Monetary Policy

The Riksbank left rates unchanged and is likely to stay on hold, as soft inflation and weaker growth leave little case for tightening. The policy rate was left at 1.75%, as expected, and the Riksbank signaled it will remain on hold in the near term. This…

The Bank of England’s latest Monetary Policy Report offers a clean framework for thinking through an oil shock and the appropriate policy response. The first channel is the direct effect of higher energy prices on inflation such as higher gas and utilities…

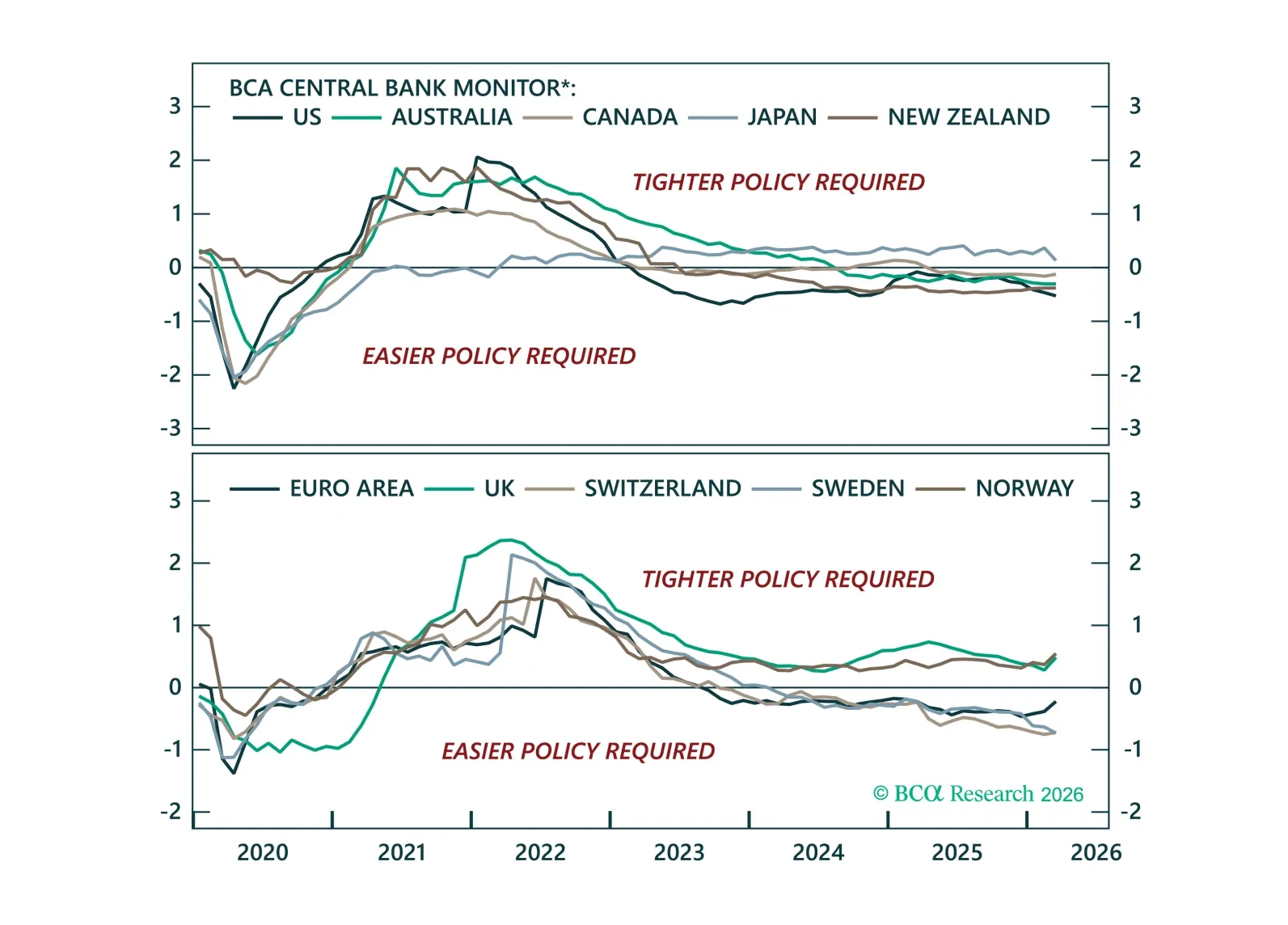

Central banks remain on hold amid heightened uncertainty. We rely on BCA’s Central Bank Monitors to assess the current policy stance of major central banks, and highlight the tactical opportunities across bond markets and currencies.

