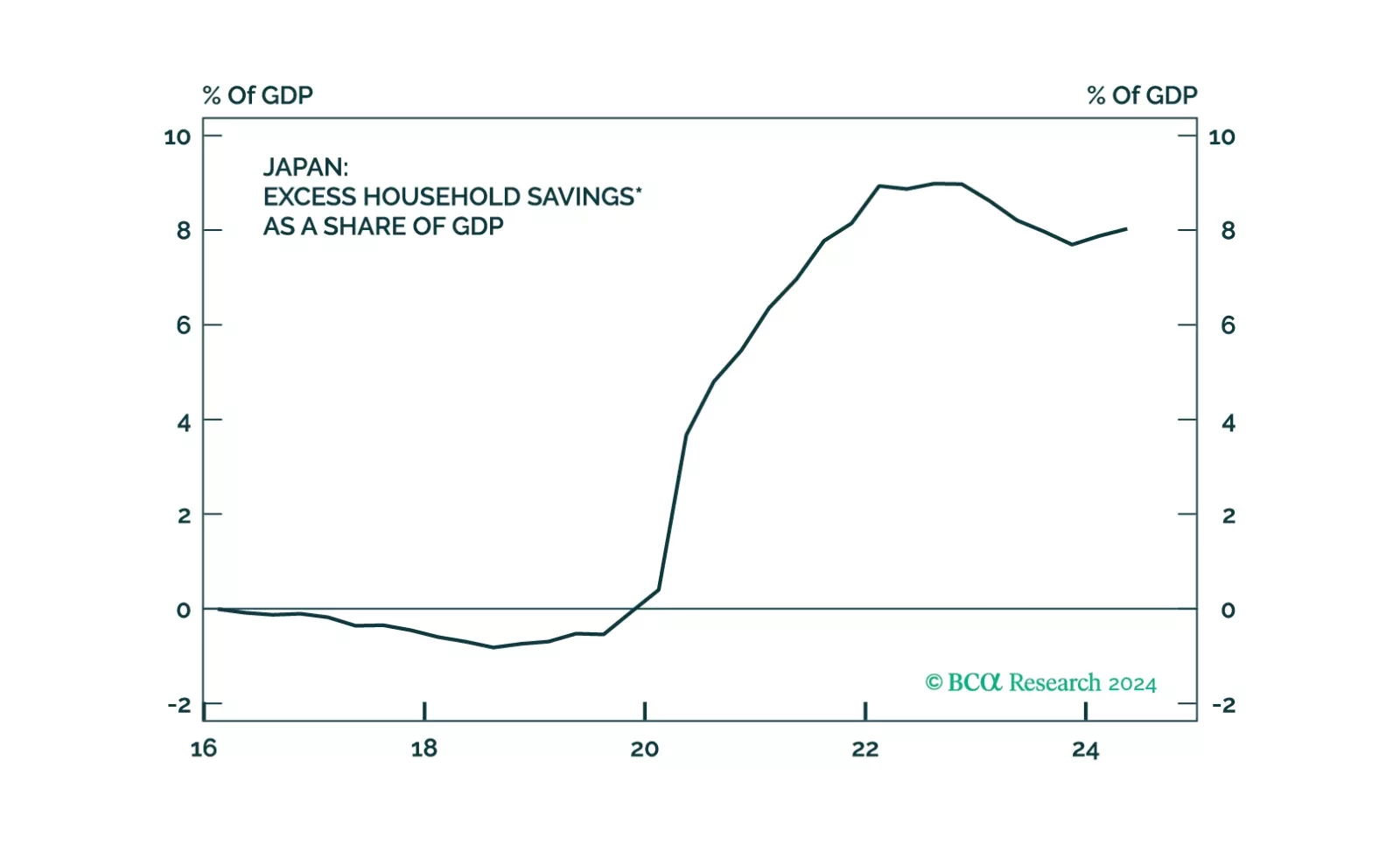

Money/Credit/Debt

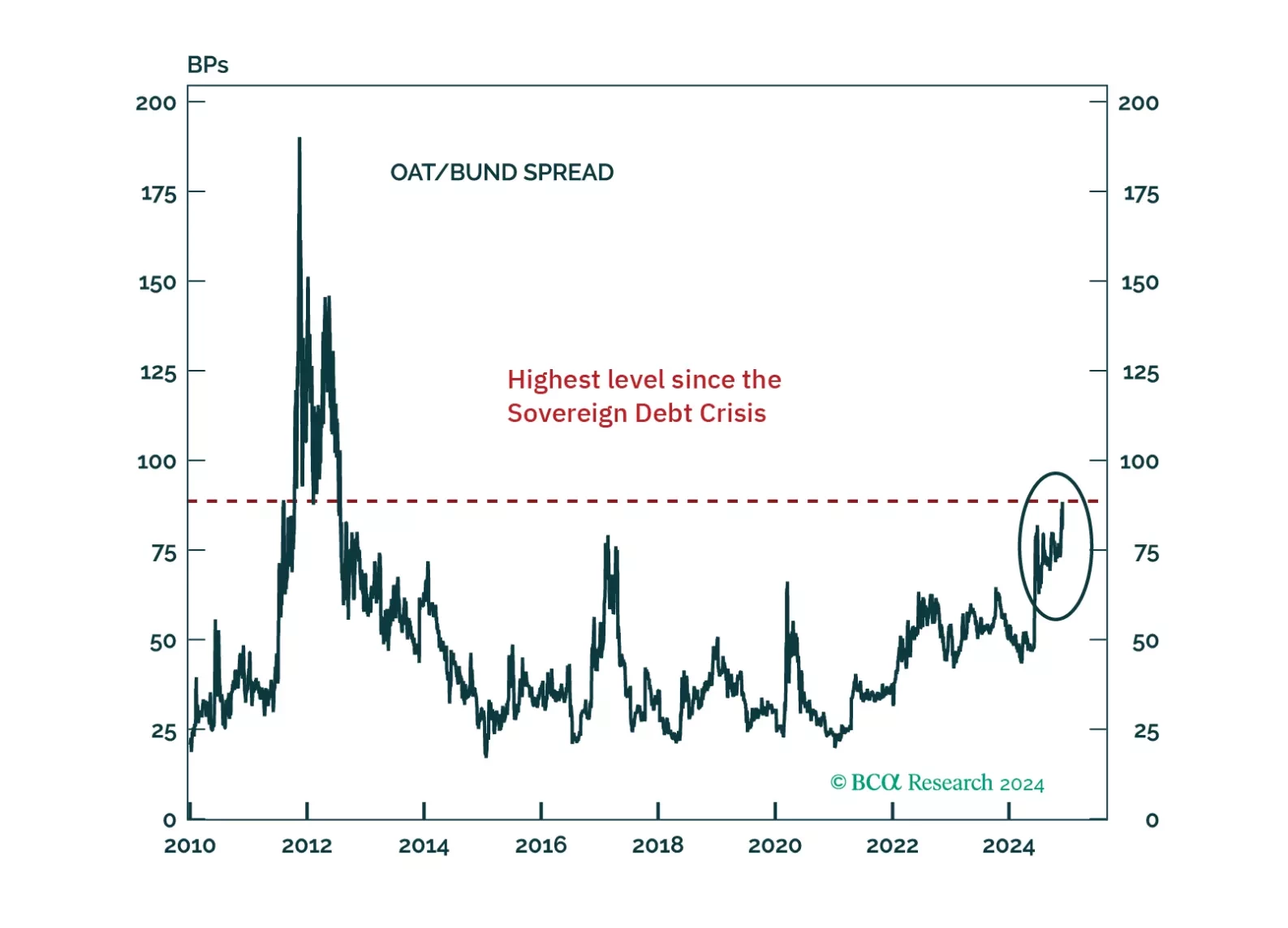

France finds itself in a unique, thorny situation. Can it heave itself out of it? And what does it mean for investors?

