Monetary Policy

The JPY’s decline reflects rising inflation expectations rather than fiscal risk, and is likely to persist until the BoJ turns more hawkish. Our Chart Of The Week comes from Mathieu Savary, Chief FICC Strategist. Mathieu examines the JPY’s decoupling from…

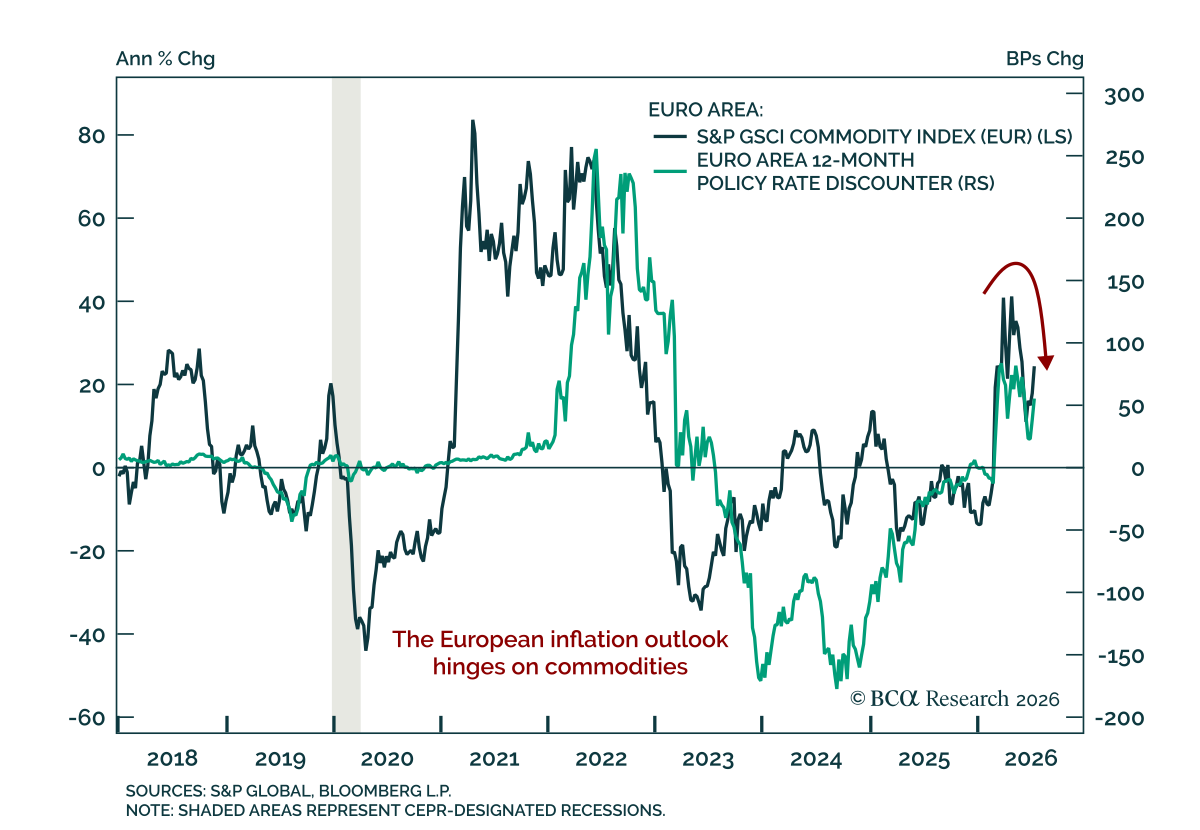

The ECB held rates at 2.25%, but kept the door open to further tightening in a near-term outlook still heavily shaped by energy prices. The hold was expected, but the ECB also signaled that every meeting remains upside risks to inflation, especially as the…