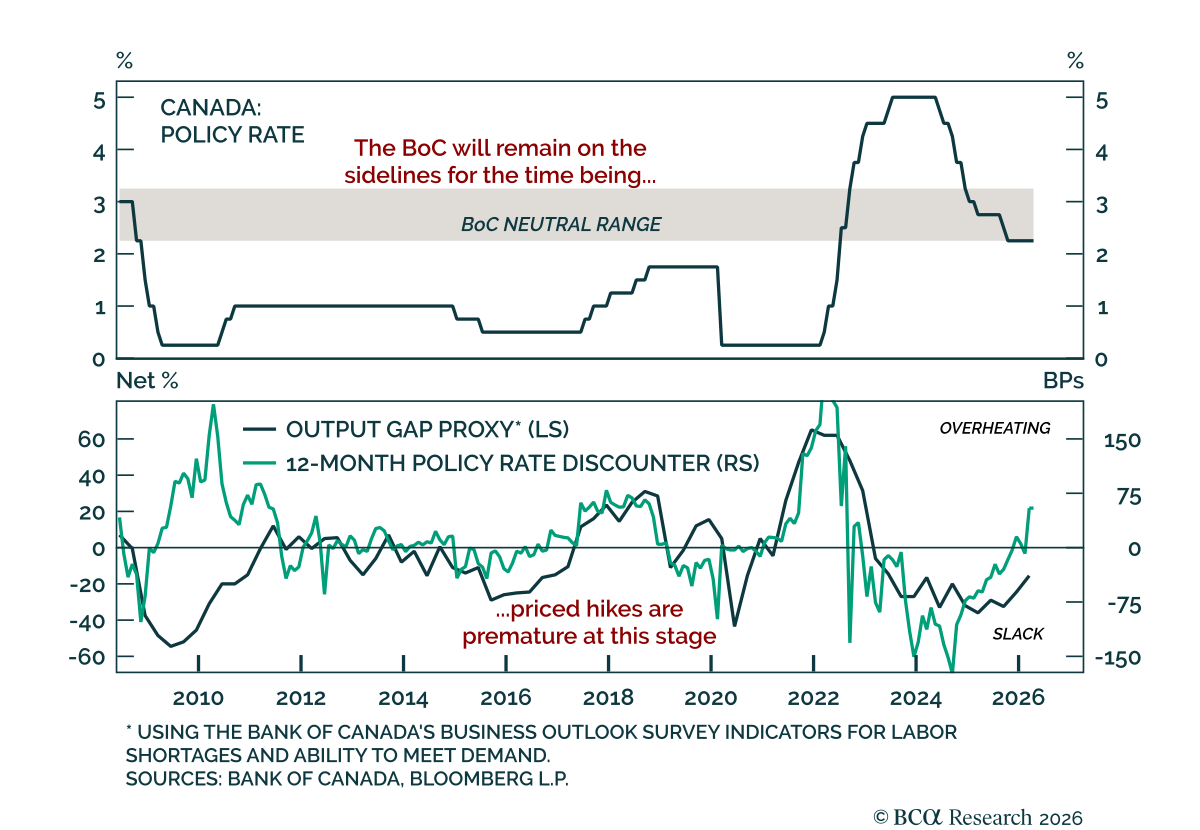

The Bank of Canada held rates at 2.25% for a fourth consecutive meeting; a weak domestic economy still argues for looking through supply-side inflation. The hold was expected, and at 2.25%, the policy rate sits at the bottom of the BoC’s estimated 2.25%-3.25%…

