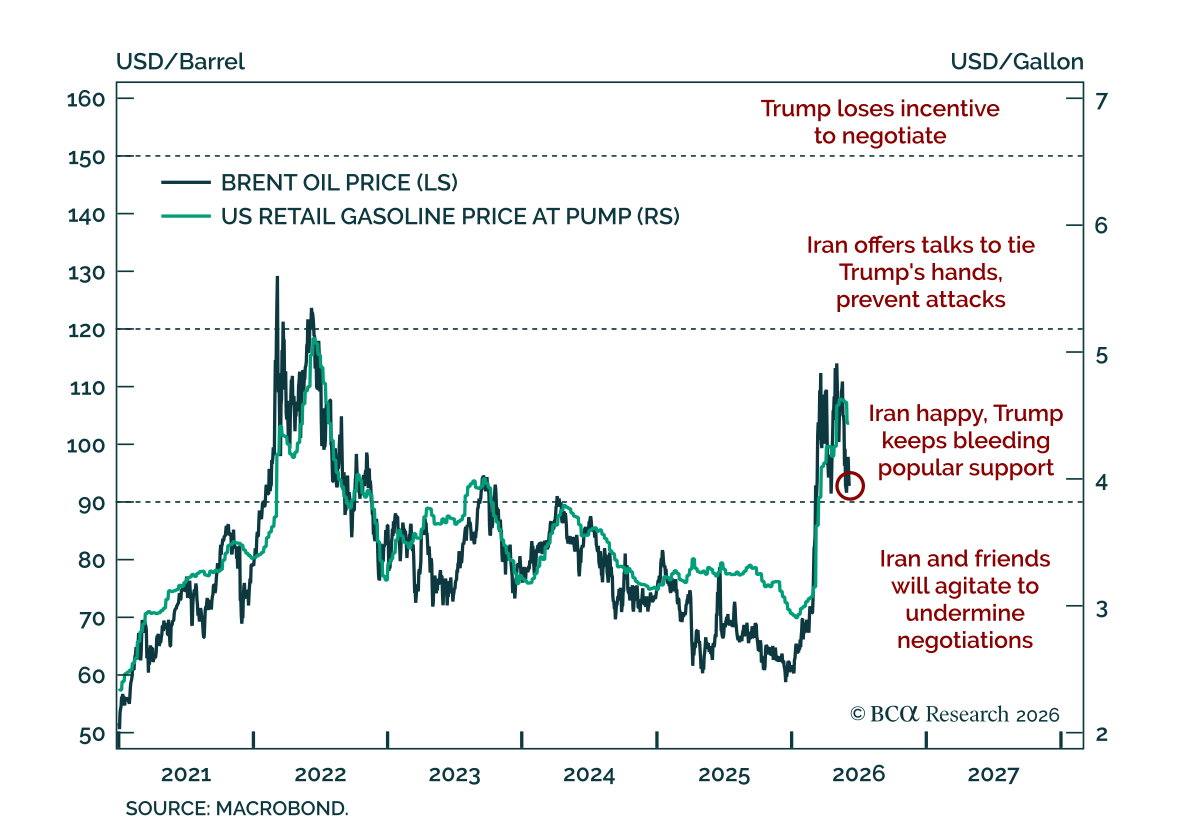

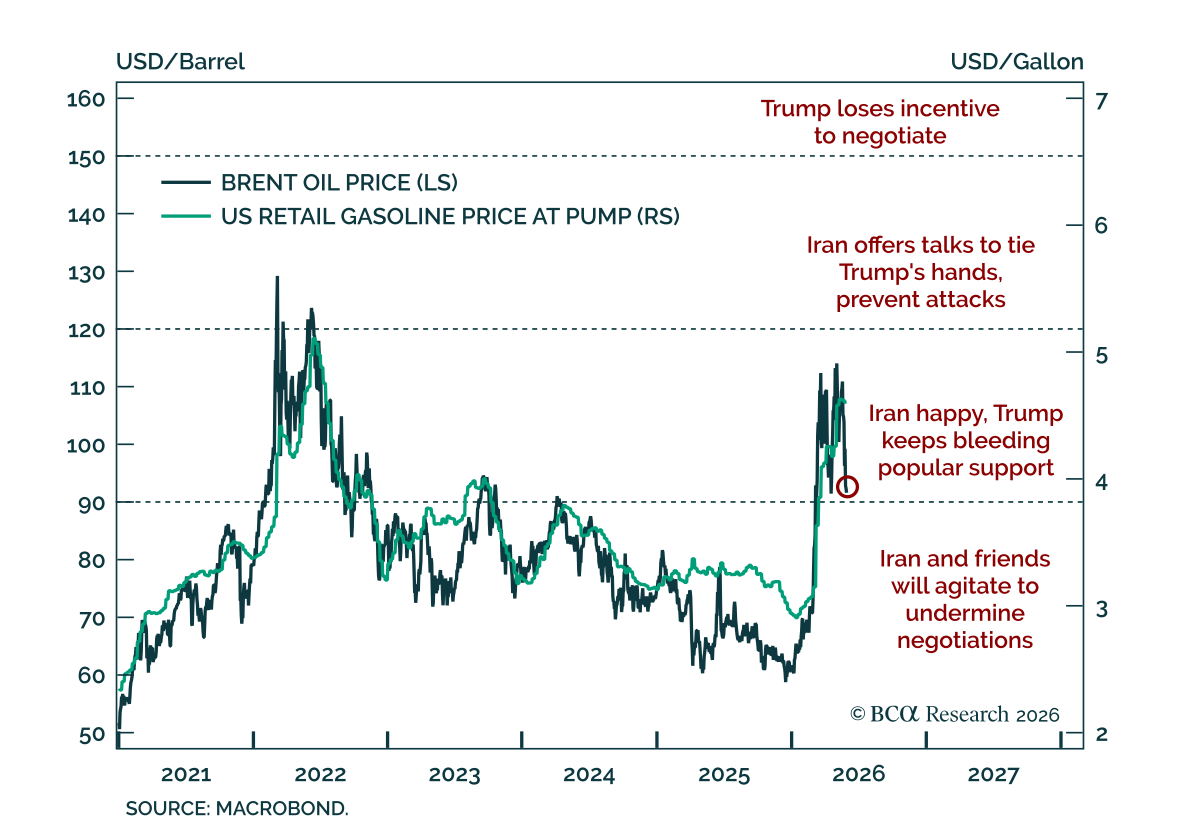

Oil