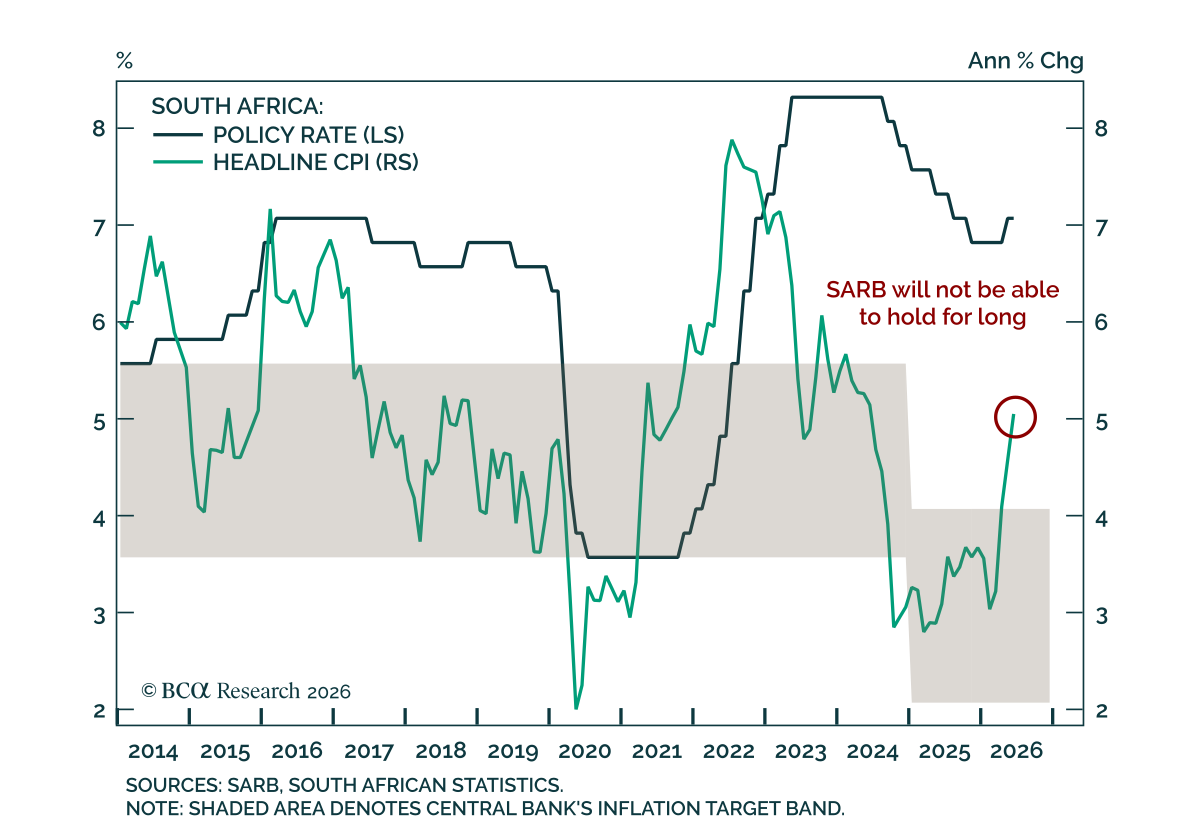

The South African Reserve Bank will not be able to hold rates for long. The SARB held its policy rate at 7%, defying expectations for a 25 bps hike. With inflation reaccelerating above the target band, our Emerging Markets strategists believe policymakers…

A more aggressive BoJ hiking stance is needed to stabilize the JPY. Recent price action has fueled speculation that Japanese officials now see yen weakness as an inflation risk, and that the BoJ may be open to accelerate the pace of hiking. Verbal…