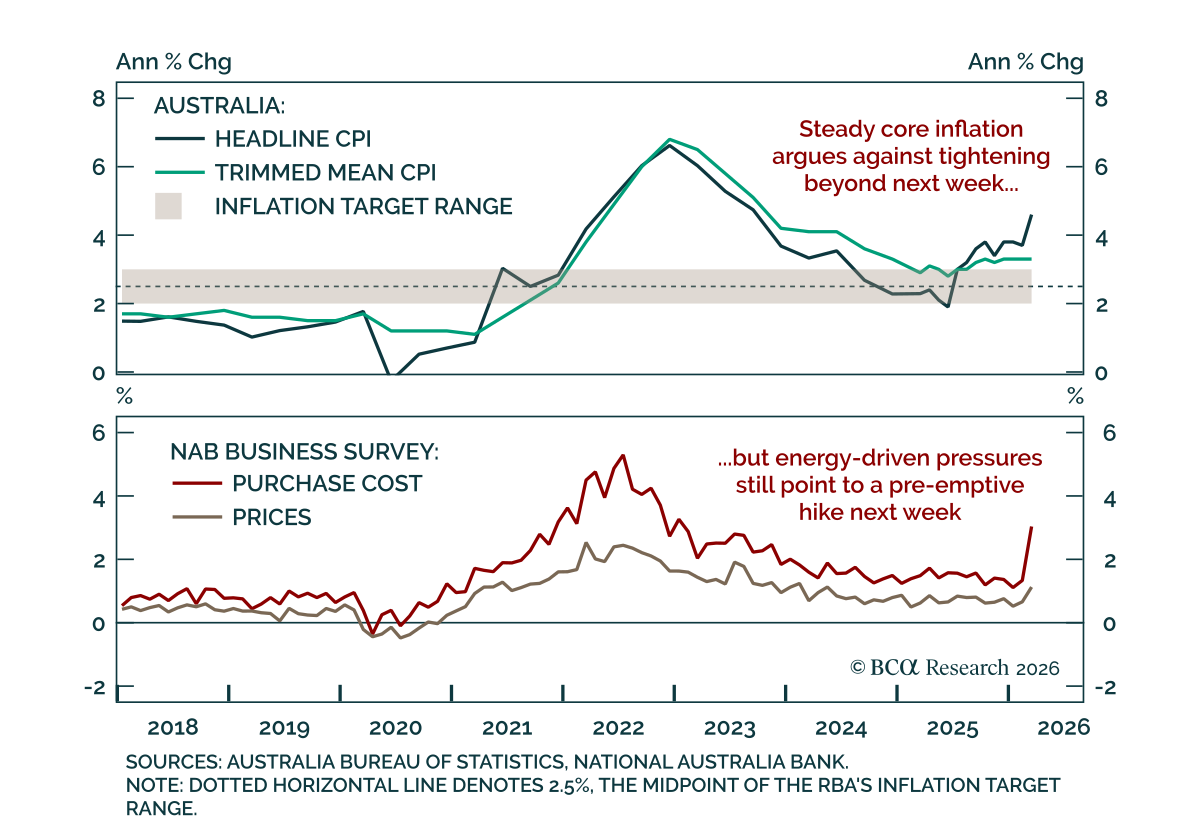

Australia's Q1 CPI showed energy-driven headline acceleration, but steady core inflation suggests markets are over-pricing RBA tightening. Headline inflation accelerated to 4.1% y/y (1.4% q/q) from 3.6% (0.6%), while the trimmed mean was largely unchanged at…

