Money/Credit/Debt

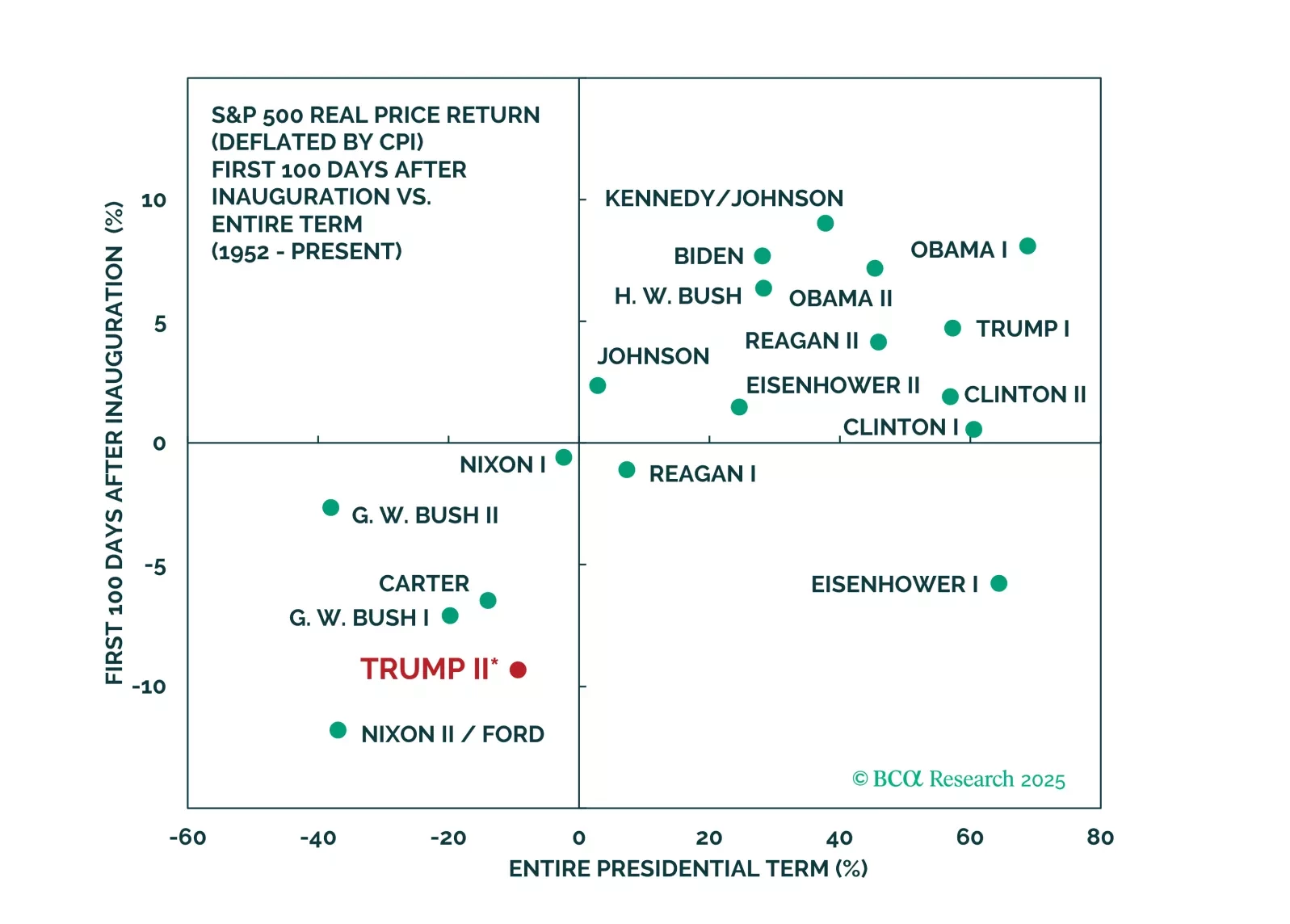

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

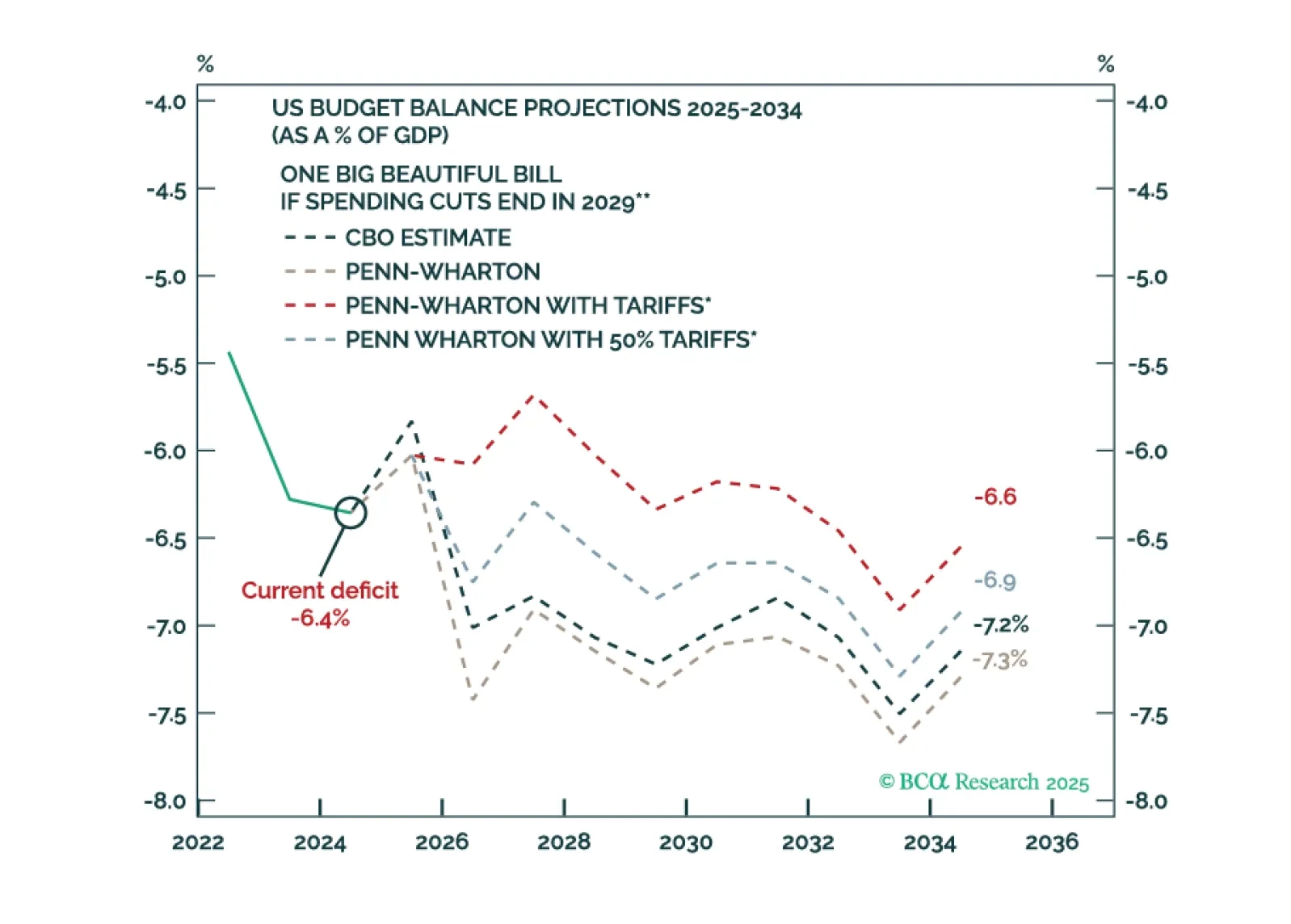

Bond market volatility will spike again in the near term. The Fed is committed to an easing cycle yet the Trump administration’s signature fiscal policy action will stimulate the economy. Tariffs are supposed to keep the budget deficit contained but they are inflationary.