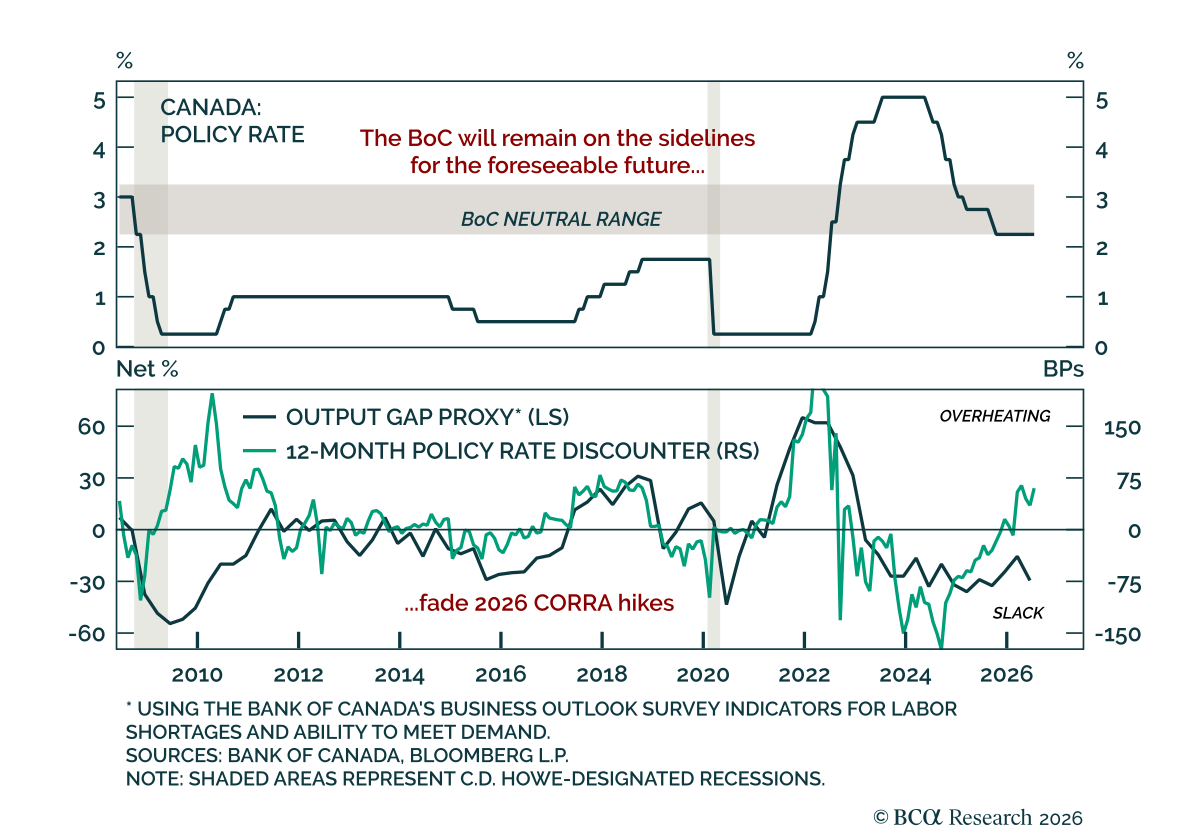

The Bank of Canada held rates, reinforcing its intention to stay on hold in the near term. The BoC kept rates unchanged for a sixth consecutive meeting, as expected. It also removed references to both cuts and hikes from its press release, reinforcing its…