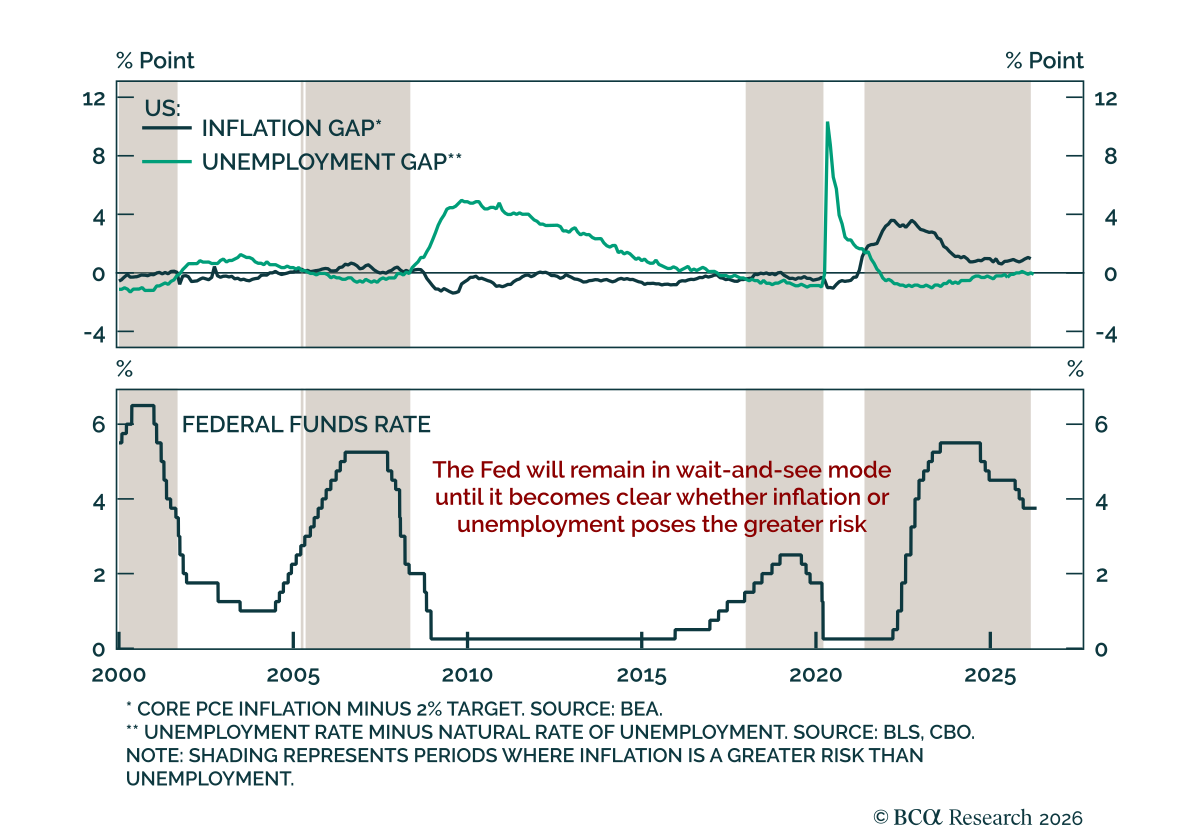

The Fed held rates for a third consecutive meeting and signaled no urgency to cut. The Fed left rates at 3.5-3.75%, with a 8-4 vote in favor of the relatively unchanged statement. Dissents were two-sided, with Governor Miran favoring a 25 bps cut, and…