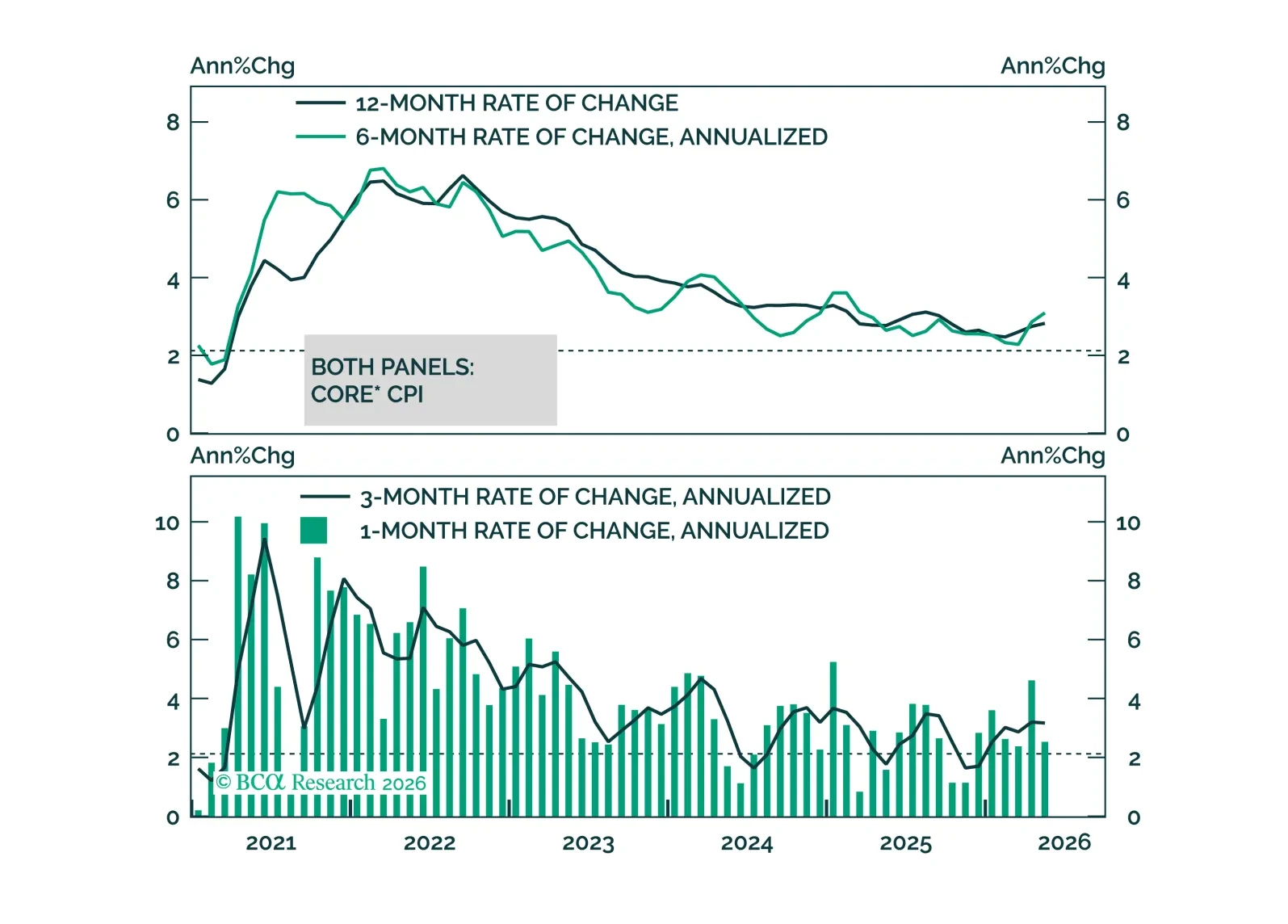

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