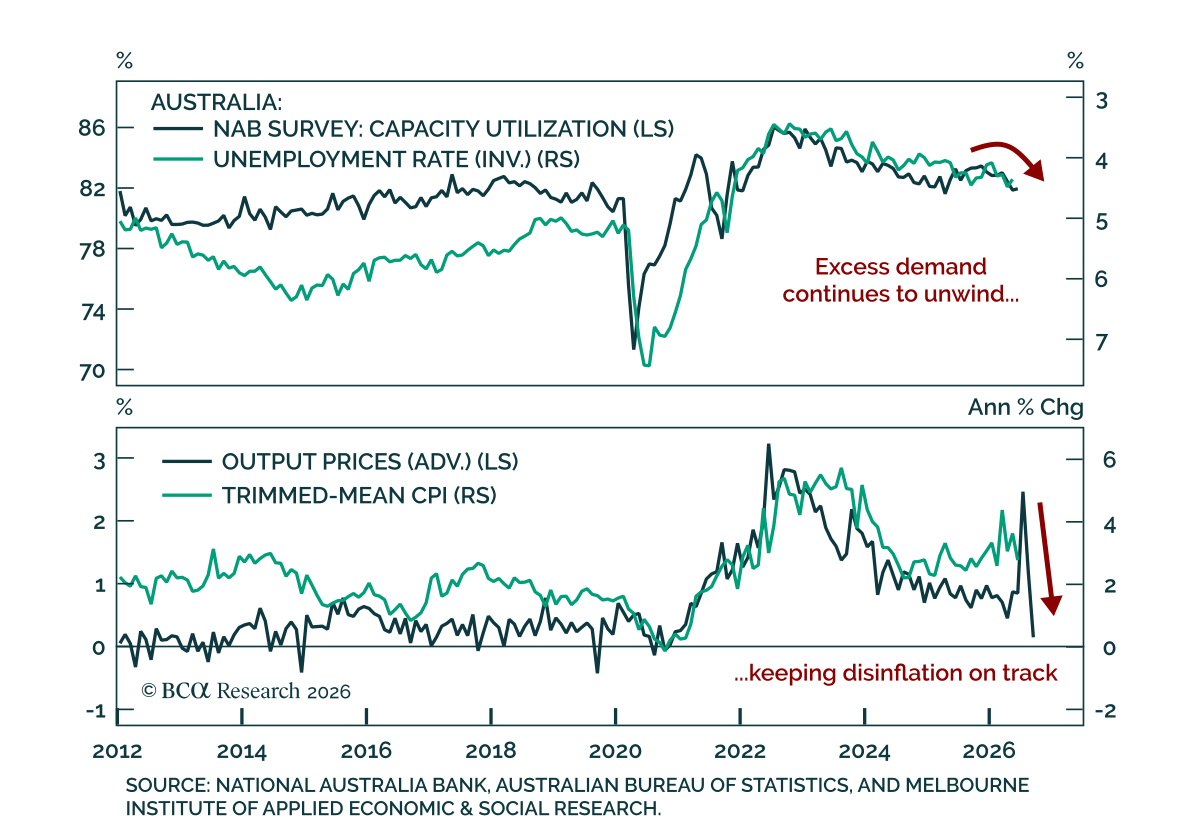

Australia's June NAB Business Survey points to a cooling economy, reinforcing the case for an extended RBA pause. Business conditions held at +3 for a third consecutive month, while business confidence, the more forward-looking measure, rebounded from -14 to…