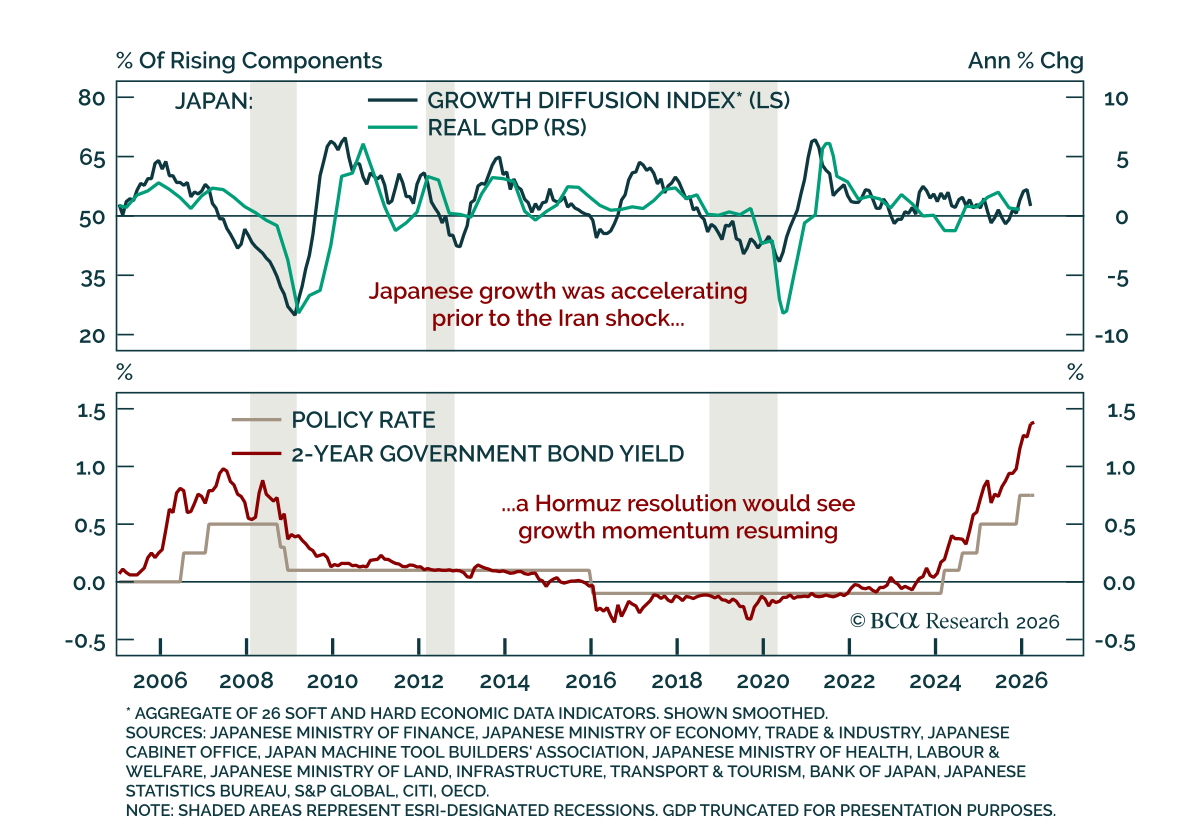

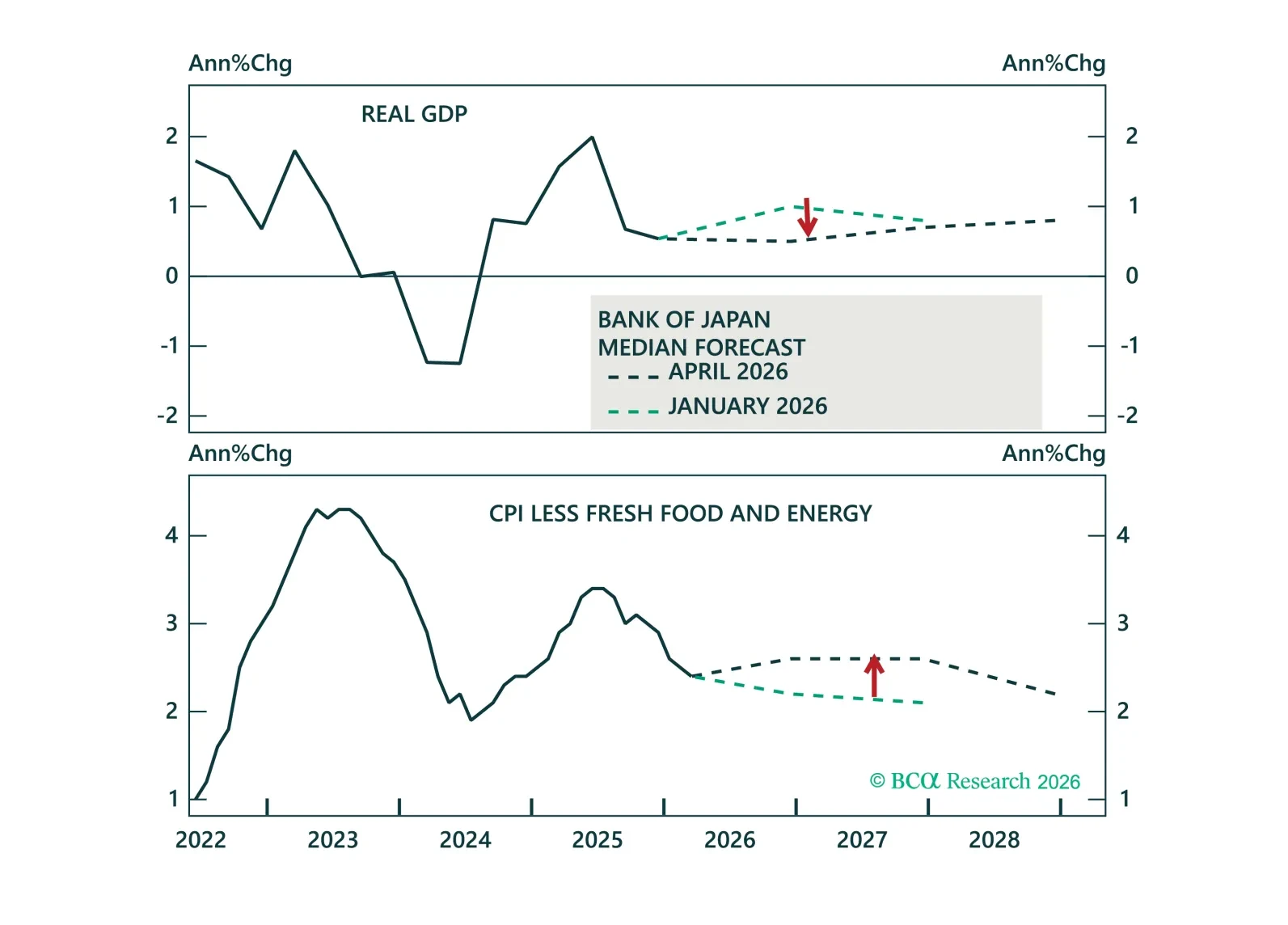

The Bank of Japan held rates at 0.75%, but the meeting still leaned hawkish. The hold was expected, but had a hawkish tone with 3 dissents in favor of a hike. That signal came alongside upward revisions to the BoJ’s inflation forecasts for 2026 and 2027, and…

The BoJ held rates overnight, but the direction of travel hasn’t changed. We discuss how stronger wages, rising inflation, and a weak yen point to further tightening ahead.