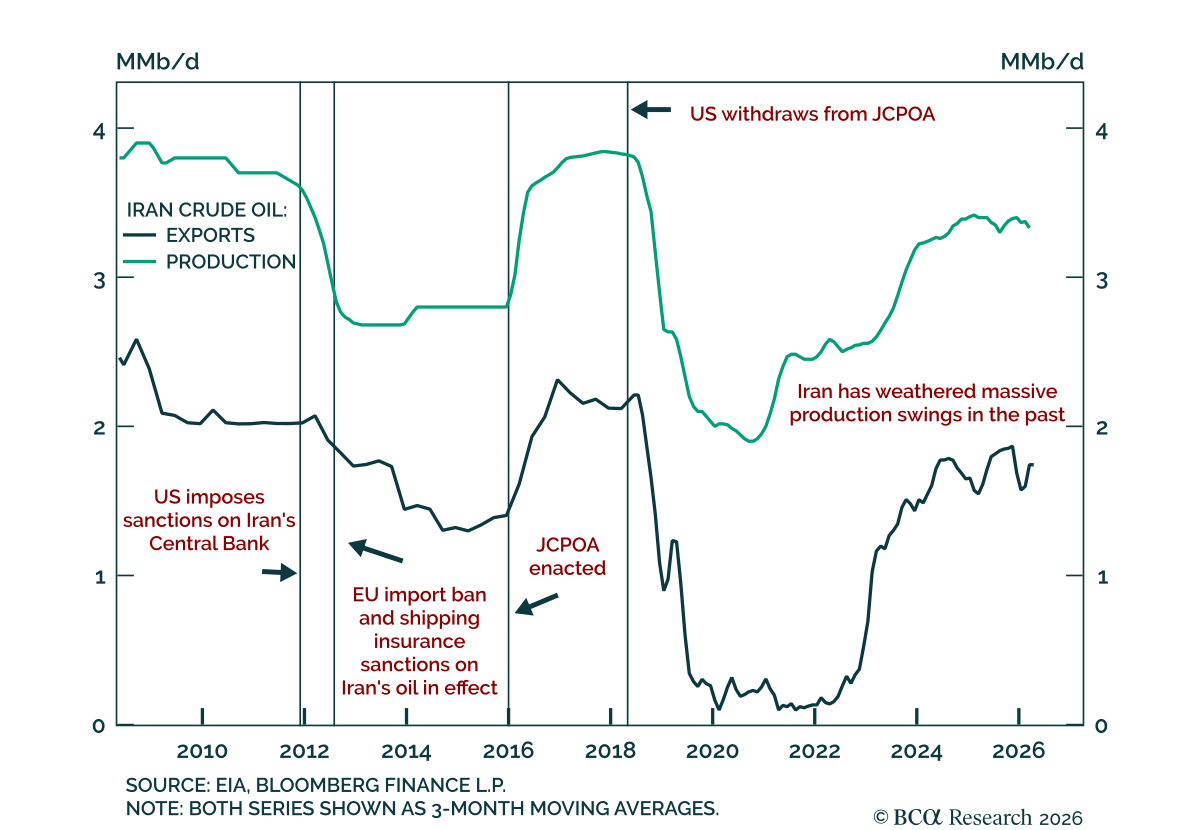

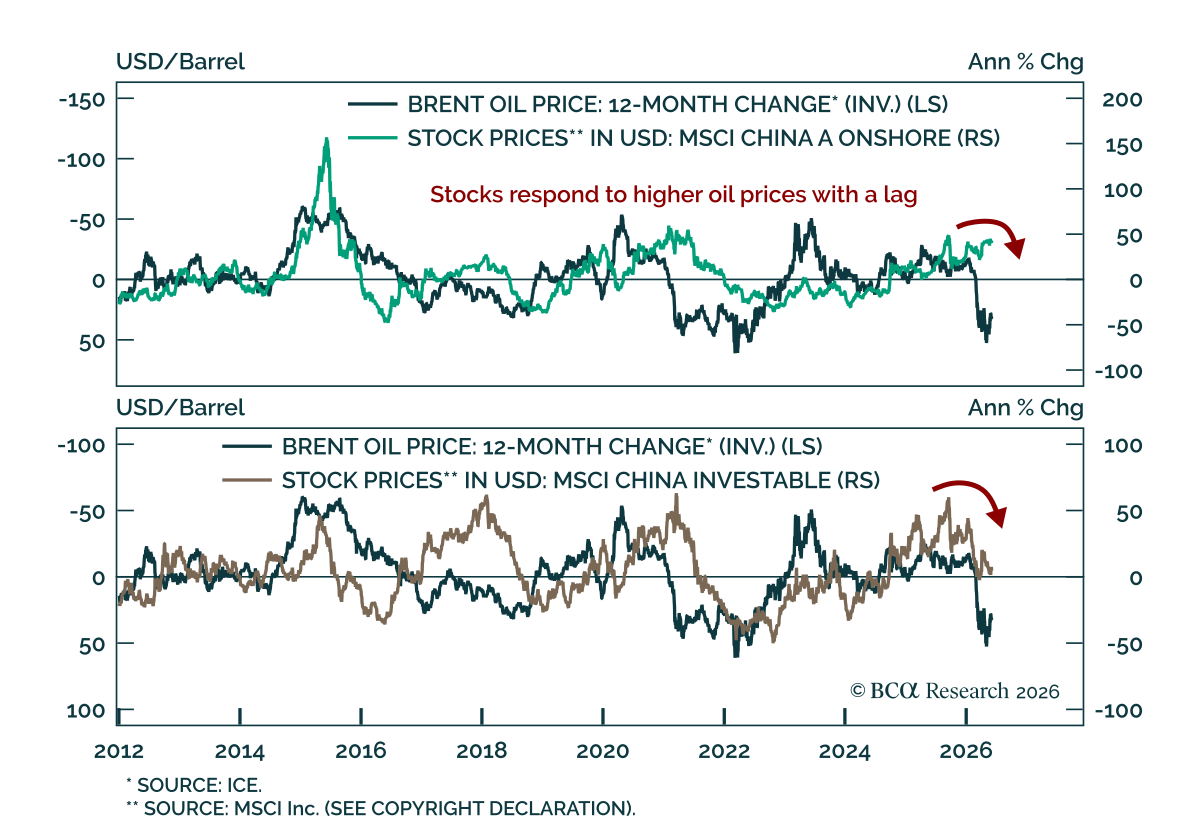

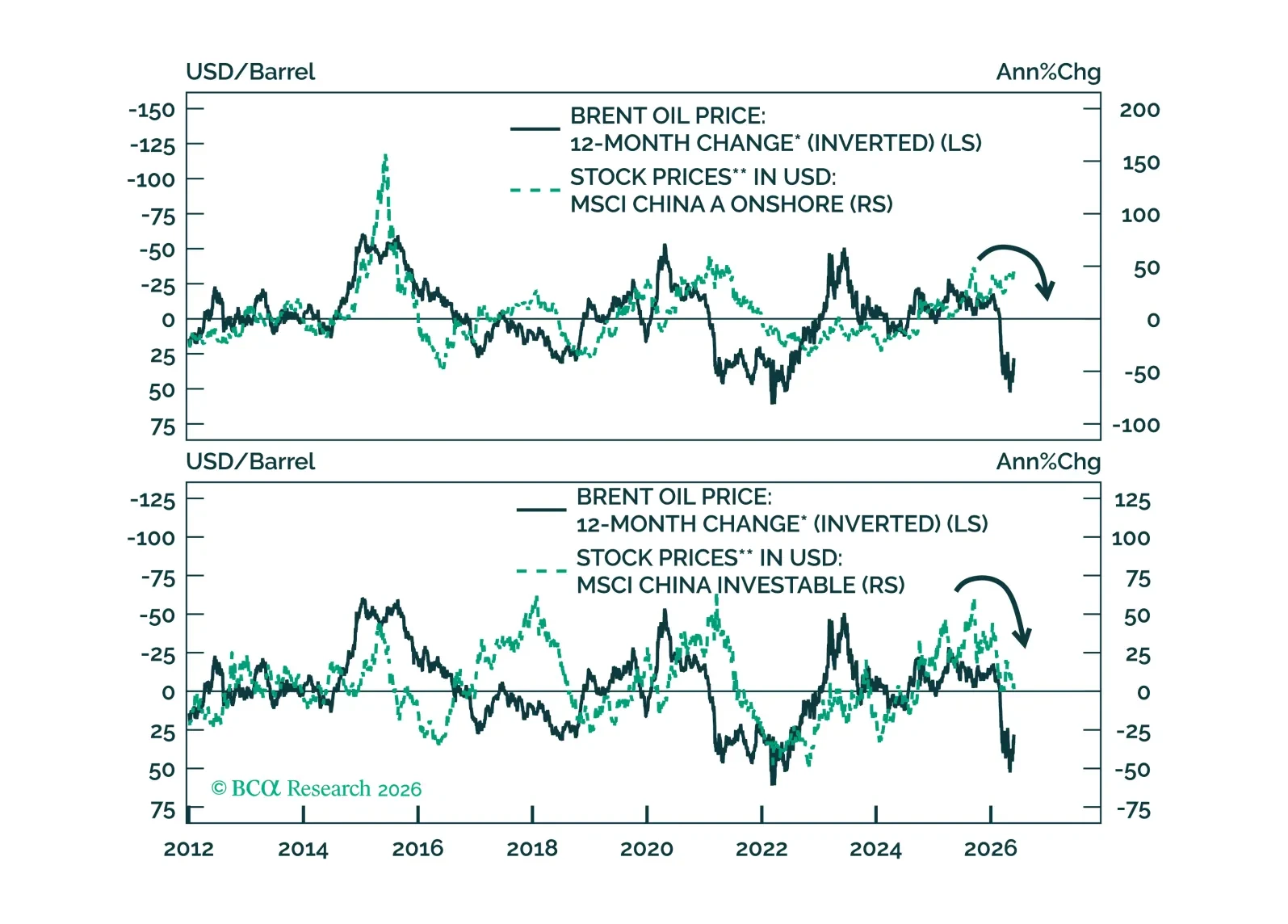

Oil shocks hit economies with a lag. China will feel the delayed pain of surging oil prices, pushing Beijing toward infrastructure spending as its main tool to prop up growth.