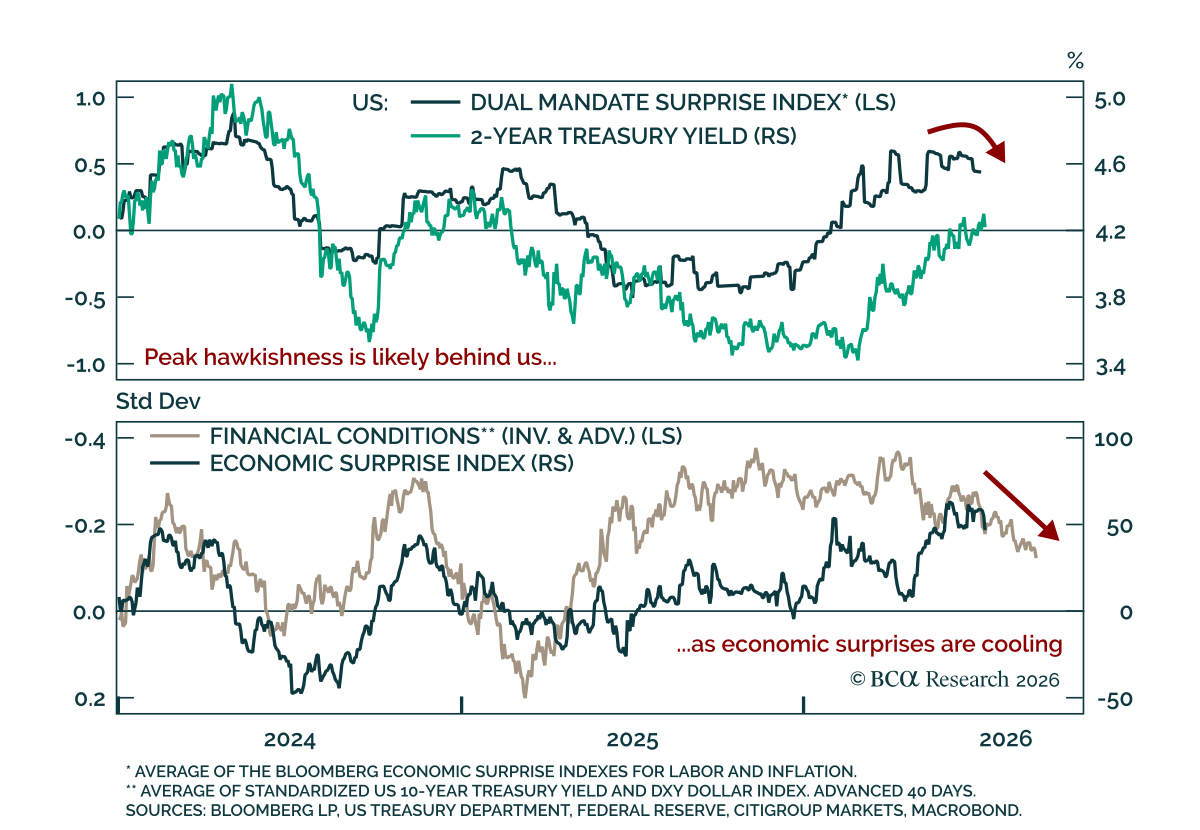

Rolling economic surprises support the view that peak Fed hawkishness is behind us. As the last few major reports have shown, including June employment, CPI, and ISM Manufacturing, economic surprises appear to be rolling over. That supports our thesis that…