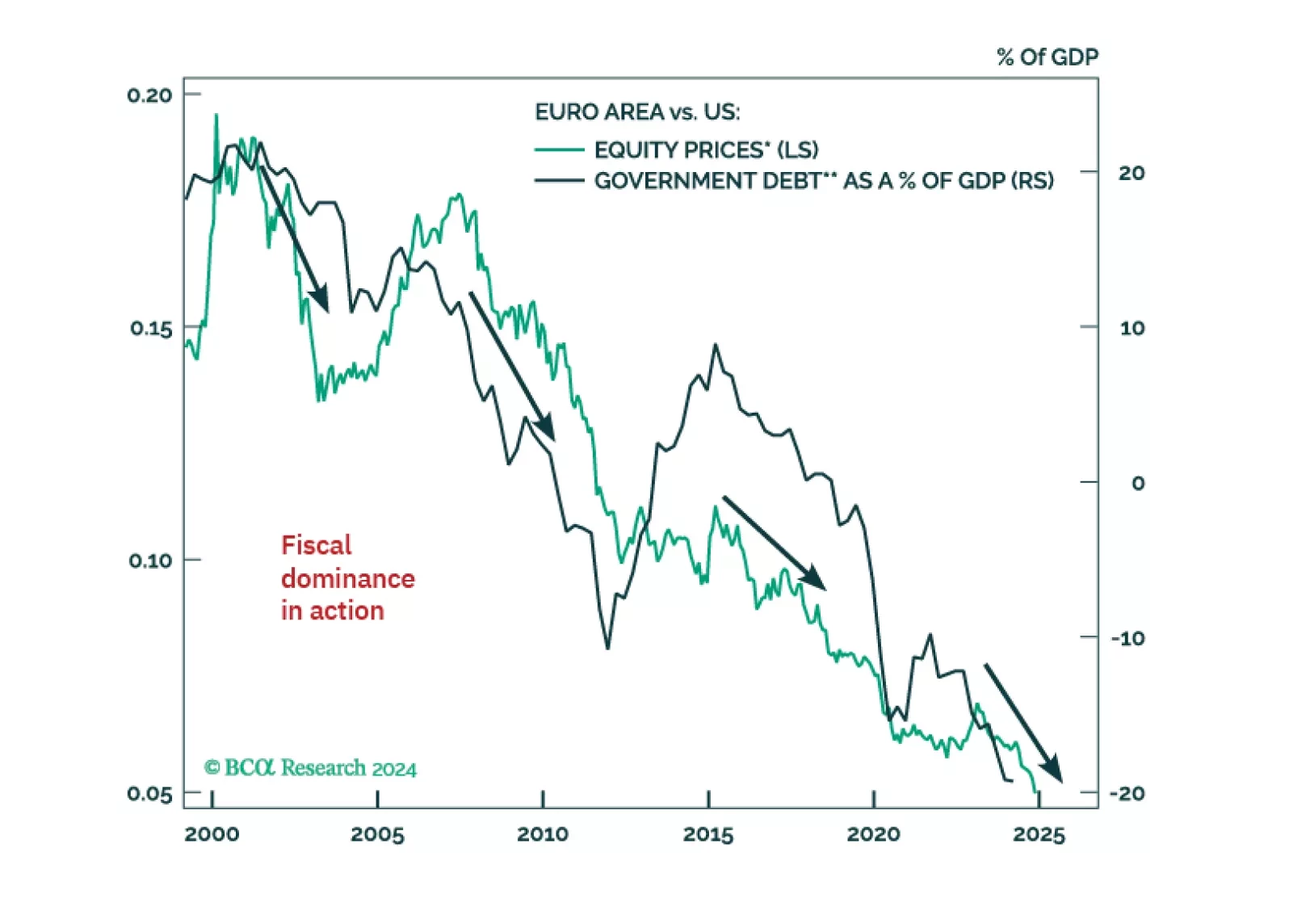

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

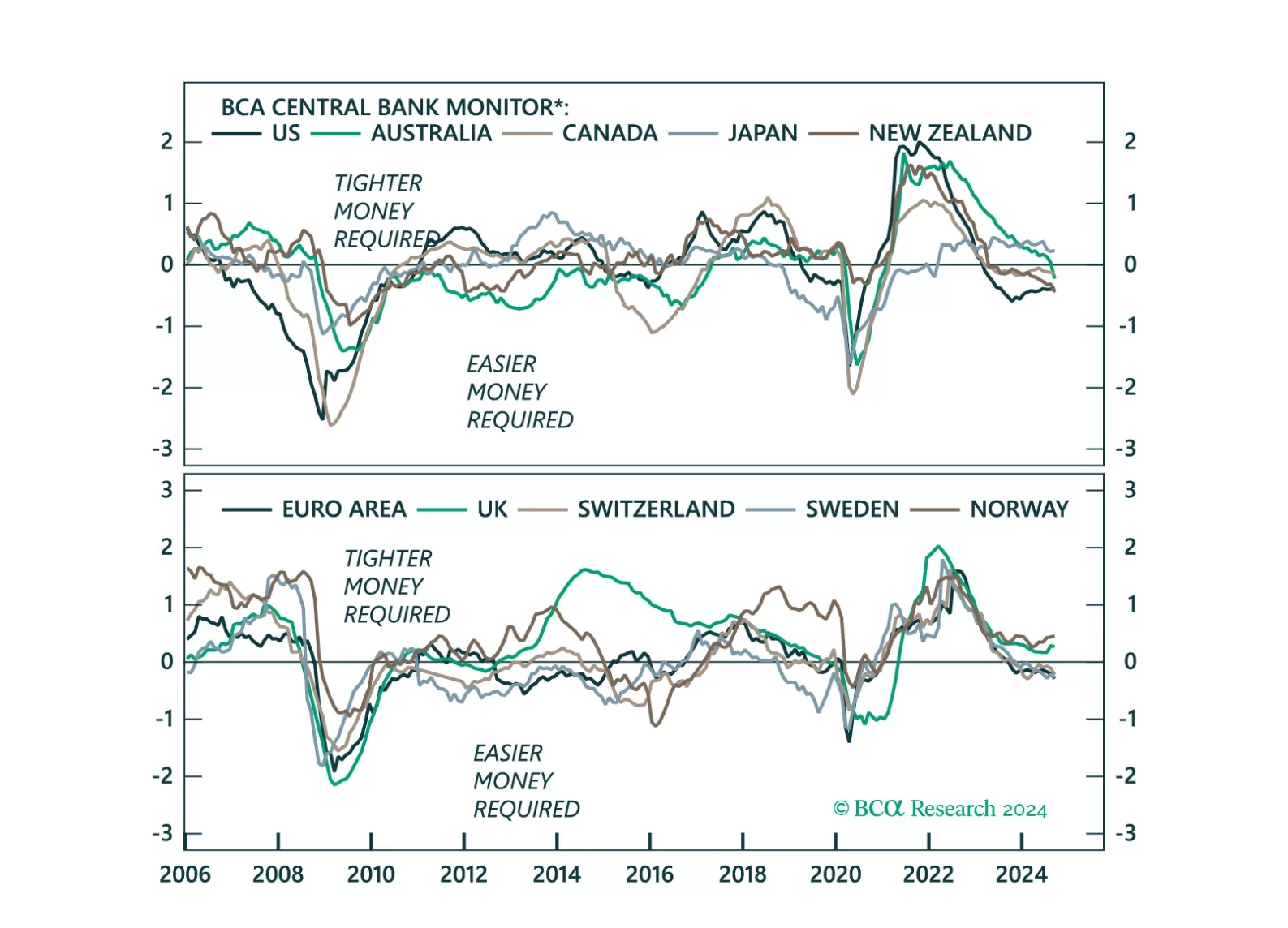

This week, we update our Central Bank Monitors (CBMs), that help us calibrate how monetary policy should be adjusted in developed-market economies. Our conclusion is that while overall, easier monetary settings are required, there a few trade ideas that arise from the divergences in signals amongst G10 countries.

The force of the post-election momentum leads us to believe we could be stopped out of our defensive positioning before the week is out, but we still believe in our recession call. If we are eventually stopped out, we will seek a more opportune entry point to bet against risk assets once the election fever runs its course.

The latest Bank of Japan meeting did not alter our high-conviction views of being long the yen and underweight JGBs.