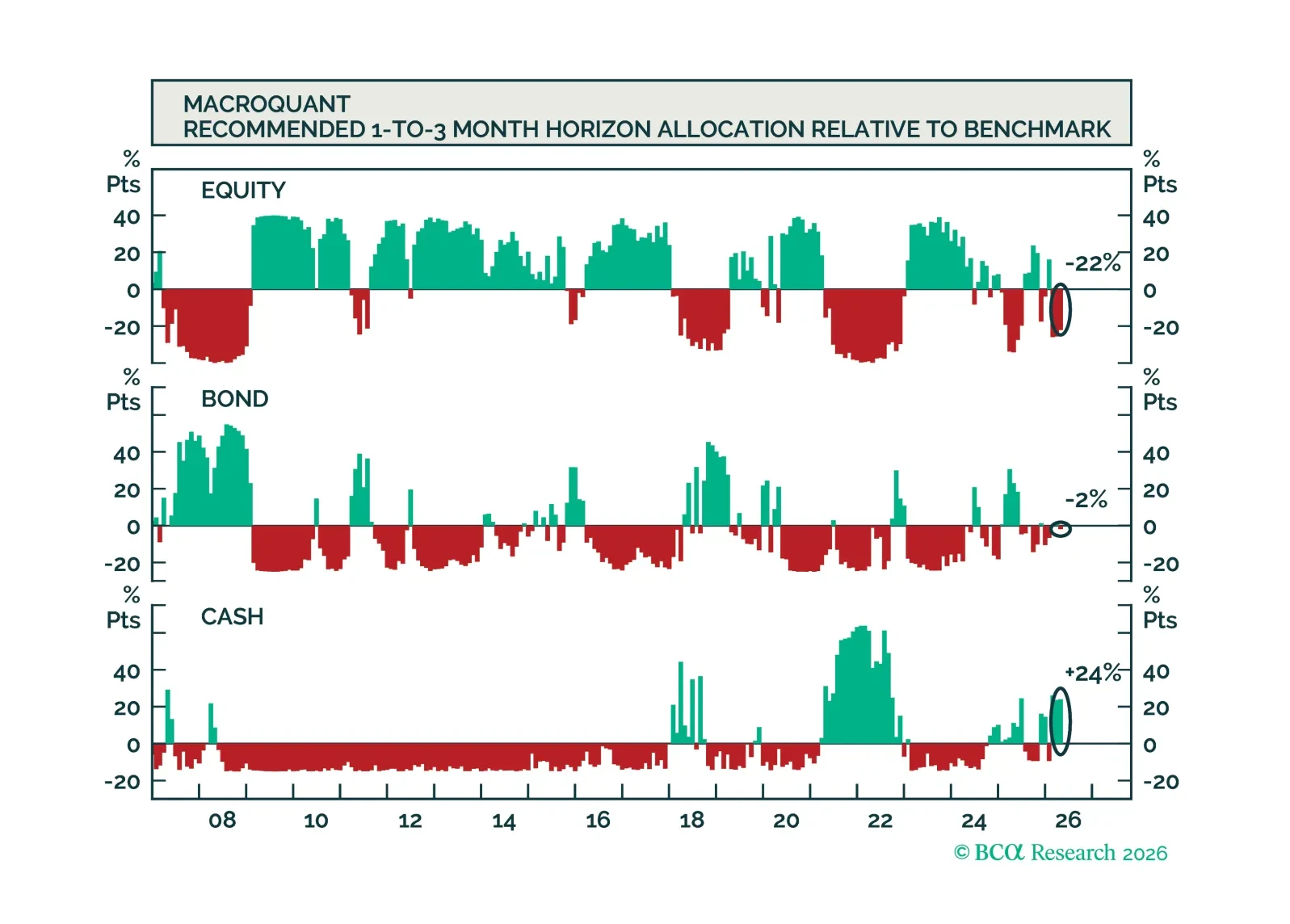

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

Against the earnings-versus-everything-else market backdrop, stellar earnings are easily outweighing elevated oil prices, rising yields and the increased probability that the Fed may hike rates before the year is out. US allocators should remain invested in equities.