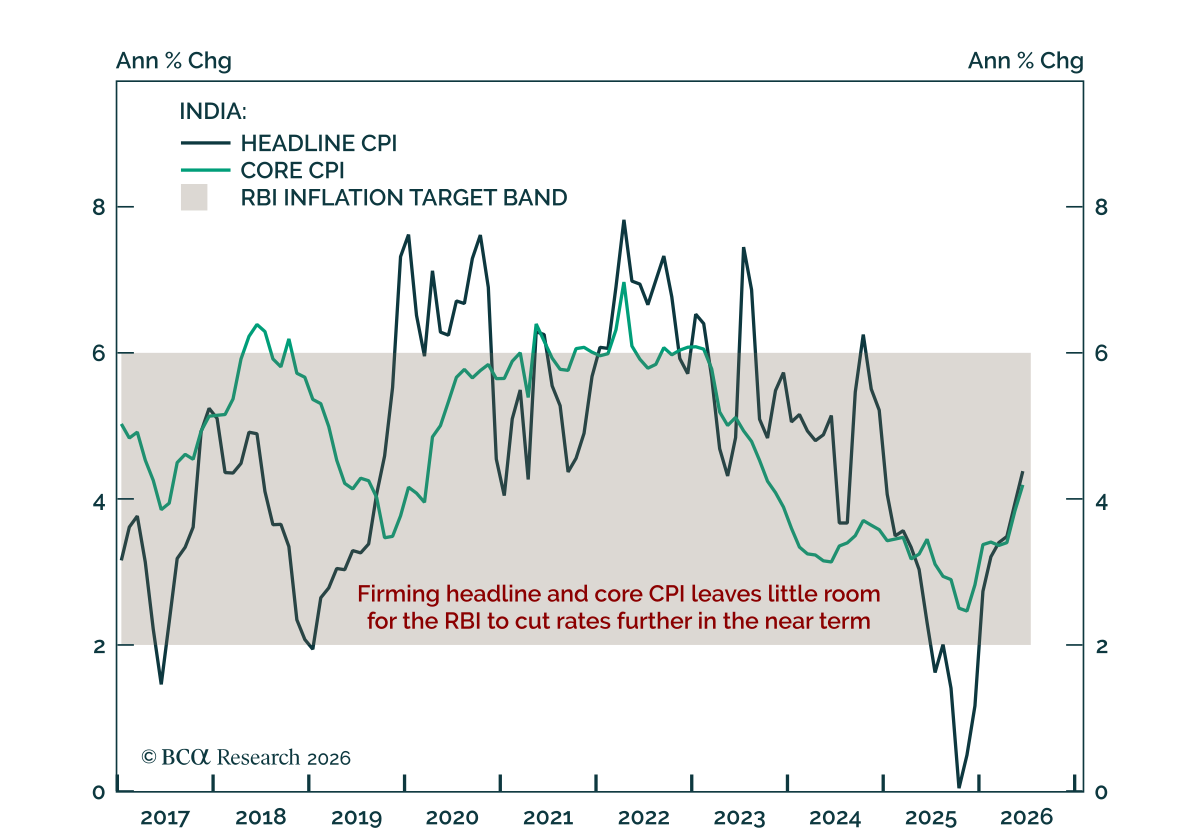

Indian headline CPI rose to 4.4%, limiting the RBI’s scope to ease and creating a less supportive backdrop for Indian assets. The increase pushed inflation above the RBI’s 4% target, though it remains within the tolerance band. Higher fuel and food prices…