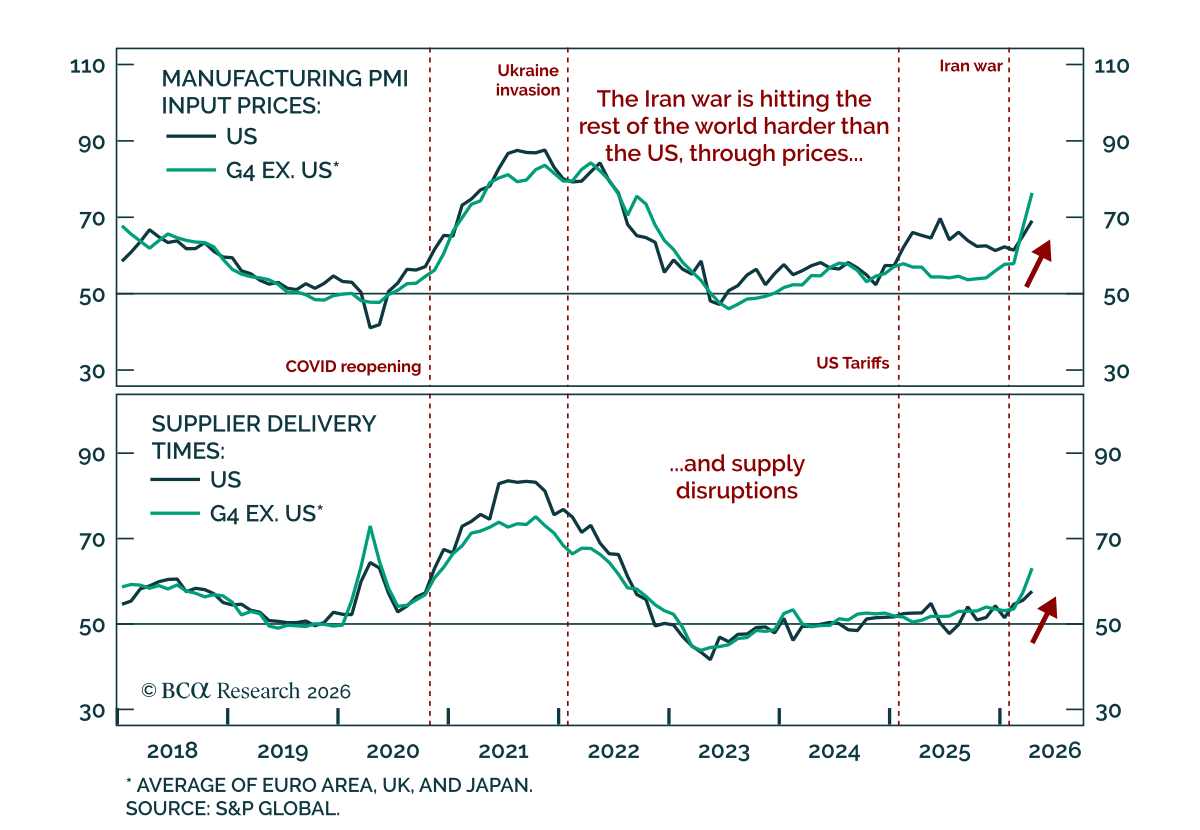

The April flash PMIs show that the global energy shock is feeding through unevenly, with sharper price pressures outside the US. Longer delivery times were widespread across developed markets, and input prices rose. One of our most timely tools for tracking…

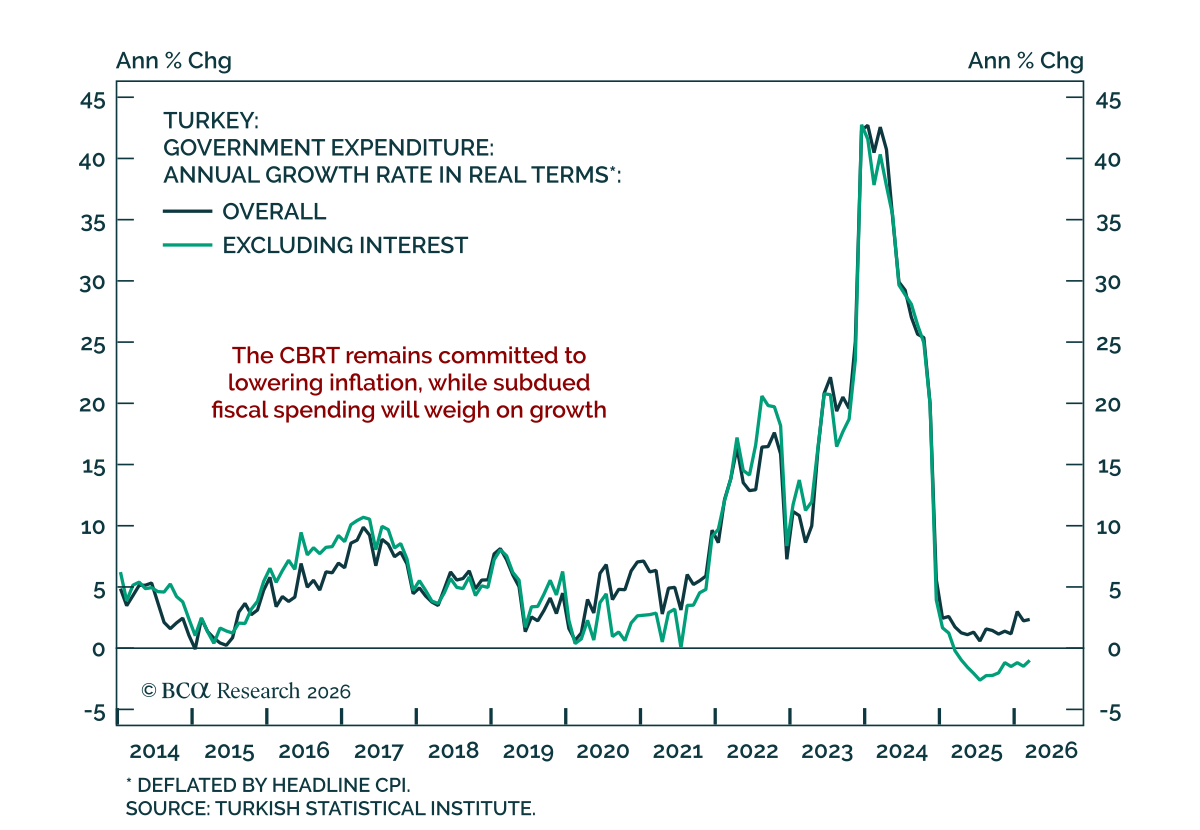

The Turkish Central Bank held rates at 37% this week, in line with expectations. While the energy shock may halt disinflation and delay near-term CBRT easing, the structural background remains disinflationary. An easing pause coupled with a slowing domestic…