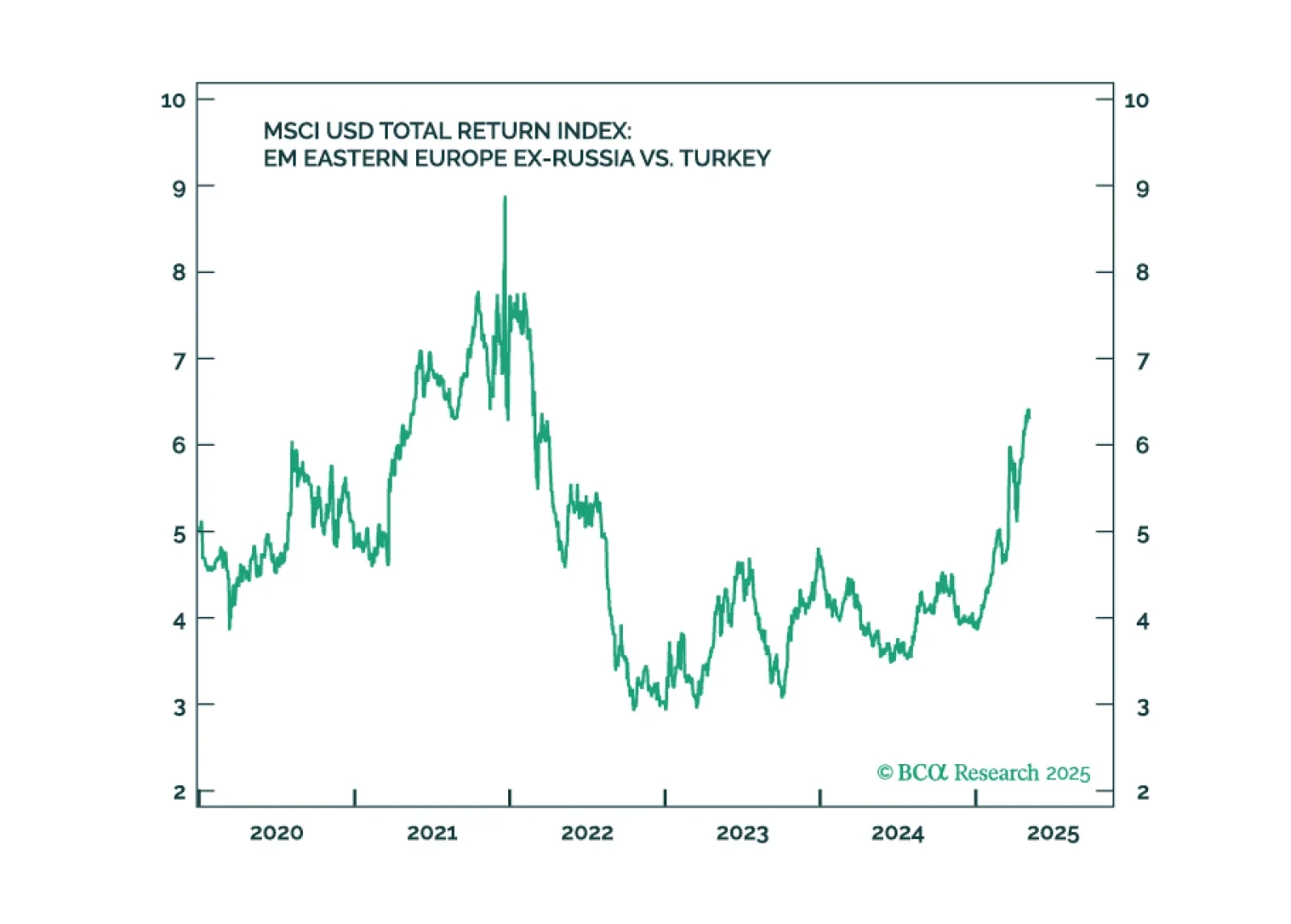

Erdogan's rule continues to decline. Social unrest will persist, governance will erode, and the macro backdrop will deteriorate further. We recommend underweighting Turkish assets.

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.