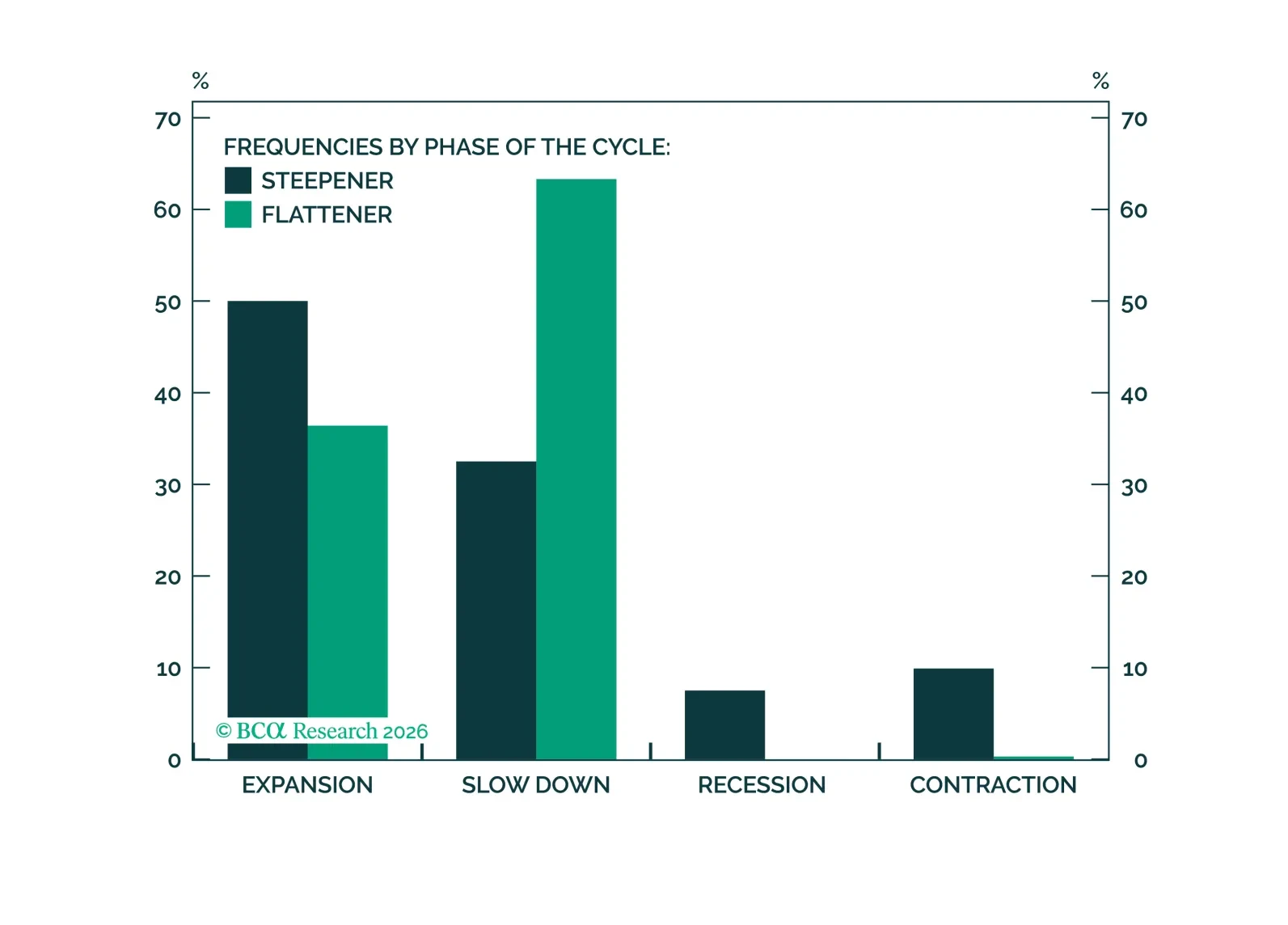

History suggests that the equity impact of rate moves depends heavily on the stock/bond correlation regime, and today’s positive correlation regime leaves the bond market as the main risk to equity multiples.

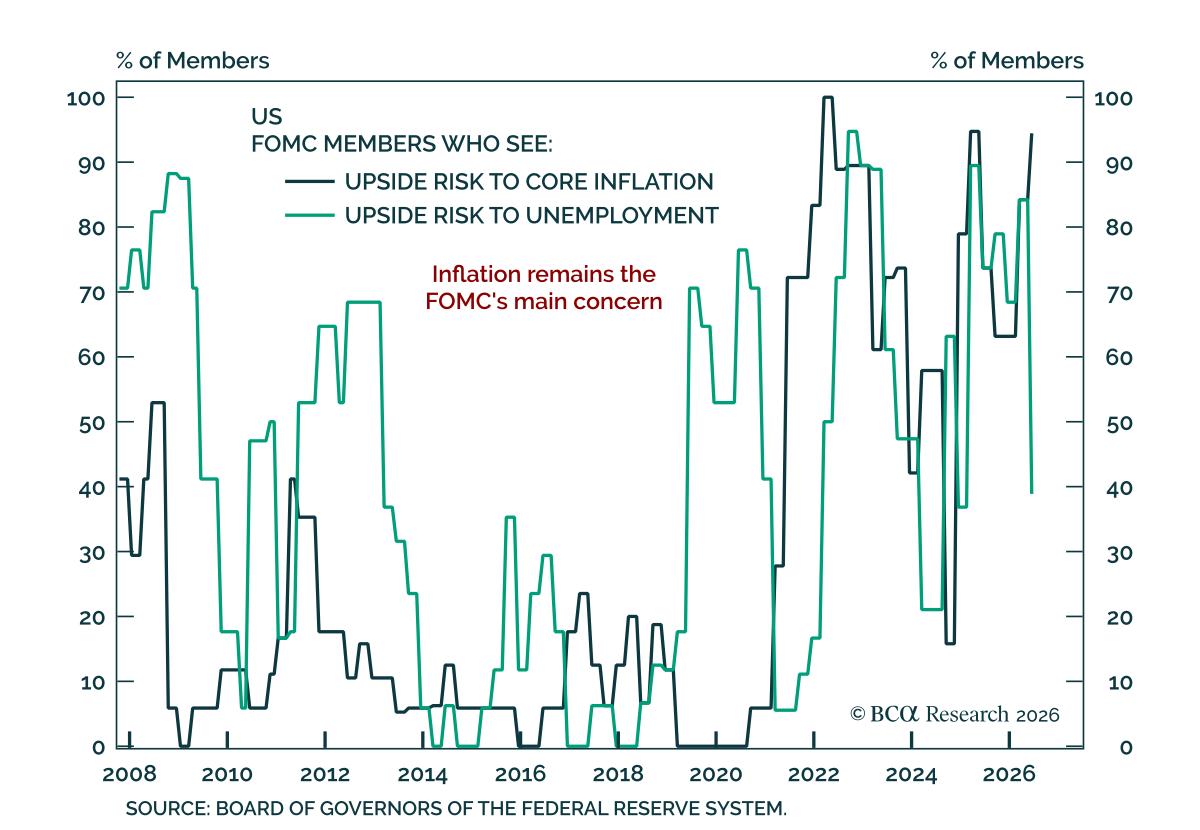

The June FOMC minutes showed broad agreement on the Fed’s reaction function, but uncertainty over the inflation path. The minutes were the first released under Chairman Warsh’s leadership. The minutes showed broad agreement on the reaction function across…