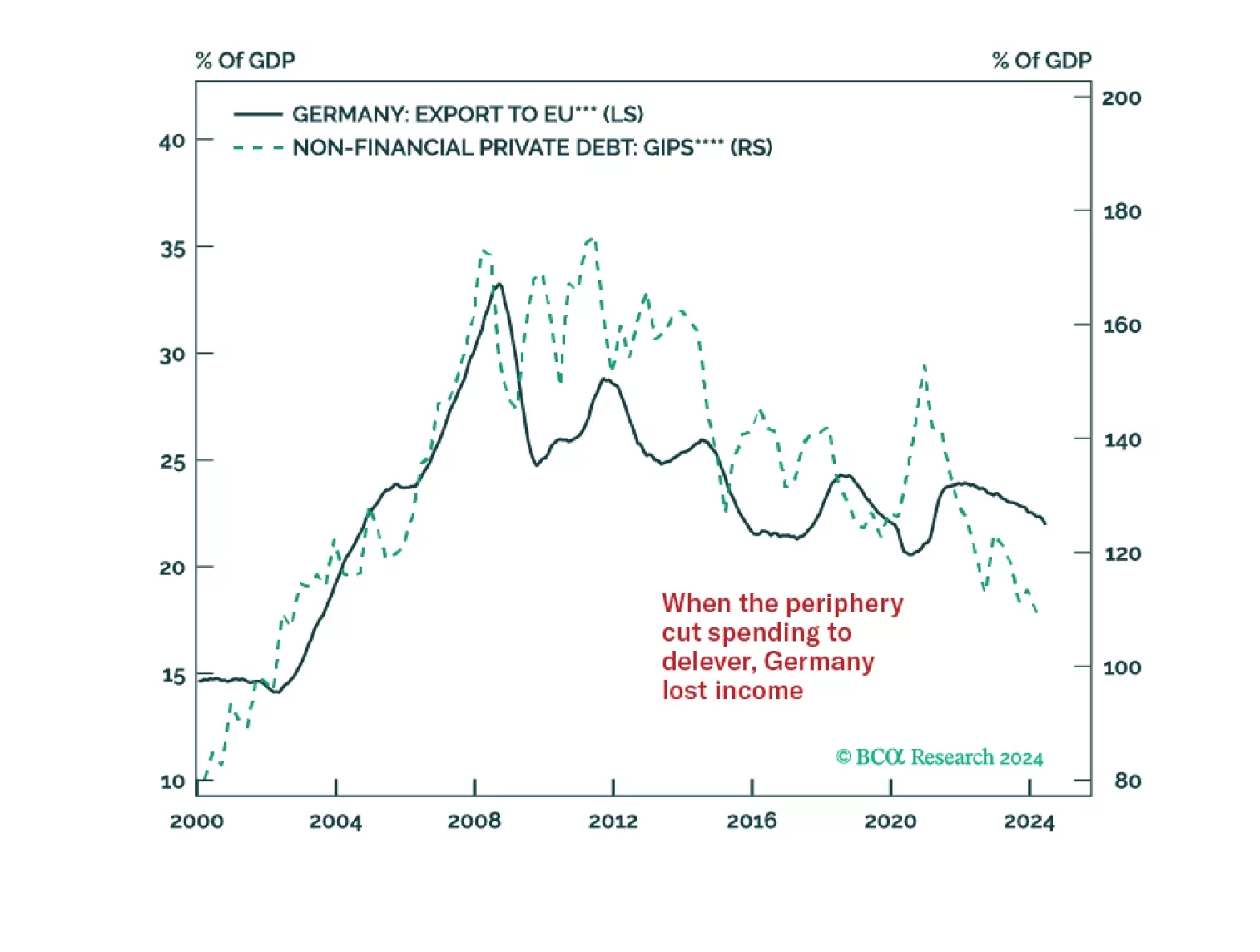

Germany’s economy has lagged that of the rest of Europe for nearly 10 years. So have German stocks. Investors are extrapolating these trends to bet on the country’s deindustrialization. Could Germany manage to beat dismal expectations?

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.